00015177679/30falseN-2xbrli:pureiso4217:USDiso4217:USDxbrli:shares00015177672023-10-012024-09-300001517767ck0001517767:A8.75SeriesATermPreferredSharesMember2024-09-300001517767ck0001517767:A8.75SeriesATermPreferredSharesMember2023-10-012024-09-300001517767ck0001517767:A7.125SeriesBConvertiblePreferredSharesMember2024-09-300001517767ck0001517767:PortfolioFairValueRiskMember2023-10-012024-09-300001517767ck0001517767:PotentialConflictsOfInterestRiskMember2023-10-012024-09-300001517767ck0001517767:CollateralizedLoanObligationsRiskMember2023-10-012024-09-300001517767ck0001517767:CovenantLiteLoansRiskMember2023-10-012024-09-300001517767ck0001517767:SubordinatedSecuritiesRiskMember2023-10-012024-09-300001517767ck0001517767:HighYieldInvestmentRiskMember2023-10-012024-09-300001517767ck0001517767:DefaultRiskMember2023-10-012024-09-300001517767ck0001517767:NonDiversificationRiskMember2023-10-012024-09-300001517767ck0001517767:LeverageRiskMember2023-10-012024-09-300001517767ck0001517767:SeniorManagementPersonnelRiskMember2023-10-012024-09-300001517767ck0001517767:ConflictsOfInterestRiskMember2023-10-012024-09-300001517767ck0001517767:LiquidityRiskMember2023-10-012024-09-300001517767ck0001517767:TheAdvisersIncentiveFeeRiskMember2023-10-012024-09-300001517767ck0001517767:MarketRisksMember2023-10-012024-09-300001517767ck0001517767:InflationRiskMember2023-10-012024-09-300001517767us-gaap:InterestRateRiskMember2023-10-012024-09-300001517767ck0001517767:RegulatoryRiskMember2023-10-012024-09-300001517767us-gaap:CreditRiskContractMember2023-10-012024-09-300001517767ck0001517767:CreditSpreadRiskMember2023-10-012024-09-300001517767us-gaap:PrepaymentRiskMember2023-10-012024-09-300001517767ck0001517767:VolatilityRiskMember2023-10-012024-09-300001517767ck0001517767:EquityRiskMember2023-10-012024-09-300001517767ck0001517767:ForeignExchangeRateRiskMember2023-10-012024-09-300001517767ck0001517767:CybersecurityRiskMember2023-10-012024-09-300001517767ck0001517767:A7.125SeriesBConvertiblePreferredSharesMember2023-10-012024-09-3000015177672021-12-3100015177672021-10-012021-12-3100015177672022-03-3100015177672022-01-012022-03-3100015177672022-06-3000015177672022-04-012022-06-3000015177672022-09-3000015177672022-07-012022-09-3000015177672022-12-3100015177672022-10-012022-12-3100015177672023-03-3100015177672023-01-012023-03-3100015177672023-06-3000015177672023-04-012023-06-3000015177672023-09-3000015177672023-07-012023-09-3000015177672023-12-3100015177672023-10-012023-12-3100015177672024-03-3100015177672024-01-012024-03-3100015177672024-06-3000015177672024-04-012024-06-3000015177672024-09-3000015177672024-07-012024-09-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-22554

Carlyle Credit Income Fund

(Exact Name of Registrant as Specified In Its Charter)

One Vanderbilt Avenue, Suite 3400

New York, New York 10017

(Address of principal executive offices) (Zip Code)

Joshua Lefkowitz, Esq.

Chief Legal Officer, Carlyle Credit Income Fund

One Vanderbilt Avenue, Suite 3400

New York, New York 10017

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 813-4900

Date of fiscal year end: September 30

Date of reporting period: September 30, 2024

Item 1. Reports to Stockholders

The annual report to stockholders for the year ended September 30, 2024 is filed herewith pursuant to Rule 30e -1 under the Investment Company Act of 1940.

CARLYLE CREDIT INCOME FUND

ANNUAL REPORT

SEPTEMBER 30, 2024

Table of Contents

| | | | | |

| Section | Page |

| Year End 2024 Shareholder Letter | |

| Important Information about this Report and Carlyle Credit Income Fund | |

| Performance Data | |

| Summary of Certain Unaudited Portfolio Characteristics | |

| Fees and Expenses | |

| Statement of Assets and Liabilities | |

| Schedule of Investments | |

| Statement of Operations | |

| Statements of Changes in Net Assets | |

| Statement of Cash Flows | |

| Financial Highlights | |

| Notes to Financial Statements | |

| Results of Shareholder Meeting | |

| Report of Independent Registered Public Accounting Firm | |

| Price Range of Common Shares | |

| Dividend Reinvestment Plan | |

| Management of the Fund | |

| Portfolio Proxy Voting Policies and Proxy Voting Record | |

| Additional Information | |

ANNUAL 2024 SHAREHOLDER LETTER

FUND REVIEW & DISCUSSION OF PERFORMANCE

On November 20, 2024, Carlyle Credit Income Fund (“we,” “us,” “our,” “CCIF” or the “Fund”) (NYSE: CCIF) announced via press release the financial results for the fourth quarter ending September 30, 2024. Over the past year, the Fund has successfully implemented the following:

•Constructed a diversified portfolio of 49 unique collateralized loan obligation (“CLO”) investments managed by 27 different collateral managers with exposure to 1,916 separate loans. The weighted average GAAP yield of the portfolio is 18.63% as of September 30, 2024.

•We increased the monthly dividend to $0.1050 per common share in March 2024. We have maintained this dividend and it is declared through February 2025. This equates to a 15.2% annualized dividend rate based on the share price as of November 19, 2024.

•We have grown the Fund through accretive issuance of common equity and flexible long-term preferred capital to leverage the Fund:

◦We implemented an at-the-market (“ATM”) offering program to issue common shares at a premium to net asset value (“NAV”) for net proceeds of $16.8 million through September 30, 2024.

◦We leveraged the Fund through the issuance of 8.75% Series A Term Preferred Stock due 2028 with a total of $52 million.

◦We completed a private placement of 7.125% convertible preferred shares due 2029. Concurrently, we issued 1.4 million of our common shares through a registered direct placement at a price above the Fund’s NAV per common share. Total net proceeds from these offerings were approximately $22.2 million.

As of September 30, 2024, the NAV of the Fund is $7.64 per share.

We believe Carlyle has differentiated insights into the CLO market given its 15 year track record of CLO investing and team of over 30 credit analysts across the U.S. and Europe. Carlyle remains one of the largest CLO managers globally

with over $50 billion of AUM and $2.5 billion in third party managed CLO investments.1,2

MARKET REVIEW

Year-to-date (“YTD”) 2024, leveraged loan returns remain robust even as the market begins to anticipate the onset of the rate-cutting cycle. The LSTA U.S. Leveraged Loan Index (the “LSTA Index”) has returned 6.54% YTD, on track for one of the strongest years of performance over the past 10+ years.3 In late May, the LSTA Index reached a bid price of $96.99, which is its highest level since May 2022.3

Through October month-end, institutional gross loan issuance totals over $1 trillion, which will result in the highest annual amount on record.4 Over $500 billion of loans have been repriced YTD and borrowers have reduced spread by 50 basis points (“bps”) with each repricing, resulting in an overall spread decline of 20 bps in the loan market.4 However, excluding refinancings and repricings, new issue loan volume remains fairly muted including approximately $100 billion of leveraged buyout or M&A activity YTD.4

The CLO market experienced robust issuance activity amidst tightening spreads in global fixed income and a stable backdrop for credit. CLO new issue YTD totals $158.1 billion and may surpass 2021’s record $184.8 billion.5 The weighted average cost of debt for broadly syndicated loan (“BSL”) CLO issuance declined from 230 bps in Q3 2023 to 176 bps in Q3 2024.5 As a result, volumes for CLO refinancings, which reduce a CLO’s financing costs, and resets, which typically extend a CLO’s reinvestment period (“RP”) to a fresh 5 years, have surged. YTD CLO refinancing and reset activity of $65.8 billion and $166.9 billion, respectively, have surpassed full-year 2023 volumes of $5.0 billion and $19.6 billion.5 CLO reset activity remains on record annual pace, including record monthly volumes in August of $26.2 billion.5 Within CCIF’s portfolio, we continue to work with CLO managers and have completed 7 resets YTD, extending the RP, and cash flows, of these CLOs.6

From a fundamental perspective, U.S. loan borrowers have remained resilient. As a proxy for third-party managed CLOs, the 600+ borrowers in Carlyle’s U.S. loan portfolio have continued to focus on free cash flow generation. Q2 2024 borrower EBITDA growth of 9.0% has outpaced revenue growth of 5.4%.2 Furthermore, the average interest coverage ratio (“ICR”) of borrowers increased quarter-over-quarter to 3.3x and approaches the historical average

1 Creditflux as of September 30, 2024.

2 Carlyle Internal Sources as of June 30, 2024.

3 Leveraged Commentary & Data (“LCD”) as of September 30, 2024.

4 LevFin Insights as of October 31, 2024.

5 Citi Research as of October 31, 2024.

6 CCIF Portfolio as of September 30, 2024.

of 3.9x.2 Notably, in-court and out-of-court bankruptcy activity continue to diverge. While the LSTA Index LTM default rate of 0.80% remains less than half of its 20-year average, the default rate inclusive of distressed exchanges (“DEs”) remains higher at 3.70%.7 Carlyle continues to leverage the insights of its dedicated Special Credits Group and over 30 credit analysts when evaluating loan borrowers in third-party managed CLO portfolios, evidenced by a CCIF portfolio default rate of 1.54% inclusive of DEs, which is less than half of the market’s rate.6

CLO liquidations have increased to $40 billion YTD 2024, driven by increasing net asset values and the elevated number of CLOs post-RP.8Additionally, CLO market amortization rates have remained elevated resulting in $60 billion of amortizations. With the combination of over $60 billion of amortizations and $40 billion of liquidations, the CLO market has experienced approximately $30 billion of growth YTD in 2024 despite the record issuance pace.5,8

CLO equity continues to produce attractive current yields as Q3 2024 cash-on-cash distributions averaged 4% based on par purchase price, in-line with the historical mid-to-high teens yield produced by CLO equity.9

STRATEGY & OUTLOOK

We remain pleased with the diversified portfolio that we have created allowing CCIF to pay a $0.1050 per share monthly dividend. Leveraged credit and broader economic conditions continue to support the health of the CLO equity market.

We believe investor sentiment will continue to remain strong for CLOs, evidenced by robust CLO creation following the Federal Reserve’s latest interest rate decision. Additionally, the forward interest rate curve and anticipated rate cuts may not reflect the strength of the U.S. economy based on Carlyle’s Chief Economist. Therefore, Carlyle has started to observe a market recalibration of rate expectations. Given CLO equity is modeled using a forward curve for base rates, current yields account for future rate cut predictions.

Based on trends of borrowers held within Carlyle-managed CLOs, we believe loan fundamentals will remain resilient. For example, only 3% of borrowers possess ICRs of less than 1.0x, an indicator of the ability to service existing debt.2 Furthermore, we continue to position CCIF’s portfolio defensively with higher quality managers and deals with enhanced structural subordination, as evidenced by the portfolio’s weighted average junior over-collateralization cushion of 4.33%.6

Due to record reset activity, the percentage of the U.S. CLO market out of RP has declined from 40% at the start

of 2024 to 33%, but still remains elevated compared to historical figures.8 CCIF’s portfolio only has 2 CLO positions outside of their RP, both of which were opportunistic purchases.6

While we anticipate that CLO amortization rates will moderate, we still think that investors will continue to redeploy proceeds in new issue CLOs in conjunction with liquidation activity. This could imply further tightening in CLO primary spreads which may benefit CLO equity. As such, we believe a number of CLO equity investment opportunities may emerge in the coming months based on YTD 2024 CLO market activity.

The CLO market should continue to experience robust issuance from sustained stability in loan market fundamentals. For CCIF, we remain focused on constructing a defensive portfolio of CLO equity with clean underlying loan portfolios. We continue to leverage Carlyle’s 14-step CLO investment process and the credit expertise of the broader Carlyle Liquid Credit platform.

7 J.P. Morgan Research as of September 30, 2024.

8 Nomura Research as of September 30, 2024.

9 Bank of America Global Research as of September 30, 2024.

IMPORTANT INFORMATION ABOUT THIS REPORT AND CARLYLE CREDIT INCOME FUND

Investment Objectives and Strategies

The Fund is a non-diversified, closed-end management investment company that has registered as an investment company under the 1940 Act. We have elected to be treated, and intend to qualify annually, as a regulated investment company, or “RIC,” under Subchapter M of the Internal Revenue Code of 1986, as amended, or the “Code.”

The Fund’s primary investment objective is to generate current income, with a secondary objective to generate capital appreciation. We seek to achieve our investment objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations, or “CLOs,” that are collateralized by a portfolio consisting primarily of below investment grade U.S. senior secured loans with a large number of distinct underlying borrowers across various industry sectors. We may also invest in other related securities and instruments or other securities and instruments that the Adviser believes are consistent with our investment objectives, including senior debt tranches of CLOs, loan accumulation facilities (“LAFs”) and securities issued by other securitization vehicles, such as collateralized bond obligations, or “CBOs.” LAFs are short- to medium-term facilities often provided by the bank that will serve as the placement agent or arranger on a CLO transaction. LAFs typically incur leverage between four and six times equity value prior to a CLO’s pricing. The CLO securities in which we primarily seek to invest are unrated or rated below investment grade and are considered speculative with respect to timely payment of interest and repayment of principal. Unrated and below investment grade securities are also sometimes referred to as “junk” securities. In addition, the CLO equity and junior debt securities in which we invest are highly leveraged (with CLO equity securities typically being leveraged ten times), which magnifies our risk of loss on such investments.

“Names Rule” Policy

In accordance with the requirements of the 1940 Act, we have adopted a policy to invest at least 80% of our assets in the particular type of investments suggested by our name. Accordingly, under normal circumstances, we invest at least 80% of the aggregate of its net assets and borrowings for investment purposes in credit and credit-related instruments. For purposes of this policy, the Fund considers credit and credit-related instruments to include, without limitation: (i) equity and debt tranches of CLOs, LAFs and securities issued by other securitization vehicles, such as CBOs; (ii) secured and unsecured floating rate and fixed rate loans; (iii) investments in corporate debt obligations, including bonds, notes, debentures, commercial paper and other obligations of corporations to pay interest and repay principal; (iv) debt issued by governments, their agencies, instrumentalities, and central banks; (v) commercial paper and short-term notes; (vi) convertible debt securities; (vii) certificates of deposit, bankers’ acceptances and time deposits; and (viii) other credit-related instruments. The Fund’s investments in derivatives, other investment companies, and other instruments designed to obtain indirect exposure to credit and credit-related instruments will be counted towards its 80% investment policy to the extent such instruments have similar economic characteristics to the investments included within that policy.

Our 80% policy with respect to investments in credit and credit-related instruments is not fundamental and may be changed by the Board without prior approval of our shareholders. Shareholders will be provided with sixty (60) days notice in the manner prescribed by the SEC before making any change to this policy.

Investment Restrictions

The Fund’s stated fundamental policies, which may only be changed by the affirmative vote of a majority of the outstanding voting securities of the Fund (the shares), are listed below. “Majority of the outstanding voting securities of the Fund” means the vote, at an annual or special meeting of shareholders, duly called, (a) of 67% or more of the shares present at such meeting, if the holders of more than 50% of the outstanding shares are present or represented by proxy; or (b) of more than 50% of the outstanding shares, whichever is less. The Fund may not:

1.Borrow money, except to the extent permitted by the 1940 Act (which currently limits borrowing to no more than 33-1/3% of the value of the Fund’s total assets, including the value of the assets purchased with the proceeds of its indebtedness, if any). The Fund may borrow for investment purposes, for temporary liquidity, or to finance repurchases of its shares.

2.Issue senior securities, except to the extent permitted by Section 18 of the 1940 Act (which currently limits the issuance of a class of senior securities that is indebtedness to no more than 33-1/3% of the value of the Fund’s total assets or, if the class of senior security is stock, to no more than 50% of the value of the Fund’s total assets).

3.Underwrite securities of other issuers, except insofar as the Fund may be deemed an underwriter under the Securities Act of 1933, as amended (the “Securities Act”) in connection with the disposition of its portfolio securities. The Fund may invest in restricted securities (those that must be registered under the Securities Act before they may be offered or sold to the public) to the extent permitted by the 1940 Act.

4.Invest more than 25% of the market value of its assets in the securities of companies, entities or issuers engaged in any one industry. This limitation does not apply to investment in the securities of the U.S. Government, its agencies or instrumentalities. For purposes of this restriction, an investment in a CLO, CBO, collateralized debt obligation, or “CDO” or a swap or other derivative will be considered to be an investment in the industry (if any) of the underlying or reference security, instrument or asset.

5.Purchase or sell real estate or interests in real estate. This limitation is not applicable to investments in securities that are secured by or represent interests in real estate (e.g. mortgage loans evidenced by notes or other writings defined to be a type of security). Additionally, the preceding limitation on real estate or interests in real estate does not preclude the Fund from investing in mortgage-related securities or investing in companies engaged in the real estate business or that have a significant portion of their assets in real estate (including real estate investment trusts), nor from disposing of real estate that may be acquired pursuant to a foreclosure (or equivalent procedure) upon a security interest.

6.Purchase or sell commodities, commodity contracts, including commodity futures contracts, unless acquired as a result of ownership of securities or other investments, except that the Fund may invest in securities or other instruments backed by or linked to commodities, and invest in companies that are engaged in a commodities business or have a significant portion of their assets in commodities, and may invest in commodity pools and other entities that purchase and sell commodities and commodity contracts.

7.Make loans to others, except (a) through the purchase of debt securities in accordance with its investment objectives and policies, including notes secured by real estate, which may be considered loans; (b) to the extent the entry into a repurchase agreement is deemed to be a loan; and (c) by loaning portfolio securities. Additionally, the preceding limitation on loans does not preclude the Fund from modifying note terms.

The Fund will treat with respect to participation interests both the financial intermediary and the borrower as “issuers” for purposes of fundamental investment restriction.

The fundamental investment limitations set forth above restrict the ability of the Fund to engage in certain practices and purchase securities and other instruments other than as permitted by, or consistent with, applicable law, including the 1940 Act. Relevant limitations of the 1940 Act as they presently exist are described below. These limitations are based either on the 1940 Act itself, the rules or regulations thereunder or applicable orders of the SEC. In addition, interpretations and guidance provided by the SEC staff may be taken into account to determine if a certain practice or the purchase of securities or other instruments is permitted by the 1940 Act, the rules or regulations thereunder or applicable orders of the SEC. As a result, the foregoing fundamental investment policies may be interpreted differently over time as the statute, rules, regulations or orders (or, if applicable, interpretations) that relate to the meaning and effect of these policies change, and no vote of Shareholders, as applicable, will be required or sought.

Use of Leverage and Leverage Risks

The use of leverage, whether directly or indirectly through investments such as CLO equity or junior debt securities that inherently involve leverage, may magnify our risk of loss. CLO equity or junior debt securities are very highly leveraged (with CLO equity securities typically being leveraged ten times), and therefore the CLO securities in which we invest are subject to a higher degree of loss since the use of leverage magnifies losses.

We may incur leverage, directly or indirectly, through one or more special purpose vehicles (entities primarily engaged in investment activities in securities or other assets that are wholly owned by the Fund), indebtedness for borrowed money, as well as leverage in the form of Derivative Transactions, preferred shares, debt securities and other structures and instruments, in significant amounts and on terms that the Adviser and the Board deem appropriate, subject to applicable limitations under the 1940 Act. Such leverage may be used for the acquisition and financing of our investments, to pay fees and expenses and for other purposes. Such leverage may be secured and/or unsecured. Any such leverage does not include leverage embedded or inherent in the CLO structures in which we invest or in derivative instruments in which we may invest. Accordingly, there is a layering of leverage in our overall structure.

The more leverage we employ, the more likely a substantial change will occur in our NAV. Accordingly, any event that adversely affects the value of an investment would be magnified to the extent leverage is utilized. For instance, any decrease in our income would cause net income to decline more sharply than it would have had we not borrowed. Such a decline could also negatively affect our ability to make distributions and other payments to our security holders. Leverage is generally considered a speculative investment technique. Our ability to service any debt that we incur will depend largely on our financial performance and will be subject to prevailing economic conditions and competitive pressures. The cumulative effect of the use of leverage with respect to any investments in a market that moves adversely to such investments could result in a substantial loss that would be greater than if our investments were not leveraged.

As a registered closed-end management investment company, we are required to meet certain asset coverage requirements, as defined under the 1940 Act, with respect to any senior securities. With respect to senior securities representing indebtedness (i.e., borrowings or deemed borrowings, including any notes), other than temporary borrowings as defined under the 1940 Act, we are required under current law to have an asset coverage of at least 300%, as measured at the time of borrowing and calculated as the ratio of our total assets (less all liabilities and indebtedness not represented by senior securities) over the aggregate amount of our outstanding senior securities representing indebtedness. With respect to senior securities that are stock (i.e., our preferred shares), we are required under current law to have an asset coverage of at least 200%, as measured at the time of the issuance of any such preferred shares and calculated as the ratio of our total assets (less all liabilities and indebtedness not represented by senior securities) over the aggregate amount of our outstanding senior securities representing indebtedness plus the aggregate liquidation preference of any outstanding preferred shares. If legislation were passed that modifies this section of the 1940 Act and increases the amount of senior securities that we may incur, we may increase our leverage to the extent then permitted by the 1940 Act and the risks associated with an investment in us may increase.

If our asset coverage declines below 300% (or 200%, as applicable), we would not be able to incur additional debt or issue additional preferred shares, and could be required by law to sell a portion of our investments to repay some debt or redeem preferred shares when it is disadvantageous to do so, which could have a material adverse effect on our operations, and we may not be able to make certain distributions or pay dividends of an amount necessary to continue to be subject to tax as a RIC. The amount of leverage that we employ will depend on the Adviser’s and the Board’s assessment of market and other factors at the time of any proposed borrowing. We cannot assure you that we will be able to obtain credit at all or on terms acceptable to us.

In addition, any debt facility into which we may enter would likely impose financial and operating covenants that restrict our business activities, including limitations that could hinder our ability to finance additional loans and investments or to make the distributions required to maintain our ability to be subject to tax as a RIC under Subchapter M of the Code.

The following table illustrates the effects of the Fund’s leverage due to senior securities on corresponding share total return, assuming investment portfolio total returns (consisting of income and changes in the value of investments held in the Fund’s portfolio) of -10%, -5%, 0%, 5% and 10%. These assumed investment portfolio returns are hypothetical figures and are not necessarily indicative of the investment portfolio returns expected to be experienced by the Fund. Your actual returns may be greater or less than those appearing below.

The following table assumes the Fund’s continued use of Preferred Shares representing approximately 35.07% of the Fund’s Managed Assets as of September 30, 2024, and the Fund bears expenses relating to such Preferred Shares at an annualized average interest rate of 8.46%. The table below also assumes that the annual return that the Fund’s portfolio must experience (net of expenses not related to Preferred Shares) in order to cover the costs of such leverage would be approximately 2.97%.

| | | | | | | | | | | | | | | | | |

| Assumed Return on Portfolio (Net of Expenses) | (10.00)% | (5.00)% | —% | 5.00% | 10.00% |

| Corresponding Share Total Return | (19.97)% | (12.27)% | (4.57)% | 3.13% | 10.83% |

Principal Risk Factors

For a description of the principal risk factors associated with an investment in the Fund, please refer to Note 5. Risk Factors, to the Financial Statements.

Additional Information

We file with or submit to the SEC annual and semi-annual reports, proxy statements and other information meeting the informational requirements of the Exchange Act or pursuant to Rule 30b2-1 under the 1940 Act. The SEC maintains a website that contains reports, proxy and information statements and other information we file with the SEC at www.sec.gov. This information is also available free of charge on our website (www.carlylecreditincomefund.com) or by calling (866) 277-8243 (toll-free).

Forward Looking Statements

This report may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements other than statements of historical facts included in this report may constitute forward-looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of a number of factors, including those described in the Fund’s filings with the SEC. The Company undertakes no duty to update any forward-looking statement made herein. All forward-looking statements speak only as of the date of this report.

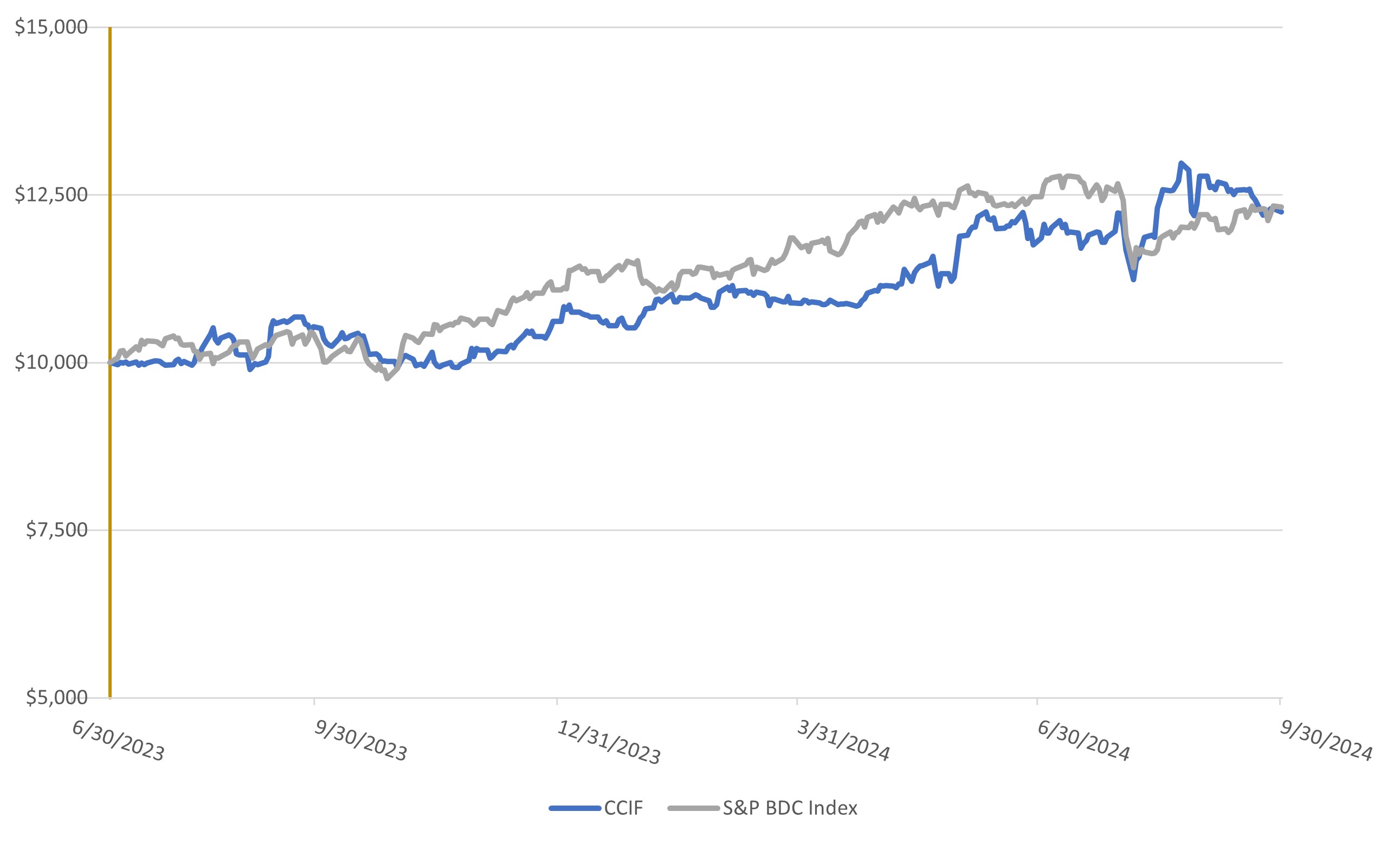

PERFORMANCE DATA

The graph presented below compares the cumulative shareholder return on our common shares with that of the S&P BDC Index. The Fund commenced operations on September 20, 2013; however prior to the close of business on July 14, 2023, the Fund was advised by a different investment adviser that is not affiliated with the Fund’s current adviser and the Fund’s performance for periods prior to July 14, 2023 are not shown in the graph below. Effective at the close of business on July 14, 2023, the Fund’s principal investment strategy was changed and the Fund seeks to achieve its investment objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations, or “CLOs.” The Fund believes the S&P BDC Index is the most appropriate and relevant index for comparative purposes for this investment strategy.

The graph assumes an investment of $10,000 in the Fund since the change in investment adviser on July 14, 2023. Total return is calculated assuming reinvestment of all dividends and distributions. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the repurchase of fund shares.

Past performance is not indicative of future results or a guarantee of future returns. Future results may vary and may be higher or lower than the data shown.

| | | | | | | | | | | | | | | | | |

| Annualized Total Return | Since Change in Strategy (July 14, 2023) |

| 3 Month | 6 Month | 9 Month | 1 Year |

| Carlyle Credit Income Fund | 19.00% | 27.39% | 21.96% | 17.21% | 19.59% |

| S&P BDC Index | (2.57)% | 7.36% | 13.32% | 16.27% | 16.97% |

SUMMARY OF CERTAIN UNAUDITED PORTFOLIO CHARACTERISTICS

The information presented below is on a look-through basis to the collateralized loan obligation, or “CLO”, equity and related investments held by the Fund as of September 30, 2024, and reflects the aggregate underlying exposure of the Fund based on the portfolios of those investments. The data is estimated, unaudited, and derived from CLO trustee reports received by the Fund as of and for the year ended September 30, 2024 and from custody statements and/or other information received from CLO collateral managers, or third party sources.

Portfolio Investment Breakdown as of September 30, 2024

(Excludes cash equivalents and other assets)

| | | | | |

| Summary of Underlying Portfolio |

| Number of Unique Underlying Loan Obligors | 1,367 |

| Number of Underlying Loans | 1,916 |

| Aggregate Balance of Underlying Loans | $24.34 Billion |

| Average Individual Loan Obligor Exposure | 0.07 | % |

| Currency: USD Exposure | 100.00 | % |

| Aggregate Indirect Exposure to Senior Secured Loans | 96.58 | % |

| Weighted Average Junior OC Cushion | 4.33 | % |

| Weighted Average Market Price of Loan Collateral | 97.43 |

| Weighted Average Remaining CLO Reinvestment Period | 2.5 years |

| Last 12 Month Default Rate including Distressed Exchanges of Underlying Loans | 1.54 | % |

| | | | | |

| Top 10 Underlying Obligors |

| Obligor | % Total |

| TransDigm | 0.61 | % |

| Asurion | 0.57 | % |

| Medline | 0.56 | % |

| Sedgwick Claims Management Service | 0.52 | % |

| Caesars Entertainment | 0.49 | % |

| Peraton | 0.48 | % |

| TIBCO Software | 0.47 | % |

| Altice France | 0.45 | % |

| Brookfield WEC Holdings | 0.44 | % |

| Calpine | 0.44 | % |

| Total | 5.03 | % |

| | | | | |

| Top 10 Industries of Underlying Obligors |

| Industry | % Total |

| High Tech | 12.53 | % |

| Healthcare & Pharmaceuticals | 11.44 | % |

| Banking, Finance, Insurance & Real Estate | 9.61 | % |

| Services: Business | 7.68 | % |

| Hotels, Gaming & Leisure | 5.36 | % |

| Chemicals, Plastics & Rubber | 4.87 | % |

| Construction & Building | 4.75 | % |

| Capital Equipment | 4.31 | % |

| Aerospace & Defense | 4.07 | % |

| Telecommunications | 3.89 | % |

| Total | 68.51 | % |

Weighted Average Rating Distribution Weighted Average Maturity Distribution

Wtd Avg = B+ Wtd Avg = 4.5 yrs

Weighted Average Price Distribution Weighted Average Spread Distribution

Wtd Avg = 97.43 Wtd Avg = 3.46%

FEES AND EXPENSES

The following table is intended to assist in understanding the costs and expenses that an investor in our common shares will bear, directly or indirectly, based on the assumptions set forth below. The expenses shown in the table under “Annual Expenses” are estimated amounts based on historical fees and expenses, as appropriate. We caution that some of the percentages indicated in the table below are estimates and may vary. Except where the context suggests otherwise, whenever this table contains a reference to our fees or expenses, we will pay such fees and expenses out of our net assets and, consequently, shareholders will indirectly bear such fees or expenses as investors in the Fund.

| | | | | | | | |

| SHAREHOLDER TRANSACTION FEES | | |

| Sales load | — | % | (1) |

| Offering expenses borne by the Fund | — | % | (2) |

| Dividend reinvestment plan expenses | — | % | (3) |

| Total shareholder transaction fees | — | % | (4) |

| | | | | | | | |

ESTIMATED ANNUAL FUND EXPENSES

(as a percentage of net assets attributable to common shares) | | |

| Management Fee | 2.59 | % | (5) |

| Incentive Fee payable under Investment Advisory Agreement (17.5%) | 2.76 | % | (6) |

| Interest payments and fees on borrowed funds | 4.82 | % | (7) |

| Other Expenses | 2.24 | % | (8) |

| Total annual fund expenses | 12.41 | % |

|

1.In the event that the Fund sells its securities publicly through underwriters or agents the related prospectus supplement will disclose the applicable sales load.

2.In the event that the Fund sells its securities publicly through underwriters or agents the related prospectus supplement will disclose the estimated amount of total offering expenses (which may include offering expenses borne by third parties on the Fund’s behalf), the offering price and the offering expenses borne by the Fund as a percentage of the offering price.

3.The expenses of administering the Dividend Reinvestment Plan (the “DRP”) are included in “Other Expenses.” Investors will pay brokerage charges if they direct their broker or the DRP Plan agent to sell their Common Shares that they acquired pursuant to the DRP. See “Dividend Reinvestment Plan.”

4.The related prospectus supplement will disclose the offering price and the total stockholder transaction expenses as a percentage of the offering price.

5.The Management Fee is calculated and payable monthly in arrears at the annual rate of 1.75% of the month-end value of the Fund’s managed Assets. “Managed Assets” means the total assets of the Fund (including any assets attributable to any preferred shares or to indebtedness) minus the Fund’s liabilities other than liabilities relating to indebtedness.

6.The Fund shall pay CGCIM an Incentive Fee calculated and payable quarterly in arrears based upon the Fund’s “pre-incentive fee net investment income” for the immediately preceding quarter, and is subject to a hurdle rate, expressed as a rate of return on the Fund’s net assets, equal to 2.00% per quarter (or an annualized hurdle rate of 8.00%), subject to a “catch-up” feature. For this purpose, “pre-incentive fee net investment income” means interest income, dividend income, income generated from original issue discounts, payment-in-kind income, and any other income earned or accrued during the calendar quarter, minus the Fund’s operating expenses (which, for this purpose shall not include any distribution and/or shareholder servicing fees, litigation, any extraordinary expenses or Incentive Fee) for the quarter. For purposes of computing the Fund’s pre-incentive fee net investment income, the calculation methodology will look through total return swaps as if the Fund owned the referenced assets directly. As a result, the Fund’s pre-incentive fee net investment income includes net interest, if any, associated with a derivative or swap, which is the difference between (a) the interest income and transaction fees related to the reference assets and (b) all interest and other expenses paid by the Fund to the derivative or swap counterparty. “Net assets” means the total assets of the Fund minus the Fund’s liabilities. For purposes of the Incentive Fee, net assets are calculated for the relevant quarter as the weighted average of the net asset value of the Fund as of the first business day of each month therein. The weighted average net asset value shall be calculated for each month by multiplying the net asset value as of the beginning of the first business day of the month times the number of days in that month, divided by the number of days in the applicable calendar quarter.

The calculation of the Incentive Fee for each calendar quarter is as follows:

•No Incentive Fee is payable to CGCIM if the Fund’s pre-incentive fee net investment income, expressed as a percentage of the Fund’s net assets in respect of the relevant calendar quarter, does not exceed the quarterly hurdle rate of 2.00%;

•100% of the portion of the Fund’s pre-incentive fee net investment income that exceeds the hurdle rate but is less than or equal to 2.4242% (the “catch-up”) is payable to CGCIM if the Fund’s pre-incentive fee net investment income, expressed as a percentage of the Fund’s net assets in respect of the relevant calendar quarter, exceeds the hurdle rate but is less than or equal to 2.4242% (9.6968% annualized). The “catch-up” provision is intended to provide CGCIM with an incentive fee

of 17.5% on all of the Fund’s pre-incentive fee net investment income when the Fund’s pre-incentive fee net investment income reaches 2.4242% of net assets; and

•17.5% of the portion of the Fund’s pre-incentive fee net investment income that exceeds the “catch-up” is payable to CGCIM if the Fund’s pre-incentive fee net investment income, expressed as a percentage of the Fund’s net assets in respect of the relevant calendar quarter, exceeds 2.4242% (9.6968% annualized). As a result, once the hurdle rate is reached and the catch-up is achieved, 17.5% of all the Fund’s pre-incentive fee net investment income thereafter is allocated to CGCIM.

7.The Fund may issue preferred shares or debt securities. The above figure assumes an aggregate of $52 million of the Fund’s Series A Term Preferred Shares with an interest rate of 8.75% per annum, and $11.5 million of the Fund’s Series B Convertible Preferred Shares with an interest rate of 7.125% per annum. In the event that the Fund were to issue additional preferred shares or debt securities, the Fund’s borrowing costs, and correspondingly its total annual expenses, including, in the case of such preferred shares, the base management fee as a percentage of the Fund’s net assets attributable to common shares, would increase.

8.“Other expenses” includes the Fund’s overhead expenses, including payments under the Administration Agreement based on the Fund’s allocable portion of overhead and other expenses incurred by Administrator, and payment of fees in connection with outsourced administrative functions, and are based on estimated amounts for the current fiscal year. “Other expenses” also includes the ongoing administrative expenses to the independent accountants and legal counsel of the Fund, compensation of independent directors, and costs and expenses relating to rating agencies.

The following examples illustrate the hypothetical expenses that would be paid on a $1,000 investment assuming annual expenses attributable to common shares remain unchanged and common shares earn a 5% annual return:

| | | | | | | | | | | | | | |

| Example | 1 Year | 3 Years | 5 Years | 10 Years |

| Expenses on a $1,000 investment, assuming a 5% annual return | $127 | $353 | $545 | $910 |

The example and the expenses in the tables above should not be considered a representation of the Fund’s future expenses, and actual expenses may be greater or less than those shown. While the example assumes a 5.0% annual return, as required by the SEC, the Fund’s performance will vary and may result in a return greater or less than 5.0%.

CARLYLE CREDIT INCOME FUND

STATEMENT OF ASSETS AND LIABILITIES

As of September 30, 2024

(expressed in U.S. dollars)

| | | | | | | | | |

| | September 30, 2024 | |

| ASSETS | | | |

| Investments, at fair value (cost $184,008,668) | | $ | 173,453,913 | | |

| Cash and cash equivalents | | 725,402 | | |

| Interest receivable | | 6,038,543 | | |

| Prepaid expenses | | 457,705 | | |

| Receivable for common shares issued pursuant to the Fund's dividend reinvestment plan | | 119,038 | | |

| Total assets | | $ | 180,794,601 | | |

| | | |

| LIABILITIES | | | |

| | | |

| Preferred Shares (net of unamortized deferred issuance costs of $2,645,568) (Note 7) | | $ | 60,871,432 | | |

| | | |

| Incentive fee payable | | 900,954 | | |

| Management fee payable | | 260,905 | | |

| Professional fees payable | | 635,885 | | |

| Interest payable | | 77,500 | | |

| Administration and custodian fees payable | | 46,109 | | |

| Other payables and accrued expenses | | 388,813 | | |

| | | |

| Total liabilities | | $ | 63,181,598 | | |

| | | |

| COMMITMENTS AND CONTINGENCIES (Note 8) | | | |

| | | |

| Net Assets | | $ | 117,613,003 | | |

| | | |

| COMPOSITION OF NET ASSETS | | | |

| | | |

| Paid-in capital | | $ | 125,310,011 | | |

| Total distributable earnings (losses) | | (7,697,008) | | |

| Total Net Assets | | $ | 117,613,003 | | |

| Common shares outstanding (no par value) | | 15,387,448 | | |

| Net asset value per share of common stock | | $ | 7.64 | | |

See accompanying Notes to Financial Statements.

CARLYLE CREDIT INCOME FUND

SCHEDULE OF INVESTMENTS

As of September 30, 2024

(expressed in U.S. dollars)

| | | | | | | | | | | | | | | | | | | | |

Issuer (1)(7) | Investment Description | Acquisition Date (2) | Principal Amount | Cost | Fair Value (3) | % of Net Assets |

CLO - Equity(4)(5) | | | | | | |

| 522 Funding CLO 2021-7, Ltd. | Subordinated Notes (effective yield 14.24%, 4/23/2034) | 7/27/2023 | $ | 4,505,000 | | $ | 2,649,366 | | $ | 2,347,367 | | 2.00 | % |

| AGL CLO 17, Ltd. | Subordinated Notes (effective yield 15.22%, 1/21/2035) | 5/6/2024 | 2,750,000 | | 2,072,304 | | 1,931,794 | | 1.64 | % |

| Aimco CLO 10, Ltd. | Subordinated Notes (effective yield 31.23%, 7/22/2032) | 11/27/2023 | 11,071,800 | | 6,049,880 | | 6,290,114 | | 5.35 | % |

| Aimco CLO 14, Ltd. | Subordinated Notes (effective yield 15.12%, 4/20/2034) | 7/17/2023 | 6,200,000 | | 4,475,170 | | 4,228,760 | | 3.60 | % |

| Apidos CLO XXXIII, Ltd. | Subordinated Notes (effective yield 16.29%, 10/24/2034) | 7/25/2024 | 4,000,000 | | 2,928,200 | | 2,813,880 | | 2.39 | % |

| Apidos CLO XXXIX, Ltd. | Subordinated Notes (effective yield 15.40%, 4/21/2035) | 5/2/2024 | 5,710,000 | | 4,010,434 | | 3,925,441 | | 3.34 | % |

| Ares LIX CLO, Ltd. | Subordinated Notes (effective yield 22.88%, 4/25/2034) | 12/7/2023 | 8,000,000 | | 4,713,812 | | 5,058,711 | | 4.30 | % |

| Ares LVI CLO, Ltd. | Subordinated Notes (effective yield 21.90%, 10/25/2034) | 8/24/2023 | 3,900,000 | | 2,435,090 | | 2,562,165 | | 2.18 | % |

| Ares LX CLO, Ltd. | Subordinated Notes (effective yield 24.52%, 7/18/2034) | 11/29/2023 | 1,600,000 | | 820,994 | | 919,454 | | 0.78 | % |

| Ballyrock CLO 15, Ltd. | Subordinated Notes (effective yield 16.60%, 4/15/2034) | 8/16/2023 | 5,000,000 | | 3,330,018 | | 3,162,917 | | 2.69 | % |

| Ballyrock CLO 16, Ltd. | Subordinated Notes (effective yield 18.29%, 7/20/2034) | 8/20/2024 | 5,000,000 | | 3,195,000 | | 3,168,458 | | 2.69 | % |

| Ballyrock CLO 18, Ltd. | Subordinated Notes (effective yield 13.49%, 1/15/2035) | 8/16/2023 | 2,500,000 | | 1,726,933 | | 1,494,190 | | 1.27 | % |

| Ballyrock CLO 19, Ltd. | Subordinated Notes (effective yield 14.96%, 4/20/2035) | 5/6/2024 | 4,300,000 | | 2,724,051 | | 2,528,035 | | 2.15 | % |

| Barings CLO, Ltd. 2019-III | Subordinated Notes (effective yield 28.74%, 4/20/2031) (6) | 12/13/2023 | 5,250,000 | | 2,567,872 | | 2,408,223 | | 2.05 | % |

| Barings CLO, Ltd. 2021-I | Subordinated Notes (effective yield 19.91%, 4/25/2034) | 7/17/2023 | 3,400,000 | | 2,038,280 | | 1,866,005 | | 1.59 | % |

| Benefit Street Partners CLO XXIII, Ltd. | Subordinated Notes (effective yield 21.60%, 4/25/2034) | 8/2/2023 | 10,000,000 | | 6,780,053 | | 6,744,863 | | 5.73 | % |

| Birch Grove CLO 3, Ltd. | Subordinated Notes (effective yield 15.30%, 7/20/2034) | 9/04/2024 | 5,000,000 | | 4,150,000 | | 4,128,401 | | 3.51 | % |

| CIFC Funding 2020-III, Ltd. | Subordinated Notes (effective yield 16.44%, 10/20/2034) | 9/20/2023 | 8,750,000 | | 6,623,682 | | 6,301,512 | | 5.36 | % |

| Elmwood CLO 16, Ltd. | Subordinated Notes (effective yield 16.25%, 4/20/2034) | 8/10/2023 | 6,000,000 | | 3,596,602 | | 3,822,452 | | 3.25 | % |

| Elmwood CLO I, Ltd. | Subordinated Notes (effective yield 14.35%, 4/20/2037) | 9/10/2024 | 7,010,000 | | 5,007,593 | | 5,102,296 | | 4.34 | % |

| Elmwood CLO VI, Ltd. | Subordinated Notes (effective yield 19.53%, 10/20/2034) | 7/17/2023 | 2,000,000 | | 1,219,379 | | 1,393,890 | | 1.19 | % |

| Elmwood CLO VII, Ltd. | Subordinated Notes (effective yield 22.37%, 1/17/2034) | 7/17/2023 | 2,000,000 | | 1,102,028 | | 1,196,862 | | 1.02 | % |

| Empower CLO 2022-1, Ltd. | Subordinated Notes (effective yield 16.84%, 10/20/2037) | 9/27/2024 | 6,500,000 | | 6,516,250 | | 6,509,118 | | 5.53 | % |

| Galaxy XXII CLO, Ltd. | Subordinated Notes (effective yield 19.95%, 4/16/2034) | 12/15/2023 | 3,560,000 | | 1,923,783 | | 1,675,143 | | 1.42 | % |

| Invesco CLO 2021-1, Ltd. | Subordinated Notes (effective yield 17.54%, 4/15/2034) | 9/20/2023 | 5,000,000 | | 3,170,403 | | 2,457,980 | | 2.09 | % |

| Invesco CLO 2022-1, Ltd. | Subordinated Notes (effective yield 19.29%, 4/20/2035) | 10/25/2023 | 5,500,000 | | 3,257,800 | | 2,895,749 | | 2.46 | % |

| KKR CLO 25, Ltd. | Subordinated Notes (effective yield 21.92%, 7/15/2034) | 12/11/2023 | 2,500,000 | | 1,623,181 | | 1,653,087 | | 1.41 | % |

| KKR CLO 31, Ltd. | Subordinated Notes (effective yield 20.69%, 4/20/2034) | 12/7/2023 | 6,000,000 | | 4,128,321 | | 3,940,842 | | 3.35 | % |

| KKR CLO 33, Ltd. | Subordinated Notes (effective yield 20.80%, 7/20/2034) | 9/13/2023 | 5,000,000 | | 3,279,645 | | 3,011,368 | | 2.56 | % |

| Madison Park Funding LXII, Ltd. | Subordinated Notes (effective yield 14.93%, 7/17/2036) | 7/25/2023 | 12,000,000 | | 8,632,020 | | 6,944,660 | | 5.90 | % |

| Magnetite XIX, Ltd. | Subordinated Notes (effective yield 13.72%, 4/17/2034) | 9/15/2023 | 8,614,583 | | 5,271,114 | | 4,469,147 | | 3.80 | % |

| MidOcean Credit CLO XI, Ltd. | Subordinated Notes (effective yield 23.17%, 10/18/2033) | 1/12/2024 | 6,250,000 | | 3,942,829 | | 3,630,182 | | 3.09 | % |

CARLYLE CREDIT INCOME FUND

SCHEDULE OF INVESTMENTS

As of September 30, 2024

(expressed in U.S. dollars)

| | | | | | | | | | | | | | | | | | | | |

Issuer (1)(7) | Investment Description | Acquisition Date (2) | Principal Amount | Cost | Fair Value (3) | % of Net Assets |

| MidOcean Credit CLO XIV, Ltd. | Subordinated Notes (effective yield 13.39%, 4/15/2037) | 2/15/2024 | $ | 6,750,000 | | $ | 4,743,456 | | $ | 4,534,020 | | 3.86 | % |

| Neuberger Berman Loan Advisers CLO 38, Ltd. | Subordinated Notes (effective yield 16.38%, 10/20/2035) | 8/1/2023 | 9,500,000 | | 5,543,626 | | 5,408,974 | | 4.60 | % |

| Neuberger Berman Loan Advisers CLO 41, Ltd. | Subordinated Notes (effective yield 15.41%, 4/15/2034) | 11/1/2023 | 4,500,000 | | 2,744,213 | | 2,585,115 | | 2.20 | % |

| Niagara Park CLO, Ltd. | Subordinated Notes (effective yield 35.91%, 7/17/2032) | 12/1/2023 | 6,850,000 | | 3,603,707 | | 3,336,466 | | 2.84 | % |

| OCP CLO 2015-9, Ltd. | Subordinated Notes (effective yield 24.92%, 1/15/2033) | 12/6/2023 | 13,000,000 | | 4,661,043 | | 4,441,180 | | 3.77 | % |

| OCP CLO 2024-34, Ltd. | Subordinated Notes (effective yield 13.47%, 10/15/2037) | 7/2/2024 | 5,000,000 | | 4,120,855 | | 4,195,136 | | 3.57 | % |

| Octagon 55, Ltd. | Subordinated Notes (effective yield 20.26%, 7/20/2034) | 7/19/2023 | 6,000,000 | | 3,256,512 | | 3,002,302 | | 2.55 | % |

| OHA Credit Partners XIII, Ltd. | Subordinated Notes (effective yield 20.72%, 10/21/2034) | 7/17/2023 | 2,950,000 | | 1,660,579 | | 2,287,728 | | 1.95 | % |

| Rad CLO 3, Ltd. | Subordinated Notes (effective yield 16.95%, 7/15/2037) (6) | 9/4/2024 | 15,392,500 | | 10,250,122 | | 10,538,115 | | 8.95 | % |

| RR 12, Ltd. | Subordinated Notes (effective yield 22.43%, 1/15/2036) | 7/31/2024 | 8,542,000 | | 2,680,052 | | 2,427,667 | | 2.06 | % |

| RR 2, Ltd. | Subordinated Notes (effective yield 14.94%, 4/15/2036) | 1/18/2024 | 11,000,000 | | 6,539,814 | | 5,525,264 | | 4.70 | % |

| RR 6, Ltd. | Subordinated Notes (effective yield 19.75%, 4/15/2036) | 4/25/2024 | 2,206,250 | | 1,583,020 | | 1,373,933 | | 1.16 | % |

| Signal Peak CLO 10, Ltd. | Subordinated Notes (effective yield 20.47%, 1/24/2035) | 3/28/2024 | 3,000,000 | | 1,604,615 | | 1,334,093 | | 1.13 | % |

| Voya CLO 2020-2, Ltd. | Subordinated Notes (effective yield 18.21%, 7/19/2034) | 8/2/2023 | 10,500,000 | | 7,996,280 | | 6,842,791 | | 5.82 | % |

| Voya CLO 2020-3, Ltd. | Subordinated Notes (effective yield 18.59%, 10/20/2034) | 8/3/2023 | 4,000,000 | | 2,884,492 | | 2,676,271 | | 2.28 | % |

| Total CLO Equity | | | | $ | 179,834,473 | | $ | 171,092,121 | | 145.47 | % |

CLO - Subordinated Fee Note (4)(5) | | | | | | |

| Invesco CLO 2022-1, Ltd. | Subordinated Fee Notes (effective yield 31.70%, 4/20/2035) | 10/25/2023 | $ | 550,000 | | $ | 122,753 | | $ | 146,239 | | 0.13 | % |

| Neuberger Berman Loan Advisers CLO 38, Ltd. | Subordinated Fee Notes (effective yield 21.34%, 10/20/2035) | 8/1/2023 | 69,788 | | 47,563 | | 40,553 | | 0.03 | % |

| Total CLO Subordinated Fee Notes | | | | $ | 170,316 | | $ | 186,792 | | 0.16 | % |

Real Estate(8) | | | | | | |

| Moores Crossing - Travis County, TX | | 7/14/2023 | $ | 4,000,000 | | $ | 4,003,879 | | $ | 2,175,000 | | 1.85 | % |

| | | | | | |

| Total Investments | | | | $ | 184,008,668 | | $ | 173,453,913 | | 147.48 | % |

| | | | | | |

| Cash Equivalents | | | | | | |

| U.S. Bank MMDA | Money Market Deposit Account | | $ | 725,402 | | $ | 725,402 | | $ | 725,402 | | 0.62 | % |

| | | | | | |

| Total Investments and Cash Equivalents | | | | $ | 184,734,070 | | $ | 174,179,315 | | 148.10 | % |

| | | | | | |

(1) The Fund is not affiliated with, nor does it "control" (as such term is defined in the Investment Company Act of 1940 (the "1940 Act")), any of the issuers listed. In general, under the 1940 Act, the Fund would be presumed to "control" an issuer if it owned 25% or more of its voting securities.

(2) Acquisition date represents the initial date of purchase or the date the investment was contributed to the Fund at the time of the Fund's formation.

(3) Fair value is determined by the Adviser in accordance with the written valuation policies and procedures, subject to oversight by the Fund's Board of Trustees, in accordance with Rule 2a-5 under the 1940 Act.

(4) Securities exempt from registration under the Securities Act of 1933, and are deemed to be "restricted securities." As of September 30, 2024, the aggregate fair value of these securities is $171,278,913, or 145.63% of the Fund's net assets.

(5) CLO subordinated notes and subordinated fee notes are considered CLO equity positions. CLO equity positions are entitled to recurring distributions which are generally equal to the remaining cash flow of payments made by underlying assets less contractual payments to debt

CARLYLE CREDIT INCOME FUND

SCHEDULE OF INVESTMENTS

As of September 30, 2024

(expressed in U.S. dollars)

holders and fund expenses. The effective yield is estimated based upon the current projection of the amount and timing of these recurring distributions in addition to the estimated amount of terminal principal payment. It is the Fund's policy to calculate the effective yield for each CLO equity position held within the Fund's portfolio at the initiation of each investment and to update it each subsequent quarter thereafter. The effective yield and investment cost may ultimately not be realized. As of September 30, 2024, the Fund's weighted average effective yield on its aggregate CLO equity positions, based on current amortized cost, was 18.63%.

(6) Fair value includes the Fund’s interests in fee rebates on the CLO subordinated notes.

(7) The fair value of the investment was determined using significant unobservable inputs. See “Note 3. Fair Value Measurements.”

(8) The Fund inherited a non-income producing defaulted real estate loan from VCIF that was not included in the legacy portfolio sale. Pursuant to a deed-in-lieu of foreclosure on August 10, 2023, the Fund has ownership of the real estate.

See accompanying Notes to Financial Statements.

CARLYLE CREDIT INCOME FUND

STATEMENT OF OPERATIONS

For the Year Ended September 30, 2024

(expressed in U.S. dollars)

| | | | | | | | |

| | Year Ended September 30, 2024 |

| Investment Income | | |

| Interest income | | $ | 27,923,746 | |

| | |

| Total investment income | | 27,923,746 | |

| | |

| Expenses | | |

| Interest expense | | 4,631,258 | |

| Incentive fees | | 3,191,296 | |

| Management fees | | 2,685,093 | |

| Professional fees | | 1,357,653 | |

| Insurance expense | | 238,551 | |

| Administration and custodian fees | | 211,408 | |

| Printing expense | | 211,029 | |

| Trustees' fees and expenses | | 125,000 | |

| Transfer agent fees | | 124,142 | |

| Other expenses | | 102,773 | |

| | |

| | |

| | |

| Total expenses | | 12,878,203 | |

| | |

| | |

| Net Investment Income | | 15,045,543 | |

| | |

| Net Realized and Unrealized Gain (Loss) | | |

| Net realized gain (loss) on investments and foreign currency transactions | | 99,225 | |

| | |

| Net change in unrealized appreciation (depreciation) on investments, foreign currency, and cash equivalents | | (9,578,026) | |

| Net Realized and Unrealized Gain (Loss) | | (9,478,801) | |

| | |

| Net Increase in Net Assets Attributable to Common Shares from Operations | | $ | 5,566,742 | |

| | |

See accompanying Notes to the Financial Statements.

CARLYLE CREDIT INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS

For the Years Ended September 30, 2024 and September 30, 2023

(expressed in U.S. dollars)

| | | | | | | | | | | | | | | | |

| | | | |

| | Year Ended September 30, 2024 | | Year Ended September 30, 2023 | | |

| Net increase (decrease) in net assets from operations: | | | | | | |

| Net investment income | | $ | 15,045,543 | | | $ | 572,740 | | | |

| Net realized gain (loss) on investments and foreign currency transactions | | 99,225 | | | (10,719,160) | | | |

| Net change in unrealized appreciation (depreciation) on investments, foreign currency and cash equivalents | | (9,578,026) | | | (1,675,639) | | | |

| Net increase (decrease) in net assets resulting from operations | | 5,566,742 | | | (11,822,059) | | | |

| | | | | | |

| Distributions to shareholders from: | | | | | | |

| Net investment income | | (427,365) | | | (4,512,176) | | | |

| Return of capital | | (15,218,076) | | | (4,166,758) | | | |

| Total distributions to shareholders | | (15,645,441) | | | (8,678,934) | | | |

| | | | | | |

| Capital share transactions | | | | | | |

| Net increase (decrease) in net assets resulting from beneficial interest: | | | | | | |

| Issuance of common shares | | 28,063,654 | | | 10,816,451 | | | |

| Reinvestment of dividends | | 877,308 | | | 605,817 | | | |

| Net increase in net assets from capital share transactions | | 28,940,962 | | | 11,422,268 | | | |

| | | | | | |

| | | | | | |

| Total increase (decrease) in net assets | | 18,862,263 | | | (9,078,725) | | | |

| Net assets at the beginning of the period | | 98,750,740 | | | 107,829,465 | | | |

| Net assets at the end of the period | | $ | 117,613,003 | | | $ | 98,750,740 | | | |

See accompanying Notes to Financial Statements.

CARLYLE CREDIT INCOME FUND

STATEMENT OF CASH FLOWS

For the Year Ended September 30, 2024

(expressed in U.S. dollars)

| | | | | | | | |

| | Year Ended September 30, 2024 |

| Cash flows from operating activities | | |

| Net increase in net assets resulting from operations | | $ | 5,566,742 | |

| Adjustments to reconcile net increase in net assets from operations to net cash provided by operating activities: | | |

| Purchases of investments, net of change in payable for investments purchased | | (112,288,796) | |

Proceeds from disposition of investments and reductions to investment cost value (1) | | 23,236,392 | |

| Net amortization on investments | | (4,028) | |

| Amortization of deferred issuance costs on preferred shares | | 481,918 | |

| Net realized gain on investments | | (99,225) | |

| Change in unrealized depreciation on investments | | 9,578,026 | |

| Changes in assets: | | |

| Increase in interest receivable | | (3,713,962) | |

| Decrease in receivable for investments sold | | 1,450,000 | |

| Increase in prepaid expenses and other assets | | (77,860) | |

| Changes in liabilities: | | |

| | |

| Increase in incentive fee payable | | 900,954 | |

| Increase in management fee payable | | 260,905 | |

| Increase in interest payable on preferred shares | | 77,500 | |

| Decrease in professional fees payable | | (90,950) | |

| Decrease in administration and custodian fees payable | | (39,008) | |

| Increase in other payables and accrued expenses | | 144,364 | |

| Net cash used in operating activities | | (74,617,028) | |

| | |

| Cash flows from financing activities | | |

| Proceeds from the issuance of preferred shares | | 63,517,000 | |

| Deferred issuance costs for the issuance of preferred shares | | (3,127,486) | |

| Proceeds from common shares issued, net of commissions and fees | | 28,063,654 | |

| Dividends paid to shareholders, net of reinvestments | | (14,768,133) | |

| Decrease in dividend payable | | (1,159,119) | |

| | |

| | |

| | |

| Net cash provided by financing activities | | 72,525,916 | |

| Effect of exchange rate changes on cash | | 448 | |

| Net decrease in cash and cash equivalents | | (2,090,664) | |

| Cash and cash equivalents, beginning of year | | 2,816,066 | |

| Cash and cash equivalents, end of year | | $ | 725,402 | |

| | | | | | | | |

| Supplemental information: | | |

| | |

| Cash paid for interest on preferred shares | | $ | 4,071,840 | |

| Non-cash activities: | | |

| Reinvestment of dividends | | $ | 877,308 | |

(1) Proceeds from the disposition of investments and reductions to investment cost value includes $12,087,526 of return of capital on CLO equity investments from recurring cash flows and refinancings during the year ended September 30, 2024.

See accompanying Notes to Financial Statements.

CARLYLE CREDIT INCOME FUND

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended September 30, | |

| 2024 | | 2023(4) | | 2022 | | 2021 | | 2020 | |

| Per Share Operating Data | | | | | | | | | | |

| Net asset value, beginning of period | $ | 8.42 | | | $ | 10.39 | | | $ | 11.69 | | | $ | 12.05 | | | $ | 12.71 | | |

| Income (loss) from investment operations: | | | | | | | | | | |

Net investment income (1) | 1.19 | | | 0.05 | | | 0.50 | | | 0.42 | | | 0.36 | | |

| Net realized and unrealized gain (loss) | (0.74) | | | (1.20) | | | (0.80) | | | 0.33 | | | (0.50) | | |

| Total from investment operations | 0.45 | | | (1.15) | | | (0.30) | | | 0.75 | | | (0.14) | | |

| Dividends to shareholders from: | | | | | | | | | | |

| Net investment income | (0.03) | | | (0.43) | | | (0.73) | | | (0.89) | | | (0.33) | | |

| Net realized gains | — | | | — | | | (0.18) | | | (0.22) | | | (0.19) | | |

| Return of capital | (1.20) | | | (0.40) | | | (0.09) | | | — | | | — | | |

| Total dividends | (1.23) | | | (0.82) | | — | | (1.00) | | | (1.11) | | — | | (0.52) | | |

| Net asset value, end of period | $ | 7.64 | | | $ | 8.42 | | | $ | 10.39 | | | $ | 11.69 | | | $ | 12.05 | | |

| Per share market value at beginning of period | $ | 8.18 | | | $ | 8.92 | | | $ | 10.49 | | | $ | 9.93 | | | $ | 10.68 | | |

| Per share market value at end of period | $ | 8.23 | | | $ | 8.18 | | | $ | 8.92 | | | $ | 10.49 | | | $ | 9.93 | | |

| | | | | | | | | | |

Total Return based on Net Asset Value (2) | 6.07 | % | | (11.75) | % | | (2.77) | % | | 6.52 | % | | (1.09) | % | |

Total Return based on Market Value (2) | 17.21 | % | | 0.39 | % | | (5.95) | % | | 17.59 | % | | (2.99) | % | |

| Ratios/Supplemental Data | | | | | | | | | | |

| Net assets, end of period (in thousands) | $ | 117,613 | | | $ | 98,751 | | | $ | 107,829 | | | $ | 121,324 | | | $ | 125,034 | | |

Ratio of gross expenses to average net assets (3) | 12.92 | % | | 7.42 | % | | 3.27 | % | | 3.05 | % | | 3.06 | % | |

Ratio of net expenses to average net assets (3) | 12.92 | % | | 6.72 | % | | 3.09 | % | | 2.88 | % | | 2.73 | % | |

Ratio of net expenses before incentive fees to average net assets (3) | 9.72 | % | | N/A | | N/A | | N/A | | N/A | |

Ratio of net investment income to average net assets (3) | 15.10 | % | | 0.56 | % | | 4.53 | % | | 3.56 | % | | 2.95 | % | |

| Portfolio turnover rate | 17.69 | % | | 100.91 | % | | 28.39 | % | | 14.73 | % | | 20.13 | % | |

| Asset coverage of preferred shares | 285 | % | | N/A | | N/A | | N/A | | N/A | |

Loan Outstanding, End of Year/Period (in thousands) (5) | N/A | | N/A | | $ | 7,455 | | | $ | 1,923 | | | $ | 13,000 | | |

Asset Coverage Ratio for Loan Outstanding (5) | N/A | | N/A | | 1546 | % | | 6409 | % | | 1062 | % | |

Asset Coverage, per $1,000 Principal Amount of Loan Outstanding (5) | N/A | | N/A | | $ | 15,463 | | | $ | 64,090 | | | $ | 10,618 | | |

Weighted Average Loans Outstanding (in thousands) (5) | N/A | | $ | 3,732 | | | $ | 8,051 | | | $ | 10,788 | | | $ | 9,796 | | |

Weighted Average Interest Rate on Loans Outstanding (5) | N/A | | 7.94 | % | | 4.50 | % | | 3.75 | % | | 3.79 | % | |

(1) Per share amounts are calculated based on the average shares outstanding during the period.

(2) Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any, and excludes the effect of sales charges. Had the Adviser not waived expenses, total returns would have been lower. Returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

(3) Annualized for periods less than one full year. For years ended September 2020, 2021, 2022, and 2023 the Fund waived certain expenses in connection with an expense limitation agreement. For the year ended September 30, 2024, there were no expenses waived. See Note 4. Related Party Transactions, for further information.

(4) Effective at the close of business on July 14, 2023, CGCIM replaced Oakline Advisors as the Fund’s new investment adviser and the Fund’s investment strategy was changed to invest primarily in debt and equity tranches issued by collateralized loan obligations. Prior to the close of business on July 14, 2023, the investment strategy was to invest primarily in mortgage notes secured by residential real estate.

(5) As of September 30, 2024, the Fund did not have any outstanding loans. A revolving line of credit agreement between the Fund and Nexbank was terminated on July 5, 2023.

CARLYLE CREDIT INCOME FUND

FINANCIAL HIGHLIGHTS (Continued)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Senior Securities | | | | | | | | |

| Class and Period Ended | | Total Amount Outstanding Exclusive of Treasury Securities (1) | | Asset Coverage Per Unit (2) | | Involuntary Liquidating Preference Per Unit (3) | | Average Market Value Per Unit (4) |

8.75% Series A Term Preferred Shares | | | | | | | | |

| September 30, 2024 | | $ | 52,000,000 | | | $ | 87.08 | | | $ | 25 | | | $ | 25.60 | |

7.125% Series B Convertible Preferred Shares | | | | | | | | |

| September 30, 2024 | | $ | 11,517,000 | | | $ | 15,727.19 | | | $ | 1,000 | | | N/A |

(1) Total amount of each class of senior securities outstanding at principal value at the end of the period presented.

(2) The asset coverage ratio for a class of senior securities representing indebtedness is calculated as our consolidated total assets, less all liabilities and indebtedness not represented by senior securities, divided by total senior securities representing indebtedness as calculated separately for each of the Preferred Shares in accordance with Section 18(h) of the 1940 Act. The asset coverage per unit figure is expressed in terms of dollar amounts per share of outstanding Preferred Shares (based on a per share liquidation preference of $25 in the case of the 8.75% Series A Term Preferred Shares and $1,000 in the case of the 7.125% Series B Convertible Preferred Shares).

(3) The amount to which such class of senior security would be entitled upon our involuntary liquidation in preference to any security junior to it.

(4) The average market value per unit is calculated by taking the average of the closing price of the 8.75% Series A Term Preferred Shares (NYSE: CCIA) for each day during the year for which it was listed on the NYSE. Not applicable for the 7.125% Series B Convertible Preferred Shares.

See accompanying Notes to Financial Statements.

CARLYLE CREDIT INCOME FUND

NOTES TO FINANCIAL STATEMENTS

1. ORGANIZATION

Carlyle Credit Income Fund (the “Fund”) is a non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund was organized as a Delaware statutory trust on April 8, 2011. In addition, the Fund has elected to be treated, and intends to continue to comply with the requirements to qualify annually, as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (together with the rules and regulations promulgated thereunder, the “Code”). The Fund currently has one class of common shares which commenced operations on December 30, 2011. The Fund was previously named Vertical Capital Income Fund (“VCIF”) and was managed by its Adviser, Oakline Advisors LLC (“Oakline”). Effective at the close of business on July 14, 2023, the Fund is managed by its Adviser, Carlyle Global Credit Investment Management L.L.C. (“CGCIM” or the “Adviser”), a wholly owned subsidiary of Carlyle Investment Management L.L.C.

On January 12, 2023, the Fund entered into a definitive agreement (the “Transaction Agreement”) with the Adviser pursuant to which, among other things, CGCIM would become the investment adviser to the Fund (the “Transaction”). Pursuant to the Transaction Agreement, the investment advisory agreement between the Fund and Oakline terminated at or near the closing of the Transaction (the “Closing”). As a result, the holders of the Fund’s common shares (“Shareholders”) were asked to approve a new investment advisory agreement between the Fund and CGCIM and to approve certain other proposals upon which the Closing was conditioned. The Shareholders approved the new Investment Advisory Agreement and the other proposals at a shareholder meeting on June 15, 2023, followed by the Closing, which occurred on July 14, 2023. In connection with Closing, (i) the Fund sold existing investments with a gross asset value equal to approximately 97% of the total gross asset value of such investments as of August 31, 2022, subject to certain exclusions; (ii) CGCIM replaced Oakline as the Fund’s new investment adviser; (iii) the Fund’s investment strategy was changed to invest primarily in debt and equity tranches issued by collateralized loan obligations; (iv) each of the Fund’s trustees and officers were replaced; (v) the Fund changed its name on July 14, 2023 from Vertical Capital Income Fund to Carlyle Credit Income Fund; and (vi) on July 27, 2023 the Fund’s common shares began trading on NYSE under the symbol “CCIF.” In addition, Shareholders of the Fund received a special one-time payment of $10,000,000 from CGCIM (or one of its affiliates), or approximately $0.96 per common share.

Following the closing of the Transaction and pursuant to the Transaction Agreement, (i) CG Subsidiary Holdings L.L.C., an affiliate of the Adviser (the “Purchaser”) commenced a tender offer on July 18, 2023 to purchase up to $25,000,000 of outstanding Fund common shares at the then-current net asset value per common share (the “Tender Offer”), and (ii) the Purchaser agreed to invest $15,000,000 into the Fund through the purchase of newly issued Fund common shares at a price equal to the greater of the then-current net asset value per common share and the net asset value per common share that represents the tender offer purchase price (the “New Issuance”), and through acquiring common shares in private purchases (the “Private Purchase”).

The Tender Offer expired on August 28, 2023, and the Purchaser accepted for purchase 3,012,049 common shares at a purchase price of $8.30 per common share for an aggregate purchase price of $25,000,007, excluding fees and expenses relating to the Tender Offer.

On September 12, 2023, the Fund closed the New Issuance and issued and sold 1,269,537 common shares to the Purchaser at a purchase price of $8.52 per common share, which price represented the net asset value per common share as of the closing of the New Issuance, for an aggregate purchase price of $10,816,451.

On September 12, 2023, the Purchaser closed the Private Purchase and acquired 504,042 common shares from existing shareholders of the Fund.

Prior to the close of business on July 14, 2023, the Fund’s investment objective was to generate income by primarily investing in mortgage notes secured by residential real estate. Following the closing of the Transaction, the Fund’s primary investment objective is to generate current income, with a secondary objective to generate capital appreciation. The Fund seeks to achieve its investment objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations (“CLO”) that are collateralized by a portfolio consisting primarily of below investment grade U.S. senior secured loans with a large number of distinct underlying borrowers across various industry sectors. The Fund may also invest in other related securities and instruments or other securities and instruments that the Adviser believes are consistent with its investment objectives, including senior debt tranches of CLOs, loan accumulation facilities (“LAFs”) and securities issued by other securitization vehicles, such as collateralized bond obligations, or “CBOs.” LAFs are short- to medium-term facilities often provided by the bank that will serve as the placement agent or arranger on a CLO transaction. LAFs typically incur leverage between four and six times equity value prior to a CLO’s pricing. The CLO securities in which the Fund primarily seek to invest are unrated or rated below investment grade and are considered speculative with respect to timely payment of interest and repayment of principal. Unrated and below investment grade securities are also sometimes referred to as “junk” securities. In addition, the CLO equity and junior debt securities in which the Fund invests are highly leveraged (with CLO equity securities typically being leveraged ten times), which magnifies the Fund’s risk of loss on such investments.

CARLYLE CREDIT INCOME FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

To qualify as a RIC, the Fund must, among other things, meet certain source-of-income and asset diversification requirements and timely distribute to its shareholders generally at least 90% of its investment company taxable income, as defined by the Code, for each year. Pursuant to this election, the Fund generally does not have to pay corporate level taxes on any income that it distributes to shareholders, provided that the Fund satisfies those requirements.

2. SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The financial statements have been prepared on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”). The Fund is an investment company for the purposes of accounting and financial reporting in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services—Investment Companies (“ASC 946”). U.S. GAAP for an investment company requires investments to be recorded at fair value. With the exception of the line item entitled “preferred shares” which is reported at amortized cost, the carrying value for all other assets and liabilities approximates their fair value. The Fund’s fiscal year ends on September 30, and unless otherwise noted, references to fiscal year or year are for fiscal years ended September 30.

Use of Estimates

The preparation of the financial statements in conformity with U.S. GAAP requires management to make assumptions and estimates that affect the reported amounts reported in the financial statements and accompanying notes. Management’s estimates are based on historical experiences and other factors, including expectations of future events that management believes to be reasonable under the circumstances. It also requires management to exercise judgment in the process of applying the Fund’s accounting policies.

Investments

Investment transactions are recorded as of the applicable trade date. Realized gains or losses are measured by the difference between the net proceeds from the repayment or sale and the amortized cost basis of the investment using the specific identification method without regard to unrealized appreciation or depreciation previously recognized, and includes investments charged off during the period, net of recoveries. Net change in unrealized appreciation or depreciation on investments as presented in the accompanying Statement of Operations reflects the net change in the fair value of investments, including the reversal of previously recorded unrealized appreciation or depreciation when gains or losses are realized. See Note 3. Fair Value Measurements, for further information.

Cash and Cash Equivalents

Cash and cash equivalents consist of demand deposits and highly liquid investments (e.g., money market funds, U.S. treasury notes) with original maturities of three months or less. The Fund’s cash and cash equivalents are held at one or more large financial institutions and cash held in such financial institutions may, at times, exceed the Federal Deposit Insurance Corporation insured limit. The Fund classifies cash equivalents as Level I in the fair value hierarchy. Cash equivalents are carried at cost or amortized cost which approximates fair value.

Interest from Investments

CLO equity investments recognize investment income by utilizing an effective interest methodology based upon an effective yield to maturity utilizing projected cash flow, as required by ASC Topic 325-40, Beneficial Interest in Securitized Financial Assets. The Fund monitors the expected residual payments, and effective yield is determined and updated periodically, as needed. Accordingly, investment income recognized on CLO equity securities in the U.S. GAAP statement of operations differs from both the tax-basis investment income and from the cash distributions actually received by the Fund during the quarterly period.