U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

SECURITIES EXCHANGE

ACT OF 1934

For the Month of October 2023

Nexa Resources S.A.

(Exact Name as Specified in its Charter)

N/A

(Translation of Registrant’s Name)

37A, Avenue J.F. Kennedy

L-1855, Luxembourg

Grand Duchy of Luxembourg

(Address of principal executive offices)

Indicate by check mark

whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Indicate by check mark

if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ____

Indicate by check mark

if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ____

Indicate by check mark

whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission

pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

If “Yes” is marked,

indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): Not applicable.

SIGNATURES

Pursuant to the requirements

of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto

duly authorized.

Date: October 30, 2023

| Nexa Resources S.A. |

| By:/s/ José Carlos del Valle |

| Name: José Carlos del Valle |

|

Title: Senior Vice President of

Finance and Group Chief Financial Officer

|

EXHIBIT INDEX

Nexa Reports Third

Quarter 2023 Net Loss of US$63 million and Adjusted EBITDA of US$82 Million

Luxembourg, October

30, 2023 – Nexa Resources S.A. (“Nexa Resources”, “Nexa”, or the “Company”)

announces today its results for the three and nine-month periods ended September 30, 2023.

CEO Message – Ignacio

Rosado

“In 3Q23, there continued to be downward

pressure on metal prices, mainly driven by the persistence of negative external factors, such as inflation in the U.S. leading to still

high interest rates and uncertainties about the performance of key sectors of the Chinese economy (e.g., property). Consequently, the

prices of our main metals remained at levels below our expectations for the period and slightly lower than the previous quarter.

Faced with this challenging metal price

environment, we remain committed to our financial discipline, which includes a portfolio of initiatives focused on cost reduction, CAPEX,

and working capital optimization. Some of these initiatives are still being implemented but have allowed us to improve some line items

in our 2023 guidance. Furthermore, they also contributed to positive cash flow generation in 3Q23.

On the operational side, as disclosed a

week ago, we have revised Aripuanã’s production range downwards for the year, given primarily to the limitations related

to the designed capacity of the flotation pumping system, which also resulted in the extension of the ramp-up phase. However, during 3Q23,

we continued the ramp-up phase in a structured and disciplined manner, maintaining recoveries and improving the concentrate quality and

grades. We are focused on ensuring safe and steady production by processing the zinc concentrate produced in our smelters while expanding

sales of lead and copper concentrates.

With respect to our mineral exploration

plan, we are moving forward with special attention to expanding the resource and mineral reserves base in our current mines. Additionally,

on the growth front, we are making progress with the advanced studies related to the Pasco Integration Project.

Looking ahead, our priorities are the completion

of the Aripuanã ramp-up phase, our capital optimization initiatives and the proactive adoption of appropriate measures to maintain

a healthy balance sheet, such as the reinforcement of our liquidity through the new 5-year sustainability-linked revolving credit facility

of US$320 million, which replaces the previous line that was due to expire in October 2024.

Lastly, we are confident in the long-term

fundamentals of our industry and our business. As always, we will continue to focus on safety, productivity, our ESG commitments, and

cost control to create value for all of our stakeholders.”

Summary of Financial

Performance

| US$ million (except per share amounts) |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| Net revenues |

649 |

627 |

703 |

1,943 |

2,254 |

| Gross profit |

67 |

62 |

85 |

228 |

555 |

| Net income (loss) |

(63) |

(103) |

(40) |

(182) |

158 |

| EBITDA (1) |

67 |

(44) |

111 |

139 |

614 |

| Basic and diluted earnings per share ("EPS") |

(0.56) |

(0.77) |

(0.31) |

(1.48) |

0.99 |

| Adjusted net income (loss) (1) |

(49) |

12 |

(30) |

(34) |

184 |

Earnings Release – 3Q23 |  |

| US$ million (except per share amounts) |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| Adjusted EBITDA (1) |

82 |

72 |

121 |

286 |

640 |

| Adjusted basic and diluted EPS (1) |

(0.43) |

0.04 |

(0.24) |

(0.40) |

1.19 |

| Cash provided by operating activities before working capital (1) (2) |

40 |

51 |

93 |

197 |

561 |

| Capex |

82 |

60 |

85 |

198 |

265 |

| Free cash flows (1) |

14 |

34 |

(87) |

(84) |

(226) |

| Total cash (3) |

422 |

421 |

538 |

422 |

538 |

| Net debt (1) |

1,242 |

1,262 |

1,115 |

1,242 |

1,115 |

| Net Debt/LTM Adj. EBITDA |

3.06x |

2.83x |

1.41x |

3.06x |

1.41x |

(1) Refer

to “Use of Non-IFRS Financial Measures” for further information. Adjusted EBITDA, adjusted net income (loss) and adjusted

EPS, exclude the items presented in the “Net income (loss) reconciliation to Adjusted EBITDA” section for further details

on page 13 of this earnings release. For details on segment definition and accounting policy, please refer to explanatory note 2 –

“Information by business segment” in the “Condensed consolidated interim financial statements (unaudited) at and for

the three and nine-month periods ended on September 30, 2023”.

(2) Working

capital had a positive impact of US$95 million in 3Q23, totaling US$74 million in 9M23. Working capital in 3Q22 had a negative impact

of US$23 million, totaling negative US$203 million in 9M22.

(3) Cash,

cash equivalents and financial investments.

Executive Summary

Operational Performance

| § | Zinc production of 87kt in 3Q23 rose by 15% compared to 3Q22, mainly

explained by the increase in treated ore volume and the beginning of production in the Aripuanã mine. Compared to 2Q23, zinc production

increased by 8%, primarily due to the higher volumes from the Cerro Lindo, Vazante and Morro Agudo mines, in addition to further production

from the Aripuanã ramp-up. |

| § | Run-of-mine mining cost in 3Q23 was US$44/t, up 1% from 3Q22. Compared

to 2Q23, run-of-mine mining cost was relatively flat. |

| § | Mining cash cost net of by-products[1]

in 3Q23 was US$0.35/lb compared with US$0.57/lb in 3Q22. This decrease was primarily

due to higher by-products contribution driven by higher lead prices and higher copper concentrate volumes. Compared to 2Q23, mining cash

cost net of by-products decreased by 6% from US$0.37/lb explained by higher zinc volumes produced, which was partially offset by lower

by-products-contribution. |

| § | The smelting segment delivered total production (zinc metal and oxide)

of 150kt, down 6% from 3Q22, mainly driven by lower volumes in Cajamarquilla and Juiz de Fora. Compared to 2Q23, production was up 1%. |

| § | In 3Q23, zinc metal and oxide sales were 154kt, down 5% from 3Q22, following

lower production volumes, in addition to lower domestic demand for oxide in the period. Compared to 2Q23, metal sales grew 3% driven by

higher production volumes and sales strategy in line with working capital improvement initiatives. |

| § | Smelting conversion cost was US$0.29/lb in 3Q23 compared with US$0.26/lb

in 3Q22 due to higher maintenance, personnel costs and energy expenses impacted by inflation in the period. Compared to 2Q23, conversion

cost was down US$0.03/lb. |

| § | Smelting cash cost1 was US$1.01/lb in 3Q23 compared with

US$1.36/lb in 3Q22 and compared with US$1.12 in 2Q23. In both periods, the decrease was mainly explained by lower zinc prices, which reduced

concentrate purchase costs. |

Aripuanã

| § | As

previously disclosed in our press release dated October 24,

2023, at the beginning of 3Q23, the plant performance was averaging above 75%

of nameplate capacity. We then observed design limitations in the capacity of

the flotation pumping system, identified during the detection of bottlenecks in March, which required resizing and upgrade along with

certain plant processing facilities and systems, as well as the clean-up and upgrading of water treatment facilities, which will also

contribute to a better resiliency during the rainy season (which is expected to run from December to March). Due to the aforementioned

limitations, in 3Q23 we reduced plant throughput and, as a result, the utilization rate was also reduced in the period and the plant performed

at an average of 56% in the quarter. Despite this reduction, our priority is to continue improving metal recovery and concentrate quality

and grades, aiming to achieve a stable operation and to minimize impacts related to the needed extension of the ramp-up phase. With this

revised plan in place, we expect to gradually return to an average of 70% capacity utilization level during 4Q23 and reaching 100% of

nameplate capacity in 1H24. |

1 Our cash cost net of

by-products credits is measured with respect to zinc sold.

| 2 |

Earnings Release – 3Q23 |  |

Financial Performance

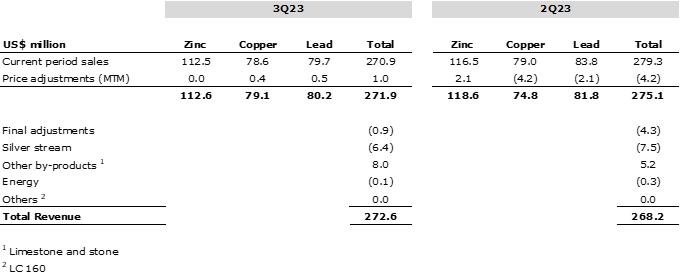

| § | Net revenues in 3Q23 were US$649 million compared with US$703 million

in 3Q22. This decrease was mainly due to lower zinc LME metal prices and smelting sales volume. Compared to 2Q23, net revenues increased

by 4%, because of higher mining production and metal sales volumes, partially offset by lower LME metal prices. In 9M23, net revenues

amounted to US$1,943 million, down by 14% compared to the same period a year ago. |

| § | In 3Q23, net loss was US$63 million, totaling US$182

million in 9M23, resulting in a basic and diluted losses per share of US$0.56 and

US$1.48, respectively. |

| § | Adjusted EBITDA[2]

in 3Q23 was US$82 million, compared with US$121 million in 3Q22 and US$72 million

in 2Q23. This performance was mainly driven by lower zinc LME metal prices (Zn down 26% vs 3Q22 and 4% vs 2Q23). Compared to 2Q23, the

lower zinc LME metal prices was offset by lower costs in Brazil and higher treatment charges (“TCs”) applied to concentrate

purchases from third-parties. In 9M23, Adjusted EBITDA amounted to US$286 million, down by 55% compared to the same period a year ago. |

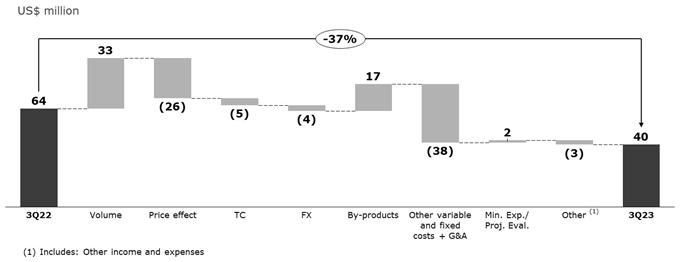

| § | Adjusted EBITDA for the mining segment in 3Q23 was US$40 million compared

with US$20 million in 2Q23. This increase was mainly driven by higher volumes in Cerro Lindo, El Porvenir and Vazante, in addition to

lower operational costs in Aripuanã, related to concentrate and stockpile costs, which were partially offset by lower LME metal

prices. Compared to 3Q22, Adjusted EBITDA decreased by 37%. |

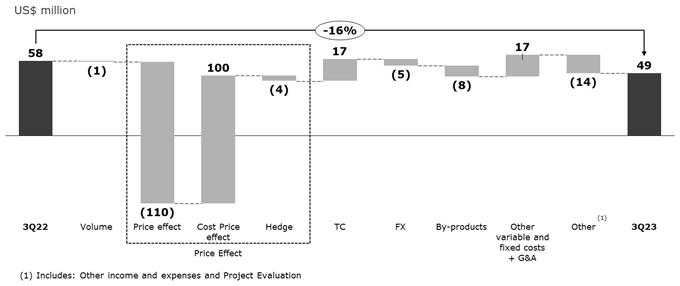

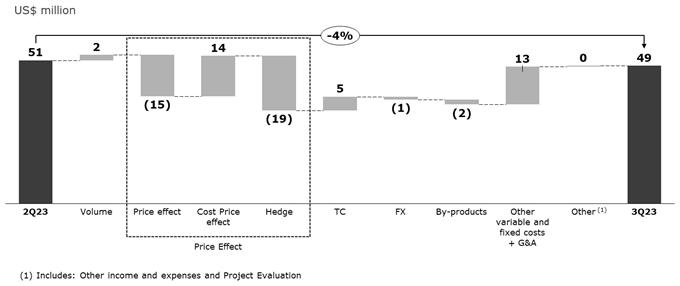

| § | Adjusted EBITDA for the smelting segment in 3Q23 was US$49 million compared

with US$51 million in 2Q23. This decrease was mainly driven by the negative hedge variation and lower by-products contribution, which

were partially offset by higher TCs and higher sales volume. Compared to 3Q22, Adjusted EBITDA decreased by 16%. |

| § | Adjusted

net loss in 3Q23, was US$49 million, totaling US$34 million in 9M23. Adjusted net loss attributable

to Nexa’s shareholders was US$57 million in 3Q23 and US$53 million in 9M23, resulting in

adjusted basic and diluted loss per share of US$0.43 and US$0.40,

respectively. |

Financial Position,

Investments and Financing

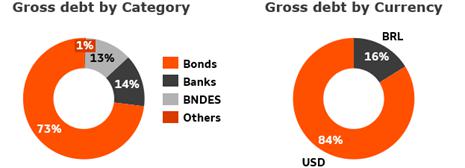

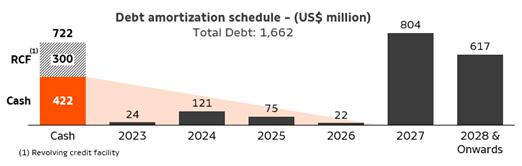

| § | Total cash[3]

at September 30, 2023, was US$422 million compared to US$421 million at June 30,

2023. Our available liquidity in 3Q23 remained at US$722 million, including our revolving credit facility of US$300 million. Nevertheless,

on October 20, 2023, we successfully closed a US$320 million sustainability-linked revolving credit facility. This new facility, with

a term of 5-year, replaced Nexa’s 2019 US$300 million revolving credit facility. |

| § | In 3Q23, our free cash flow generation was US$14 million, mainly due

to the positive impact of working capital variations of US$95 million, a result of a reduction in inventories and increase in trade and

confirming payables, which were partially offset by an increase in trade accounts receivables, and by investments

in sustaining CAPEX (including HS&E investments) in the amount of US$75 million, including US$20 million related to Aripuanã.

Refer to our “Net cash flows from operating activities excluding working capital variations and free cash flow - Reconciliation”

section for further details. |

2

Adjusted EBITDA exclude the items presented in

the “Net income (loss) reconciliation to Adjusted EBITDA” section on page 13 of this earnings release – US$15 million

in 3Q23, totaling US$148 million in 9M23.

3

Cash and cash equivalents and financial investments.

| | 3 |

Earnings Release – 3Q23 | |

| § | Net debt to Adjusted EBITDA ratio for the last twelve months (“LTM”)

increased to 3.06x compared with 2.83x at the end of June 2023 and 1.41x at the end of 3Q22. This increase was mainly explained by lower

LTM Adjusted EBITDA, impacted in part by lower metal prices, while total debt remained relatively flat. |

Environmental,

Social and Governance (“ESG”) and Corporate Highlights

| § | In July 2023, Nexa Peru committed to RED (“Red de Empresas y Discapacidad”)

to improve the employment and inclusion of professionals with disabilities, reaffirming our commitment to providing equal opportunities

and promoting a diverse and inclusive organizational culture. |

| § | In August 2023, Nexa signed a partnership agreement focused on reducing

waste disposal with a local cement supplier to test and evaluate the feasibility of technological routes for Cajamarquilla’s dried

neutral sludge to be used in the cement production chain. |

| § | In August 2023, in line with our ESG commitments, targeting net-zero

greenhouse gas emissions by 2050, we implemented the ON GRID solar system at our Cajamarquilla smelter, providing electric power from

solar energy, resulting in a reduced footprint carbon emissions and promoting clean energy production. We have early-stage initiatives

in place and plan to expand the utilization of this solar system in the available locations of deactivated tailings dams in Cajamarquilla. |

| § | In September 2023, Nexa was recognized as a leader in Social Governance

and awarded “Company of the Year - Mining Sector 2023” by Brasil Mineral (a Brazilian magazine specializing in mining). This

recognition was partly in acknowledgement of our training program in Aripuanã. The program as a whole trained 1,987 people, of

whom 53% were women. Furthermore, 40% of program participants were placed back into the job market. It is estimated that more than 15%

of the local population has benefited from this initiative, underscoring our commitment to being a collaborative force in regional development. |

| § | In September 2023, Nexa held its annual Safety Week, which included

several employees across all operations in Brazil and Peru. The purpose of this event is to share insights and experiences to enhance

our safety culture and strengthen our awareness of potential risks, promote healthy habits, and to encourage safer behaviors. |

| § | In September 2023, Ms. Jane Sadowsky, our board member, was named as

one of the most influential leaders in corporate governance by the National Association of Corporate Directors (“NACD”) as

part of their 2023 NACD Directorship 100™, an annual list of leading corporate directors and governance advocates. This accolade

underscores our commitment to governance excellence, integrity, and accountability. |

| § | Nexa recently announced organizational changes aimed at some of its

leadership roles. In September 2023, Mrs. Sofia Bresani was appointed as Head of Corporate Controlling, Tax Planning and Investment Analysis,

and in October 2023, Mrs. Neuma Eufrazio was appointed as Head of Internal Auditing, Compliance and Internal Controls. These appointments

strengthen our diversity and recognize that their professional experience will contribute positively to shaping the future of our business. |

| § | On October 20, 2023, Nexa announced the successful closing of a US$320

million sustainability-linked revolving credit facility, which replaces Nexa’s 2019 US$300 million revolving credit facility that

was set to mature in October 2024. This new revolving credit facility has a term of five years, and the amounts drawn are subject to an

initial interest rate of 1.60% plus Term SOFR. The applicable margin is subject to compliance with carbon reduction key performance indicators,

reflecting the company's unwavering commitment to reducing its carbon footprint. Such efforts are consistent with Nexa's ESG ambitions,

targeting net-zero greenhouse gas emissions by 2050, in alignment with the Paris Agreement. |

| | 4 |

Earnings Release – 3Q23 | |

| § | On July 27, 2023, Nexa informed that production at the Atacocha San

Gerardo open pit mine was resumed after protest activities by local communities ceased and access to the mine was released. The communities

were illegally blocking access to the mine and claiming rights over areas registered as the property of Nexa Atacocha. Nexa remains committed

to the social development of its host communities and will continue to pursue an active dialogue with the local community and its members. |

Growth Strategy

and Asset Portfolio

| § | We

have been focused on free cash flow generation and we continue to evaluate our capital allocation framework, which includes

priorities related to ESG and HS&E, whilst ensuring that Nexa’s capital is appropriately allocated to the highest

return assets. |

| § | The

strategic review of our assets continues with initiatives to optimize the portfolio. We continue to assess risk-return alternatives

for our Magistral copper project in Peru and for our Morro Agudo mine and Bonsucesso project in Brazil. |

| § | We

continue to advance the technical studies of the Pasco Integration project, aiming to develop a robust organic growth option for Nexa.

Technical studies cover different work, from mine planning to important projects to sustain and expand production, such as mine design

and studies for the underground interconnection, shaft upgrade and engineering assessment of the plant, as well as key routes to improve

capacity to provide a long-term solution for tailings storage facilities (“TSF”). Furthermore, we continue to advance the

required environmental studies and permits. As studies progress, the project continues to demonstrate potential to unlock important value

for Nexa through economies of scale, costs improvements and extension of asset life. |

Outlook

Production, Sales

and Cash Cost Guidance

| § | Nexa will continue to monitor risks associated with global supply chain

disruptions, which could be exacerbated, among other factors, by the ongoing Russia-Ukraine war, as well as the Israel-Hamas conflict,

unusual weather conditions and/or increased restrictions related to the COVID-19 pandemic; the global recession, and the potential impact

on the demand for our products; inflationary cost pressure; metal prices; and community protests, political situation and changes to the

regulatory framework in the countries in which we operate that could affect our production levels and our costs. Refer to “Risks

and Uncertainties” and “Cautionary Statement on Forward-Looking Statements” for further information. |

| § | Nexa reiterates its 2023 production guidance for all metals, except

for the Aripuanã mine, which guidance was updated due to the reasons aforementioned. Zinc metal sales, consolidated cash cost for

mining and smelting, capital expenditures, exploration, project evaluation and other expenses are outlined below. |

| o | Cerro Lindo: zinc and copper production is expected to slightly increase

in 4Q23 due to the ongoing mining plan, which encompasses higher-grade stopes. These areas were restricted in 2Q23 after the rainfall-related

shutdown in mid-March, impacting mine development, and resumed in 3Q23. |

| o | El Porvenir: the mine is running at full throughput capacity and based

on mine sequencing, zinc production in 4Q23 is expected to slightly decrease compared to 3Q23. However, lead and silver production are

expected to increase due to estimated higher average head grades for those metals. |

| o | Atacocha: the mine is currently running at full throughput capacity

and all metals production is estimated to increase in 4Q23 compared to 3Q23, driven by the expected production recovery after the illegal

protest activities that took place in June and July. |

| o | Vazante: ore throughput and zinc head grade in 4Q23 are expected to

slightly decrease compared to 3Q23, resulting in lower zinc production, given the mine sequencing plan for the period. Nonetheless,

production for 2023 is expected to reach the upper range of the guidance. |

| | 5 |

Earnings Release – 3Q23 | |

| o | Morro Agudo: zinc production in 4Q23 is expected to remain at a similar

level to the average of 3Q23. Lead production is expected to decrease compared to 3Q23 due to the estimated lower average head grade. |

| o | Aripuanã: the overall ramp-up is expected to improve in 4Q23

compared to 3Q23. The utilization rate at the plant is expected to increase gradually, reaching 70% in the quarter. However, we may expect

some additional impact on 2024 production. The 2023 production guidance was revised downwards as previously disclosed in our press release

on October 24, 2023. |

| § | Zinc metal sales guidance also remains unchanged at 580-605kt. |

| o | Peru: we expect production at Cajamarquilla in 4Q23 to be higher than

the average in 3Q23, mainly driven by better performance and production stability. |

| o | Brazil: in Três Marias we expect production to slightly increase

in 4Q23 compared to 3Q23, following production stability, while Juiz de Fora production is expected to remain at similar level to the

average in 3Q23. |

Mining segment – production

| Mining production |

|

9M23 |

|

2023e |

| (Metal in concentrate) |

|

Updated |

| |

|

|

|

|

|

|

|

| Zinc |

kt |

|

243 |

|

299 |

- |

334 |

| Cerro Lindo |

|

|

54 |

|

69 |

- |

79 |

| El Porvenir |

|

|

42 |

|

51 |

- |

55 |

| Atacocha |

|

|

6 |

|

9 |

- |

11 |

| Vazante |

|

|

111 |

|

131 |

- |

144 |

| Morro Agudo |

|

|

16 |

|

17 |

- |

23 |

| Aripuanã |

|

|

15 |

|

20 |

- |

23 |

| |

|

|

|

|

|

|

|

| Copper |

kt |

|

24 |

|

29 |

- |

33 |

| Cerro Lindo |

|

|

21 |

|

25 |

- |

28 |

| El Porvenir |

|

|

0.3 |

|

0.2 |

- |

0.3 |

| Aripuanã |

|

|

3.1 |

|

4.2 |

- |

5.0 |

| |

|

|

|

|

|

|

|

| Lead |

kt |

|

48 |

|

53 |

- |

65 |

| Cerro Lindo |

|

|

9 |

|

11 |

- |

13 |

| El Porvenir |

|

|

18 |

|

20 |

- |

26 |

| Atacocha |

|

|

8 |

|

10 |

- |

12 |

| Vazante |

|

|

1.2 |

|

1.1 |

- |

1.2 |

| Morro Agudo |

|

|

6.4 |

|

4.9 |

- |

6.1 |

| Aripuanã |

|

|

4.1 |

|

5.7 |

- |

6.9 |

| |

|

|

|

|

|

|

|

| Silver |

MMoz |

|

7.6 |

|

9.1 |

- |

10 |

| Cerro Lindo |

|

|

2.5 |

|

3.5 |

- |

3.8 |

| El Porvenir |

|

|

3.3 |

|

3.7 |

- |

4.5 |

| Atacocha |

|

|

1.0 |

|

1.0 |

- |

1.2 |

| Vazante |

|

|

0.4 |

|

0.3 |

- |

0.4 |

| Aripuanã |

|

|

0.3 |

|

0.4 |

- |

0.5 |

Smelting segment – sales

| | 6 |

Earnings Release – 3Q23 | |

| Smelting sales |

|

9M23 |

|

2023e |

| |

|

|

|

|

|

|

|

| Metal Sales |

kt |

|

447 |

|

580 |

- |

605 |

| Zinc metal |

|

|

421 |

|

545 |

- |

565 |

| Zinc oxide |

|

|

26 |

|

35 |

- |

40 |

| § | Nexa

reiterates its cost ROM at mining operations and conversion costs at smelting operations

despite a challenging inflationary environment, however, on October

24, 2023, we lowered our cash cost guidance for both segments. On the mining side,

primarily due to higher by-products contribution and lower TCs, while on the smelting side

lower zinc prices positively impacted the purchase of zinc concentrate. We believe that the

lowered 2023 consolidated cash cost guidance for our mining and smelting segments will be

achieved. |

| o | Mining and smelting volumes are expected to be higher in 4Q23 compared

to previous quarters and remain in the guidance ranges, as noted above. |

| o | Continued improvements in operational efficiency and cost management

are expected to offset some of the ongoing inflationary pressures. Certain initiatives focused on optimizing costs and increasing productivity

continue to be implemented in Aripuanã and the Peruvian mines, in addition to Cajamarquilla. |

| o | Commodity prices have been revised for 2023e – (Zn: US$1.19/lb,

Cu: US$3.84/lb, Pb: US$0.97/lb, Ag: US$23.3/oz, Au: US$1,927/oz), versus previous 2023e – (Zn: US$1.29/lb, Cu: US$3.54/lb, Pb: US$0.91/lb,

Ag: US$20/oz, Au: US$1,700/oz). Nexa’s C1 cash cost is sensitive to by-products prices and volumes, which may affect the results

of our final costs. |

| o | Foreign exchange rates assumptions have been updated to (BRL/USD: 4.99

and Soles/USD: 3.72), versus previous 2023e – (BRL/USD: 5.07 and Soles/USD: 3.94). |

| o | Zinc treatment charges (“TCs”) assumptions for the year

have been updated to US$274/t concentrate, versus previous 2023e US$285/t concentrate. |

Cash Costs

| Mining Operating costs |

|

Cost ROM

(US$/t) |

|

Cash Cost

(US$/lb) |

|

Cost ROM

(US$/t) |

|

Cash Cost

(US$/lb) |

| |

|

|

|

| |

9M23 |

|

9M23 |

|

2023e |

|

2023e |

| |

|

|

|

Updated |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Mining (1) |

|

44.2 |

|

0.38 |

|

43.9 |

- |

46.4 |

|

0.35 |

- |

0.38 |

| Cerro Lindo |

|

40.3 |

|

(0.12) |

|

40.1 |

- |

42.1 |

|

(0.12) |

- |

(0.10) |

| El Porvenir |

|

60.2 |

|

0.26 |

|

57.3 |

- |

60.7 |

|

0.26 |

- |

0.28 |

| Atacocha |

|

33.1 |

|

(0.72) |

|

33.1 |

- |

35.4 |

|

(0.45) |

- |

(0.38) |

| Vazante |

|

56.7 |

|

0.62 |

|

57.2 |

- |

59.0 |

|

0.59 |

- |

0.65 |

| Morro Agudo |

|

30.6 |

|

0.83 |

|

35.0 |

- |

38.2 |

|

0.80 |

- |

0.94 |

(1) C1 Weighted Cash cost net

of by-products credits is measured with respect to zinc sold per mine.

| Smelting Operating costs |

|

Conversion cost

(US$/lb) |

|

Cash Cost

(US$/lb) |

|

Conversion cost

(US$/lb) |

|

Cash Cost

(US$/lb) |

| |

|

|

|

| |

9M23 |

|

9M23 |

|

2023e |

|

2023e |

| |

|

|

|

Updated |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Smelting (2) |

|

0.31 |

|

1.13 |

|

0.29 |

- |

0.32 |

|

1.07 |

- |

1.12 |

| Cajamarquilla |

|

0.28 |

|

1.07 |

|

0.27 |

- |

0.29 |

|

1.04 |

- |

1.08 |

| Três Marias |

|

0.27 |

|

1.16 |

|

0.27 |

- |

0.30 |

|

1.08 |

- |

1.13 |

| Juiz de Fora |

|

0.50 |

|

1.29 |

|

0.45 |

- |

0.49 |

|

1.19 |

- |

1.28 |

(2) C1 Weighted Cash cost net

of by-products credits is measured with respect to zinc sold per smelter.

| | 7 |

Earnings Release – 3Q23 | |

| § | Mining C1 cash cost of US$0.38/lb in 9M23 was within our updated 2023

guidance, primarily driven by Cerro Lindo and Atacocha performances. For reference, please see the section “Business performance

– Mining segment”. Nonetheless, we expect a reduction in C1 cash in 4Q23, ending the year within the updated guidance range. |

| § | Smelting C1 cash cost of US$1.13/lb in 9M23 was slightly higher than

our updated 2023 guidance. This was mainly related to lower by-products credits in the period, driven by lower-than-expected metal prices

and production in 3Q23. Nonetheless, we expect a reduction in C1 cash in 4Q23, ending the year within the updated guidance range. |

Capital Expenditures

(“CAPEX”) Guidance

| § | Nexa invested US$82 million in 3Q23, totaling US$198

million in 9M23. Nearly all of the investment was classified

as sustaining, which includes CAPEX to sustain operations, HS&E and mine development. |

| § | At Aripuanã, sustaining and HS&E CAPEX in 3Q23 accounted

for US$20 million, totaling US$51 million in 9M23. Of this amount, US$6 million was invested in mine development in the quarter, totaling

US$16 million in 9M23. |

| § | The Brazilian real appreciation against the U.S. dollar had a negative

impact of US$2.8 million in the quarter, totaling a negative impact of US$3.7 million in 9M23. |

| § | 2023 CAPEX guidance remains unchanged. |

| CAPEX |

|

9M23 |

|

2023e |

| (US$ million) |

|

|

| Expansion projects (1) |

|

2 |

|

7 |

| |

|

|

|

|

| Non-Expansion |

|

201 |

|

303 |

| Sustaining (2) |

|

185 |

|

268 |

| HS&E |

|

11 |

|

26 |

| Others (3) |

|

5 |

|

10 |

| Reconciliation to Financial Statements (4) |

|

(5) |

|

- |

| TOTAL |

|

198 |

|

310 |

(1) Including

Vazante deepening, among other several projects to improve operational performance.

(2) Investments

in tailing dams are included in sustaining expenses.

(3) Modernization,

IT and others.

(4) The

amounts are mainly related to capitalization of interest net of advanced payments for imported materials and tax credits.

Exploration &

Project Evaluation and Other Expenses Guidance

| § | In 3Q23, we invested US$26 million in exploration and project evaluation,

totaling US$69 million in 9M23. |

| § | Our updated exploration and project evaluation guidance is now expected

to be US$100 million in 2023, a reduction of US$10 million from the previous guidance, mainly due to initiatives to optimize capital allocation.

Additionally, we reduced US$5 million of our 2023 guidance for technology and communities to continue contributing

to the social and economic development of our host communities. |

| | 8 |

Earnings Release – 3Q23 | |

| § | As part of our long-term strategy, we will maintain our efforts to replace

and increase mineral reserves and resources. We expect to continue advancing with our exploration activities, primarily focusing on identifying

new ore bodies and upgrading resources classification through infill drilling campaigns. |

| Other Operating Expenses |

|

9M23 |

|

2023e |

| (US$ million) |

|

|

Updated |

| Exploration |

|

44 |

|

49 |

| Mineral Exploration |

|

28 |

|

30 |

| Mineral rights |

|

4 |

|

5 |

| Sustaining (mine development) |

|

11 |

|

14 |

| |

|

|

|

|

| Project Evaluation |

|

25 |

|

50 |

| Três Marias Project |

|

10 |

|

15 |

| |

|

|

|

|

| Exploration & Project Evaluation (1) |

|

69 |

|

100 |

| |

|

|

|

|

| Other |

|

12 |

|

20 |

| Technology |

|

4.3 |

|

6 |

| Communities |

|

7.4 |

|

14 |

(1) Exploration

and Project Evaluation expenses in 3Q23, were adjusted downwards by US$1.6 million due to a reclassification from the previous quarter,

not affecting the cumulative amount for 9M23.

Note: Exploration and project evaluation expenses

consider several stages of development, from mineral potential definition, R&D, and subsequent scoping and pre-feasibility studies

(FEL1 and FEL2).

| | 9 |

Earnings Release – 3Q23 | |

Earnings Release

– 3Q23

This Earnings Release should be read

in conjunction with the Condensed consolidated interim financial statements (unaudited) at and for the three and nine-month periods ended

on September 30, 2023. This document contains forward-looking statements.

Table of contents

| Consolidated performance |

11 |

| Business performance – Mining |

16 |

| Business performance – Smelting |

28 |

| Liquidity and Indebtedness |

35 |

| Cash flows |

36 |

| Others |

37 |

| Market scenario |

38 |

| Risks and Uncertainties |

40 |

| Use of Non-IFRS Financial Measures |

41 |

| Cautionary Statement on Forward-Looking Statements |

43 |

| Appendix |

45 |

UPCOMING EVENT

Earnings Conference

Call

Date: Tuesday, October 31, 2023

– 9:00am (EST)

Dial In

US: +1-833-816-1265

Canada: +1-647-484-8814

Brazil: +55 11 3181-8565

International: +1-412-317-5635

Conference ID: Nexa Resources

Live audio webcast with slide presentation

will be available on:

https://ir.nexaresources.com

| | 10 |

Earnings Release – 3Q23 | |

Consolidated performance

Selected financial

information

US$ million

(excepted indicated otherwise) |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| |

|

|

|

|

|

| Net Revenues |

649 |

627 |

703 |

1,943 |

2,254 |

| Mining |

273 |

268 |

241 |

809 |

933 |

| Smelting |

484 |

465 |

616 |

1,493 |

1,861 |

| Intersegment results | Adjustments |

(107) |

(107) |

(154) |

(358) |

(539) |

| |

|

|

|

|

|

| Cost of Sales |

(583) |

(565) |

(618) |

(1,715) |

(1,699) |

| Mining |

(246) |

(256) |

(193) |

(745) |

(602) |

| Current Operations |

(203) |

(195) |

(193) |

(601) |

(602) |

| Aripuanã |

(43) |

(60) |

0 |

(144) |

0 |

| Smelting |

(439) |

(415) |

(579) |

(1,323) |

(1,648) |

| Intersegment results | Adjustments |

102 |

106 |

154 |

352 |

551 |

| |

|

|

|

|

|

| Selling, general and administrative |

(33) |

(33) |

(32) |

(94) |

(105) |

| Mining |

(16) |

(14) |

(17) |

(45) |

(49) |

| Smelting |

(15) |

(16) |

(14) |

(46) |

(44) |

| Intersegment results | Adjustments |

(2) |

(3) |

0 |

(3) |

(11) |

| |

|

|

|

|

|

| Depreciation and amortization |

72 |

72 |

73 |

216 |

213 |

| Mining |

51 |

53 |

49 |

157 |

145 |

| Smelting |

20 |

19 |

20 |

58 |

61 |

| Intersegment results | Adjustments |

0 |

0 |

4 |

1 |

7 |

| |

|

|

|

|

|

| Adjusted EBITDA (1) |

82 |

72 |

121 |

286 |

640 |

| Mining |

40 |

20 |

64 |

102 |

362 |

| Smelting |

49 |

51 |

58 |

189 |

281 |

| Intersegment results | Adjustments |

(7) |

1 |

(1) |

(4) |

(2) |

| Adj. EBITDA margin (%) |

12.6% |

11.4% |

17.2% |

14.7% |

28.4% |

| |

|

|

|

|

|

| Net income (loss) |

(63) |

(103) |

(40) |

(182) |

158 |

| Attributable to Nexa's shareholders |

(74) |

(102) |

(41) |

(196) |

131 |

| Attributable to non-controlling interests |

10 |

(0) |

1 |

14 |

27 |

| |

|

|

|

|

|

| Basic and diluted EPS |

(0.56) |

(0.77) |

(0.31) |

(1.48) |

0.99 |

| |

|

|

|

|

|

| Adjusted net income (loss) (1) |

(49) |

12 |

(30) |

(34) |

184 |

| Attributable to Nexa's shareholders |

(57) |

6 |

(32) |

(53) |

157 |

| Attributable to non-controlling interests |

8 |

7 |

2 |

19 |

26 |

| |

|

|

|

|

|

| Adjusted basic and diluted EPS (1) |

(0.43) |

0.04 |

(0.24) |

(0.40) |

1.19 |

(1) Refer to “Use of Non-IFRS Financial

Measures” for further information. Adjusted EBITDA, adjusted net income (loss) and adjusted EPS, exclude the items presented in

the “Net income (loss) reconciliation to Adjusted EBITDA” section for further details on page 13 of this earnings release.

For details on segment definition and accounting policy, please refer to explanatory note 2 – “Information by business segment”

in the “Condensed consolidated interim financial statements (unaudited) at and for the three and nine-month periods ended on September

30, 2023”.

| | 11 |

Earnings Release – 3Q23 | |

Net revenues

In 3Q23, net revenues were US$649 million,

8% lower year-over-year, primarily due to lower zinc metal prices and smelting sales volume. The LME average price for zinc was down by

26%, while copper and lead rose by 8% and 10%, respectively, compared to the same period in 2022 – for more information on metal

prices, refer to the “Market Scenario” section.

Compared to 2Q23, net revenues increased

by 4%, mainly due to higher mining production and metal sales volumes, which was partially offset by lower zinc and copper metal prices.

In 9M23, net revenues amounted to US$1,943

million, down by 14% compared to the same period a year ago, as a result of lower LME metal prices across all base metals, which was partially

offset by higher zinc mining production.

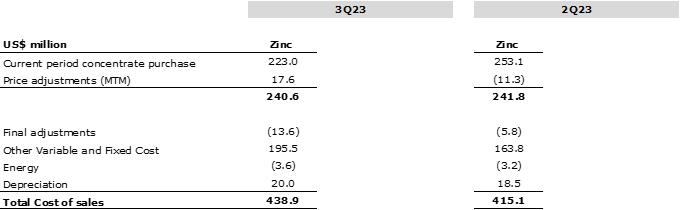

Cost of Sales

In 3Q23, cost of sales amounted to US$583

million, down 6% year-over-year, mainly due to lower zinc prices, positively impacting our smelting raw material purchase and lower smelting

sales, which were partially offset by higher mining sales volumes driving overall higher cost of sales for the mining segment. Compared

to 2Q23, cost of sales increased by 3%, explained by higher mining sales volumes and smelting sales, which was partially offset by lower

zinc prices, positively impacting the purchase of the zinc concentrate in our smelting segment.

In 9M23, cost of sales amounted to US$1,715

million, up 1% compared to the same period a year ago, mainly due to higher mining production volumes and lower zinc prices, positively

impacting the purchase of the zinc concentrate in our smelting segment.

Mineral exploration

and project evaluation

In 3Q23, mineral exploration and project

evaluation investments were US$26 million compared to US$24 million in 3Q22, mainly driven by higher project evaluation expenses. In 9M23,

mineral exploration and project evaluation investment amounted to US$69 million.

For additional information about our exploration

results in the third quarter of 2023, please refer to our 3Q23 Exploration Report published on October 23, 2023.

SG&A

In 3Q23, SG&A expenses of US$33 million

were relatively flat compared with US$33 million in 2Q23, mainly driven by higher employee benefit expenses, partially offset by lower

third-party services in support areas, and were higher by 5% when compared to 3Q22. In 9M23, SG&A

expenses amounted to US$94 million, down by 10% compared to the same period a year ago, partially a result of our organizational redesign

that occurred in 2022 and lower third-party services in support areas.

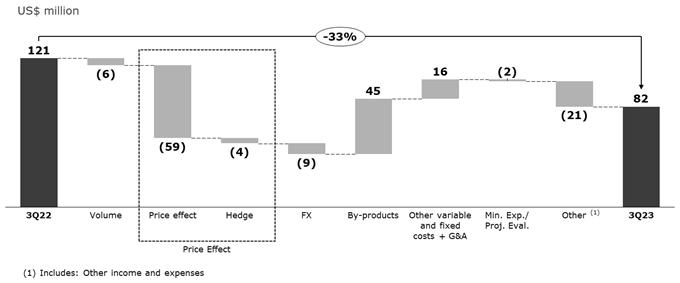

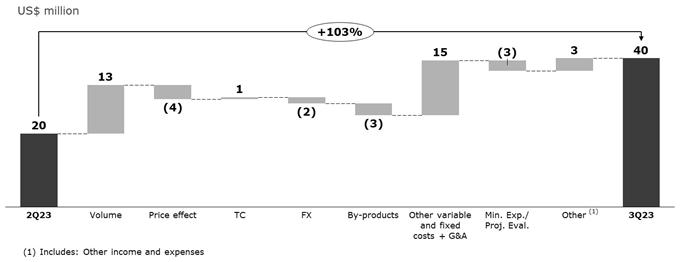

Adjusted EBITDA

In 3Q23, Adjusted EBITDA was US$82 million

compared with US$121 million in 3Q22. The main factors that contributed to this decrease were (i) the negative net price effect of US$59

million, primarily related to lower LME metal prices, which was partially offset by the positive effect of variation in MTM (“mark-to-market”);

(ii) negative impact of FX variation of US$9 million; (iii) the negative accounting effect regarding Enercan’s deconsolidation of

US$8 million; (iv) lower zinc metal sales volume of US$6 million; and (v) the negative hedge variation of US$4 million, which were partially

offset by (vi) higher by-products contribution of US$45 million, primarily related to higher copper and lead prices and volumes, partially

offset by lower payable value of sulphuric acid; and (vii) the positive net impact of US$16 million in costs, mainly due to higher zinc

concentrate volumes from our own mines, higher TCs applied to concentrate purchases from third-parties and a better smelting raw material

mix consumption, partially offset by Aripuanã’s sales expenses in the quarter compared to 3Q22.

| | 12 |

Earnings Release – 3Q23 | |

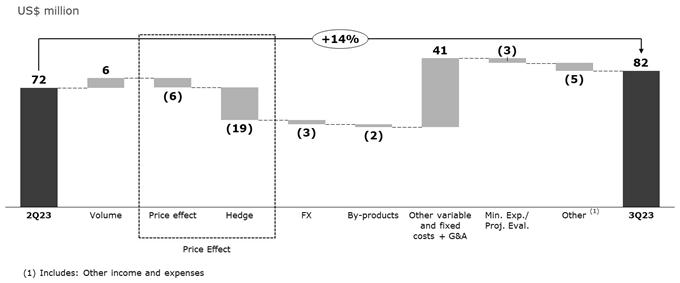

Compared to 2Q23, Adjusted EBITDA increased

by 14%. This increase was mainly driven by (i) the positive net impact of US$41 million, mainly due to the effect of lower ore stockpile

in Aripuanã, lower costs on raw material consumption in Brazil, lower freight and sales expenses in Cajamarquilla, and higher TCs

applied to concentrate purchases from third-parties, which was partially offset by (ii) the negative hedge effect of US$19 million; (iii)

the negative net price effect of US$6 million due to lower LME metal prices; (iv) the negative FX impact of US$3 million; and (v) lower

by-products contribution of US$2 million driven by lower prices.

During 9M23, Adjusted EBITDA was US$286

million compared with US$640 million in the same period a year ago, primarily driven by lower LME metal prices with a negative impact

of US$307 million and higher operational costs mainly in Aripuanã, related to concentrate and stockpile costs.

Net income (loss) reconciliation

to Adjusted EBITDA

| US$ million |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| Net Income (loss) |

(63.4) |

(102.8) |

(39.9) |

(181.6) |

157.8 |

| Depreciation, amortization and depletion |

72.1 |

71.7 |

72.8 |

215.5 |

213.0 |

| Share in the results of associates |

(6.3) |

(5.7) |

0.0 |

(17.4) |

0.0 |

| Net financial results |

64.4 |

26.5 |

52.3 |

130.1 |

115.9 |

| Taxes on income |

0.4 |

(33.5) |

26.2 |

(8.1) |

127.7 |

| | 13 |

Earnings Release – 3Q23 | |

| US$ million |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| EBITDA |

67.1 |

(43.7) |

111.4 |

138.6 |

614.4 |

| Fair value of offtake agreement (2) |

(1.0) |

(13.4) |

(7.8) |

(1.0) |

(16.6) |

| Impairment loss of long-lived assets |

1.9 |

57.2 |

(0.3) |

59.1 |

(0.3) |

| Pre-operating and ramp-up expenses during the commissioning and ramp-up of greenfield projects (Aripuanã) (3) |

3.5 |

(3.8) |

12.1 |

5.4 |

40.7 |

| Loss on sale of property, plant and equipment |

(0.1) |

1.0 |

0.6 |

1.2 |

0.5 |

| Remeasurement in estimates of asset retirement obligations |

(2.6) |

1.4 |

(5.5) |

(2.8) |

(9.2) |

| Remeasurement adjustment of streaming agreement |

2.3 |

0.0 |

10.6 |

2.3 |

10.6 |

| Energy forward contracts – MTM |

(2.3) |

9.7 |

0.0 |

7.4 |

0.0 |

| Provisions – Value added tax ("VAT") discussions |

12.8 |

63.2 |

0.0 |

76.0 |

0.0 |

| Adjusted EBITDA (1) |

81.7 |

71.5 |

121.1 |

286.2 |

640.2 |

(1) Adjusted EBITDA exclude the items presented

above in the “Net income (loss) reconciliation to Adjusted EBITDA”. For details on segment definition and accounting policy,

please refer to explanatory note 2 – “Information by business segment” in the “Condensed consolidated interim

financial statements (unaudited) at and for the three and nine-month periods ended on September 30, 2023”.

(2) Refers to the fair value of the financial

instrument related to the “Offtake agreement” described on page 37 of this earnings release.

(3) Expenses related to pre-operating and

ramp-up expenses incurred during the commissioning and ramp-up phases of greenfield projects which have not achieved their nameplate capacity

are not indicative of the Company’s normal operating activities. Once Aripuanã operation is stabilized and operational at

its nameplate capacity, such effects will no longer be excluded.

Net financial

results

The net

financial results in 3Q23 were an expense of US$65 million compared to US$27 million expense in 2Q23, mainly driven by higher FX rate

losses, higher financial income (interest on financial investments and cash equivalents) and lower financial expenses, including interest

paid in the forfaiting and confirming payables program, accrued interest related to our two outstanding corporate bonds and other financial

expenses[4].

The foreign

exchange variation had a negative impact of US$27 million versus a positive impact of US$27 million in 2Q23, mainly explained by the 4%

depreciation of the Brazilian real against the U.S. dollar[5]

in 3Q23 versus the previous quarter.

Excluding the effect of the foreign exchange

variation, the net financial results in 3Q23 were an expense of US$37 million compared to an expense of US$53 million in the previous

quarter.

| US$ thousand |

3Q23 |

2Q23 |

3Q22 |

| |

|

|

|

| Financial income |

8,359 |

6,700 |

6,701 |

| |

|

|

|

| Financial expenses |

(45,316) |

(59,363) |

(41,571) |

| |

|

|

|

| Other financial items, net |

(27,400) |

26,149 |

(17,423) |

| Foreign exchange gain (loss) |

(26,882) |

26,812 |

(16,076) |

| |

|

|

|

4

For details on other financial expenses, please

refer to the Legal Matters section of this Earnings Release and explanatory note 1 (b) “VAT discussions – TAX Voluntary Disclosure

and Contingent Liabilities” in the “Condensed consolidated interim financial statements ended on September 30, 2023”.

5

In 3Q23, the Brazilian real / U.S. dollar (end of period) exchange rate was R$5.007/US$1.00 compared to R$4.819/US$1.00 in 2Q23.

| | 14 |

Earnings Release – 3Q23 | |

| US$ thousand |

3Q23 |

2Q23 |

3Q22 |

| Net financial result |

(64,357) |

(26,514) |

(52,293) |

| Net financial result excluding FX |

(37,475) |

(53,326) |

(36,217) |

Net income (loss)

Net loss

was US$63 million in 3Q23 compared to net loss of US$40 million in 3Q22 and net loss of US$103 million in 2Q23, mainly driven by the increase

in operating income when compared to 2Q23, the recognition of an impairment loss[6]

and contingent liabilities and provisions in 2Q23. In 9M23, net loss was US$182 million compared to net

income of US$158 million in the same period a year ago.

Excluding the miscellaneous adjustments

presented below and detailed above in the Net income (loss) reconciliation to Adjusted EBITDA section, adjusted net loss was US$49 million

in the quarter. In 9M23, adjusted net loss totaled US$34 million.

Adjusted net loss attributable to Nexa’s

shareholders was US$57 million in 3Q23 and US$53 million in 9M23, resulting in adjusted loss per share of US$0.43 and

US$0.40, respectively.

US$ million

(excepted indicated otherwise) |

3Q23 |

2Q23 |

3Q22 |

9M23 |

9M22 |

| Net Income (loss) |

(63.4) |

(102.8) |

(39.9) |

(181.6) |

157.8 |

| Attributable to Nexa's shareholders |

(73.7) |

(102.5) |

(41.2) |

(196.0) |

130.8 |

| Attributable to non-controlling interests |

10.4 |

(0.3) |

1.4 |

14.4 |

27.0 |

| Basic and diluted earnings (loss) per share |

(0.56) |

(0.77) |

(0.31) |

(1.48) |

0.99 |

| |

|

|

|

|

|

| Miscellaneous adjustments |

14.6 |

115.2 |

9.7 |

147.6 |

25.8 |

| Attributable to Nexa's shareholders |

16.6 |

108.2 |

9.3 |

143.2 |

26.5 |

| Attributable to non-controlling interests |

(2.0) |

7.0 |

0.4 |

4.4 |

(0.7) |

| Basic and diluted miscellaneous adjustments per share |

0.13 |

0.82 |

0.07 |

1.08 |

0.20 |

| |

|

|

|

|

|

| Adjusted net income (loss) |

(48.8) |

12.5 |

(30.2) |

(33.9) |

183.6 |

| Attributable to Nexa's shareholders |

(57.2) |

5.7 |

(31.9) |

(52.8) |

157.3 |

| Attributable to non-controlling interests |

8.4 |

6.7 |

1.7 |

18.8 |

26.3 |

| Weighted average number of outstanding shares - in thousand |

132,439 |

132,439 |

132,439 |

132,439 |

132,439 |

| Adjusted basic and diluted EPS |

(0.43) |

0.04 |

(0.24) |

(0.40) |

1.19 |

(1) Miscellaneous adjustments include: (i)

Fair value of offtake agreement; (ii) Impairment loss of long-lived assets; (iii) Aripuanã pre-operating expenses and ramp-up impacts;

(iv) Impairment of other assets; (v) Loss on sale of property, plant and equipment; (vi) Remeasurement in estimates of asset retirement

obligations; (vii) Remeasurement adjustment of streaming agreement; and (viii) Other adjustments.

6

Note: For details on Impairment Loss and Contingent Liabilities and Provisions, please refer to the “Condensed consolidated interim

financial statements ended on September 30, 2023”.

| | 15 |

Earnings Release – 3Q23 | |

Business Performance

Mining segment

| Consolidated |

|

3Q23 |

2Q23 |

3Q22 |

3Q23 vs. 3Q22 |

9M23 |

9M22 |

9M23 vs. 9M22 |

| Ore Mined |

kt |

3,284 |

3,214 |

3,029 |

8.4% |

9,437 |

8,900 |

6.0% |

| Treated Ore |

kt |

3,470 |

3,546 |

3,135 |

10.7% |

10,147 |

9,062 |

12.0% |

| |

|

|

|

|

|

|

|

|

| Grade |

|

|

|

|

|

|

|

|

| Zinc |

% |

2.99 |

2.72 |

2.78 |

21 bps |

2.90 |

2.82 |

8 bps |

| Copper |

% |

0.37 |

0.35 |

0.30 |

6 bps |

0.33 |

0.33 |

(0 bps) |

| Lead |

% |

0.67 |

0.64 |

0.62 |

5 bps |

0.67 |

0.61 |

6 bps |

| Silver |

oz/t |

1.01 |

1.02 |

1.08 |

(6.3%) |

1.02 |

1.08 |

(5.7%) |

| Gold |

oz/t |

0.005 |

0.005 |

0.005 |

2.0% |

0.005 |

0.005 |

3.0% |

| |

|

|

|

|

|

|

|

|

| Production | metal contained |

|

|

|

|

|

|

|

| Zinc |

kt |

87.4 |

80.7 |

76.0 |

15.0% |

242.9 |

221.5 |

9.6% |

| Copper |

kt |

9.3 |

8.7 |

7.4 |

24.7% |

24.0 |

23.9 |

0.5% |

| Lead |

kt |

16.5 |

16.0 |

15.3 |

7.9% |

47.6 |

41.8 |

14.0% |

| Silver |

MMoz |

2.6 |

2.6 |

2.6 |

(0.5%) |

7.6 |

7.4 |

1.8% |

| Gold |

koz |

6.6 |

6.8 |

7.1 |

(7.1%) |

19.9 |

20.3 |

(2.0%) |

| Zinc Equivalent (1) |

kt |

141.8 |

133.5 |

125.2 |

13.3% |

393.3 |

367.7 |

7.0% |

(1) Consolidated mining production in kt

of zinc equivalent is calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade, assuming 2022 LME average

benchmark prices: Zn: US$1.58/lb; Cu: US$3.99/lb; Pb: US$0.98/lb; Ag: US$21.7/oz; Au: US$1,800/oz.

In 3Q23, treated ore volume was 3,470kt

up 11% year-over-year, explained by better plant performance in El Porvenir, Vazante and Morro Agudo and the beginning of production in

Aripuanã. However, Cerro Lindo treated ore slightly dropped by 3%, and was in line with our expectations for the year (following

the current mine sequencing plan), while Atacocha decreased by 14% explained by the temporary suspension of production for approximately

one month (end of June through end of July) in the period due to illegal protest activities.

Compared to 2Q23, treated ore volume decreased

by 2%, mainly driven by the Atacocha and Aripuanã mines.

The ore throughput, year-over-year, increased

at El Porvenir (+8%), Vazante (+3%) and Morro Agudo (+27%), while Cerro Lindo decreased by (-3%) and Atacocha decreased by (-14%).

Zinc production of 87kt in the quarter

rose by 15% from 3Q22, mainly explained by the increase in treated ore volume and the start-up of the Aripuanã mine. Compared with

2Q23, zinc production rose by 8%, mainly due to the higher volumes from Cerro Lindo, Morro Agudo and Vazante, in addition to Aripuanã

ramp-up phase progress.

Copper production of 9kt increased by

25% from 3Q22, as a result of higher average grade in Cerro Lindo and the Aripuanã ramp-up. Compared to 2Q23, copper production

was 7% higher, mainly driven by Cerro Lindo performance in the period.

Lead production increased by 8% year-over-year

and 3% quarter-over-quarter driven by El Porvenir, Morro Agudo and Aripuanã.

In 9M23, treated ore volume increased

by 12% year-over-year to 10,147kt mainly explained by the higher ore throughput in all mines, except Atacocha. Zinc average grade was

up 8bps to 2.90%.

| | 16 |

Earnings Release – 3Q23 | |

Therefore, zinc production totaled 243kt,

10% higher than in 9M22. Copper production was 0.5% higher and lead production increased by 14% to 48kt, following higher average grades.

Cerro Lindo

Cerro Lindo

(100% basis) |

|

3Q23 |

2Q23 |

1Q23 |

9M23 |

4Q22 |

3Q22 |

2Q22 |

1Q22 |

9M22 |

| |

|

|

|

|

|

|

|

|

|

|

| Ore Mined |

kt |

1,515 |

1,595 |

1,254 |

4,365 |

1,581 |

1,558 |

1,698 |

1,425 |

4,681 |

| Treated Ore |

kt |

1,540 |

1,530 |

1,277 |

4,347 |

1,589 |

1,594 |

1,661 |

1,392 |

4,647 |

| |

|

|

|

|

|

|

|

|

|

|

| Grade |

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

% |

1.63 |

1.31 |

1.38 |

1.44 |

1.49 |

1.42 |

1.58 |

1.71 |

1.57 |

| Copper |

% |

0.63 |

0.57 |

0.48 |

0.57 |

0.65 |

0.55 |

0.66 |

0.57 |

0.59 |

| Lead |

% |

0.32 |

0.33 |

0.25 |

0.30 |

0.28 |

0.37 |

0.35 |

0.34 |

0.35 |

| Silver |

oz/t |

0.81 |

0.83 |

0.72 |

0.79 |

0.70 |

0.94 |

0.99 |

0.92 |

0.95 |

| Gold |

oz/t |

0.002 |

0.002 |

0.002 |

0.002 |

0.003 |

0.002 |

0.003 |

0.003 |

0.002 |

| |

|

|

|

|

|

|

|

|

|

|

| Production | metal contained |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

kt |

21.7 |

16.9 |

15.0 |

53.6 |

20.7 |

19.9 |

22.7 |

21.1 |

63.7 |

| Copper |

kt |

8.1 |

7.4 |

5.2 |

20.7 |

9.1 |

7.4 |

9.5 |

6.8 |

23.7 |

| Lead |

kt |

3.6 |

3.6 |

2.1 |

9.3 |

3.2 |

4.7 |

4.4 |

3.4 |

12.5 |

| Silver |

MMoz |

0.9 |

0.9 |

0.6 |

2.5 |

0.8 |

1.1 |

1.2 |

1.0 |

3.3 |

| Gold |

koz |

0.7 |

0.8 |

0.7 |

2.2 |

0.9 |

1.0 |

1.1 |

1.1 |

3.2 |

| |

|

|

|

|

|

|

|

|

|

|

| Zinc sales |

kt |

20.8 |

17.5 |

14.8 |

53.1 |

19.9 |

19.7 |

22.9 |

23.4 |

66.0 |

| |

|

|

|

|

|

|

|

|

|

|

| Costs |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Cost of sales |

US$ mm |

88.6 |

86.5 |

81.6 |

256.7 |

99.0 |

94.6 |

105.9 |

97.0 |

297.5 |

| Cost ROM (2) |

US$/t |

41.3 |

39.8 |

39.6 |

40.3 |

42.2 |

40.1 |

38.2 |

41.0 |

39.7 |

| Cash cost (1) |

US$/lb |

(0.18) |

(0.13) |

(0.02) |

(0.12) |

(0.38) |

0.37 |

(0.59) |

(0.34) |

(0.22) |

| Sustaining cash cost (1) |

US$/lb |

0.07 |

0.15 |

0.23 |

0.14 |

(0.04) |

0.59 |

(0.39) |

(0.19) |

(0.03) |

| |

|

|

|

|

|

|

|

|

|

|

| CAPEX |

US$ mm |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Sustaining |

|

9.1 |

9.4 |

8.0 |

26.5 |

12.8 |

8.6 |

9.4 |

7.3 |

25.3 |

| Other |

|

2.0 |

1.5 |

0.4 |

3.9 |

2.1 |

1.0 |

0.8 |

0.5 |

2.3 |

(1) Our cash cost and sustaining cash cost

are net of by-products credits, measured with respect to zinc sold per mine. For a cash cost reconciliation to COGS, please refer to Appendix

– All in Sustaining Cash Cost | Mining.

(2) Our cost per ROM is measured with respect

to treated ore volume. Refer to “Use of Non-IFRS Financial Measures” for further information.

Zinc production of 22kt increased 9% year-over-year

and 28% quarter-over-quarter.

During 3Q23, according to the mine sequencing

plan, areas with better zinc grades were prioritized, resulting in higher zinc production.

| | 17 |

Earnings Release – 3Q23 | |

Zinc head grade averaged 1.63% in the

quarter, up 20bps and 32bps compared to 3Q22 and 2Q23, respectively.

Copper production of 8kt increased by

11% compared to 3Q22 and increased by 10% compared to 2Q23. Copper average grade was 0.63%, up 9bps and 6bps from 3Q22 and 2Q23, respectively.

Lead production was 3.6kt, down 24% year-over-year

driven by lower treated ore and lead average grade in the period. Compared to 2Q23, lead production was relatively flat.

In the first nine months of 2023, zinc

production totaled 54kt, down 16% compared to 9M22. Copper and lead production were down 13% and 26%, to 21kt and 9kt, respectively, as

daily production for all metals was significantly reduced in 1Q23.

Cost

Cost of sales was US$89 million in 3Q23

compared to US$95 million in the same period last year, mainly due to depreciation and amortization and lower treated ore volume. Compared

to 2Q23, cost of sales increased by 2%, mainly driven by higher variable costs in line with higher volumes produced.

Run-of-mine mining cost was US$41.3/t

in the quarter, up 3% and 4% from 3Q22 and 2Q23, respectively, primarily explained by the increase in operational costs related to mine

development, which contributed to higher grades in the period.

Cash cost net of by-products in 3Q23 decreased

to US$(0.18)/lb compared with US$0.37/lb in 3Q22 and US$(0.13)/lb in 2Q23. The performance year-over-year was mainly explained by higher

by-products contribution, particularly lead and copper, while the quarter-over-quarter performance was explained by higher production

volumes, which was partially offset by lower by-products prices (copper and silver).

CAPEX

In 3Q23, sustaining capital expenditures

amounted to US$9.1 million, mainly related to mining development, and other mining infrastructure expenses, totaling US$26 million in

9M23.

El Porvenir

El Porvenir

(100% basis) |

|

3Q23 |

2Q23 |

1Q23 |

9M23 |

4Q22 |

3Q22 |

2Q22 |

1Q22 |

9M22 |

| |

|

|

|

|

|

|

|

|

|

|

| Ore Mined |

kt |

568 |

546 |

544 |

1,658 |

551 |

529 |

520 |

513 |

1,563 |

| Treated Ore |

kt |

568 |

546 |

544 |

1,658 |

550 |

527 |

521 |

514 |

1,562 |

| |

|

|

|

|

|

|

|

|

|

|

| Grade |

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

% |

2.89 |

2.89 |

2.82 |

2.87 |

2.61 |

2.77 |

2.86 |

2.96 |

2.86 |

| Copper |

% |

0.16 |

0.17 |

0.15 |

0.16 |

0.13 |

0.16 |

0.17 |

0.18 |

0.17 |

| Lead |

% |

1.36 |

1.35 |

1.38 |

1.36 |

1.38 |

1.34 |

1.34 |

1.31 |

1.33 |

| Silver |

oz/t |

2.22 |

2.42 |

2.55 |

2.39 |

2.64 |

2.45 |

2.35 |

2.41 |

2.40 |

| Gold |

oz/t |

0.010 |

0.011 |

0.011 |

0.011 |

0.012 |

0.011 |

0.011 |

0.013 |

0.012 |

| |

|

|

|

|

|

|

|

|

|

|

| Production | metal contained |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

kt |

14.4 |

13.8 |

13.6 |

41.9 |

12.6 |

12.7 |

13.0 |

13.2 |

39.0 |

| Copper |

kt |

0.1 |

0.1 |

0.1 |

0.3 |

0.0 |

0.1 |

0.1 |

0.1 |

0.2 |

| Lead |

kt |

6.3 |

6.0 |

6.2 |

18.5 |

6.3 |

5.8 |

5.7 |

5.4 |

16.9 |

| | 18 |

Earnings Release – 3Q23 | |

El Porvenir

(100% basis) |

|

3Q23 |

2Q23 |

1Q23 |

9M23 |

4Q22 |

3Q22 |

2Q22 |

1Q22 |

9M22 |

| Silver |

MMoz |

1.0 |

1.1 |

1.2 |

3.3 |

1.2 |

1.0 |

1.0 |

1.0 |

3.0 |

| Gold |

koz |

2.0 |

2.2 |

2.3 |

6.6 |

2.5 |

2.4 |

2.1 |

2.2 |

6.7 |

| |

|

|

|

|

|

|

|

|

|

|

| Zinc sales |

kt |

14.5 |

14.5 |

14.4 |

43.5 |

12.1 |

12.4 |

14.0 |

13.5 |

39.9 |

| |

|

|

|

|

|

|

|

|

|

|

| Costs |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Cost of sales |

US$ mm |

47.8 |

48.1 |

51.8 |

147.7 |

39.2 |

40.1 |

45.6 |

42.9 |

128.7 |

| Cost ROM (2) |

US$/t |

57.5 |

63.1 |

60.1 |

60.2 |

58.6 |

58.5 |

60.1 |

62.1 |

60.2 |

| Cash cost (1) |

US$/lb |

0.20 |

0.35 |

0.22 |

0.26 |

(0.00) |

0.63 |

0.31 |

0.37 |

0.43 |

| Sustaining cash cost (1) |

US$/lb |

0.73 |

0.65 |

0.64 |

0.67 |

0.63 |

0.98 |

0.48 |

0.54 |

0.66 |

| |

|

|

|

|

|

|

|

|

|

|

| CAPEX |

US$ mm |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Sustaining |

|

16.7 |

9.7 |

13.4 |

39.8 |

16.6 |

9.4 |

5.1 |

4.7 |

19.1 |

| Other |

|

- |

(0.0) |

(0.0) |

(0.0) |

0.3 |

0.1 |

0.2 |

0.4 |

0.7 |

(1) Our cash cost and sustaining cash cost

are net of by-products credits, measured with respect to zinc sold per mine. For a cash cost reconciliation to COGS, please refer to Appendix

– All in Sustaining Cash Cost | Mining.

(2) Our cost per ROM is measured with respect

to treated ore volume. Refer to “Use of Non-IFRS Financial Measures” for further information.

In 3Q23, zinc production of 14kt was up

13% and 4% from 3Q22 and 2Q23, respectively. Zinc grade increased to 2.89% in the quarter, as production focused on cut and fill areas

with higher grades.

Lead production in 3Q23 increased by 9%

and 5% from 3Q22 and 2Q23, respectively, while silver production decreased by 2% and 5% from the same periods, respectively, as a result

of lower grades in the period.

The mine is running at full throughput

capacity and achieved 568kt of ore mined and treated ore in 3Q23, which represents its record production performance for a quarterly period.

In the first nine months of 2023, zinc

production totaled 42kt, up 7% compared to 9M22. Lead and silver production were up 9% to 18kt and 8% to 3MMoz, respectively, following

higher average grades.

Cost

Cost of sales was US$48 million in 3Q23

compared to US$40 million in 3Q22 due to higher inventory costs and inflation, which impacted mainly third-party services. Compared to

2Q23, cost of sales was relatively flat.

Run-of-mine mining cost was US$58/t in

the quarter, down 2% and 9% from 3Q22 and 2Q23, mainly driven by higher treated ore.

Cash cost net of by-products in 3Q23 decreased

to US$0.20/lb compared to 3Q22, mainly driven by higher by-products contribution, explained by higher lead prices and volumes. Compared

to 2Q23, cash cost decreased US$0.14/lb due to lower operating costs and higher by-products contribution.

CAPEX

In 3Q23, sustaining capital expenditures

amounted to US$16.7 million, mainly related to mine development, the tailings dam project and other mining infrastructure implementation,

totaling US$40 million in 9M23.

Atacocha

| | 19 |

Earnings Release – 3Q23 | |

Atacocha

(100% basis) |

|

3Q23 |

2Q23 |

1Q23 |

9M23 |

4Q22 |

3Q22 |

2Q22 |

1Q22 |

9M22 |

| |

|

|

|

|

|

|

|

|

|

|

| Ore Mined |

kt |

290 |

363 |

342 |

995 |

394 |

339 |

325 |

296 |

960 |

| Treated Ore |

kt |

290 |

373 |

342 |

1,004 |

394 |

339 |

325 |

296 |

960 |

| |

|

|

|

|

|

|

|

|

|

|

| Grade |

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

% |

0.58 |

0.67 |

0.94 |

0.73 |

0.87 |

0.90 |

0.82 |

1.00 |

0.90 |

| Lead |

% |

0.84 |

0.80 |

1.23 |

0.96 |

1.20 |

0.96 |

0.83 |

0.82 |

0.87 |

| Silver |

oz/t |

1.33 |

1.11 |

1.24 |

1.21 |

1.26 |

0.99 |

0.99 |

0.94 |

0.97 |

| Gold |

oz/t |

0.009 |

0.010 |

0.012 |

0.010 |

0.013 |

0.016 |

0.015 |

0.015 |

0.016 |

| |

|

|

|

|

|

|

|

|

|

|

| Production | metal contained |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Zinc |

kt |

1.2 |

1.9 |

2.5 |

5.5 |

2.6 |

2.4 |

2.1 |

2.4 |

6.9 |

| Lead |

kt |

2.1 |

2.6 |

3.6 |

8.2 |

4.1 |

2.8 |

2.3 |

2.1 |

7.1 |

| Silver |

MMoz |

0.3 |

0.3 |

0.4 |

1.0 |

0.4 |

0.3 |

0.3 |

0.2 |

0.7 |

| Gold |

koz |

1.4 |

2.2 |

2.6 |

6.2 |

3.1 |

3.8 |

3.6 |

3.1 |

10.5 |

| |

|

|

|

|

|

|

|

|

|

|

| Zinc sales |

kt |

1.1 |

2.4 |

2.3 |

5.8 |

2.9 |

2.3 |

2.3 |

2.1 |

6.7 |

| |

|

|

|

|

|

|

|

|

|

|

| Costs |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Cost of sales |

US$ mm |

13.1 |

19.8 |

16.5 |

49.5 |

23.3 |

15.7 |

21.1 |

15.3 |

52.1 |

| Cost ROM (2) |

US$/t |

30.7 |

31.7 |

36.6 |

33.1 |

35.7 |

37.7 |

35.5 |

38.0 |

37.1 |

| Cash cost (1) |

US$/lb |

(1.22) |

(1.05) |

(0.12) |

(0.72) |

(1.54) |

0.54 |

(1.28) |

(0.30) |

(0.35) |

| Sustaining cash cost (1) |

US$/lb |

(0.19) |

(0.58) |

0.81 |

0.05 |

(1.36) |

0.64 |

(1.14) |

0.14 |

(0.13) |

| |

|

|

|

|

|

|

|

|

|

|

| CAPEX |

US$ mm |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| Sustaining |

|

2.6 |

2.5 |

4.7 |

9.7 |

1.1 |

0.5 |

0.8 |

2.0 |

3.3 |

| Other |

|

0.0 |

0.0 |

(0.0) |

0.0 |

0.1 |

- |

(0.0) |

0.0 |

0.0 |

(1) Our cash cost and sustaining cash cost