UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(D) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported):

December 2, 2024

Cartica Acquisition Corp

(Exact name of registrant as specified in its

charter)

| Cayman Islands |

|

001-41198 |

|

N/A |

(State or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(I.R.S. Employer

Identification No.) |

|

1345 Avenue of the Americas, 11th Floor

New York, NY

(Address of principal executive offices)

|

10105

(Zip Code) |

+1

(202) 741-3677

(Registrant’s telephone number, including

area code)

Not Applicable

(Former name or former address, if changed

since last report)

Check the appropriate box below if the Form 8-K is intended to simultaneously satisfy the filing obligation of the Registrant under any

of the following provisions:

| x |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| x |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ¨ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ¨ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange

on which registered |

| Units, each consisting of one Class A Ordinary Share and one-half of one Redeemable Warrant |

|

CITEU |

|

The Nasdaq Stock Market LLC |

| |

|

|

|

|

| Class A Ordinary Shares, par value $0.0001 per share |

|

CITE |

|

The Nasdaq Stock Market LLC |

| |

|

|

|

|

| Redeemable Warrants |

|

CITEW |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the

Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company x

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Item 7.01 Regulation FD Disclosure.

As

previously disclosed, on June 24, 2024, Cartica Acquisition Corp, a Cayman Islands exempted company (“Cartica”), entered

into an Agreement and Plan of Merger (as it may be amended, supplemented or otherwise modified from time to time, the “Business

Combination Agreement”), by and among Cartica, Nidar Infrastructure Limited, a Cayman Islands exempted company (“Nidar”),

and Yotta Data and Cloud Limited, a Cayman Islands exempted company and a wholly owned subsidiary of Nidar (“Merger Sub”).

Pursuant to the Business Combination Agreement, Merger Sub will merge with and into Cartica (such merger, the “First Merger”),

with Cartica surviving the First Merger as a wholly owned subsidiary of Nidar (Cartica, as the surviving entity of the First Merger, the

“Surviving Entity”). Immediately following the consummation of the First Merger, the Surviving Entity will merge with

and into Nidar (such merger, the “Second Merger”), with Nidar surviving the Second Merger (such

company, as the surviving entity of the Second Merger, the “Surviving Company”

and, such transactions, collectively, the “Business Combination”).

Attached

hereto as Exhibit 99.1 and incorporated by reference herein is an investor presentation, which provides an overview of Nidar and certain

information regarding the Business Combination and supersedes the investor presentation included as Exhibit 99.2 to the Current Report

on Form 8-K filed by Cartica with the Securities and Exchange Commission (“SEC”) on June 24, 2024.

In accordance

with General Instructions B.2 and B.6 of Form 8-K, Exhibit 99.1 shall not be deemed “filed” for purposes of Section 18

of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of

that section, nor shall they be deemed incorporated by reference into any filing made by Cartica or Nidar under the Exchange Act or the

Securities Act of 1933, as amended (the “Securities Act”), except as shall be expressly set forth by specific reference

in such a filing.

Forward-Looking Statements

This

Current Report on Form 8-K includes “forward-looking statements” within the meaning of the “safe harbor” provisions

of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of words

such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,”

“expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions

that predict or indicate future events or trends or that are not statements of historical matters, but the absence of these words does

not mean that a statement is not forward-looking. Such statements may include, but are not limited to, statements regarding the Business

Combination and certain agreements entered into in connection therewith. The forward-looking statements contained in this Current Report

on Form 8-K reflect Cartica’s current views about future events and are subject to numerous known and unknown risks, uncertainties,

assumptions and changes in circumstances that may cause its actual results to differ significantly from those expressed in any forward-looking

statement. Cartica does not guarantee that the transactions and events described will happen as described (or that they will happen at

all). In particular, there can be no assurance that the Business Combination will close in a timely manner or at all. These forward-looking

statements are subject to a number of risks and uncertainties, including, but not limited to, changes in domestic and foreign business,

market, financial, political, and legal conditions; the occurrence of any event, change or other circumstances that could give rise to

the termination of the Business Combination; the outcome of any legal proceedings that may be instituted against Cartica, Nidar, the Surviving

Company or others following the announcement of the Business Combination; the inability of Nidar to obtain commitments from third parties

to make private investments in public equity in the form of Nidar’s

ordinary shares in the amount contemplated by the Business Combination Agreement; the amount of redemptions by Cartica’s

public shareholders in connection with the Business Combination; the inability to complete the Business Combination due to the failure

to obtain approval of the shareholders of Cartica or to satisfy other conditions to closing; changes to the proposed structure of the

Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining

regulatory approval of the Business Combination; the ability to meet the applicable stock exchange listing standards following the consummation

of the Business Combination; the risk that the Business Combination disrupts current plans and operations of Nidar as a result of the

announcement and consummation of the Business Combination; the ability to recognize the anticipated benefits of the Business Combination,

which may be affected by, among other things, competition and the ability of the Surviving Company to grow and manage growth profitably,

maintain relationships with customers and retain its management and key employees; costs related to the Business Combination; changes

in applicable laws or regulations; Nidar’s estimates of expenses and profitability and underlying assumptions with respect to shareholder

redemptions and purchase price and other adjustments; any downturn or volatility in economic conditions; changes in the competitive environment

affecting Nidar or its customers, including Nidar’s inability to introduce new services or technologies; the impact of pricing pressure

and erosion; supply chain risks; risks to Nidar’s ability to protect its intellectual property and avoid infringement by others,

or claims of infringement against Nidar; the possibility that Cartica or Nidar may be adversely affected by other economic, business and/or

competitive factors; Nidar’s estimates of its financial performance; and other risks and uncertainties set forth in the sections

entitled “Risk Factors” and “Forward Looking Statements” in the Registration Statement (as defined below) and

in reports Cartica files with the SEC. If any of these risks materialize or Cartica’s assumptions prove incorrect, actual results

could differ materially from the results implied by these forward-looking statements. While forward-looking statements reflect Cartica’s

good faith beliefs, they are not guarantees of future performance. Cartica disclaims any obligation to publicly update or revise any forward-looking

statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes after

the date of this Current Report on Form 8-K, except as required by applicable law. You should not place undue reliance on any forward-looking

statements, which are based only on information currently available to Cartica.

Additional Information and Where to Find It

In connection with the Business Combination, Cartica

and Nidar prepared, and Nidar has filed, a Registration Statement on Form F-4 (the “Registration Statement”) containing

a proxy statement/prospectus and certain other related documents, which will be both the proxy statement to be distributed to Cartica’s

shareholders in connection with Cartica’s solicitation of proxies for the vote by Cartica’s shareholders with respect to the

Business Combination and other matters as may be described in the Registration Statement, as well as the prospectus relating to the offer

and sale of the securities to be issued in connection with the Business Combination. Once the Registration Statement is declared effective,

Cartica will mail the definitive proxy statement/prospectus and other relevant documents to its shareholders as of a record date to be

established for voting on the Business Combination. This Current Report on Form 8-K is not a substitute for the Registration Statement,

the definitive proxy statement/prospectus or any other document that Cartica will send to its shareholders in connection with the Business

Combination. Investors and security holders are urged to read the preliminary proxy statement/prospectus in connection with Cartica’s

solicitation of proxies for its Extraordinary General Meeting to be held to approve the Business Combination (and related matters) and,

when available, general amendments thereto and the definitive proxy statement/prospectus because the proxy statement/prospectus contains

important information about the Business Combination and the parties to the Business Combination.

Copies

of the preliminary proxy statement/prospectus and, once available, the definitive proxy statement/prospectus and other documents filed

by Cartica or Nidar with the SEC may be obtained free of charge at the SEC’s website at www.sec.gov.

Investors

and security holders will be able to obtain free copies of the Registration Statement, the proxy statement/prospectus and all other relevant

documents filed or that will be filed with the SEC by Cartica or Nidar through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

Cartica and its directors,

executive officers, other members of management, and employees, under SEC rules, may be deemed to be participants in the solicitation

of proxies of Cartica’s shareholders in connection with the Business Combination. Information regarding the persons who may, under

SEC rules, be deemed participants in the solicitation of Cartica’s shareholders in connection with the Business Combination is in

the Registration Statement, including the preliminary proxy statement/prospectus. Investors and security holders may obtain more detailed

information regarding the names and interests in the Business Combination of Cartica’s directors and officers in Cartica’s

filings with the SEC and such information is also in the Registration Statement, which includes the preliminary proxy statement/prospectus

of Cartica for the Business Combination. These documents can be obtained free of charge at the SEC’s website at www.sec.gov.

Nidar and its directors

and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of Cartica in connection

with the Business Combination. A list of the names of such directors and executive officers and information regarding their interests

in the Business Combination is included in the Registration Statement, which includes the preliminary proxy statement/prospectus for the

Business Combination.

No Offer or Solicitation

This Current

Report on Form 8-K relates to the Business Combination and is neither an offer to purchase, nor a solicitation of an offer to sell, subscribe

for or buy any securities or the solicitation of any vote in any jurisdiction pursuant to the Business Combination or otherwise, nor shall

there be any sale, issuance or transfer or securities in any jurisdiction in contravention of applicable law. No offer of securities shall

be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act or an exemption therefrom, and otherwise

in accordance with applicable law.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits.

| |

|

|

Exhibit

No. |

|

Description |

| |

|

|

| 99.1 |

|

Investor

Presentation |

| |

|

| 104 |

|

Cover Page Interactive Data File (embedded within the Inline XBRL document).

|

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934,

the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| |

CARTICA ACQUISITION CORP |

| |

|

|

| Date: December 2, 2024 |

By: |

/s/ Suresh Guduru |

| |

Name: |

Suresh Guduru |

| |

Title: |

Chairman and Chief Executive Officer |

Exhibit 99.1

| INDIA’S LEADING DATA CENTER PROVIDER

FOR AI AND HIGH PERFORMANCE COMPUTE |

| CONFIDENTIAL | 2

DISCLAIMERS

This “Presentation” is for informational purposes only. Refer to the Glossary on Slide 58 of this Presentation for certain defined terms used herein. This Presentation shall not constitute an offer to sell, or the solicitation of an offer to buy, any

securities, nor shall there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful. This Presentation has been prepared to assist interested parties in making their own evaluation with

respect to a potential business combination between Cartica Acquisition Corp (“Cartica”) and Nidar Infrastructure Limited (together with its subsidiaries, “Nidar”) and the related transactions (the “Proposed Business Combination”) and for

no other purpose. These materials are exclusively for the use of the party or the parties to whom they have been provided by representatives of Cartica and Nidar. This Presentation supersedes and replaces all previous oral or written

communications relating to the subject matter hereof. Information disclosed in this Presentation is current as of September 30, 2024, except as otherwise provided herein, and neither Nidar nor Cartica undertakes or agrees to update this

Presentation after the date hereof. By your acceptance of this Presentation, you acknowledge that applicable securities laws restrict a person from purchasing or selling securities of a person with tradeable securities and from communicating

such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities. Certain information included herein describes or assumes the expected terms that will

be included in the agreements to be entered into by the parties to the Proposed Business Combination. Such agreements are under negotiation and subject to change. The consummation of the Proposed Business Combination is also subject to

other various risks and contingencies, including customary closing conditions. There can be no assurance that the Proposed Business Combination will be consummated with the terms described herein or otherwise. As such, the subject matter

of these materials is evolving and is subject to further change by Cartica and Nidar in their joint and absolute discretion. Neither the U.S. Securities and Exchange Commission (“SEC”) nor any securities commission of any other U.S. or non-U.S. jurisdiction has approved or disapproved of the Proposed Business Combination presented herein or determined that this Presentation is truthful or complete. No representations or warranties, express or implied, are given in, or in

respect of, this Presentation, and no person may rely on any of the information or projections contained herein. To the fullest extent permitted by law, in no circumstances will Cartica, Nidar, any placement agent, any financial advisor or any

of their respective subsidiaries, shareholders, affiliates, representatives, directors, officers, employees, advisers or agents be responsible or liable, including for a direct, indirect or consequential loss or loss of profit arising from the use of this

Presentation, its contents, its omissions, reliance on the information contained within it, or any opinions communicated in relation thereto or otherwise arising in connection therewith.

Forward-Looking Statements

This Presentation includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995.

Forward-looking statements may be identified by the use of words such as “estimate,” plan,” project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions that predict or indicate future

events or trends that are not statements of historical matters, but the absence of these words does not mean that a statement is not forward-looking. These forward-looking statements include, but are not limited to, statements regarding

expectations of Nidar or Cartica concerning the outlook for their business, productivity, plans and goals for future operational improvements and capital investments, operational performance, future market conditions or economic

performance and developments in the capital and credit markets, as well as any information concerning possible, assumed, estimated or expected future operations and future financial performance of Nidar and Yotta Data Services. Forward-looking statements also include statements regarding the expected benefits of the Proposed Business Combination. These statements are based on various assumptions, whether or not identified in this Presentation, and on the current

expectations of management of Cartica, Nidar and Cartica Acquisitions Partners, LLC (the “Sponsor”) and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not

intended to serve as and must not be relied on by any investor as a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from

assumptions. Many actual events and circumstances are beyond the control of Cartica, Nidar and the Sponsor. You should carefully consider the risks and uncertainties set forth in the sections entitled “Risk Factors” and “Cautionary Note

Regarding Forward-Looking Statements” in Cartica’s final prospectus relating to its initial public offering dated January 4, 2022, and its Annual Report on Form 10-K for the fiscal year ended December 31, 2023. In addition, there are risks and

uncertainties described in the Registration Statement on Form F-4 filed with the SEC on November 13, 2024, by Nidar in connection with the Proposed Business Combination (as amended from time to time, the “Registration Statement”) and

in the other documents filed by Nidar from time to time with the SEC. These filings would identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the

forward-looking statements. These forward-looking statements are subject to a number of risks and uncertainties, including, but not limited to, changes in domestic and foreign business, market, financial, political, and legal conditions; the

inability of the parties to successfully or timely consummate the Proposed Business Combination, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could

materially and adversely affect the combined company or the expected benefits of the Proposed Business Combination or that the approval of shareholders is not obtained; failure to realize the anticipated benefits of the Proposed Business

Combination; risks relating to the uncertainty of the projected financial information with respect to Nidar; any downturn or volatility in economic conditions, including inflation; risks related to the rollout of Nidar’s business and the timing of

expected business milestones, and to relationships with customers; the effects of competition on Nidar’s future business; risks related to Nidar’s ability to protect its intellectual property and avoid infringement by others, or claims of

infringement against it; disruption of Nidar’s relationships with its customers, business partners and others resulting from the announcement of the Proposed Business Combination; the amount of redemption requests made by Cartica’s public

shareholders; the ability of Cartica or the combined company to issue equity or equity-linked securities in connection with the Proposed Business Combination or in the future. If any of these risks materialize or Nidar’s assumptions prove

incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither Cartica nor Nidar presently know or that they currently believe are immaterial that could

also cause actual results to differ, potentially materially, from those contained in or implied by the forward-looking statements. In addition, forward-looking statements reflect Cartica’s and Nidar’s expectations, plans or forecasts of future

events and views as of the date of this Presentation. There may be additional risks that Cartica and Nidar do not presently know or that they currently believe are immaterial that could also cause actual results to differ from those contained in

the forward-looking statements. While Cartica or Nidar may elect to update these forward-looking statements at some point in the future, Cartica and Nidar specifically disclaim any obligation to do so. These forward-looking statements should

not be relied upon as representing Cartica’s or Nidar’s assessments as of any date subsequent to the date of this Presentation. Accordingly, undue reliance should not be placed upon the forward-looking statements. |

| CONFIDENTIAL | 3

DISCLAIMERS (CONT’D.)

Financial Information; Non-IFRS Financial Measures

The financial information contained in this Presentation has been taken from, or prepared based on, the historical financial statements of Nidar for the periods presented. Nidar’s historical financial information is prepared in accordance with

international financial reporting standards (“IFRS”). Such information has been audited in accordance with Public Company Oversight Board (“PCAOB”) standards. Certain monetary amounts, percentages and other figures included in this

Presentation have been subject to rounding adjustments. Certain other amounts that appear in this Presentation may not sum due to rounding.

This Presentation includes certain financial measures not presented in accordance with IFRS, including earnings before interest, taxes, depreciation and amortization (“EBITDA”), EBITDA margin, Core Revenue, Core EBITDA, Non-Core

Revenue and Non-Core EBITDA. These non-IFRS financial measures are not measures of financial performance in accordance with IFRS and may exclude items that are significant in understanding and assessing Nidar’s financial results.

Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other measures of profitability, liquidity or performance under IFRS. You should be aware that Nidar’s

presentation of these measures may not be comparable to similarly titled measures used by other companies. Nidar believes these non-IFRS measures of financial results provide useful information to management and investors regarding

certain financial and business trends relating to Nidar’s financial condition and results of operations. A reconciliation of non-IFRS financial measures used in this Presentation to the most directly comparable IFRS financial measures is

included in the Appendix beginning on Slide 57 with respect to historical financial information but is not included with respect to forecasted financial information.

This Presentation contains financial forecasts for Nidar (including Yotta Data Services) with respect to certain financial results for Nidar’s fiscal years through 2026. Neither Cartica’s nor Nidar’s independent auditors have audited, studied,

reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, they did not express an opinion or provide any other form of assurance with respect

thereto for the purpose of this Presentation. These projections are forward-looking statements and should not be relied upon as being necessarily indicative of future results. See “Forward-Looking Statements” on Slide 2 of this Presentation.

In this Presentation, certain of the above-mentioned projected information has been provided for purposes of providing comparisons with historical data. The assumptions and estimates underlying the prospective financial information are

inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information.

Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Nidar or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the

prospective financial information in this Presentation should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

This Presentation also includes certain projections of non-IFRS financial measures, including EBITDA, EBITDA margin, Core Revenue, Core EBITDA, Non-Core Revenue and Non-Core EBITDA. Due to the high variability and difficulty

in making accurate forecasts and projections of some of the information excluded from these projected measures, together with some of the excluded information not being ascertainable or accessible, Nidar is unable to quantify certain

amounts that would be required to be included in the most directly comparable IFRS financial measures without unreasonable effort. Consequently, no disclosure of the projected most directly comparable IFRS measures is included, and no

reconciliation of forward-looking EBITDA and EBITDA margin to the most directly comparable IFRS measures is included.

Industry and Market Data; Trademarks

This Presentation has been prepared by Nidar and Cartica and includes market data and other statistical information from sources believed by Nidar and Cartica to be reliable, including independent industry publications, governmental

publications or other published independent sources. Some data is also based on the good faith estimates of Nidar and Cartica, which are derived from their review of internal sources as well as the independent sources described above. While

Nidar is not aware of any misstatements regarding the industry data presented herein, its estimates involve risks and uncertainties and are subject to change based on various factors. No representations or warranties expressed or implied are

given in, or in respect of, this Presentation. Although Nidar and Cartica believe these sources are reliable, they have not independently verified the information and cannot guarantee its accuracy and completeness. As such, this information is

subject to change. Recipients of this Presentation should not consider its contents, or any prior or subsequent communications from or with Nidar, Cartica or the Sponsor or their respective representatives as investment, legal or tax advice.

Nidar and Cartica own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This Presentation also contains trademarks, service marks and trade

names of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this Presentation is not intended to and does not imply a relationship with

Nidar and Cartica, or an endorsement or sponsorship by or of Nidar and Cartica. Solely for convenience, the trademarks, service marks and trade names referred to in this Presentation may appear without the ®, TM or SM symbols, but such

references are not intended to indicate, in any way, that Nidar and Cartica will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks and trade names.

Additional Information and Where to Find It

This Presentation relates to the Proposed Business Combination. This Presentation does not constitute an offer to sell or exchange, or the solicitation of an offer to buy or exchange, any securities, nor shall there be any sale of securities in any

jurisdiction in which such offer, sale or exchange would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. Nidar has filed the Registration Statement, which includes a proxy statement and

prospectus. The proxy statement/prospectus will be sent to all Cartica shareholders. Nidar and Cartica also will file other documents regarding the proposed transaction with the SEC. Before making any voting decision, investors and security

holders of Cartica are urged to read the Registration Statement, the proxy statement/prospectus and all other relevant documents filed or that will be filed with the SEC in connection with the Proposed Business Combination as they become

available because they will contain important information about the proposed transaction. Investors and security holders will be able to obtain free copies of the proxy statement/prospectus, and all other relevant documents filed or that will be

filed with the SEC by Nidar and/or Cartica through the website maintained by the SEC at www.sec.gov. In addition, the documents filed by Cartica may be obtained free of charge from Cartica’s website at https://carticaspac.com/investor-resources/ or by written request to Cartica at Cartica Acquisition Corp, c/o Morrison & Foerster LLP, 2100 L Street, NW, Suite 900, Washington, DC 20037.

Participants in Solicitation

Cartica, Nidar and their respective directors, managers and officer may be deemed participants in the solicitation of proxies of shareholders in connection with the Proposed Business Combination. Cartica shareholders and other interested

persons may obtain more detailed information regarding the directors, managers and officers of Cartica in Cartica’s filings with the SEC, which may be obtained, without charge, on the website maintained by the SEC at www.sec.gov.

Additional information will be available in the definitive proxy statement included in the Registration Statement when it becomes available.

No Offer or Solicitation

This Presentation relates to the Proposed Business Combination and is neither an offer to purchase, nor a solicitation of an offer to sell, subscribe for or buy any securities or the solicitation of any vote in any jurisdiction pursuant to the

Proposed Business Combination or otherwise, nor shall there be any sale, issuance or transfer or securities in any jurisdiction in contravention of applicable law. No offer of securities shall be made except by means of a prospectus meeting the

requirements of Section 10 of the Securities Act of 1933, as amended (the “Securities Act”), or an exemption therefrom, and otherwise in accordance with applicable law.

Risk Factors

For a description of the risks relating to Nidar, Yotta Data Services, Cartica and the Proposed Business Combination, please see the “Risk Factors” in the Appendix to this Presentation. |

| TABLE OF CONTENTS

I. INTRODUCTION & OPPORTUNITY OVERVIEW

II. KEY INVESTMENT HIGHLIGHTS

III. BUSINESS OVERVIEW

I. DATA CENTERS

II. AI SERVICES

IV. FINANCIAL OVERVIEW

V. APPENDIX

TABLE OF CONTENTS |

| I. INTRODUCTION & OPPORTUNITY OVERVIEW |

| CONFIDENTIAL | 6

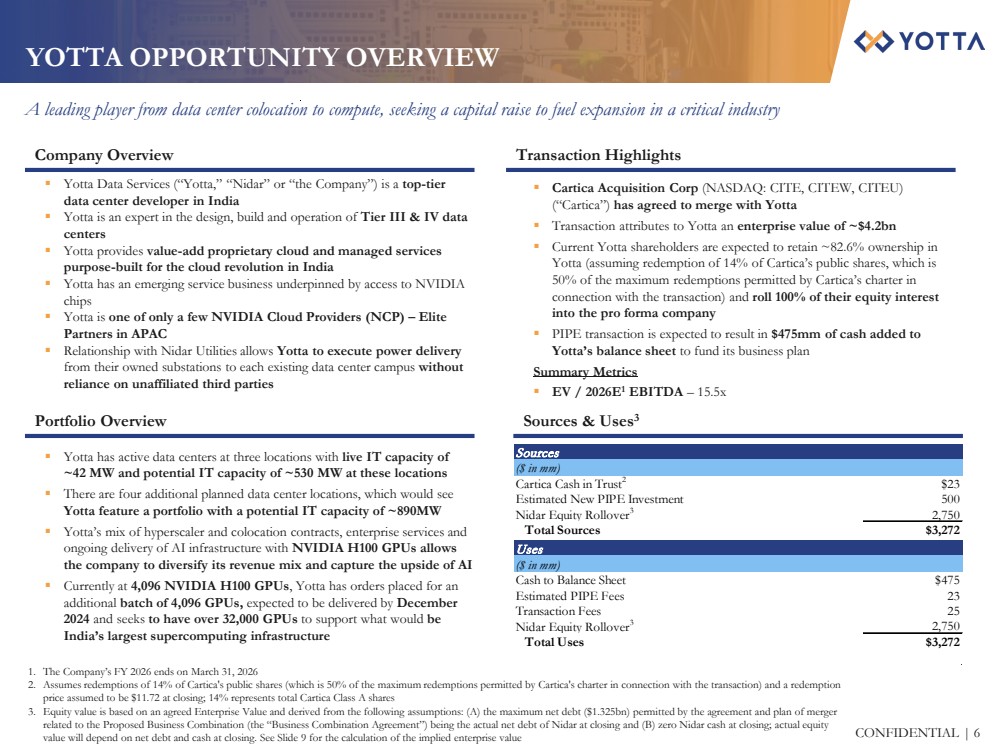

YOTTA OPPORTUNITY OVERVIEW

A leading player from data center colocation to compute, seeking a capital raise to fuel expansion in a critical industry

1. The Company’s FY 2026 ends on March 31, 2026

2. Assumes redemptions of 14% of Cartica's public shares (which is 50% of the maximum redemptions permitted by Cartica's charter in connection with the transaction) and a redemption

price assumed to be $11.72 at closing; 14% represents total Cartica Class A shares

3. Equity value is based an agreed Enterprise Value and derived on the following assumptions: (A) the maximum net debt ($1.325bn) permitted by the agreement and plan of merger

related to the Proposed Business Combination (the “Business Combination Agreement”) being the actual net debt of Nidar at closing and (B) zero Nidar cash at closing; actual equity

value will depend on net debt and cash at closing. See Slide 9 for the calculation of the implied enterprise value

Transaction Highlights

Sources & Uses3

Company Overview

Portfolio Overview

Yotta Data Services (“Yotta,” “Nidar” or “the Company”) is a top-tier

data center developer in India

Yotta is an expert in the design, build and operation of Tier III & IV data

centers

Yotta provides value-add proprietary cloud and managed services

purpose-built for the cloud revolution in India

Yotta has an emerging service business underpinned by access to NVIDIA

chips

Yotta is one of only a few NVIDIA Cloud Providers (NCP) – Elite

Partners in APAC

Relationship with Nidar Utilities allows Yotta to execute power delivery

from their owned substations to each existing data center campus without

reliance on unaffiliated third parties

Yotta has active data centers at three locations with live IT capacity of

~42 MW and potential IT capacity of ~530 MW at these locations

There are four additional planned data center locations, which would see

Yotta feature a portfolio with a potential IT capacity of ~890MW

Yotta’s mix of hyperscaler and colocation contracts, enterprise services and

ongoing delivery of AI infrastructure with NVIDIA H100 GPUs allows

the company to diversify its revenue mix and capture the upside of AI

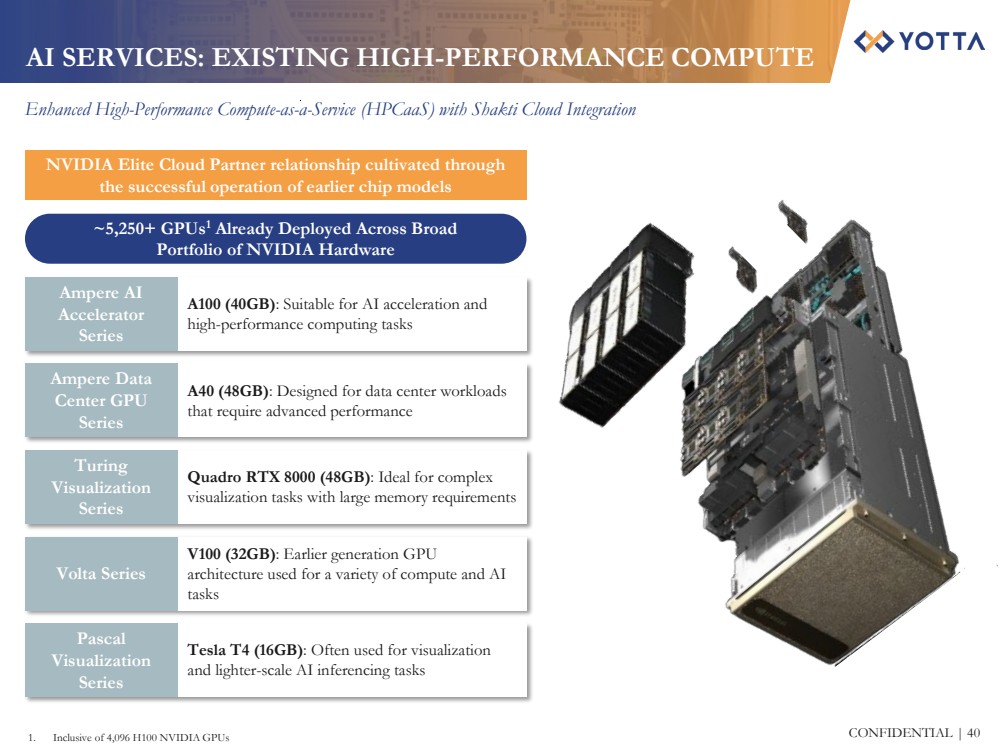

Currently at 4,096 NVIDIA H100 GPUs, Yotta has orders placed for an

additional batch of 4,096 GPUs, expected to be delivered by December

2024 and seeks to have over 32,000 GPUs to support what would be

India’s largest supercomputing infrastructure

Cartica Acquisition Corp (NASDAQ: CITE, CITEW, CITEU)

(“Cartica”) has agreed to merge with Yotta

Transaction attributes to Yotta an enterprise value of ~$4.2bn

Current Yotta shareholders are expected to retain ~82.6% ownership in

Yotta (assuming redemption of 14% of Cartica’s public shares, which is

50% of the maximum redemptions permitted by Cartica’s charter in

connection with the transaction) and roll 100% of their equity interest

into the pro forma company

PIPE transaction is expected to result in $475mm of cash added to

Yotta’s balance sheet to fund its business plan

Summary Metrics

EV / 2026E1 EBITDA – 15.5x

Sources

($ in mm)

$23

500

2,750

$3,272

Uses

($ in mm)

$475

23

25

2,750

$3,272

Transaction Fees

Nidar Equity Rollover3

Total Uses

Estimated PIPE Fees

Cartica Cash in Trust2

Estimated New PIPE Investment

Nidar Equity Rollover3

Total Sources

Cash to Balance Sheet |

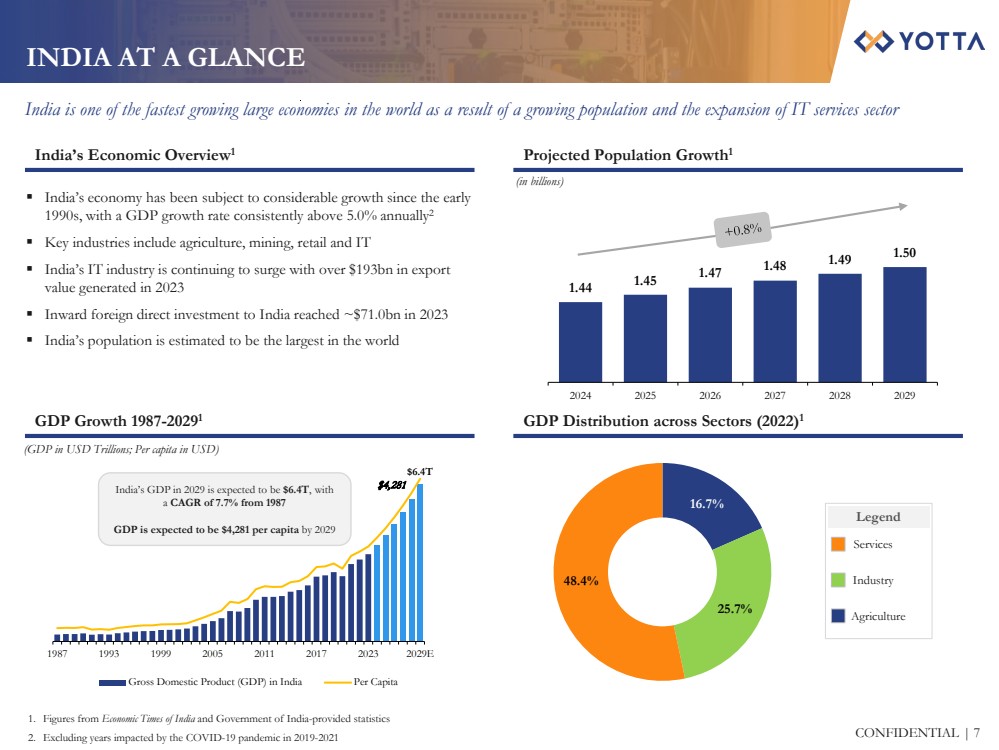

| CONFIDENTIAL | 7

1.44 1.45 1.47 1.48 1.49 1.50

2024 2025 2026 2027 2028 2029

$6.4T

$4,281

1987 1993 1999 2005 2011 2017 2023 2029E

Gross Domestic Product (GDP) in India Per Capita

INDIA AT A GLANCE

India is one of the fastest growing large economies in the world as a result of a growing population and the expansion of IT services sector

16.7%

25.7%

48.4%

1. Figures from Economic Times of India and Government of India-provided statistics

2. Excluding years impacted by the COVID-19 pandemic in 2019-2021

Projected Population Growth1

GDP Distribution across Sectors (2022)1

India’s Economic Overview1

GDP Growth 1987-20291

India’s economy has been subject to considerable growth since the early

1990s, with a GDP growth rate consistently above 5.0% annually2

Key industries include agriculture, mining, retail and IT

India’s IT industry is continuing to surge with over $193bn in export

value generated in 2023

Inward foreign direct investment to India reached ~$71.0bn in 2023

India’s population is estimated to be the largest in the world

(in billions)

(GDP in USD Trillions; Per capita in USD)

Services

Industry

Agriculture

Legend

India’s GDP in 2029 is expected to be $6.4T, with

a CAGR of 7.7% from 1987

GDP is expected to be $4,281 per capita by 2029 |

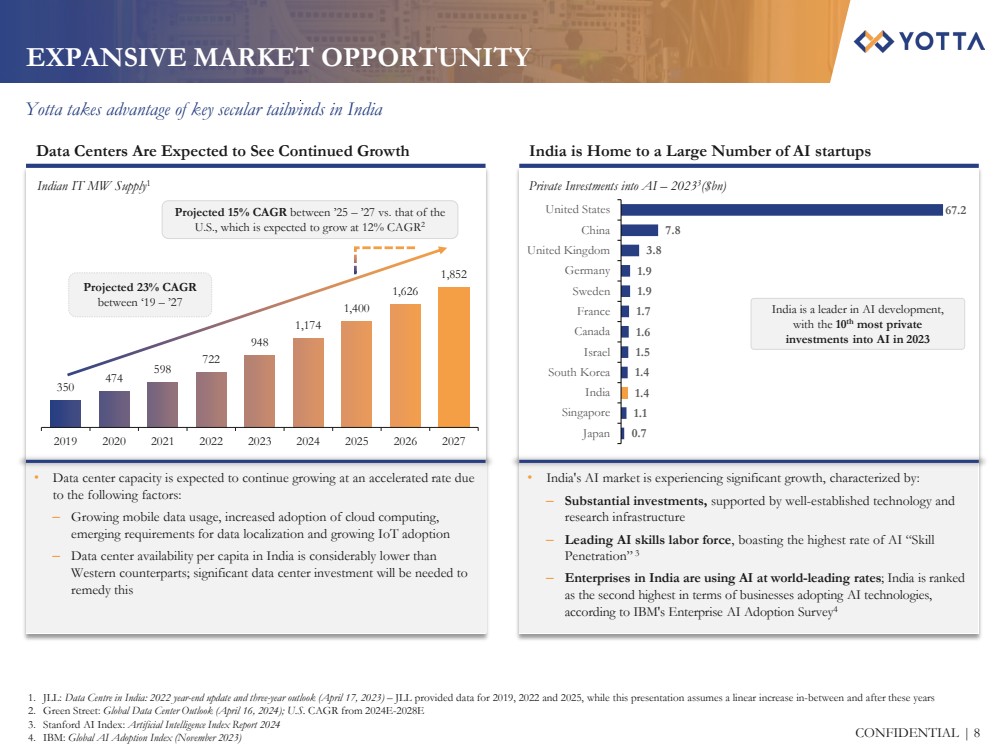

| CONFIDENTIAL | 8

EXPANSIVE MARKET OPPORTUNITY

Yotta takes advantage of key secular tailwinds in India

Data Centers Are Expected to See Continued Growth

India is a leader in AI development,

with the 10th most private

investments into AI in 2023

Indian IT MW Supply1

India is Home to a Large Number of AI startups

Private Investments into AI – 20233($bn)

• India's AI market is experiencing significant growth, characterized by:

‒ Substantial investments, supported by well-established technology and

research infrastructure

‒ Leading AI skills labor force, boasting the highest rate of AI “Skill

Penetration” 3

‒ Enterprises in India are using AI at world-leading rates; India is ranked

as the second highest in terms of businesses adopting AI technologies,

according to IBM's Enterprise AI Adoption Survey4

• Data center capacity is expected to continue growing at an accelerated rate due

to the following factors:

‒ Growing mobile data usage, increased adoption of cloud computing,

emerging requirements for data localization and growing IoT adoption

‒ Data center availability per capita in India is considerably lower than

Western counterparts; significant data center investment will be needed to

remedy this

Projected 15% CAGR between ’25 – ’27 vs. that of the

U.S., which is expected to grow at 12% CAGR2

1. JLL: Data Centre in India: 2022 year-end update and three-year outlook (April 17, 2023) – JLL provided data for 2019, 2022 and 2025, while this presentation assumes a linear increase in-between and after these years

2. Green Street: Global Data Center Outlook (April 16, 2024); U.S. CAGR from 2024E-2028E

3. Stanford AI Index: Artificial Intelligence Index Report 2024

4. IBM: Global AI Adoption Index (November 2023)

0.7

1.1

1.4

1.4

1.5

1.6

1.7

1.9

1.9

3.8

7.8

67.2

Japan

Singapore

India

South Korea

Israel

Canada

France

Sweden

Germany

United Kingdom

China

United States

Projected 23% CAGR

between ‘19 – ’27

350

474

598

722

948

1,174

1,400

1,626

1,852

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2019 2020 2021 2022 2023 2024 2025 2026 2027 |

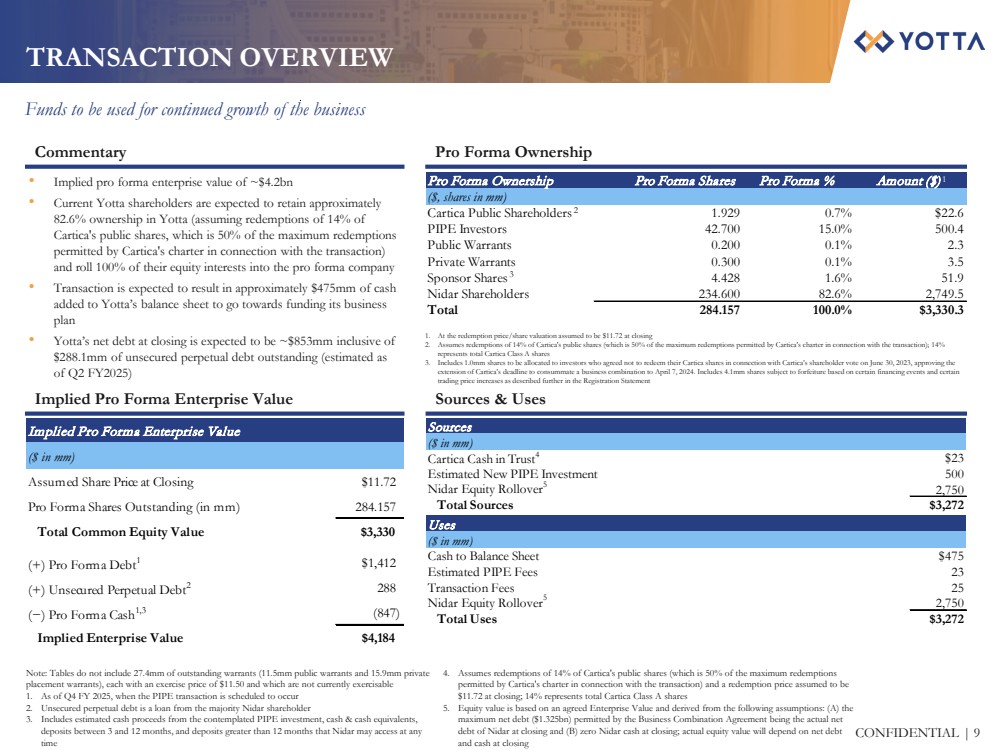

| CONFIDENTIAL | 9

Pro Forma Ownership Pro Forma Shares Pro Forma % Amount ($)

($, shares in mm)

Cartica Public Shareholders 1.929 0.7% $22.6

PIPE Investors 42.700 15.0% 500.4

Public Warrants 0.200 0.1% 2.3

Private Warrants 0.300 0.1% 3.5

Sponsor Shares 4.428 1.6% 51.9

Nidar Shareholders 234.600 82.6% 2,749.5

Total 284.157 100.0% $3,330.3

Sources & Uses

TRANSACTION OVERVIEW

Funds to be used for continued growth of the business

Commentary Pro Forma Ownership

• Implied pro forma enterprise value of ~$4.2bn

• Current Yotta shareholders are expected to retain approximately

82.6% ownership in Yotta (assuming redemptions of 14% of

Cartica's public shares, which is 50% of the maximum redemptions

permitted by Cartica's charter in connection with the transaction)

and roll 100% of their equity interests into the pro forma company

• Transaction is expected to result in approximately $475mm of cash

added to Yotta’s balance sheet to go towards funding its business

plan

• Yotta’s net debt at closing is expected to be ~$853mm inclusive of

$288.1mm of unsecured perpetual debt outstanding (estimated as

of Q2 FY2025)

Implied Pro Forma Enterprise Value

1. At the redemption price/share valuation assumed to be $11.72 at closing

2. Assumes redemptions of 14% of Cartica's public shares (which is 50% of the maximum redemptions permitted by Cartica's charter in connection with the transaction); 14%

represents total Cartica Class A shares

3. Includes 1.0mm shares to be allocated to investors who agreed not to redeem their Cartica shares in connection with Cartica’s shareholder vote on June 30, 2023, approving the

extension of Cartica’s deadline to consummate a business combination to April 7, 2024. Includes 4.1mm shares subject to forfeiture based on certain financing events and certain

trading price increases as described further in the Registration Statement

Note: Tables do not include 27.4mm of outstanding warrants (11.5mm public warrants and 15.9mm private

placement warrants), each with an exercise price of $11.50 and which are not currently exercisable

1. As of Q4 FY 2025, when the PIPE transaction is scheduled to occur

2. Unsecured perpetual debt is a loan from the majority Nidar shareholder

3. Includes estimated cash proceeds from the contemplated PIPE investment, cash & cash equivalents,

deposits between 3 and 12 months, and deposits greater than 12 months that Nidar may access at any

time

4. Assumes redemptions of 14% of Cartica's public shares (which is 50% of the maximum redemptions

permitted by Cartica's charter in connection with the transaction) and a redemption price assumed to be

$11.72 at closing; 14% represents total Cartica Class A shares

5. Equity value is based an agreed Enterprise Value and derived on the following assumptions: (A) the

maximum net debt ($1.325bn) permitted by the Business Combination Agreement being the actual net

debt of Nidar at closing and (B) zero Nidar cash at closing; actual equity value will depend on net debt

and cash at closing

1

2

3

Sources

($ in mm)

$23

500

2,750

$3,272

Uses

($ in mm)

$475

23

25

2,750

$3,272

Estimated PIPE Fees

Transaction Fees

Nidar Equity Rollover5

Total Uses

Cartica Cash in Trust4

Estimated New PIPE Investment

Nidar Equity Rollover5

Total Sources

Cash to Balance Sheet

Implied Pro Forma Enterprise Value

($ in mm)

Assumed Share Price at Closing $11.72

Pro Forma Shares Outstanding (in mm) 284.157

Total Common Equity Value $3,330

(+) Pro Forma Debt1 $1,412

(+) Unsecured Perpetual Debt2 288

(−) Pro Forma Cash1,3 (847)

Implied Enterprise Value $4,184 |

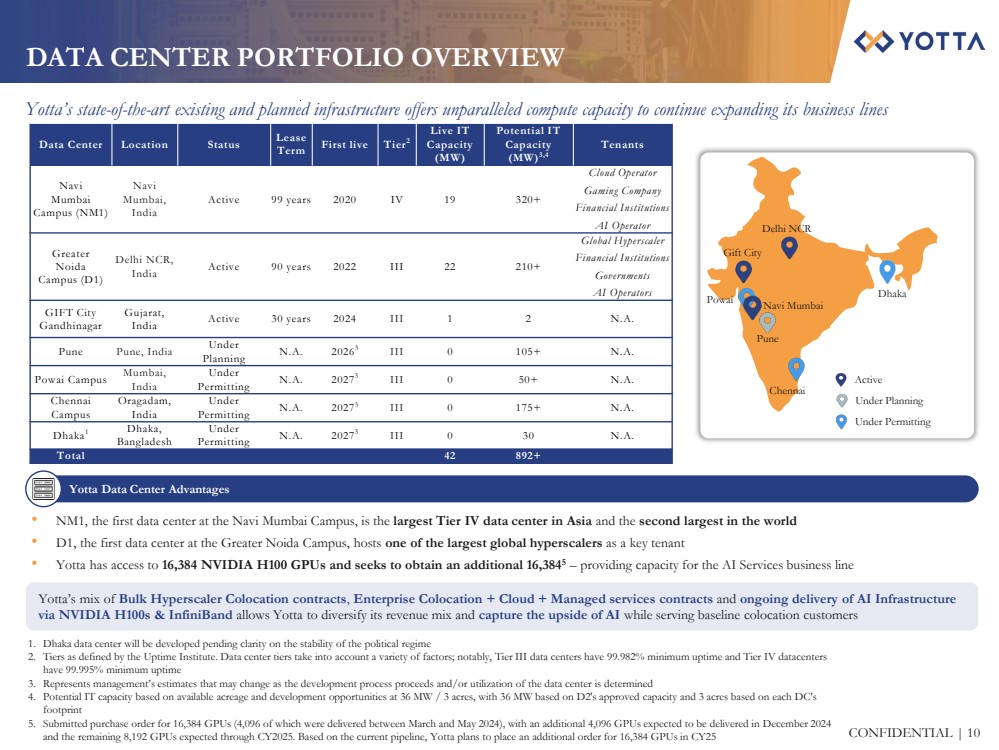

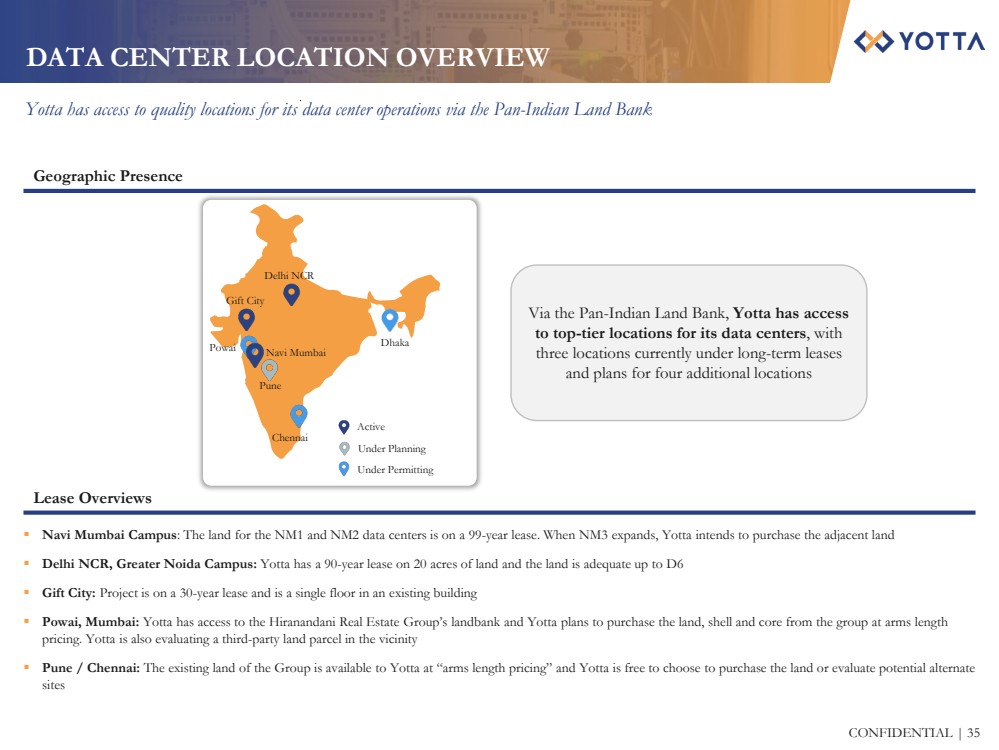

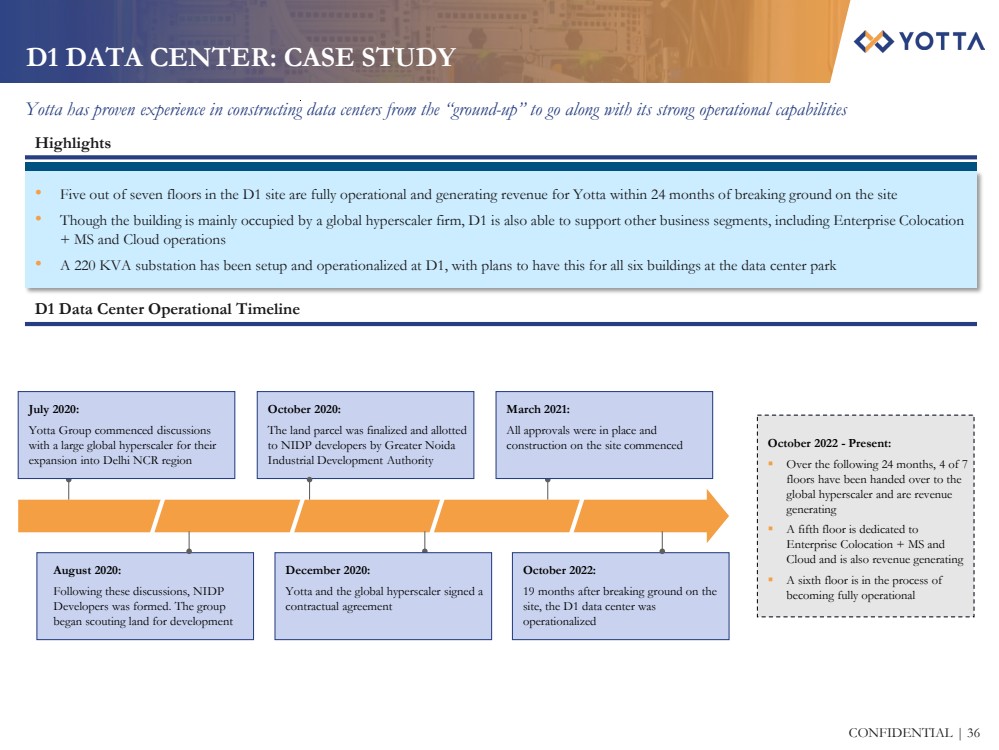

| CONFIDENTIAL | 10

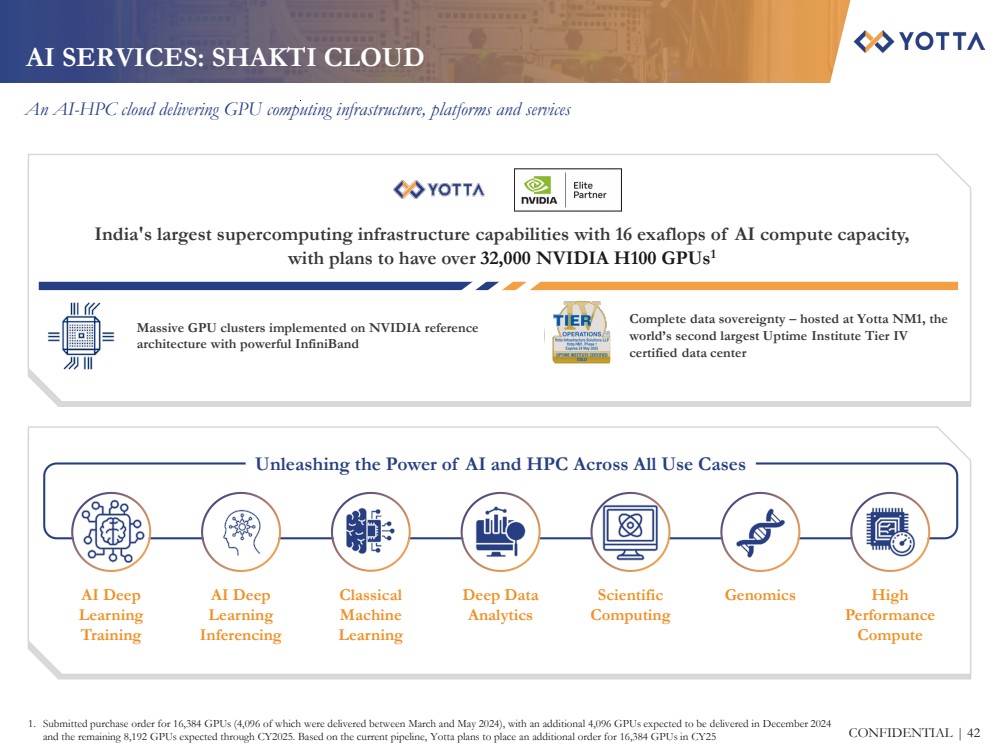

• NM1, the first data center at the Navi Mumbai Campus, is the largest Tier IV data center in Asia and the second largest in the world

• D1, the first data center at the Greater Noida Campus, hosts one of the largest global hyperscalers as a key tenant

• Yotta has access to 16,384 NVIDIA H100 GPUs and seeks to obtain an additional 16,3845 – providing capacity for the AI Services business line

Yotta’s mix of Bulk Hyperscaler Colocation contracts, Enterprise Colocation + Cloud + Managed services contracts and ongoing delivery of AI Infrastructure

via NVIDIA H100s & InfiniBand allows Yotta to diversify its revenue mix and capture the upside of AI while serving baseline colocation customers

DATA CENTER PORTFOLIO OVERVIEW

Yotta’s state-of-the-art existing and planned infrastructure offers unparalleled compute capacity to continue expanding its business lines

Data Center Location Status Lease

Term First live Tier2

Live IT

Capacity

(MW)

Potential IT

Capacity

(MW)3,4

Tenants

Navi

Mumbai

Campus (NM1)

Navi

Mumbai,

India

Active 99 years 2020 IV 19 320+

Cloud Operator

Gaming Company

Financial Institutions

AI Operator

Greater

Noida

Campus (D1)

Delhi NCR,

India Active 90 years 2022 III 22 210+

Global Hyperscaler

Financial Institutions

Governments

AI Operators

GIFT City

Gandhinagar

Gujarat,

India Active 30 years 2024 III 1 2 N.A.

Pune Pune, India Under

Planning N.A. 20263 III 0 105+ N.A.

Powai Campus Mumbai,

India

Under

Permitting N.A. 20273 III 0 50+ N.A.

Chennai

Campus

Oragadam,

India

Under

Permitting N.A. 20273 III 0 175+ N.A.

Dhaka1 Dhaka,

Bangladesh

Under

Permitting N.A. 20273 III 0 30 N.A.

Total 42 892+

1. Dhaka data center will be developed pending clarity on the stability of the political regime

2. Tiers as defined by the Uptime Institute. Data center tiers take into account a variety of factors; notably, Tier III data centers have 99.982% minimum uptime and Tier IV datacenters

have 99.995% minimum uptime

3. Represents management’s estimates that may change as the development process proceeds and/or utilization of the data center is determined

4. Potential IT capacity based on available acreage and development opportunities at 36 MW / 3 acres, with 36 MW based on D2's approved capacity and 3 acres based on each DC's

footprint

5. Submitted purchase order for 16,384 GPUs (4,096 of which were delivered between March and May 2024), with an additional 4,096 GPUs expected to be delivered in December 2024

and the remaining 8,192 GPUs expected through CY2025. Based on the current pipeline, Yotta plans to place an additional order for 16,384 GPUs in CY25

Yotta Data Center Advantages

Navi Mumbai

Chennai

Delhi NCR

Gift City

Pune

Powai

Active

Under Permitting

Under Planning

Dhaka |

| CONFIDENTIAL | 11

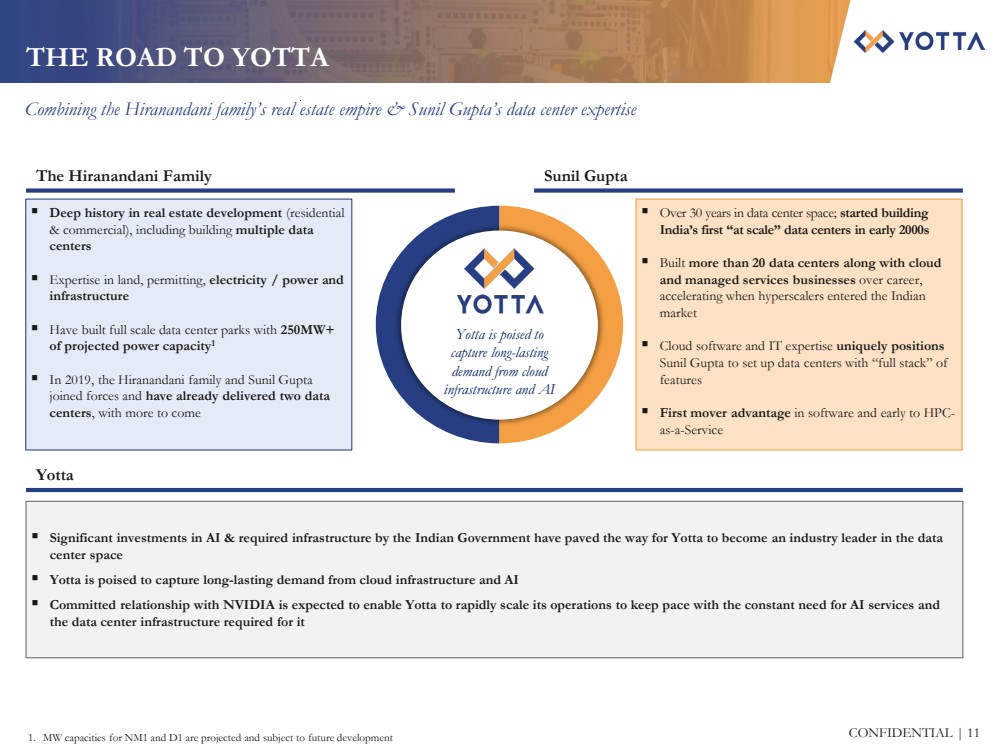

THE ROAD TO YOTTA

Combining the Hiranandani family’s real estate empire & Sunil Gupta’s data center expertise

1. MW capacities for NM1 and D1 are projected and subject to future development

The Hiranandani Family Sunil Gupta

Yotta

Deep history in real estate development (residential

& commercial), including building multiple data

centers

Expertise in land, permitting, electricity / power and

infrastructure

Have built full scale data center parks with 250MW+

of projected power capacity1

In 2019, the Hiranandani family and Sunil Gupta

joined forces and have already delivered two data

centers, with more to come

Over 30 years in data center space; started building

India’s first “at scale” data centers in early 2000s

Built more than 20 data centers along with cloud

and managed services businesses over career,

accelerating when hyperscalers entered the Indian

market

Cloud software and IT expertise uniquely positions

Sunil Gupta to set up data centers with “full stack” of

features

First mover advantage in software and early to HPC-as-a-Service

Significant investments in AI & required infrastructure by the Indian Government have paved the way for Yotta to become an industry leader in the data

center space

Yotta is poised to capture long-lasting demand from cloud infrastructure and AI

Committed relationship with NVIDIA is expected to enable Yotta to rapidly scale its operations to keep pace with the constant need for AI services and

the data center infrastructure required for it

Yotta is poised to

capture long-lasting

demand from cloud

infrastructure and AI |

| CONFIDENTIAL | 12

Strategic 2,000-acre land

bank across India to support

opportunistic investment1

Rated AA-/Stable by

CRISIL, an S&P Company

SPONSORED BY A LEADING REAL ESTATE DEVELOPER

The Hiranandani group has years of experience across India and plans for continual support of Yotta post-transaction

• 2022: Yotta – Data Centre at Delhi NCR brought live

• 2020: Yotta – Data Centre at Navi Mumbai Campus brought live

• 2019: Industrial Park – Partnership with Blackstone for a > $200mm industrial park platform; completed additional 1.2mm sq. ft. of BTS for Tata Consultancy

Services (“TCS”)

• 2019: Yotta - Entry into Data Centre development and management business

• 2017: Hiranandani Energy (“H-Energy”) & Single Large Office Leasing deal with TCS – Construction of West Coast LNG Terminal & 2mm sq. ft. commercial

office space

• 2016: Strategic sale to Brookfield – Sale of commercial office portfolio at Powai township (c. USD 1bn)

• 2015: Data Centre Construction – First DC completed (since then, Hiranandani Group has built 4 of the largest DCs in India for NTT)

• 2014: Panvel Township - Hiranandani Fortune City – Acquisition of Panvel township (600 acres) planned for integrated commercial, retail, residential and data

centers

• 2013: Chennai Township – Hiranandani Parks – Acquisition of Chennai township (330 acres) planned for integrated residential township and potential data centers

• 2012: Dubai 23 Marina – Construction and development of one of the tallest (c.400 m) premium residential towers in Dubai

• 1980s and 1990s: Hiranandani Gardens, Powai (250 acres) and Hiranandani Estate, Thane (315 acres)

1. The Times of India: Niranjan Hiranandani, brother Surendra divide some large joint realty projects in Mumbai region (March 17, 2022)

More than 40 years of

experience as a

diversified conglomerate and

real estate developer with

investment experience through all

sectors, including data centers

One of the largest real

estate companies in India,

pioneer in township and high-quality infrastructure

development

• The Hiranandani Group has been one of the premium real

estate developers in India with 40+ years of experience

• Founded by Niranjan and Surendra Hiranandani in 1978, the

group has a wide range of experience across sales, land

procurement, financial planning, regulatory approvals,

compliance, business development and operational functions

• The Hiranandani family currently has 89.93% of beneficial

ownership of Nidar and will remain the largest

shareholder post-transaction

• Hiranandani Group has infused ~$288mm of capital into the

Nidar group of companies since founding

Hiranandani Group

Timeline

Darshan Hiranandani

Yotta Chairman |

| CONFIDENTIAL | 13

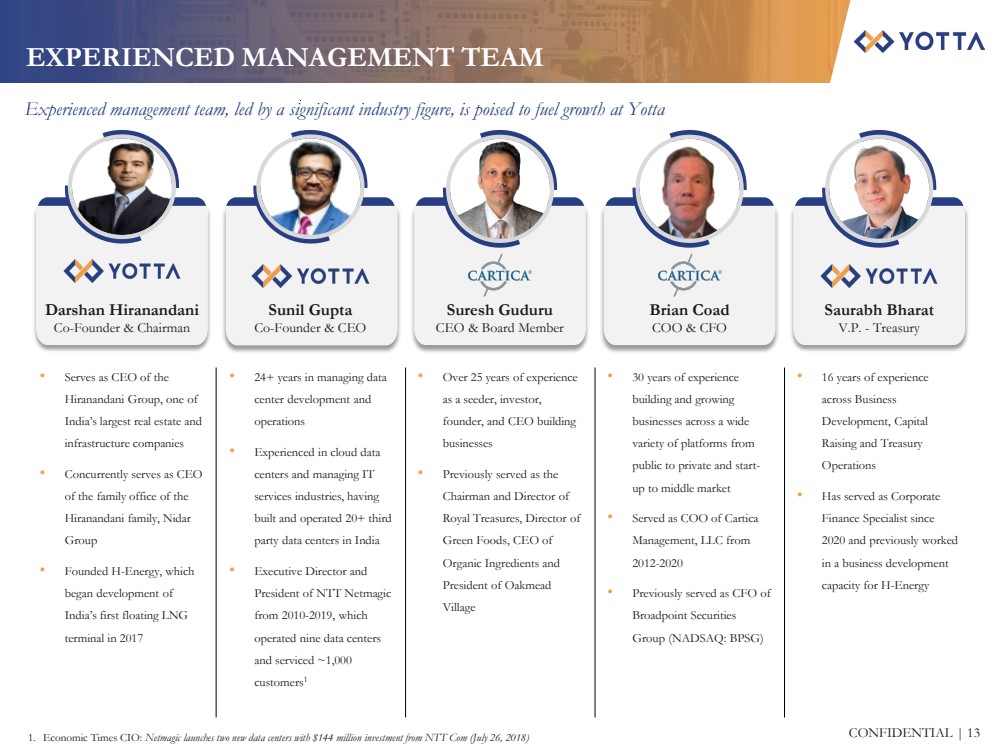

EXPERIENCED MANAGEMENT TEAM

Experienced management team, led by a significant industry figure, is poised to fuel growth at Yotta

• 16 years of experience

across Business

Development, Capital

Raising and Treasury

Operations

• Has served as Corporate

Finance Specialist since

2020 and previously worked

in a business development

capacity for H-Energy

• Over 25 years of experience

as a seeder, investor,

founder, and CEO building

businesses

• Previously served as the

Chairman and Director of

Royal Treasures, Director of

Green Foods, CEO of

Organic Ingredients and

President of Oakmead

Village

• 30 years of experience

building and growing

businesses across a wide

variety of platforms from

public to private and start-up to middle market

• Served as COO of Cartica

Management, LLC from

2012-2020

• Previously served as CFO of

Broadpoint Securities

Group (NADSAQ: BPSG)

• 24+ years in managing data

center development and

operations

• Experienced in cloud data

centers and managing IT

services industries, having

built and operated 20+ third

party data centers in India

• Executive Director and

President of NTT Netmagic

from 2010-2019, which

operated nine data centers

and serviced ~1,000

customers1

1. Economic Times CIO: Netmagic launches two new data centers with $144 million investment from NTT Com (July 26, 2018)

Saurabh Bharat

V.P. - Treasury

Suresh Guduru

CEO & Board Member

Brian Coad

COO & CFO

Sunil Gupta

Co-Founder & CEO

Darshan Hiranandani

Co-Founder & Chairman

• Serves as CEO of the

Hiranandani Group, one of

India’s largest real estate and

infrastructure companies

• Concurrently serves as CEO

of the family office of the

Hiranandani family, Nidar

Group

• Founded H-Energy, which

began development of

India’s first floating LNG

terminal in 2017 |

| CONFIDENTIAL | 14

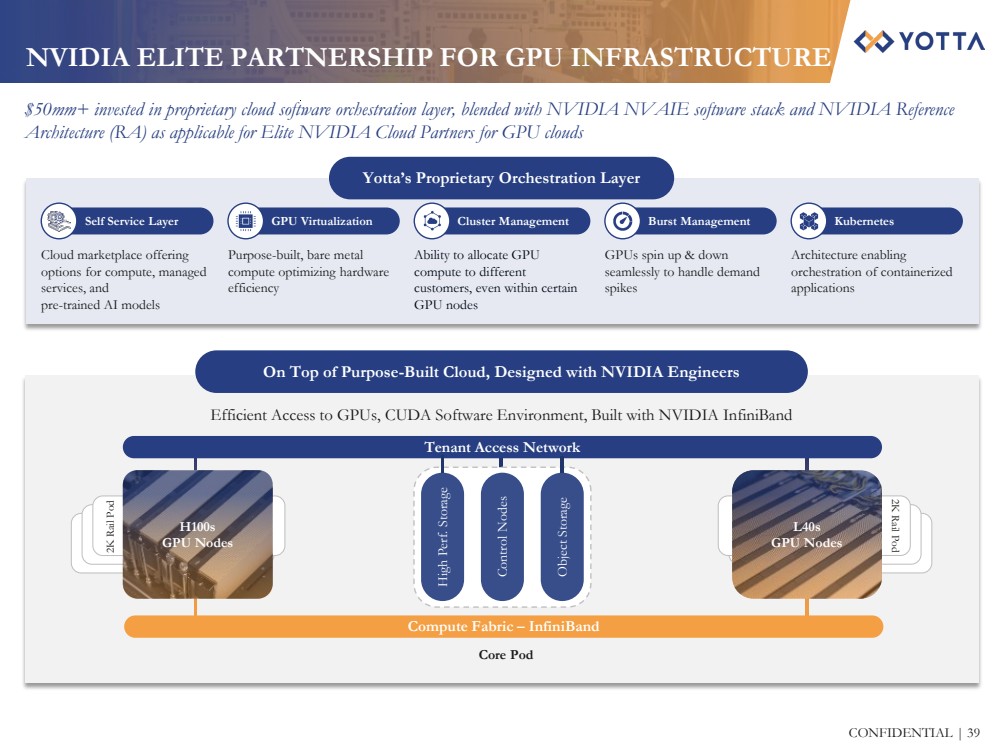

NVIDIA Cloud

Provider (NCP) -

Elite Partner

Designed cloud

compute

infrastructure

alongside NVIDIA

Engineers

c

NVIDIA has shown

deep commitment to

India by entering into

multiple partnerships

to expand its

presence in India’s

growing AI market

Indian government

planning GPU

purchases and

encouraging allocations

to local Indian startups

Jensen Huang’s

meeting with

Prime Minister

Narendra Modi

reaffirms NVIDIA’s

commitment

to India

U.S. restrictions on

GPU exports to China

have positioned India a

priority in GPU

allocations

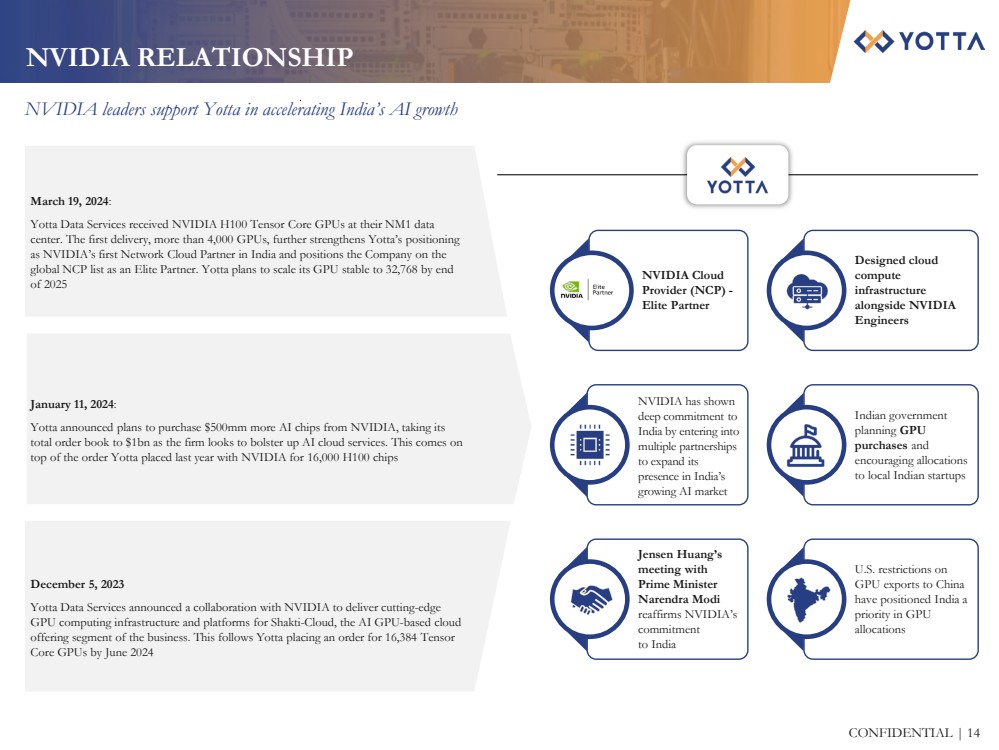

NVIDIA RELATIONSHIP

NVIDIA leaders support Yotta in accelerating India’s AI growth

March 19, 2024:

Yotta Data Services received NVIDIA H100 Tensor Core GPUs at their NM1 data

center. The first delivery, more than 4,000 GPUs, further strengthens Yotta’s positioning

as NVIDIA’s first Network Cloud Partner in India and positions the Company on the

global NCP list as an Elite Partner. Yotta plans to scale its GPU stable to 32,768 by end

of 2025

December 5, 2023

Yotta Data Services announced a collaboration with NVIDIA to deliver cutting-edge

GPU computing infrastructure and platforms for Shakti-Cloud, the AI GPU-based cloud

offering segment of the business. This follows Yotta placing an order for 16,384 Tensor

Core GPUs by June 2024

January 11, 2024:

Yotta announced plans to purchase $500mm more AI chips from NVIDIA, taking its

total order book to $1bn as the firm looks to bolster up AI cloud services. This comes on

top of the order Yotta placed last year with NVIDIA for 16,000 H100 chips |

| II. KEY INVESTMENT HIGHLIGHTS |

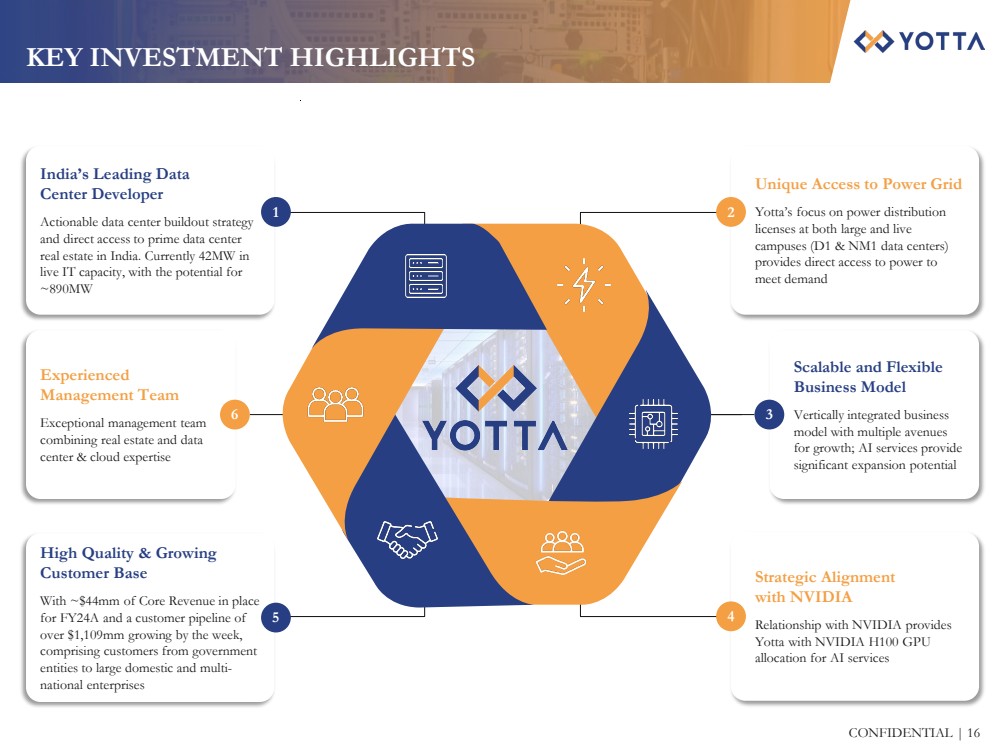

| CONFIDENTIAL | 16

India’s Leading Data

Center Developer

Actionable data center buildout strategy

and direct access to prime data center

real estate in India. Currently 42MW in

live IT capacity, with the potential for

~890MW

Experienced

Management Team

Exceptional management team

combining real estate and data

center & cloud expertise

Strategic Alignment

with NVIDIA

Relationship with NVIDIA provides

Yotta with NVIDIA H100 GPU

allocation for AI services

KEY INVESTMENT HIGHLIGHTS

6

1

2

Unique Access to Power Grid

Yotta’s focus on power distribution

licenses at both large and live

campuses (D1 & NM1 data centers)

provides direct access to power to

meet demand

Scalable and Flexible

Business Model

Vertically integrated business

model with multiple avenues

for growth; AI services provide

significant expansion potential

High Quality & Growing

Customer Base

With ~$44mm of Core Revenue in place

for FY24A and a customer pipeline of

over $1,109mm growing by the week,

comprising customers from government

entities to large domestic and multi-national enterprises

5

2

3

4 |

| CONFIDENTIAL | 17

1. INDIA’S LEADING DATA CENTER DEVELOPER

Yotta’s flagship data centers with its AI offering are NM1 and D1, in addition to its strategic G1 data center

1. Expected to increase to ~50MW with GPU deployment

2. 6 KW equivalent

3. Potential IT capacity based on available acreage and development opportunities at 36 MW / 3 acres, with 36 MW based on D2’s approved capacity and 3 acres based on each DC's

footprint

NM1 (Navi Mumbai) D1 (Delhi) G1 (Gujarat)

Design Capacity: 6,000 Racks,

30.4MW1, 1.45 PUE

NM DC Park: 30+ Acres, 320+ MW1

Design Capacity: 4,500+ Rack Capacity2,

28.8 MW, 1.4 PUE

Delhi DC Park: 20 Acres, 180+ MW3

Stats: 300 Racks, 2 MW

India’s only uptime institute Tier IV Gold

Operations Certified data center

Hosts one of the largest global hyperscalers as

a key tenant

Located In IFSC, GIFT City, Gandhinagar - the

heart of Gujarat

• Leading international technology communications company

• Indian pharmaceutical company

• International specialty packaging company

• Leading multinational financial services company

• Online payment gateway service provider

• Video game developer and publisher

• Global cloud computing company

• American retail automotive services company

Yotta’s Existing Customer Base |

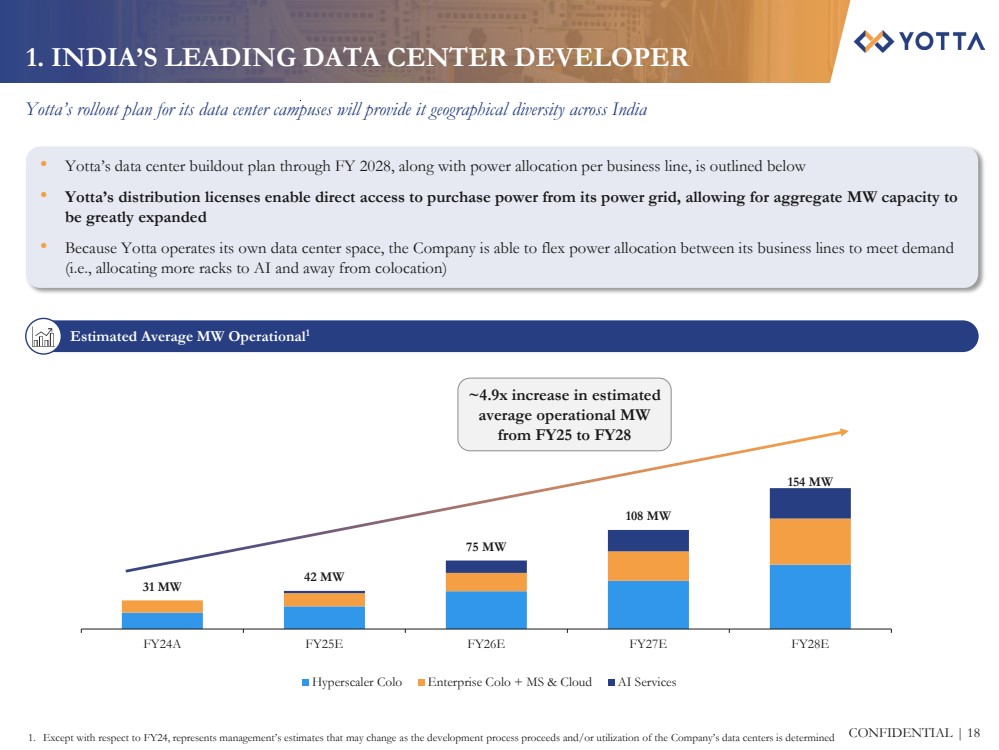

| CONFIDENTIAL | 18

31 MW

42 MW

75 MW

108 MW

154 MW

FY24A FY25E FY26E FY27E FY28E

Hyperscaler Colo Enterprise Colo + MS & Cloud AI Services

1. INDIA’S LEADING DATA CENTER DEVELOPER

Yotta’s rollout plan for its data center campuses will provide it geographical diversity across India

1. Except with respect to FY24, represents management’s estimates that may change as the development process proceeds and/or utilization of the Company’s data centers is determined

• Yotta’s data center buildout plan through FY 2028, along with power allocation per business line, is outlined below

• Yotta’s distribution licenses enable direct access to purchase power from its power grid, allowing for aggregate MW capacity to

be greatly expanded

• Because Yotta operates its own data center space, the Company is able to flex power allocation between its business lines to meet demand

(i.e., allocating more racks to AI and away from colocation)

Estimated Average MW Operational1

~4.9x increase in estimated

average operational MW

from FY25 to FY28 |

| CONFIDENTIAL | 19

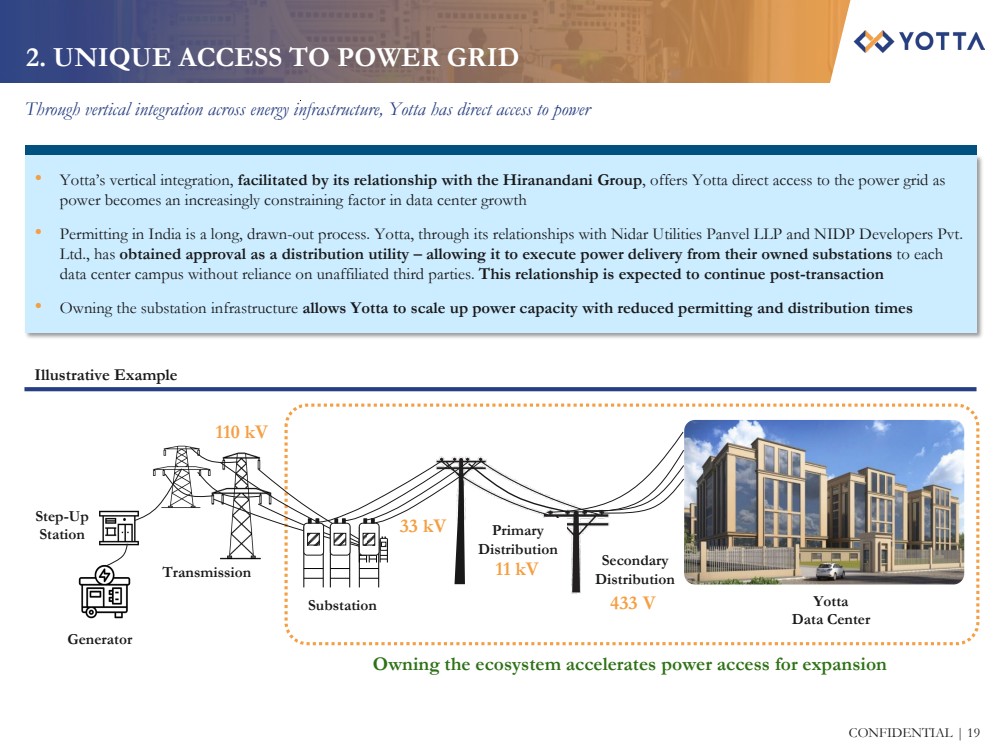

2. UNIQUE ACCESS TO POWER GRID

Through vertical integration across energy infrastructure, Yotta has direct access to power

Illustrative Example

• Yotta’s vertical integration, facilitated by its relationship with the Hiranandani Group, offers Yotta direct access to the power grid as

power becomes an increasingly constraining factor in data center growth

• Permitting in India is a long, drawn-out process. Yotta, through its relationships with Nidar Utilities Panvel LLP and NIDP Developers Pvt.

Ltd., has obtained approval as a distribution utility – allowing it to execute power delivery from their owned substations to each

data center campus without reliance on unaffiliated third parties. This relationship is expected to continue post-transaction

• Owning the substation infrastructure allows Yotta to scale up power capacity with reduced permitting and distribution times

Owning the ecosystem accelerates power access for expansion

Yotta

Data Center

33 kV

11 kV

433 V

110 kV

Secondary

Distribution

Primary

Distribution

Substation

Transmission

Generator

Step-Up

Station |

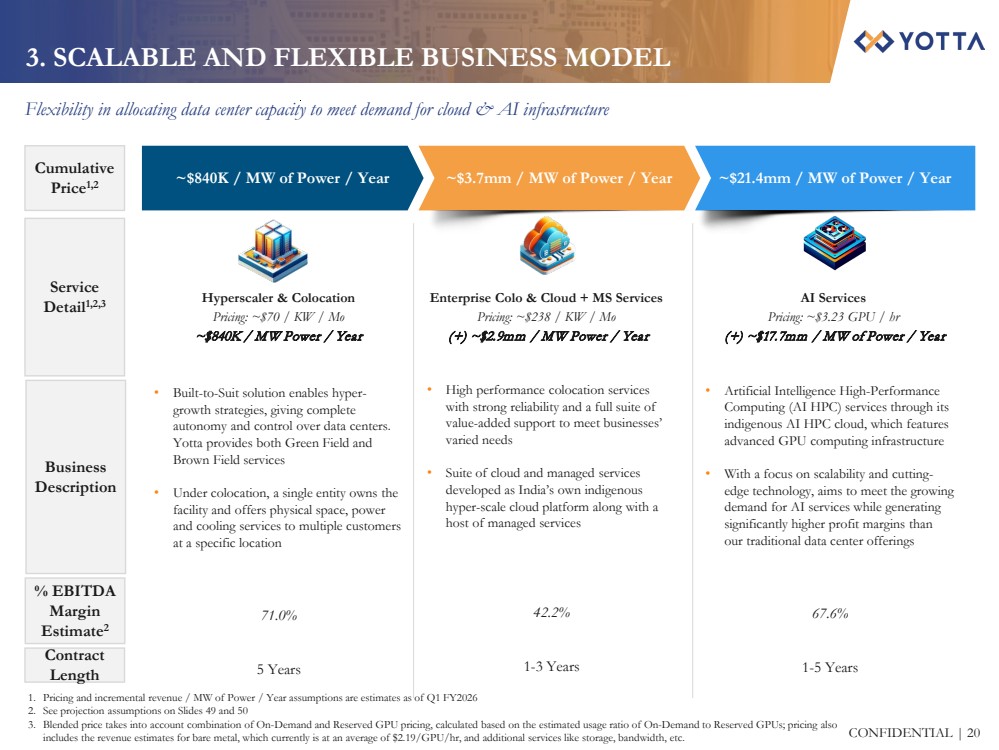

| CONFIDENTIAL | 20

3. SCALABLE AND FLEXIBLE BUSINESS MODEL

Flexibility in allocating data center capacity to meet demand for cloud & AI infrastructure

1. Pricing and incremental revenue / MW of Power / Year assumptions are estimates as of Q1 FY2026

2. See projection assumptions on Slides 49 and 50

3. Blended price takes into account combination of On-Demand and Reserved GPU pricing, calculated based on the estimated usage ratio of On-Demand to Reserved GPUs; pricing also

includes the revenue estimates for bare metal, which currently is at an average of $2.19/GPU/hr, and additional services like storage, bandwidth, etc.

~$840K / MW of Power / Year ~$3.7mm / MW of Power / Year ~$21.4mm / MW of Power / Year Cumulative

Price1,2

Service

Detail1,2,3

% EBITDA

Margin

Estimate2

Business

Description

Contract

Length

AI Services

Pricing: ~$3.23 GPU / hr

(+) ~$17.7mm / MW of Power / Year

67.6%

1-5 Years

• Artificial Intelligence High-Performance

Computing (AI HPC) services through its

indigenous AI HPC cloud, which features

advanced GPU computing infrastructure

• With a focus on scalability and cutting-edge technology, aims to meet the growing

demand for AI services while generating

significantly higher profit margins than

our traditional data center offerings

Hyperscaler & Colocation

Pricing: ~$70 / KW / Mo

~$840K / MW Power / Year

• Built-to-Suit solution enables hyper-growth strategies, giving complete

autonomy and control over data centers.

Yotta provides both Green Field and

Brown Field services

• Under colocation, a single entity owns the

facility and offers physical space, power

and cooling services to multiple customers

at a specific location

71.0%

5 Years

Enterprise Colo & Cloud + MS Services

Pricing: ~$238 / KW / Mo

(+) ~$2.9mm / MW Power / Year

• High performance colocation services

with strong reliability and a full suite of

value-added support to meet businesses’

varied needs

• Suite of cloud and managed services

developed as India’s own indigenous

hyper-scale cloud platform along with a

host of managed services

42.2%

1-3 Years |

| CONFIDENTIAL | 21

Yotta Cloud to serve as the backbone of cloud adoption by the Government of India

Yotta has contracted with two of the largest Government

of India enterprises who are responsible for hosting

government data and rolling out cloud for adoption by

various federal and state-owned institutions

Yotta has commenced managing national data centers

These data centers currently offer hosting services to a large

number of government enterprises in the country

The Indian government’s cloud strategy emphasizes the

migration of services to the cloud to enhance efficiency and

reduce costs, facilitating improved service delivery to

citizens

As a result, Yotta is deploying a new cloud setup in vacant

racks to offer various cloud services under the broad

categories of Infrastructure as a Service (IaaS), Platform as a

Service (PaaS), and Software as a Service (SaaS) to

government departments

3. GOVERNMENT SERVICES BUSINESS |

| CONFIDENTIAL | 22

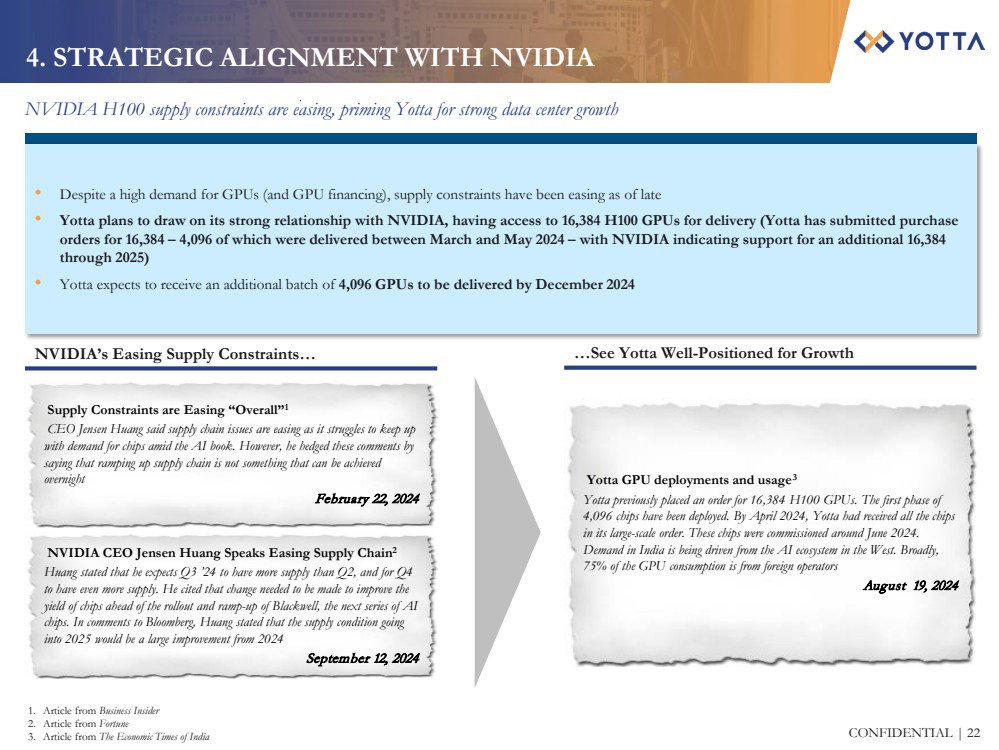

4. STRATEGIC ALIGNMENT WITH NVIDIA

NVIDIA H100 supply constraints are easing, priming Yotta for strong data center growth

NVIDIA’s Easing Supply Constraints… …See Yotta Well-Positioned for Growth

1. Article from Business Insider

2. Article from Fortune

3. Article from The Economic Times of India

• Despite a high demand for GPUs (and GPU financing), supply constraints have been easing as of late

• Yotta plans to draw on its strong relationship with NVIDIA, having access to 16,384 H100 GPUs for delivery (Yotta has submitted purchase

orders for 16,384 – 4,096 of which were delivered between March and May 2024 – with NVIDIA indicating support for an additional 16,384

through 2025)

• Yotta expects to receive an additional batch of 4,096 GPUs to be delivered by December 2024

NVIDIA CEO Jensen Huang Speaks Easing Supply Chain2

Huang stated that he expects Q3 ’24 to have more supply than Q2, and for Q4

to have even more supply. He cited that change needed to be made to improve the

yield of chips ahead of the rollout and ramp-up of Blackwell, the next series of AI

chips. In comments to Bloomberg, Huang stated that the supply condition going

into 2025 would be a large improvement from 2024

September 12, 2024

Supply Constraints are Easing “Overall”1

CEO Jensen Huang said supply chain issues are easing as it struggles to keep up

with demand for chips amid the AI book. However, he hedged these comments by

saying that ramping up supply chain is not something that can be achieved

overnight

February 22, 2024

Yotta GPU deployments and usage3

Yotta previously placed an order for 16,384 H100 GPUs. The first phase of

4,096 chips have been deployed. By April 2024, Yotta had received all the chips

in its large-scale order. These chips were commissioned around June 2024.

Demand in India is being driven from the AI ecosystem in the West. Broadly,

75% of the GPU consumption is from foreign operators

August 19, 2024 |

| CONFIDENTIAL | 23

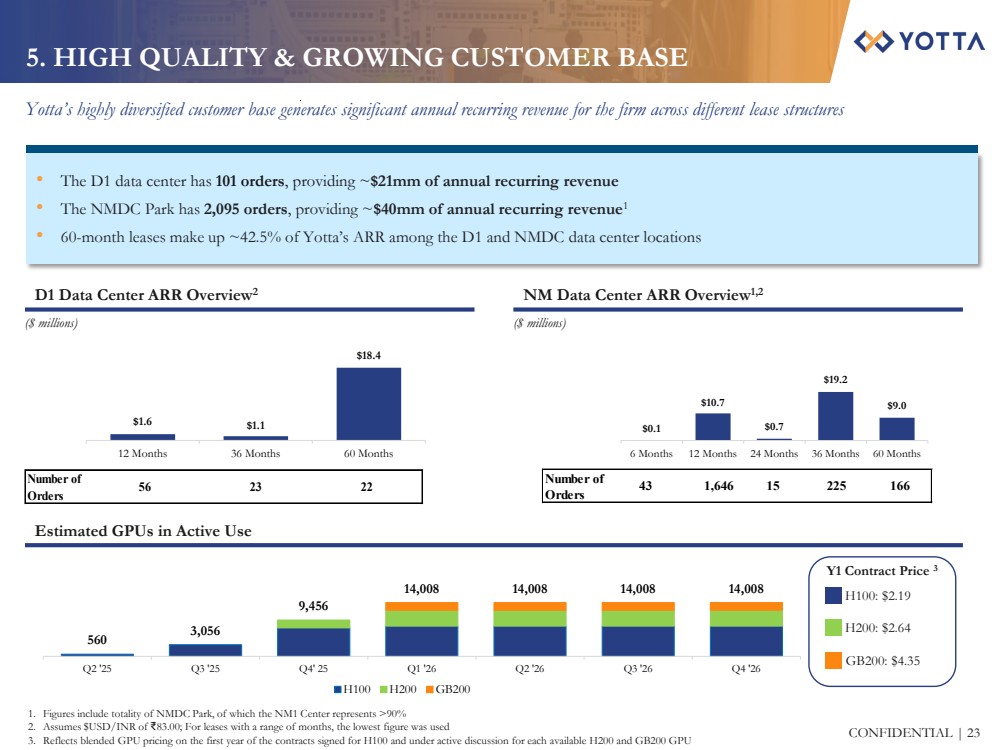

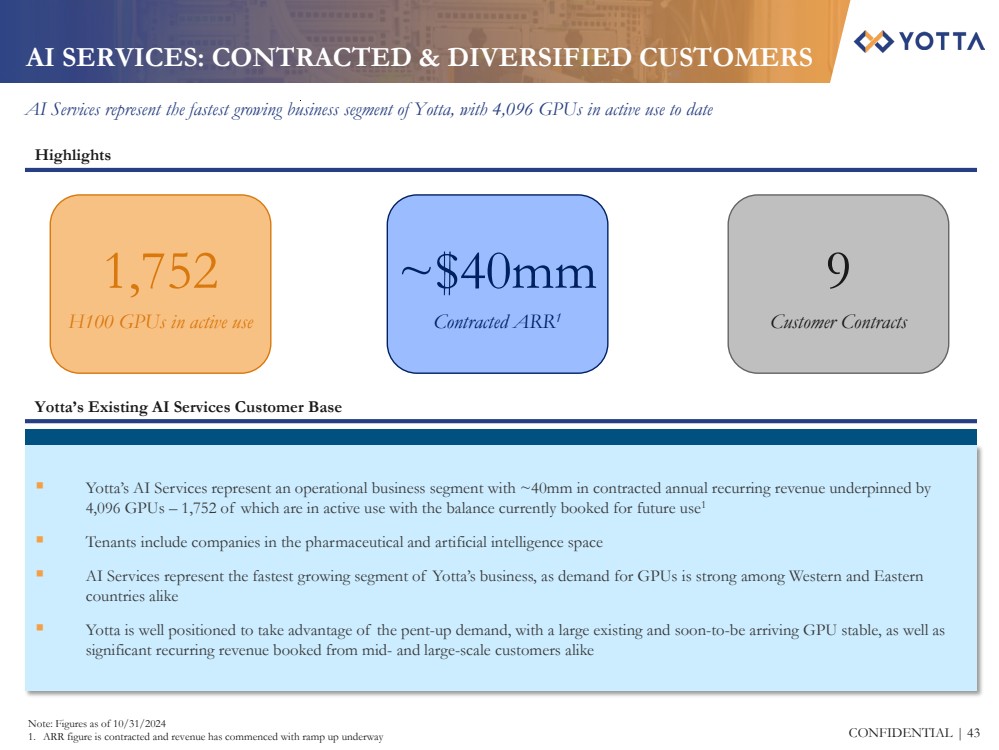

5. HIGH QUALITY & GROWING CUSTOMER BASE

Yotta’s highly diversified customer base generates significant annual recurring revenue for the firm across different lease structures

1. Figures include totality of NMDC Park, of which the NM1 Center represents >90%

2. Assumes $USD/INR of ₹83.00; For leases with a range of months, the lowest figure was used

3. Reflects blended GPU pricing on the first year of the contracts signed for H100 and under active discussion for each available H200 and GB200 GPU

1

• The D1 data center has 101 orders, providing ~$21mm of annual recurring revenue

• The NMDC Park has 2,095 orders, providing ~$40mm of annual recurring revenue1

• 60-month leases make up ~42.5% of Yotta’s ARR among the D1 and NMDC data center locations

$1.6 $1.1

$18.4

12 Months 36 Months 60 Months

D1 Data Center ARR Overview2 NM Data Center ARR Overview1,2

($ millions) ($ millions)

Y1 Contract Price 3

H100: $2.19

H200: $2.64

GB200: $4.35

Number of

Orders 56 23 22

560 3,056

9,456

14,008 14,008 14,008 14,008

Q2 '25 Q3 '25 Q4' 25 Q1 '26 Q2 '26 Q3 '26 Q4 '26

H100 H200 GB200

Number of

Orders

43 1,646 15 225 166

$0.1

$10.7

$0.7

$19.2

$9.0

6 Months 12 Months 24 Months 36 Months 60 Months

Estimated GPUs in Active Use |

| CONFIDENTIAL | 24

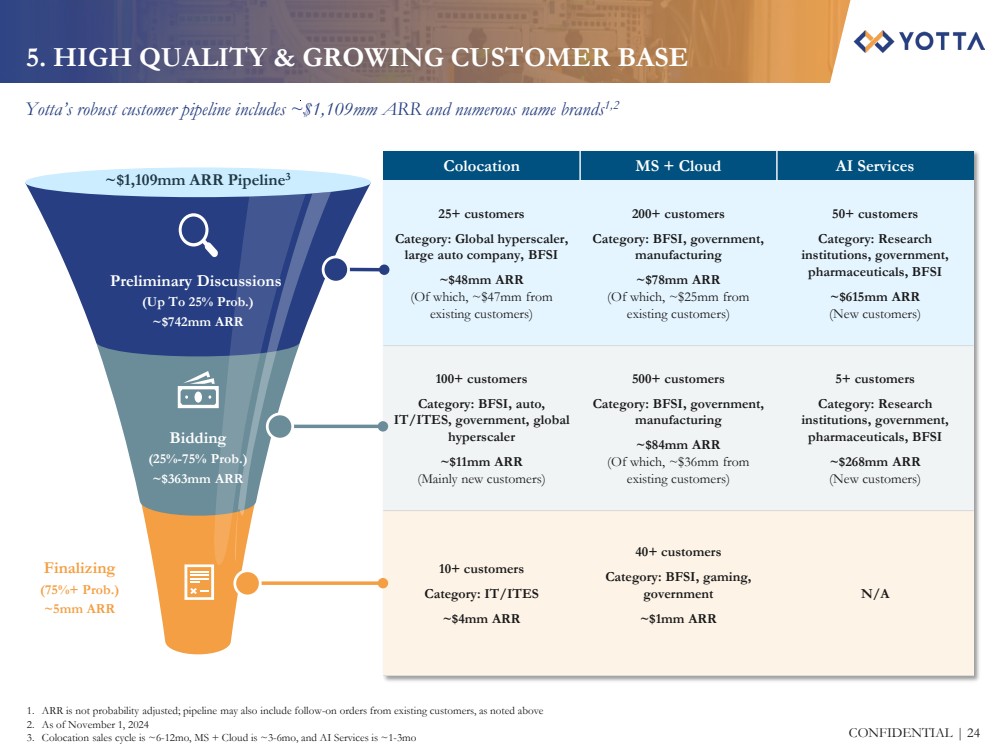

5. HIGH QUALITY & GROWING CUSTOMER BASE

Yotta’s robust customer pipeline includes ~$1,109mm ARR and numerous name brands1,2

1. ARR is not probability adjusted; pipeline may also include follow-on orders from existing customers, as noted above

2. As of November 1, 2024

3. Colocation sales cycle is ~6-12mo, MS + Cloud is ~3-6mo, and AI Services is ~1-3mo

Finalizing

(75%+ Prob.)

~5mm ARR

Bidding

(25%-75% Prob.)

~$363mm ARR

Preliminary Discussions

(Up To 25% Prob.)

~$742mm ARR

~$1,109mm ARR Pipeline3

Colocation MS + Cloud AI Services

25+ customers

Category: Global hyperscaler,

large auto company, BFSI

~$48mm ARR

(Of which, ~$47mm from

existing customers)

200+ customers

Category: BFSI, government,

manufacturing

~$78mm ARR

(Of which, ~$25mm from

existing customers)

50+ customers

Category: Research

institutions, government,

pharmaceuticals, BFSI

~$615mm ARR

(New customers)

100+ customers

Category: BFSI, auto,

IT/ITES, government, global

hyperscaler

~$11mm ARR

(Mainly new customers)

500+ customers

Category: BFSI, government,

manufacturing

~$84mm ARR

(Of which, ~$36mm from

existing customers)

5+ customers

Category: Research

institutions, government,

pharmaceuticals, BFSI

~$268mm ARR

(New customers)

10+ customers

Category: IT/ITES

~$4mm ARR

40+ customers

Category: BFSI, gaming,

government

~$1mm ARR

N/A |

| CONFIDENTIAL | 25

6. EXPERIENCED MANAGEMENT TEAM

Yotta’s strong leadership team across all business lines and functions

1. Economic Times CIO: Netmagic launches two new data centers with $144mm investment from NTT Com (July 26, 2018)

Sunil Gupta

Co-Founder & CEO

Expertise across the data center, cloud and managed IT services industries, having built and operated

20+ third party data centers in India

Executive Director and President of NTT Netmagic from 2010-2019, which operated 9 data centers and

had ~1,000 customers as of July 20181

Strong reputation among hyperscalers for meeting stringent quality demands

Anil Pawar

Chief AI Officer

Sashi Shekhar Panda

Chief Cloud Officer

Rajesh Garg

Chief Digital Officer

Nitin Jadhav

Head – Solution Engineering

Milind Kulkarni

Chief Technology Officer

Sunando Bhattacharya

Head – Sales & Business Dev.

Rohan Sheth

Head - Data Center & Colo BU

Srinivas Pranesh

Head - DC Design & Engineering

Gunisha Sanyal

Architecture & Design Advisor

Sanjay Kuntal

Head – DC Projects

Prashant Nandulamattam

Procurement Advisor

Rajesh Kadu

Head – DC Operations

Bhavesh Adhia

Chief Strategy Officer

Viren Wadhwa

Chief Marketing Officer

Pratap Patjoshi

Chief Evangelist Market Dev.

Viral Shah

Vice President – Finance

Sridhar Bapat

Head – Procurement & Asset Mgmt

Madhuri Mhmankar

Head – Human Resources

AI, Cloud & Managed Services Data Center & Colocation Services Business & Enabling Support Functions |

| III. BUSINESS OVERVIEW |

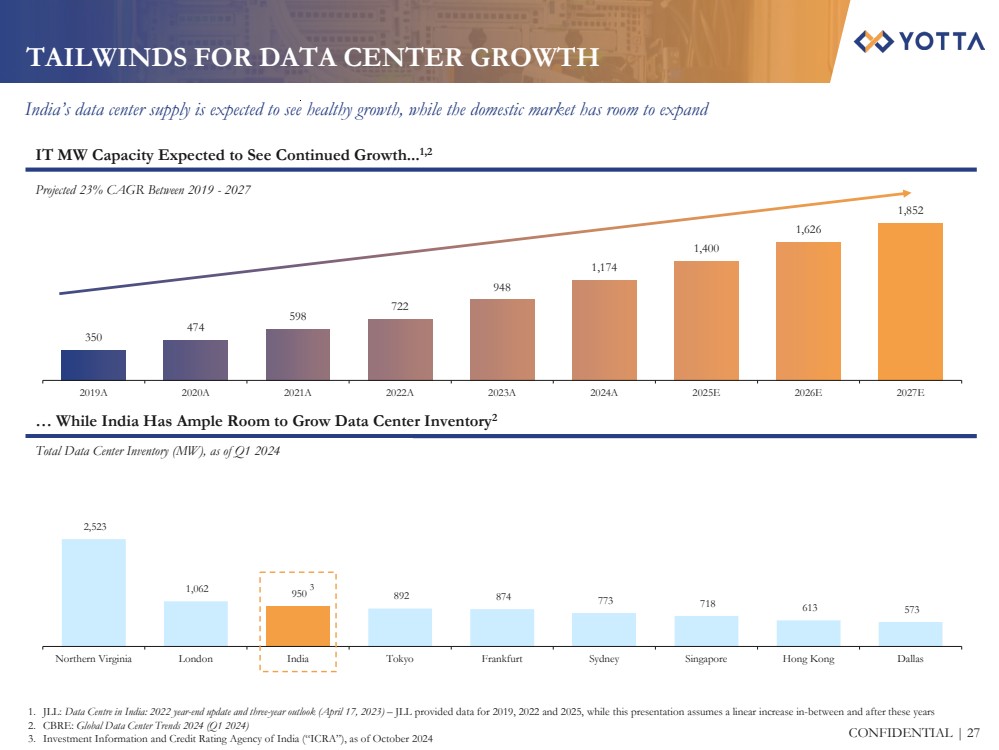

| CONFIDENTIAL | 27

2,523

1,062 950 892 874 773 718 613 573

0

500

1000

1500

2000

2500

3000

Northern Virginia London India Tokyo Frankfurt Sydney Singapore Hong Kong Dallas

… While India Has Ample Room to Grow Data Center Inventory2

TAILWINDS FOR DATA CENTER GROWTH

India’s data center supply is expected to see healthy growth, while the domestic market has room to expand

IT MW Capacity Expected to See Continued Growth...1,2

Projected 23% CAGR Between 2019 - 2027

3

1. JLL: Data Centre in India: 2022 year-end update and three-year outlook (April 17, 2023) – JLL provided data for 2019, 2022 and 2025, while this presentation assumes a linear increase in-between and after these years

2. CBRE: Global Data Center Trends 2024 (Q1 2024)

3. Investment Information and Credit Rating Agency of India (“ICRA”), as of October 2024

Total Data Center Inventory (MW), as of Q1 2024

350

474

598

722

948

1,174

1,400

1,626

1,852

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2019A 2020A 2021A 2022A 2023A 2024A 2025E 2026E 2027E |

| CONFIDENTIAL | 28

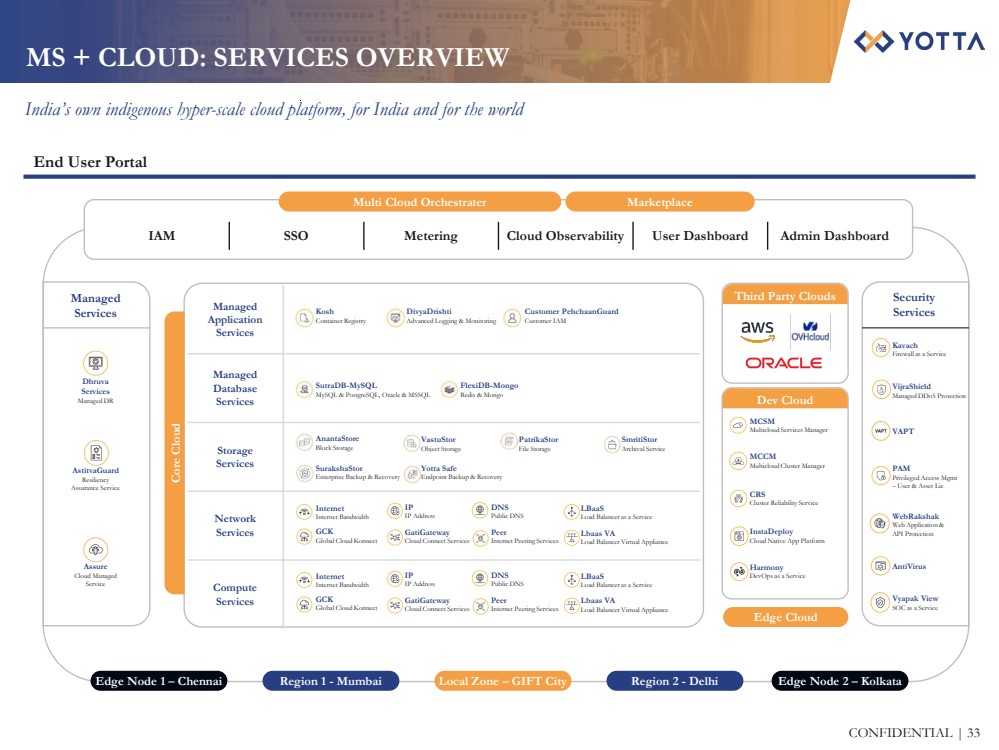

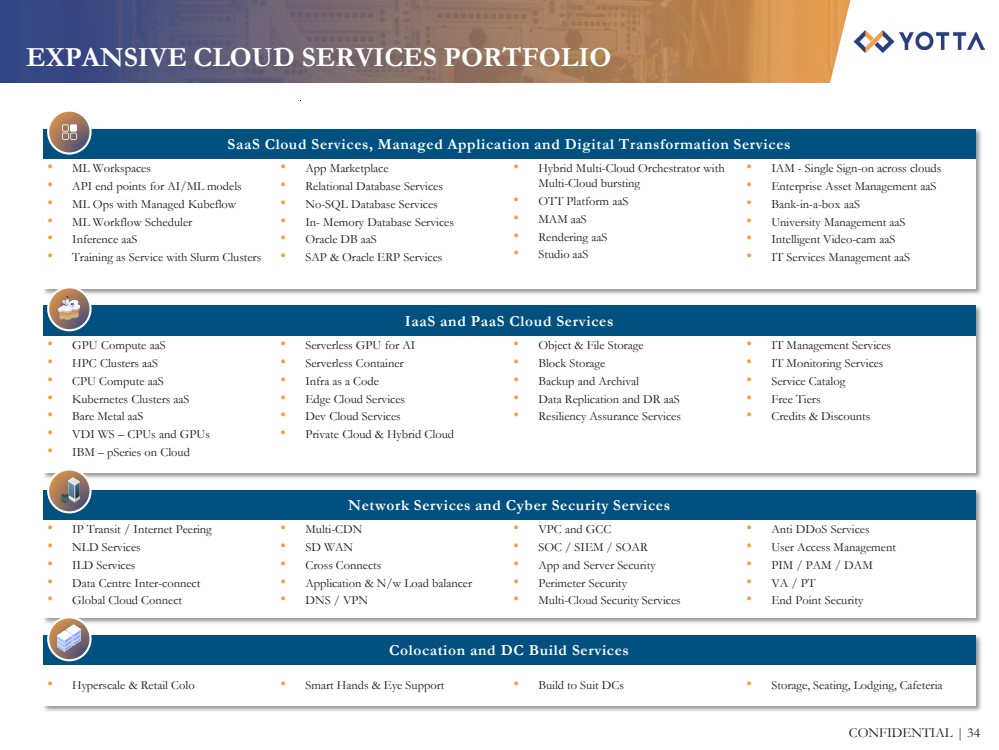

INTEGRATED DIGITAL TRANSFORMATION SERVICES

Serving advanced IT infrastructure and solutions on an “as-a-Service” (aaS) model to customers

worldwide, including enterprises, governments, start-ups & SMEs and hyperscalers

Powered by Yotta’s large scale data center parks and cloud regions, engineered, built and

fully managed and operated by Yotta

Managed Services +

Cloud

Managed application services

Managed database services

Endpoint & data security

AI Services

AI training & data analytics

AI inference

HPC / AI

Rendering & Virtual desktops

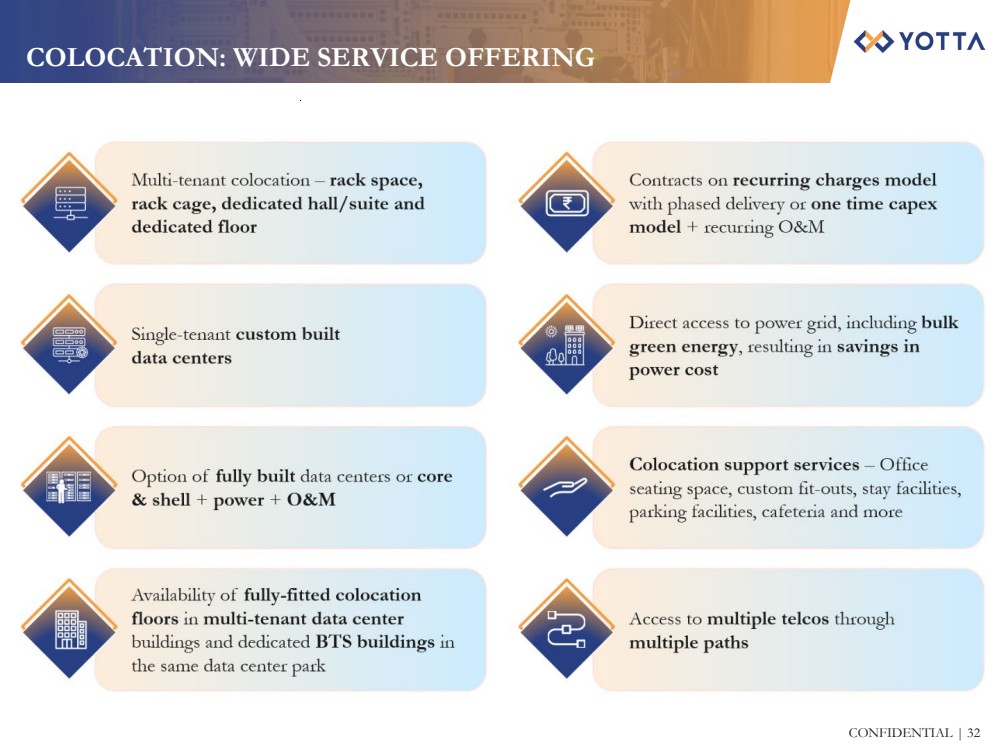

Colocation

Multi-tenant colocation

Single-tenant custom-built data centers

Contracts on recurring charges model

Colocation support services |

| CONFIDENTIAL | 29

KEY VALUE PROPOSITIONS NTT SIFY CTRLS STT PRINCETON

DIGITAL

ADANI

CONNEX

ANNOUNCEMENT OF ENTRY INTO INDIA 2019 1998 1998 2006 1995 2020 2019

GPU ACCESS AND AI SERVICES EXPERTISE ✓ Х Х Х Х Х Х

EXISTING PAN-INDIAN LAND BANK ✓ Х Х Х Х Х ✓

EXPERIENCE IN NEW LAND ACQUISITION ✓ Х Х Х Х Х ✓

POWER AND FIBER EXPERTISE ✓ Х Х Х Х Х ✓

CORE & SHELL CONSTRUCTION EXPERTISE ✓ Х Х Х Х Х Х

EXISTING RELATIONS & EXPERIENCE WITH LOCAL ✓ ✓ ✓ ✓ Х Х Х

CONTRACTORS & VENDORS

DATACENTER MEP DESIGN EXPERTISE IN-HOUSE OUTSOURCED OUTSOURCED OUTSOURCED OUTSOURCED OUTSOURCED OUTSOURCED

MTSAS WITH MAJOR HYPERSCALERS AND IT ✓ ✓ ✓ ✓ ✓ ✓ ✓ COMPANIES

DATACENTER OPERATIONS & SECURITY EXPERTISE ✓ ✓ ✓ ✓ ✓ ✓ ✓

CLOUD & MANAGED SERVICES ✓ ✓ ✓ ✓ Х Х Х

POWER DISTRIBUTION LICENSE ✓ Х Х Х Х Х ✓

COMPETITIVE EDGE IN THE INDIAN MARKET

Yotta is building the premier Tier III and IV data centers with AI compute capacity in India |

| III-I DATA CENTERS |

| CONFIDENTIAL | 31

Dense Network Connectivity

Excellent connectivity options with multiple uplink IP transits, multiple peering to internet

exchanges, direct connects to cloud providers, multiple diverse captive fiber paths and

availability of all applicable telecom licenses (IP1, ISP, NLD, VNO-ILD) to allow facilities

to connect anywhere worldwide

Near-100% Uptime

Concurrently maintainable and fault-tolerant, Tier III (99.982% uptime) & Tier IV

(99.995% uptime) data centers delivering industry-leading uptime for business operations

Security

Multiple layers of physical & cyber security to safeguard infrastructure

Scalability

Offering scalability within the same site to power businesses’ increasingly digital needs

Transparency & Control

Complete visibility & actionable insights on IT equipment hosted via variety of monitoring

and management automation tools available to customers through Yotta’s integrated

customer portal, “One Yotta”

YOTTA AI DATA CENTERS: KEY OFFERINGS

Delivering top-tier physical infrastructure in certified Tier III and Tier IV data centers

Top Global Certifications

ISO 20000

ISO 27001

ISO 27017

ISO 27018

ISO 45001

ISO 22301

ISO 9001

ISO 14001

ISO 27701

MEITY

EMPANELLED

VPC & GCC

RBI

Certification

for Cyber

Security |

| CONFIDENTIAL | 32