CA Market News

4週前

CA Market News

4週前

Sun Life Receives Regulatory Approval of Normal Course Issuer Bid RenewalMay 26, 2026 5:01 PM

PR Newswire (Canada) TORONTO, May 26, 2026 /CNW/ - Sun Life Financial Inc. (TSX: SLF) (NYSE: SLF) (the "Company") announced today that the Office of the Superintendent of Financial Institutions ("OSFI") and the Toronto Stock Exchange (the "TSX") have approved the renewal of the Company's previously announced normal course issuer bid to purchase up to 10,000,000 of its common shares ("common shares") (representing approximately 1.8% of the 554,255,267 common shares issued and outstanding as at May 15, 2026) (the "NCIB").The NCIB will provide the Company with the flexibility to acquire common shares in order to return capital to shareholders as part of its overall capital management strategy.The NCIB will commence on May 29, 2026 and continue until May 28, 2027, or such earlier date as the Company may determine. The average daily trading volume on the TSX for the six months ending April 30, 2026 was 2,008,137 common shares (the "ADTV"). Purchases under the NCIB may be made through the facilities of the TSX, other Canadian stock exchanges, the New York Stock Exchange (the "NYSE") and/or alternative trading platforms in Canada and the United States, at prevailing market rates. In accordance with the TSX rules, the Company may purchase up to 502,034 of its common shares on the TSX during any trading day, which represents 25% of the ADTV, subject to the TSX rules permitting block purchases. Subject to certain exceptions for block purchases, the maximum number of common shares which can be purchased per day on the NYSE will be 25% of the average daily trading volume for the four calendar weeks preceding the date of purchase.Subject to regulatory approval, purchases under the NCIB may also be made by way of private agreements or share repurchase programs under issuer bid exemption orders issued by securities regulatory authorities. Any purchases made under an exemption order issued by a securities regulatory authority will generally be at a discount to the prevailing market price. The actual number of common shares purchased under the NCIB, and the timing of such purchases (if any), will be determined by the Company. Any common shares purchased by the Company pursuant to the NCIB will be cancelled or used in connection with certain equity settled incentive arrangements.The Company has established an automatic repurchase plan with its designated broker in order to facilitate purchases of common shares under the NCIB. Under the automatic repurchase plan, the Company's designated broker may purchase common shares pursuant to the NCIB at times when the Company ordinarily would not be active in the market due to its own internal trading blackout periods, insider trading rules or otherwise. Purchases made pursuant to the automatic repurchase plan, if any, will be made by the Company's designated broker based upon the parameters prescribed by the TSX, the NYSE, applicable Canadian and U.S. securities laws and the terms of the written agreement between the Company and its designated broker. The automatic repurchase plan constitutes an "automatic plan" for purposes of applicable Canadian securities legislation and has been pre-cleared by the TSX.Under its prior normal course issuer bid (the "Prior NCIB"), which commenced on June 9, 2025 and expired on May 21, 2026, the Company was permitted to purchase up to 10,570,915 common shares. As of May 15, 2026, the Company had purchased 10,570,915 common shares under the Prior NCIB at a weighted average price of $83.33 per common share through the facilities of the TSX, other Canadian stock exchanges, the NYSE and/or alternative trading platforms in Canada and the United States.Forward-Looking Statements

From time to time, the Company makes written or oral forward-looking statements within the meaning of certain securities laws, including the "safe harbour" provisions of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities legislation. Forward-looking statements contained in this news release include statements (i) relating to the NCIB (including, but not limited to, statements regarding future purchases of common shares under the NCIB, including under the automatic repurchase plan), (ii) that are predictive in nature or that depend upon or refer to future events or conditions, and (iii) that include words such as "intends", "expects", "will" and similar expressions. The forward-looking statements made in this news release are stated as at May 26, 2026, represent the Company's current expectations, estimates and projections regarding future events and are not historical facts. These statements are not a guarantee of future performance and involve assumptions and risks and uncertainties that are difficult to predict. Some of these assumptions and risks and uncertainties are described further in the Company's management's discussion and analysis for the year ended December 31, 2025 under the heading "Forward-looking Statements", in the risk factors set out in the Company's annual information form for the year ended December 31, 2025 under the heading "Risk Factors", and in the Company's interim management's discussion and analysis for the quarter ended March 31, 2026 under the heading "Risk Management", in the other factors detailed in the Company's annual and interim financial statements and in the Company's other filings with Canadian and U.S. securities regulators, which are available for review at www.sedarplus.ca and www.sec.gov, respectively. Actual results may differ materially from those expressed, implied or forecasted in such forward-looking statements and there is no assurance that any common shares will be purchased under the NCIB (including under the automatic repurchase plan).The Company does not undertake any obligation to update or revise its forward-looking statements to reflect events or circumstances after the date of this news release or to reflect the occurrence of unanticipated events, except as required by law.About Sun Life

Sun Life is a leading international financial services organization providing asset management, wealth, insurance and health solutions to individual and institutional Clients. Sun Life has operations in a number of markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda. As of March 31, 2026, Sun Life had total assets under management of $1.58 trillion. For more information, please visit www.sunlife.com. Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges under the ticker symbol SLF.Note to editors: All figures in Canadian dollarsTo contact Sun Life media relations, please email Media.Relations@sunlife.com.To contact Sun Life investor relations, please email Investor_Relations@sunlife.com. View original content to download multimedia:https://www.prnewswire.com/news-releases/sun-life-receives-regulatory-approval-of-normal-course-issuer-bid-renewal-302782303.htmlSOURCE Sun Life Financial Inc. - Financial News Original: Sun Life Receives Regulatory Approval of Normal Course Issuer Bid Renewal

CA Market News

1月前

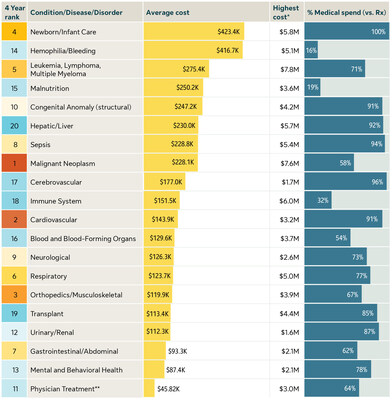

What drives multimillion-dollar medical claims? Sun Life report shows secondary health conditions, hospital stays and specialty drugs among key factorsMay 21, 2026 6:45 PM

PR Newswire (US) WELLESLEY, Mass., May 21, 2026 /PRNewswire/ -- Sun Life U.S. has released its annual High-Cost Claims and Injectable Drug Trends report, which analyzed over 70,000 high-dollar medical claims from more than 3,300 self-funded employers across the country. This year's report shows that secondary (comorbid) conditions, long inpatient hospitalizations and injectable drugs are the biggest drivers of claims above $3 million. Other contributing factors include conditions existing from birth (congenital anomalies), complicated surgeries and gene therapies. Sun Life spotlights the costliest medical conditions and injectable drugs driving million-dollar medical claimsSome of the most common conditions resulting in claims above $3 million include orthopedic/musculoskeletal (MSK) conditions, newborn/infant care (premature birth) and cancer. While cancer and premature births have been top drivers of million-dollar and multimillion-dollar claims for several years, orthopedic/MSK conditions have only recently reached this level, suggesting increases in severity as well as developments in therapies and treatments. Orthopedic/MSK conditions and cancer are also two of the most frequent diagnoses for short-term disability claims."We have a real opportunity to help people achieve meaningful, improved health outcomes by prioritizing whole-person care," said Jennifer Collier, president, Health and Risk Solutions, Sun Life U.S. "Several of these high-cost health conditions occur as comorbidities, such as orthopedic/MSK and cancer. We tend to think about diagnoses and treatments individually, but care is more effective when we recognize the interconnectedness of health conditions. By getting people the right care, we can improve both health and cost outcomes, benefitting both members and employers."Comorbidities have long been a major contributor to high-cost and multimillion-dollar claims. Multiple conditions can complicate treatment plans, exacerbate the primary diagnosis and prolong recovery. Sun Life's claims data analysis in the report identifies strong connections among cancer, cardiovascular and chronic kidney diseases, and orthopedic/MSK conditions. These conditions share several risk factors, including age, obesity, diabetes and inflammation.Rising cost of care

Healthcare costs continue to increase as specialty treatments and gene therapies become more prevalent. Supporting these life-saving treatments is crucial, as Sun Life continues to explore ways to improve outcomes and manage risk.Million-dollar+ claims increased in frequency by 46% from 2022 – 2026.Spending on treating liver disease grew 43% in 2025 from the previous year, with an average cost per patient of $230,000.The most expensive drug treatment, at an average cost of $3.6 million, was Elevidys, a gene therapy that slows the progression of Duchenne muscular dystrophy.The highest multimillion-dollar claims were for blood cancers (leukemia/lymphoma/myeloma), with an average of $5.45 million in 2025; the highest claim for a single leukemia patient in 2025 was nearly $8 million.Impact of GLP-1s

Many high-dollar conditions are associated with obesity and diabetes. Employers have an opportunity to broaden coverage of GLP-1s and proactively reduce the risk of major health conditions that can result in high-dollar claims.While the cost of GLP-1s per person is still relatively low, high-dollar claims that include GLP-1s increased by 24% over the past year.GLP-1s have broader patient eligibility than many of the higher-cost specialty drugs in Sun Life's report, and can significantly reduce the risk of costlier conditions associated with obesity.Several of the highest-cost conditions (kidney disease, cardiovascular disease and orthopedic/MSK conditions), are often associated with obesity and related health issues.Why health services matter

Programs that provide health support services can have substantial impact on health outcomes and reduce medical costs, particularly if they target the more frequently seen conditions like cancer and MSK – also both common conditions for disability leave.Osteoarthritis (OA), a common MSK condition, is more prevalent (54%) in patients on dialysis for chronic kidney disease (CKD). Research cited in the report suggests that OA may even be considered a predictor for CKD.The most prevalent and frequent diagnosis among people aged 20–59 (i.e. those in the workforce) were solid cancers (malignant neoplasm).Sun Life's Health and Risk Solutions are designed to address the conditions and factors that drive high-dollar claims and are available with its stop-loss coverage. The solutions include:Orthopedic/MSK health support services through Hinge HealthClinical 360 High-dollar claims review from clinical experts to identify cost reduction opportunitiesAccess to site- or home-based specialty drug infusions through OptiMedHealth Navigator – personalized healthcare navigation services that get people the right care at the right timeExpert Cancer Review – second opinions from expert oncologists to ensure patients receive right diagnosis and treatment plan (also part of Health Navigator services)Sun Life issues the High-Cost Claims and Injectable Drug Trends report annually, covering four-year spans of medical stop-loss claims. As the largest independent stop-loss provider in the country, Sun Life is uniquely qualified to offer analysis and commentary on the prevailing trends in care navigation, rising cost of care, complex conditions and drug treatments.Click here to register for Sun Life's upcoming webinar to learn more about this year's report from Sun Life experts. To explore Sun Life's Health and Risk Solutions, including stop-loss insurance, visit: Stop-Loss insurance | Sun Life U.S.About Sun LifeSun Life is a leading international financial services organization providing asset management, wealth, insurance and health solutions to individual and institutional Clients. Sun Life has operations in a number of markets worldwide, including Canada, the U.S., the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda. As of March 31, 2026, Sun Life had total assets under management of C$1.58 trillion. For more information, please visit www.sunlife.com.Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges under the ticker symbol SLF.Sun Life U.S. is one of the largest providers of employee and government benefits, helping approximately 48 million Americans access the care and coverage they need. Through employers, industry partners and government programs, Sun Life U.S. offers a portfolio of benefits and services, including dental, vision, disability, absence management, life, supplemental health, medical stop-loss insurance, and healthcare navigation. Sun Life employs nearly 8,300 people in the U.S., including associates in our partner dental practices and affiliated companies in asset management. Group insurance policies are issued by Sun Life Assurance Company of Canada (Wellesley Hills, Mass.), except in New York, where policies are issued by Sun Life and Health Insurance Company (U.S.) (Lansing, Mich.). For more information visit our website and newsroom.Media Contact:Devon Fernald

Sun Life U.S.

Devon.portney.fernald@sunlife.com View original content to download multimedia:https://www.prnewswire.com/news-releases/what-drives-multimillion-dollar-medical-claims-sun-life-report-shows-secondary-health-conditions-hospital-stays-and-specialty-drugs-among-key-factors-302779625.htmlSOURCE Sun Life U.S. Original: What drives multimillion-dollar medical claims? Sun Life report shows secondary health conditions, hospital stays and specialty drugs among key factors

CA Market News

2月前

La Sun Life annonce ses résultats du premier trimestre de l'exercice 2026May 6, 2026 5:01 PM

PR Newswire (Canada) La Sun Life1) a généré un bénéfice solide au premier trimestre, grâce à une forte croissance en Asie, au Canada et aux solutions en santé et en gestion des risques aux États-Unis et à un rendement des capitaux propres sous-jacent de 18,6 %2).TORONTO, le 6 mai 2026 /CNW/ - La Financière Sun Life inc.1) (TSX : SLF) (NYSE : SLF) a annoncé ses résultats pour le premier trimestre clos le 31 mars 2026.Le bénéfice net sous-jacent2) s'est établi à 1 050 M$, en hausse de 5 M$ par rapport au premier trimestre de 2025.Le bénéfice net déclaré3) s'est chiffré à 465 M$, en baisse de 463 M$, ou 50 %, par rapport au premier trimestre de 2025.Le bénéfice par action sous-jacent2), 4) s'est chiffré à 1,89 $, en hausse de 4 % par rapport au premier trimestre de 2025; le bénéfice par action déclaré4) s'est établi à 0,84 $, en baisse de 48 % par rapport au premier trimestre de 2025.Le rendement des capitaux propres sous-jacent2) s'est établi à 18,6 %; le rendement des capitaux propres déclaré2) s'est établi à 8,2 %.L'actif géré2) s'est chiffré à 1 575 G$, en hausse de 23 G$ par rapport au premier trimestre de 2025.Le ratio du TSAV de la FSL inc. s'est établi à 143 %5).Nous avons l'intention de renouveler notre offre publique de rachat dans le cours normal des activités visant le rachat d'un nombre maximal de 10 millions de nos actions ordinaires6).Le dividende par action ordinaire a augmenté, passant de 0,92 $ à 0,96 $ par action.« Ce trimestre, nous avons affiché une croissance solide de nos activités d'assurance, avec en tête l'Asie, le Canada et les solutions en santé et en gestion des risques aux États-Unis, a déclaré Kevin Strain, président et chef de la direction, Sun Life. Nous avons aussi élargi davantage la portée de notre plateforme de gestion d'actifs. En effet, nous avons déployé plus de 2,4 G$ de capital pour l'acquisition des participations restantes dans BGO et dans Crescent Capital et annoncé notre intention d'acquérir Bell Partners, un gestionnaire de placements immobiliers de premier plan aux États-Unis spécialisé dans le logement collectif et une entreprise verticalement intégrée de gestion immobilière. »« En même temps, nous avons conservé notre élan et continué à progresser vers l'atteinte de nos objectifs stratégiques liés au numérique et à l'IA, au moyen de données, d'automatisation et de solutions intelligentes qui simplifient les expériences, renforcent l'engagement et améliorent les résultats pour les Clients partout dans le monde. » Points saillants financiers et opérationnels

Résultats trimestrielsRentabilitéT1 26T1 25

Bénéfice net sous-jacent (en millions de dollars)2)1 0501 045

Bénéfice net déclaré - actionnaires ordinaires - avant les éléments importants du T1 26 (en millions de dollars)2), 7)775928

Bénéfice net déclaré - actionnaires ordinaires (en millions de dollars)465928

Bénéfice par action sous-jacent (en dollars)2), 4)1,891,82

Bénéfice par action déclaré (en dollars)4)0,841,62

Rendement des capitaux propres sous-jacent2)18,6 %17,7 %

Rendement des capitaux propres déclaré2)8,2 %15,7 %CroissanceT1 26T1 25

Flux bruts de gestion d'actifs et souscriptions de produits de gestion de patrimoine (en millions de dollars)2)62 36562 221

Flux nets de gestion d'actifs et souscriptions nettes de produits de gestion de patrimoine (en millions de dollars)2)(17 844)(6 154)

Souscriptions d'assurance collective (en millions de dollars)2), 8)552580

Souscriptions d'assurance individuelle (en millions de dollars)2), 9)1 153874

Actif géré (en milliards de dollars)2), 10)1 5751 552

Marge sur services contractuels (« MSC ») liée aux affaires nouvelles (en millions de dollars)2)429406Solidité financièreT1 26T1 25

Ratios du TSAV (à la clôture de la période)5)

Financière Sun Life inc.143 %149 %

Sun Life du Canada11)134 %141 %

Ratio de levier financier (à la clôture de la période)2), 12)23,2 %20,1 %Points saillants financiers et opérationnels - comparaison trimestrielle (entre le T1 2026 et le T1 2025)(en millions de dollars)T1 26

Sun LifeGestion d'actifs Sun LifeCanadaÉtats-UnisAsieOrganisation internationaleBénéfice net sous-jacent2)1 050363370218216(117)Bénéfice net déclaré - actionnaires ordinaires - avant les éléments importants du T1 26 (en millions de dollars)2), 7)775339232151183(130)Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires46517487151183(130)Variation du bénéfice net sous-jacent (en % d'un exercice à l'autre)— %(7) %7 %— %17 %n.s.13)Variation du bénéfice net déclaré - actionnaires ordinaires - avant les éléments importants du T1 26 (en % d'un exercice à l'autre)2), 7)(16) %(8) %(27) %(19) %19 %n.s.13)Variation du bénéfice net déclaré (en % d'un exercice à l'autre)(50) %(53) %(73) %(19) %19 %n.s.13)Flux bruts de gestion d'actifs et souscriptions de produits de gestion de patrimoine2)62 36555 3075 877—1 181—Souscriptions d'assurance collective2)552—29522037—Souscriptions d'assurance individuelle2) 1 153—114—1 039—Variation des flux bruts de gestion d'actifs et des souscriptions de produits de gestion de patrimoine (en % d'un exercice à l'autre)— %— %(6) %—26 %—Variation des souscriptions d'assurance collective (en % d'un exercice à l'autre)(5) %—(21) %25 %28 %—Variation des souscriptions d'assurance individuelle (en % d'un exercice à l'autre)32 %—(18) %—41 %—Le bénéfice net sous-jacent14) s'est chiffré à 1 050 M$, en hausse de 5 M$ par rapport à l'exercice précédent, en raison des facteurs suivants :Rendement solide en Asie reflétant la croissance des affaires à Hong Kong, et au Canada en raison de la hausse des produits tirés des honoraires attribuable à l'augmentation de l'actif géré. Ces facteurs ont été principalement contrebalancés par ce qui suit :Baisse des résultats à Gestion d'actifs Sun Life reflétant la diminution des honoraires de rattrapage et des produits nets tirés des placements en capitaux de lancement à Gestion SLC, la hausse des coûts de financement à l'Organisation internationale en appui à l'acquisition des participations restantes dans des sociétés liées de Gestion SLC, et l'incidence défavorable du change.Le bénéfice net déclaré s'est chiffré à 465 M$, en baisse de 463 M$, ou 50 % (bénéfice net déclaré avant les éléments importants du premier trimestre de 2026 de 775 M$2), 7), en baisse de 153 M$, ou 16 %), par rapport à l'exercice précédent, en raison des facteurs suivants :L'incidence des marchés reflétant principalement l'incidence défavorable des taux d'intérêt.Une charge de 165 M$ relative à l'acquisition des participations restantes dans des sociétés liées de Gestion SLC15).Une charge de 145 M$ reflétant le règlement proposé d'un litige au Canada15).L'incidence du change a donné lieu à une diminution de 35 M$ du bénéfice net sous-jacent et à une diminution de 17 M$ du bénéfice net déclaré.Le rendement des capitaux propres sous-jacent s'est établi à 18,6 % et le rendement des capitaux propres déclaré s'est établi à 8,2 % (premier trimestre de 2025 - 17,7 % et 15,7 %, respectivement). La FSL inc. a clôturé le trimestre avec un ratio du TSAV de 143 %.Points saillants des secteurs d'activitéGestion d'actifs Sun Life : Leader mondial en gestion d'actifs Le bénéfice net sous-jacent de Gestion d'actifs Sun Life s'est chiffré à 265 M$ US, en baisse de 8 M$ US, ou 3 %, par rapport à l'exercice précédent, en raison des facteurs suivants :MFS16) en hausse de 13 M$ US reflétant l'augmentation des produits tirés des honoraires attribuable à la hausse de l'actif net moyen, partiellement contrebalancée par l'augmentation des charges. La marge d'exploitation nette avant impôt de la MFS2) s'est améliorée et est passée à 36,0 % au premier trimestre de 2026, comparativement à 35,4 % à l'exercice précédent, en raison de la hausse de l'actif net moyen.Gestion SLC en baisse de 27 M$ US reflétant la baisse des produits nets tirés des placements en capitaux de lancement et le bénéfice tiré des honoraires2), qui a diminué de 25 % en raison de la hausse des honoraires de rattrapage à l'exercice précédent, partiellement contrebalancée par la diminution des charges. La marge sur le bénéfice tiré des honoraires2) s'est chiffrée à 26,3 % au premier trimestre de 2026, comparativement à 24,0 % à l'exercice précédent.Solutions et autres en hausse de 6 M$ US reflétant le résultat net favorable des activités de placement.Le bénéfice net déclaré s'est chiffré à 127 M$ US, en baisse de 131 M$ US, ou 51 %, par rapport à l'exercice précédent, en raison des facteurs suivants :Une charge de 119 M$ US relative à l'acquisition des participations restantes dans des sociétés liées de Gestion SLC15).L'incidence défavorable des marchés.La baisse du bénéfice net sous-jacent.L'incidence du change a donné lieu à une diminution de 16 M$ du bénéfice net sous-jacent et à une diminution de 3 M$ du bénéfice net déclaré.Les flux bruts de Gestion d'actifs Sun Life2) ont augmenté de 2,0 G$ US, ou 5 %, par rapport à l'exercice précédent, reflétant la hausse des flux bruts à Gestion SLC attribuable aux stratégies phares de crédit privé de Crescent Capital Group et à la plateforme de créances européennes de BentallGreenOak, et les flux bruts solides soutenus à la MFS.Le total de l'actif géré2) de Gestion d'actifs Sun Life s'est chiffré à 867,8 G$ US au premier trimestre de 2026 (premier trimestre de 2025 - 816,4 G$ US), et il se composait de ce qui suit :MFS : 622,2 G$ US (premier trimestre de 2025 - 603,8 G$ US).Gestion SLC : 188,9 G$ US (premier trimestre de 2025 - 177,2 G$ US).Solutions et autres : 56,7 G$ US (premier trimestre de 2025 - 35,4 G$ US).Le total des actifs gérés2) de Gestion d'actifs Sun Life s'est chiffré à 985,6 G$ US au premier trimestre de 2026, en hausse de 68,1 G$ US, ou 7 %, par rapport au premier trimestre de 2025.Les sorties nettes totales2) de 12,6 G$ US de Gestion d'actifs Sun Life au premier trimestre de 2026 (premier trimestre de 2025 - sorties nettes de 5,3 G$ US) reflètent ce qui suit :Les sorties nettes de 16,3 G$ US de la MFS (premier trimestre de 2025 - sorties nettes de 8,1 G$ US) attribuables aux sorties nettes aux affaires individuelles reflétant les sorties de capitaux soutenues sur les marchés américains des actions par les investisseurs individuels, et au rééquilibrage du portefeuille institutionnel.Les sorties nettes de 0,2 G$ US des Solutions et autres (premier trimestre de 2025 - entrées nettes de 0,8 G$ US). Ces facteurs ont été partiellement contrebalancés par l'élément suivant :Les entrées nettes de 3,9 G$ US de Gestion SLC (premier trimestre de 2025 - entrées nettes de 2,0 G$ US) en raison de la mobilisation de capitaux.Avec prise d'effet le 1er janvier 2026, nous avons étendu et officialisé notre pilier de gestion d'actifs, Gestion d'actifs Sun Life. Cette structure vise à accélérer la croissance de nos activités de gestion d'actifs, d'assurance et de gestion de patrimoine ainsi qu'à appuyer les partenariats stratégiques dans l'intérêt de nos Clients. Les résultats financiers de Gestion d'actifs Sun Life reflètent cette structure à partir de la même date.Au premier trimestre, nous avons achevé l'acquisition des participations restantes dans BentallGreenOak (« BGO ») et dans Crescent Capital Group (« Crescent »), ce qui témoigne de notre confiance envers leur leadership, leur rendement et leur potentiel de croissance à long terme. Nous avons acquis la participation restante de 44 % dans BGO pour un montant de 1,16 G$ US (1,59 G$ en dollars canadiens) et la participation restante de 49 % dans Crescent pour un montant de 608 M$ US (829 M$ en dollars canadiens).Dans le cadre de l'acquisition définitive et du nouveau modèle d'exploitation, Gestion SLC a introduit un programme d'actionnariat pour la direction, qui permet aux employés admissibles de détenir collectivement jusqu'à 25 % de la société. Le Programme d'actionnariat pour la direction a enregistré une forte participation et est conçu pour faire concorder les intérêts, fidéliser les meilleurs talents et soutenir la croissance à long terme.Nous avons aussi annoncé notre intention d'acquérir la totalité de Bell Partners Inc., un gestionnaire de placements immobiliers de premier plan aux États-Unis spécialisé dans le logement collectif et une entreprise verticalement intégrée de gestion immobilière. À la clôture de la transaction, Bell Partners deviendra notre plateforme opérationnelle pour les investissements dans le secteur résidentiel multifamilial aux États-Unis, sous la conduite de BGO. Bell Partners offre une plateforme nationale verticalement intégrée couvrant la gestion des placements, la gestion immobilière, les acquisitions, et la construction, et elle a conclu des transactions visant des appartements d'une valeur d'environ 11,9 G$ US depuis 2002, y compris des acquisitions de plus de 1,3 G$ US en 2025. La transaction devrait être conclue au second semestre de 2026, sous réserve des approbations des organismes de réglementation et de la Bourse de Toronto ainsi que de la satisfaction des conditions de clôture habituelles.Canada : Leader en santé, en gestion de patrimoine et en assuranceLe bénéfice net sous-jacent au Canada s'est établi à 370 M$, en hausse de 24 M$, ou 7 %, par rapport à l'exercice précédent en raison des facteurs suivants :La croissance des affaires reflétant la hausse des primes à la Sun Life Santé, l'augmentation des produits tirés des honoraires découlant de la hausse de l'actif géré et les résultats nets favorables des activités de placement. Ces facteurs ont été partiellement contrebalancés par ce qui suit :Les résultats moins favorables au chapitre de l'assurance.Le bénéfice net déclaré s'est établi à 87 M$, en baisse de 230 M$, ou 73 %, par rapport à l'exercice précédent en raison des facteurs suivants :Une charge de 145 M$ reflétant le règlement proposé d'un litige15).L'incidence des marchés reflétant l'incidence défavorable des taux d'intérêt, des marchés des actions et des résultats liés aux placements immobiliers17). Ces facteurs ont été partiellement contrebalancés par ce qui suit :La hausse du bénéfice net sous-jacent.Souscriptions au Canada18) :Les flux bruts de gestion d'actifs et souscriptions de produits de gestion de patrimoine se sont établis à 6 G$, en baisse de 6 %, reflétant la diminution des ventes de contrats importants par rapport à un exercice précédent solide pour les régimes à cotisations déterminées à la Gestion de patrimoine - Groupe19), en grande partie contrebalancée par la hausse des souscriptions de fonds communs de placement à la Gestion de patrimoine - Individuelle et l'augmentation des transferts d'actifs à la Gestion de patrimoine - Groupe19).Les souscriptions enregistrées à la Sun Life Santé se sont chiffrées à 295 M$, en baisse de 21 %, reflétant la diminution des ventes de contrats importants par rapport à un exercice précédent solide.Les souscriptions d'assurance individuelle se sont chiffrées à 114 M$, en baisse de 18 %, reflétant la diminution des souscriptions d'assurance-vie avec participation.Nous continuons à renforcer notre plateforme de gestion de patrimoine en offrant des solutions de placement solides et des expériences Client améliorées. Au cours du premier trimestre, nous avons élargi la gamme de produits de Placements mondiaux Sun Life (« PMSL ») en lançant deux nouvelles séries de fonds négociés en bourse (« FNB ») à faible volatilité, offrant aux Clients un accès amélioré aux marchés des actions mondiaux et internationaux. Nous avons également étendu l'utilisation de Recherche assistée, outil propulsé par l'IA, à l'ensemble du Centre de service à la clientèle des Régimes collectifs de retraite, simplifiant l'accès aux renseignements particuliers aux régimes pour offrir un service plus rapide et plus cohérent aux Clients. Au premier trimestre de 2026, notre plateforme de gestion de patrimoine a atteint un actif géré et administré20) de 261 G$, en hausse de 12 % par rapport à l'exercice précédent.De plus, à la Sun Life Santé, nous avons continué à renforcer le soutien à la santé en milieu de travail pour les promoteurs de régime et les participants. L'outil Explorateur Garanties Sun Life, lancé en février, est un outil d'analytique qui aide les promoteurs de régime à mieux comprendre et gérer leurs régimes de garanties grâce à des renseignements fondés sur les données. Nous avons également fait progresser le soutien complet à la santé des femmes en milieu de travail avec le lancement des soins liés à la ménopause fournis par Dialogue. Par l'entremise des Soins virtuels Lumino Santé, les participants de régime et les personnes à charge admissibles ont désormais accès à des plans de soins personnalisés, à une équipe multidisciplinaire ayant reçu une formation supplémentaire en soins liés à la ménopause, ainsi qu'à de l'accompagnement.États-Unis : Leader en santé et en garanties collectivesLe bénéfice net sous-jacent aux États-Unis s'est établi à 160 M$ US, en hausse de 9 M$ US, ou 6 %, par rapport à l'exercice précédent en raison des facteurs suivants :La hausse des résultats de la Gestion des affaires en vigueur reflétant les résultats nets favorables des activités de placement. Cette hausse a été en grande partie contrebalancée par ce qui suit :La baisse du bénéfice enregistré au chapitre des garanties de frais dentaires en raison de la baisse des produits et de l'incidence d'un paiement de prime rétroactif au cours de l'exercice précédent.Les résultats au chapitre des Garanties collectives reflètent la croissance solide des produits et l'amélioration des résultats enregistrés au chapitre de la morbidité pour l'assurance-maladie en excédent de pertes, partiellement contrebalancées par les résultats défavorables au chapitre de l'assurance invalidité de longue durée.Le bénéfice net déclaré s'est établi à 111 M$ US, en baisse de 18 M$ US, ou 14 %, par rapport à l'exercice précédent, en raison de l'incidence des marchés, reflétant surtout l'incidence défavorable des taux d'intérêt.L'incidence du change a donné lieu à une diminution de 10 M$ du bénéfice net sous-jacent et à une diminution de 9 M$ du bénéfice net déclaré.Les souscriptions aux États-Unis se sont chiffrées à 160 M$ US, en hausse de 30 % par rapport à l'exercice précédent, principalement en raison des facteurs suivants :La hausse des souscriptions d'assurance-maladie en excédent de pertes enregistrées aux Garanties collectives, reflétant la rigueur de la fixation des prix, les taux de clôture élevés et les conditions de marché favorables.La hausse des souscriptions de garanties de frais dentaires au titre des régimes commerciaux et du régime Medicare Advantage.Nous avons élargi l'accès au service Sun Life Expert Cancer Review afin que les participants de régime ayant présenté une demande de règlement pour une invalidité liée à un cancer ou pour une maladie grave obtiennent du soutien plus rapidement après leur diagnostic. Quand ces demandes de règlement sont présentées, les participants admissibles ont accès au service Expert Cancer Review par l'entremise de l'assurance-maladie en excédent de pertes Sun Life de leur employeur. Ce service offre un deuxième avis médical pour les diagnostics de cancer, aidant les participants à recevoir le plan de traitement le mieux adapté à leurs besoins.En ce qui concerne les garanties de frais dentaires, nous avons lancé Kid Smile Complete, une nouvelle solution que les employeurs peuvent offrir à leurs employés. Elle est conçue pour faciliter l'accès aux soins dentaires préventifs pour les enfants en éliminant les obstacles financiers. Pour les personnes à charge de moins de 13 ans, Kid Smile Complete offre une couverture complète sans franchise dans le réseau qui comprend les soins préventifs, les soins de base et les soins majeurs. En éliminant les frais à la charge des participants pour les soins préventifs, le programme encourage une plus grande utilisation des garanties dans le but d'améliorer la santé buccodentaire et la santé à long terme des familles.Asie : Leader régional axé sur les marchés en croissance rapideLe bénéfice net sous-jacent en Asie s'est établi à 216 M$, en hausse de 31 M$, ou 17 %, par rapport à l'exercice précédent, en raison des facteurs suivants :Un essor solide des souscriptions et la croissance des affaires en vigueur à Hong Kong.La diminution des charges et les résultats nets favorables des activités de placement. Ces éléments ont été partiellement contrebalancés par ce qui suit :La baisse des produits tirés des honoraires liée à la transition des activités de gestion administrative vers la plateforme centralisée eMPF à Hong Kong.Le bénéfice net déclaré s'est établi à 183 M$, en hausse de 29 M$, ou 19 %, par rapport à l'exercice précédent, en raison de l'augmentation du bénéfice net sous-jacent, partiellement contrebalancée par l'incidence défavorable des marchés. L'incidence des marchés est principalement attribuable à l'incidence défavorable des taux d'intérêt, partiellement contrebalancée par l'amélioration de l'incidence des marchés des actions.L'incidence du change a donné lieu à une diminution de 11 M$ du bénéfice net sous-jacent et à une diminution de 10 M$ du bénéfice net déclaré.Souscriptions en Asie18) :Les souscriptions d'assurance individuelle se sont chiffrées à 1 G$, en hausse de 41 %, reflétant l'augmentation des souscriptions pour l'ensemble des canaux à Hong Kong et une dynamique positive en ce qui concerne nos coentreprises et nos activités sur le marché de la clientèle fortunée.Les flux bruts de gestion d'actifs et souscriptions de produits de gestion de patrimoine se sont chiffrés à 1 G$, en hausse de 26 %, reflétant la hausse des souscriptions de fonds de prévoyance obligatoires à Hong Kong et la hausse des souscriptions de fonds collectifs en Inde.La MSC liée aux affaires nouvelles s'est établie à 320 M$ au premier trimestre de 2026, en hausse par rapport à 273 M$ à l'exercice précédent, en raison de la hausse des souscriptions, partiellement contrebalancée par un environnement de plus en plus concurrentiel, surtout à Hong Kong.Nous avons lancé de nouveaux produits dans l'ensemble de nos marchés pour mieux répondre aux besoins de nos Clients. En Indonésie et en Malaisie, afin d'élargir l'accès à l'assurance, nous avons lancé des solutions abordables mettant l'accent sur les risques et les questions financières que les Clients priorisent aujourd'hui. En Indonésie, le produit SHIFA21) Essential est le premier de son genre sur le marché. Il s'agit d'une solution abordable conçue pour les Clients pour qui une couverture de frais médicaux complète pourrait être financièrement hors de leur portée. En offrant une couverture ciblée des coûts de traitement des maladies graves, le produit aide les Clients à se protéger contre les répercussions financières d'une maladie grave, soit une étape importante vers une protection d'assurance-santé. En Malaisie, le produit Sun Save Future adopte une approche axée sur le Client similaire en offrant aux Clients un moyen simple et abordable de se constituer une épargne à long terme grâce à de petites cotisations périodiques. Cela encourage de bonnes habitudes financières et un engagement tôt à l'égard de la planification financière. À Hong Kong, nous avons lancé un nouveau produit d'assurance-vie universelle22) pour répondre aux besoins d'accumulation de patrimoine à long terme et de planification de l'héritage des Clients aisés et fortunés.Nous continuons aussi d'investir dans nos capacités numériques pour améliorer l'efficacité opérationnelle et l'expérience Client. À Hong Kong, l'intégration de la tarification numérique fondée sur les données dans notre système de point de vente a permis l'augmentation du nombre de cas faisant l'objet d'un traitement direct, accélérant ainsi l'intégration des Clients. En Malaisie, notre robot conversationnel assisté par l'IA a augmenté la capacité de service et appuie un engagement plus rapide et cohérent avec les Clients.Organisation internationaleLa perte nette sous-jacente s'est établie à 117 M$, comparativement à une perte nette sous-jacente de 94 M$ à l'exercice précédent, reflétant la hausse des coûts de financement soutenant l'acquisition des participations restantes dans les sociétés liées de Gestion SLC.La perte nette déclarée s'est établie à 130 M$, comparativement à une perte nette déclarée de 98 M$ à l'exercice précédent, en raison de la variation de la perte nette sous-jacente._____________________________1)Les termes « la Compagnie », « Sun Life », « nous », « notre » et « nos » font référence à la Financière Sun Life inc. (la « FSL inc. ») et à ses filiales, ainsi que, s'il y a lieu, à ses coentreprises et entreprises associées, collectivement. Nous gérons nos activités et présentons nos résultats financiers en fonction de cinq secteurs d'activité : Gestion d'actifs Sun Life, Canada, États-Unis, Asie et Organisation internationale.2)Ces éléments constituent des mesures financières non conformes aux Normes internationales d'information financière (les « normes IFRS »). Pour plus de précisions, se reporter à la rubrique « Mesures financières non conformes aux normes IFRS » du présent document et de notre rapport de gestion pour la période close le 31 mars 2026 (le « rapport de gestion du premier trimestre de 2026 »).3)Le bénéfice net déclaré (la perte nette déclarée) s'entend du bénéfice net (de la perte nette) attribuable aux actionnaires ordinaires déterminé conformément aux normes IFRS.4)Tous les montants présentés au titre du bénéfice par action tiennent compte de la dilution, sauf indication contraire.5)Ratio du Test de suffisance du capital des sociétés d'assurance-vie (le « TSAV »). Nos ratios du TSAV sont calculés conformément à la ligne directrice du BSIF intitulée Test de suffisance du capital des sociétés d'assurance-vie.6)Sous réserve de l'approbation du Bureau du surintendant des institutions financières (le « BSIF ») et de la Bourse de Toronto (la « TSX »).7)Exclut une charge de 165 M$ après impôt (277 M$ avant impôt) relative à l'acquisition des participations restantes dans des sociétés liées de Gestion SLC et une charge de 145 M$ après impôt (201 M$ avant impôt) reflétant le règlement proposé d'un litige au Canada. Pour plus de détails, se reporter à la section « Autres transactions » de la rubrique F, « Solidité financière », du rapport de gestion du premier trimestre de 2026. Cette mesure financière montre le bénéfice net déclaré qui isole les deux éléments précédemment présentés.8)Les « souscriptions d'assurance collective » comprennent les souscriptions à la Sun Life Santé au Canada, les souscriptions aux Garanties collectives et les souscriptions de garanties de frais dentaires aux États-Unis, et les activités d'assurance collective en Asie.9)Les « souscriptions d'assurance individuelle » comprennent les souscriptions à l'Assurance individuelle au Canada ainsi que les souscriptions provenant des activités d'assurance individuelle à l'ANASE, à Hong Kong, des coentreprises et auprès de la clientèle fortunée en Asie.10)Les montants présentés pour les périodes précédentes ont été mis à jour.11)La Sun Life du Canada, compagnie d'assurance-vie (la « Sun Life du Canada ») est la principale filiale d'assurance-vie active de la FSL inc.12)Le calcul du ratio de levier financier inclut le solde de la MSC (déduction faite de l'impôt) dans le dénominateur. La MSC (déduction faite de l'impôt) se chiffrait à 11,4 G$ au 31 mars 2026 (31 mars 2025 - 10,5 G$).13)Non significatif.14)Se reporter à la rubrique C, « Rentabilité », du rapport de gestion du premier trimestre de 2026 pour plus de renseignements sur des éléments importants attribuables aux éléments du bénéfice net déclaré et du bénéfice net sous-jacent et à la rubrique « Mesures financières non conformes aux normes IFRS » du présent document pour un rapprochement entre le bénéfice net déclaré et le bénéfice net sous-jacent.15)Pour plus de détails, se reporter à la section « Autres transactions » de la rubrique F, « Solidité financière », du rapport de gestion du premier trimestre de 2026.16)MFS Investment Management (la « MFS »).17)Les résultats liés aux placements immobiliers reflètent l'écart entre la valeur réelle des placements immobiliers et les rendements à long terme couvrant les passifs relatifs aux contrats d'assurance prévus par la direction (les « résultats liés aux placements immobiliers »).18)Par rapport à l'exercice précédent.19)Avec prise d'effet au premier trimestre de 2026, nous présentons notre division Régimes collectifs de retraite sous « Gestion de patrimoine - Groupe ».20)L'actif géré et administré est une mesure financière non conforme aux normes IFRS qui consiste à regrouper l'actif géré et l'actif administré. Pour plus de précisions, se reporter à la rubrique « Mesures financières non conformes aux normes IFRS » du présent document et du rapport de gestion du premier trimestre de 2026.21)Salam Healthier Future Assurance (« SHIFA ») Essential.22)SunRise Universal Life Insurance II (huit paiements).Conférence téléphonique portant sur les résultatsLes résultats financiers de la Compagnie pour le premier trimestre de 2026 seront présentés lors de la conférence téléphonique qui aura lieu le jeudi 7 mai 2026, à 11 h, heure de l'Est. Pour accéder à la webémission ou à la conférence téléphonique, rendez-vous au

www.sunlife.com/RapportsTrimestriels 10 minutes avant l'heure prévue. Nous encourageons les gens qui participent à la conférence en mode écoute seulement à se connecter à la webémission. La webémission et la présentation seront par la suite archivées sur le site Web de la Compagnie et accessibles à l'adresse www.sunlife.com jusqu'à la clôture du premier trimestre de 2027.L'information contenue dans le présent document est fondée sur les résultats financiers intermédiaires non audités de la FSL inc. pour la période close le 31 mars 2026, et elle devrait être lue parallèlement au rapport de gestion intermédiaire et à nos états financiers consolidés intermédiaires non audités et aux notes annexes (les « états financiers consolidés intermédiaires ») pour la période close le 31 mars 2026, préparés conformément aux Normes internationales d'information financière (les « normes IFRS »). Des renseignements supplémentaires sur la FSL inc. sont disponibles à l'adresse www.sunlife.com sous la rubrique « Investisseurs - Résultats et rapports financiers », sur le site de SEDAR+, à l'adresse www.sedarplus.ca, et sur le site de la Securities and Exchange Commission des États-Unis, à l'adresse www.sec.gov. À moins d'indication contraire, tous les montants sont en dollars canadiens. Les montants indiqués dans le présent document pourraient être arrondis. Pour plus de renseignements sur la façon dont nous présentons nos résultats, se reporter à la rubrique A, « Mode de présentation de nos résultats », du rapport de gestion du premier trimestre de 2026.Renseignements pour les médias :Renseignements pour les investisseurs :medias.quebec@sunlife.comrelations.investisseurs@sunlife.comMesures financières non conformes aux normes IFRSNous présentons certaines informations financières en ayant recours à des mesures financières non conformes aux normes IFRS, étant donné que nous estimons que ces mesures fournissent des informations pouvant aider les investisseurs à comprendre notre rendement et à comparer nos résultats trimestriels et annuels d'une période à l'autre. Ces mesures financières non conformes aux normes IFRS ne font pas l'objet d'une définition normalisée et peuvent ne pas être comparables à des mesures semblables utilisées par d'autres sociétés. Pour certaines mesures financières non conformes aux normes IFRS, il n'y a aucun montant calculé selon les normes IFRS qui soit directement comparable. Ces mesures financières non conformes aux normes IFRS ne doivent pas être considérées de manière isolée ou comme une solution de rechange aux mesures de performance financière établies conformément aux normes IFRS. Des renseignements supplémentaires concernant les mesures financières non conformes aux normes IFRS, ainsi que des rapprochements avec les mesures conformes aux normes IFRS les plus proches, le cas échéant, sont disponibles à la rubrique N, « Mesures financières non conformes aux normes IFRS », du rapport de gestion du premier trimestre de 2026 et dans les dossiers de renseignements financiers supplémentaires disponibles à la section « Investisseurs - Résultats et rapports financiers » à l'adresse www.sunlife.com.1. Bénéfice net sous-jacent et bénéfice par action sous-jacent

Le bénéfice net sous-jacent est une mesure financière non conforme aux normes IFRS qui aide à comprendre le rendement des activités de la Sun Life en apportant certains ajustements au bénéfice calculé en vertu des IFRS. Le bénéfice net sous-jacent, de même que le bénéfice net attribuable aux actionnaires ordinaires (le bénéfice net déclaré), servent de base à la planification de la gestion et constituent également une mesure clé de nos programmes de rémunération incitative du personnel. Cette mesure reflète le point de vue de la direction à l'égard du rendement sous-jacent des activités de la Compagnie et du potentiel de bénéfice à long terme. Par exemple, en raison de la nature à plus long terme de nos activités d'assurance individuelle, les fluctuations du marché liées aux taux d'intérêt, aux marchés des actions et aux immeubles de placement peuvent avoir une incidence importante sur le bénéfice net déclaré de la période de présentation de l'information financière. Toutefois, ces incidences ne se matérialisent pas nécessairement, et elles pourraient ne jamais se matérialiser si les marchés fluctuent dans la direction opposée au cours de périodes ultérieures ou, dans le cas des taux d'intérêt, si le placement à revenu fixe connexe est détenu jusqu'à son échéance. Le bénéfice net sous-jacent élimine l'incidence des éléments suivants du bénéfice net déclaré :L'incidence des marchés reflétant l'écart après impôt entre les fluctuations réelles et les fluctuations prévues du marché.Les modifications des hypothèses et mesures de la direction.D'autres ajustements :i) Actions de la MFS détenues par la direction;

ii) Acquisitions, intégrations et restructurations;

iii) Amortissement des immobilisations incorporelles;

iv) D'autres éléments de nature inhabituelle ou exceptionnelle.Pour plus d'information sur les ajustements retirés du bénéfice net déclaré pour arriver au bénéfice net sous-jacent, se reporter à la rubrique N, « Mesures financières non conformes aux normes IFRS - 2 - Bénéfice net sous-jacent et bénéfice par action sous-jacent », du rapport de gestion du premier trimestre de 2026.Le tableau ci-dessous présente les montants après impôt exclus de notre bénéfice net sous-jacent (perte nette sous-jacente) et de notre bénéfice par action sous-jacent, ainsi qu'un rapprochement entre ces montants et notre bénéfice net déclaré et notre bénéfice par action déclaré selon les normes IFRS.Rapprochements de certaines mesures du bénéfice netRésultats trimestriels(en millions de dollars, après impôt)T1 26T1 25Bénéfice net sous-jacent1 0501 045

Incidence des marchés

Incidence des marchés des actions(53)(48)

Incidence des taux d'intérêt1)(120)57

Incidence des variations de la juste valeur des immeubles de placement (résultats liés aux

placements immobiliers)(47)(31)

À ajouter : Incidence des marchés(220)(22)

À ajouter : Modifications des hypothèses et mesures de la direction4(4)

Autres ajustements

Actions de la MFS détenues par la direction25

Acquisitions, intégrations et restructurations2), 3), 4)(183)(54)

Amortissement des immobilisations incorporelles(43)(39)

Autres5)(145)(3)

À ajouter : Total des autres ajustements(369)(91)Bénéfice net déclaré - actionnaires ordinaires465928Bénéfice par action sous-jacent (dilué) (en dollars)1,891,82

À ajouter : Incidence des marchés (en dollars)(0,40)(0,04)

Modifications des hypothèses et mesures de la direction (en dollars)0,01(0,01)

Actions de la MFS détenues par la direction (en dollars)—0,01

Acquisitions, intégrations et restructurations (en dollars)(0,33)(0,09)

Amortissement des immobilisations incorporelles (en dollars)(0,08)(0,07)

Autres (en dollars)(0,26)(0,01)

Incidence des titres convertibles sur le bénéfice par action dilué (en dollars) 0,010,01Bénéfice par action déclaré (dilué) (en dollars)0,841,621)Nos résultats sont sensibles aux taux d'intérêt à long terme en raison de la nature de nos activités, ainsi qu'aux variations non parallèles de la courbe de rendement (par exemple, les aplatissements, les inversions, les accentuations).2)Les montants ont trait aux coûts d'acquisition relatifs à des sociétés liées de Gestion SLC, y compris la désactualisation au titre des autres passifs financiers de néant au premier trimestre de 2026 (premier trimestre de 2025 - 14 M$). Les montants du premier trimestre de 2025 comprennent la désactualisation au titre des autres passifs financiers pour BentallGreenOak, Crescent Capital Group LP et Advisors Asset Management, Inc.3)Le premier trimestre de 2026 comprend une charge de 165 M$ découlant de l'acquisition des participations restantes dans des sociétés liées de Gestion SLC. Pour plus de détails, se reporter à la section « Autres transactions » de la rubrique F, « Solidité financière », du rapport de gestion du premier trimestre de 2026.4)Comprend les coûts d'acquisition, d'intégration et de restructuration de DentaQuest, acquise le 1er juin 2022.5)Le premier trimestre de 2026 comprend une charge de 145 M$ reflétant le règlement proposé d'un litige au Canada. Pour plus de détails, se reporter à la section « Autres transactions » de la rubrique F, « Solidité financière », du rapport de gestion du premier trimestre de 2026.Le tableau suivant présente les montants avant impôt des ajustements au titre du bénéfice net sous-jacent.

Résultats trimestriels(en millions de dollars)T1 26T1 25Bénéfice net sous-jacent (après impôt)1 0501 045Ajustements au titre du bénéfice net sous-jacent (avant impôt) :

À ajouter :Incidence des marchés(247)(28)

Modifications des hypothèses et mesures de la direction1)5(5)

Autres ajustements(549)(113)

Total des ajustements au titre du bénéfice net sous-jacent (avant impôt)(791)(146)

À ajouter :Impôts liés aux ajustements au titre du bénéfice net sous-jacent20629Bénéfice net déclaré - actionnaires ordinaires (après impôt)4659281)Dans le présent document, l'incidence des modifications des hypothèses et mesures de la direction sur le bénéfice net déclaré exclut les montants attribuables aux titulaires de contrat avec participation et inclut les incidences autres que sur les passifs. À l'inverse, les états financiers consolidés intermédiaires pour la période close le 31 mars 2026 (la note 10.B.v des états financiers consolidés annuels de 2025) présentent l'incidence avant impôt des modifications des méthodes et hypothèses sur le bénéfice net, et l'incidence sur la MSC comprend les montants attribuables aux titulaires de contrat avec participation.Les impôts liés aux ajustements au titre du bénéfice net sous-jacent peuvent varier par rapport à la fourchette de taux d'imposition effectifs prévus en raison de la composition des activités de la Compagnie à l'échelle internationale ainsi que d'autres ajustements fiscaux.2. Mesures financières additionnelles non conformes aux normes IFRS

La direction utilise également les mesures financières non conformes aux normes IFRS suivantes, et une liste complète est présentée à la rubrique N, « Mesures financières non conformes aux normes IFRS », du rapport de gestion du premier trimestre de 2026.Actif géré. L'actif géré constitue une mesure financière non conforme aux normes IFRS qui indique la taille des actifs de notre Compagnie pour l'ensemble des domaines de la gestion d'actifs, de la gestion de patrimoine et de l'assurance. Il n'existe aucune mesure financière normalisée en vertu des normes IFRS. En plus des mesures conformes aux normes IFRS les plus directement comparables, soit le solde du fonds général et des fonds distincts dans nos états de la situation financière, l'actif géré comprend également les actifs de tiers et autres actifs gérés et les ajustements de consolidation. Les ajustements de consolidation sont présentés séparément, puisque les ajustements de consolidation s'appliquent à toutes les composantes du total de l'actif géré. Pour plus de renseignements sur les actifs de tiers et autres actifs gérés, se reporter aux rubriques D, « Croissance - 2 - Actif géré », et N, « Mesures financières non conformes aux normes IFRS », du rapport de gestion du premier trimestre de 2026.

Résultats trimestriels(en millions de dollars)T1 26T1 25Actif géré

Actif du fonds général232 035223 310Fonds distincts166 277149 650Actifs de tiers et autres actifs gérés1)1 258 0871 224 770Ajustements de consolidation1), 2)(81 132)(46 092)Total de l'actif géré2)1 575 2671 551 6381)Ces éléments constituent des mesures financières non conformes aux normes IFRS. Pour plus de détails, se reporter à la rubrique N, « Mesures financières non conformes aux normes IFRS », du rapport de gestion du premier trimestre de 2026.2)Les montants présentés pour les périodes précédentes ont été mis à jour.Trésorerie et autres actifs liquides. Cette mesure comprend la trésorerie, les équivalents de trésorerie, les placements à court terme et les titres négociés sur le marché, déduction faite des prêts liés aux acquisitions et des prêts à court terme détenus par la FSL inc. (la société mère ultime), et ses sociétés de portefeuille en propriété exclusive. Cette mesure constitue un des facteurs clés pris en considération à l'égard des fonds disponibles pour la réaffectation de capitaux afin de soutenir la croissance des activités.(en millions de dollars)Au 31 mars 2026Au 31 décembre 2025Trésorerie et autres actifs liquides (détenus par la FSL inc. et ses sociétés de

portefeuille en propriété exclusive) :

Trésorerie, équivalents de trésorerie et titres à court terme9301 859

Titres de créance1)396537

Titres de capitaux propres2)——Sous-total1 3262 396À déduire : Prêts liés aux acquisitions et prêts à court terme3) (détenus par la

FSL inc. et ses sociétés de portefeuille en propriété exclusive)——Trésorerie et autres actifs liquides (détenus par la FSL inc. et ses sociétés de portefeuille en propriété exclusive)1 3262 3961)Comprennent les obligations négociées sur le marché.2)Comprennent les placements dans des fonds négociés en bourse (« FNB »).3)Comprennent les prélèvements effectués sur les facilités de crédit afin de gérer le calendrier des flux de trésorerie.3. Rapprochement de certaines mesures financières non conformes aux normes IFRS

Rapprochement entre le bénéfice net sous-jacent et le bénéfice net déclaré - Données avant impôt par secteur d'activité

T1 26(en millions de dollars)Gestion d'actifs Sun LifeCanadaÉtats-UnisAsieOrganisation internationaleTotalBénéfice net sous-jacent (perte nette sous-jacente)363370218216(117)1 050

À ajouter :Incidence des marchés (avant impôt)(6)(163)(42)(25)(11)(247)

Modifications des hypothèses et mesures de la direction (avant impôt) 1——4—5

Autres ajustements (avant impôt)(281)(210)(44)(10)(4)(549)

Charge (économie) d'impôt979019(2)2206Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires17487151183(130)465

T1 25Bénéfice net sous-jacent (perte nette sous-jacente)390346218185(94)1 045

À ajouter :Incidence des marchés (avant impôt)4(24)15(19)(4)(28)

Modifications des hypothèses et mesures de la direction (avant impôt)(10)8—(3)—(5)

Autres ajustements (avant impôt)(20)(23)(60)(10)—(113)

Charge (économie) d'impôt510131—29Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires369317186154(98)928Rapprochement entre le bénéfice net sous-jacent et le bénéfice net déclaré - Données avant impôt par division - Gestion d'actifs Sun Life - en dollars américains

T1 26T4 25T1 25(en millions de dollars américains)MFSGestion SLCMFSGestion SLCMFSGestion SLCBénéfice net sous-jacent (perte nette sous-jacente)199322244218659

À ajouter :Incidence des marchés (avant impôt)—(9)—(16)—(8)

Autres ajustements (avant impôt)3(208)3(39)6(20)

Charge (économie) d'impôt(2)84(11)24(2)7Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires200(101)2161119038Rapprochement entre le bénéfice net sous-jacent et le bénéfice net déclaré - Données avant impôt par division - Gestion d'actifs Sun Life

T1 26T4 25T1 25(en millions de dollars)MFSGestion SLCMFSGestion SLCMFSGestion SLCBénéfice net sous-jacent (perte nette sous-jacente)273443125826685

À ajouter : Incidence des marchés (avant impôt) —(12)—(22)—(11)

Autres ajustements (avant impôt)5(286)5(54)9(29)

Charge (économie) d'impôt(3)115(15)34(4)10Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires275(139)3021627155Rapprochement entre le bénéfice net sous-jacent et le bénéfice net déclaré - Données avant impôt en dollars américains

T1 26T4 25T1 25(en millions de dollars américains)Gestion d'actifs Sun LifeÉtats-UnisGestion d'actifs Sun LifeÉtats-UnisGestion d'actifs Sun LifeÉtats-UnisBénéfice net sous-jacent (perte nette sous-jacente)265160304150273151

À ajouter :Incidence des marchés (avant impôt)(5)(30)(40)(19)211

Modifications des hypothèses et mesures de la

direction (avant impôt) 1——(4)(7)—

Autres ajustements (avant impôt)(205)(31)(36)(49)(14)(42)

Charge (économie) d'impôt7112151549Bénéfice net déclaré (perte nette déclarée) - actionnaires ordinaires12711124393258129Énoncés prospectifsÀ l'occasion, la Compagnie présente, verbalement ou par écrit, des énoncés prospectifs au sens de certaines lois sur les valeurs mobilières, y compris les règles d'exonération de la Private Securities Litigation Reform Act of 1995 des États-Unis et des lois canadiennes sur les valeurs mobilières applicables. Les énoncés prospectifs contenus dans le présent document comprennent i) les énoncés se rapportant à nos stratégies, nos plans, nos cibles, nos objectifs et nos priorités; ii) les énoncés se rapportant à nos initiatives de croissance et autres objectifs d'affaires; iii) les énoncés se rapportant à notre intention d'acquérir la totalité de Bell Partners, y compris le moment prévu de la clôture de la transaction; iv) les énoncés se rapportant à notre intention de renouveler notre offre publique de rachat dans le cours normal des activités; v) les énoncés se rapportant à l'incidence prévue de la nouvelle structure Gestion d'actifs Sun Life; vi) les énoncés de nature prévisionnelle, ou dont la réalisation est tributaire ou qui font mention de conditions ou d'événements futurs; et vii) les énoncés qui renferment des mots ou expressions tels que « atteindre », « viser », « ambition », « prévoir », « aspirer à », « hypothèse », « croire », « pourrait », « estimer », « s'attendre à », « but », « avoir l'intention de », « peut », « objectif », « initiatives », « perspectives », « planifier », « projeter », « chercher à », « devrait », « stratégie », « s'efforcer de », « cibler », « fera », ou d'autres expressions semblables. Entrent dans les énoncés prospectifs les possibilités et hypothèses présentées relativement à nos résultats d'exploitation futurs. Ces énoncés font état de nos attentes, estimations et prévisions actuelles en ce qui concerne les événements futurs, et non de faits passés, et ils pourraient changer.Les énoncés prospectifs ne constituent pas une garantie des résultats futurs et comportent des risques et des incertitudes dont la portée est difficile à prévoir. Les résultats et la valeur pour l'actionnaire futurs pourraient différer sensiblement de ceux qui sont présentés dans ces énoncés prospectifs en raison, entre autres, des facteurs traités aux rubriques C, « Rentabilité - 5 - Impôt sur le résultat », F, « Solidité financière », et I, « Gestion du risque », du rapport de gestion du premier trimestre de 2026 et à la rubrique « Facteurs de risque » de la notice annuelle de 2025 de la FSL inc., et des facteurs décrits à la rubrique K, « Gestion du risque », du rapport de gestion annuel de 2025 de la FSL inc. ainsi que dans ses autres documents déposés auprès des autorités canadiennes et américaines de réglementation des valeurs mobilières, que l'on peut consulter au www.sedarplus.ca et au www.sec.gov, respectivement.Les facteurs de risque importants qui pourraient faire en sorte que nos hypothèses et nos estimations, ainsi que nos attentes et nos prévisions, soient inexactes et que les résultats ou événements réels diffèrent de façon significative de ceux qui sont exprimés ou sous-entendus dans les énoncés prospectifs figurant dans le présent document sont indiqués ci-dessous. La réalisation de nos énoncés prospectifs dépend essentiellement du rendement de nos activités, qui est assujetti à de nombreux risques. Les facteurs susceptibles d'entraîner un écart significatif entre les résultats réels et les résultats escomptés comprennent notamment : les risques de marché - les risques liés au rendement des marchés des actions; à la fluctuation ou à la volatilité des taux d'intérêt, des écarts de crédit et des écarts de swap; aux placements immobiliers; aux fluctuations des taux de change et à l'inflation; les risques d'assurance - les risques liés aux résultats enregistrés au chapitre de la mortalité, aux résultats enregistrés au chapitre de la morbidité et à la longévité; aux comportements des titulaires de contrat; à la conception des produits et à la fixation des prix; à l'incidence de dépenses futures plus élevées que prévu; et à la disponibilité, au coût et à l'efficacité de la réassurance; les risques de crédit - les risques liés aux émetteurs des titres de notre portefeuille de placements, aux débiteurs, aux titres structurés, aux réassureurs, aux contreparties, à d'autres institutions financières et à d'autres entités; les risques d'entreprise et risques stratégiques - les risques liés aux conjonctures économique et géopolitique mondiales; à l'élaboration et à la mise en œuvre de stratégies d'entreprise; aux changements se produisant dans les canaux de distribution ou le comportement des Clients, y compris les risques liés aux pratiques commerciales des intermédiaires et des agents; à l'incidence de la concurrence; au rendement de nos placements et des portefeuilles de placements qui sont gérés pour les Clients, tels que les fonds distincts et les fonds communs de placement; aux changements dans les tendances en matière de placement et dans les préférences des Clients en faveur de produits différents des produits ou des stratégies de placement que nous offrons; à l'évolution des environnements juridique et réglementaire, y compris les exigences en matière de capital et les lois fiscales; aux enjeux environnementaux et sociaux, ainsi qu'aux lois et aux règlements connexes; les risques opérationnels - les risques liés aux atteintes à la sécurité informatique et à la protection des renseignements personnels et aux défaillances à ces égards, y compris les cyberattaques; à notre capacité d'attirer et de fidéliser des employés; à l'observation des exigences réglementaires et prévues par la loi et aux pratiques commerciales, y compris l'incidence des demandes de renseignements et des enquêtes liées à la réglementation; à la réalisation des fusions, des acquisitions, des investissements stratégiques et des cessions, et aux activités d'intégration qui s'y rattachent; à notre infrastructure de technologies de l'information; aux défaillances des systèmes informatiques et des technologies fonctionnant sur Internet; à la dépendance à l'égard de relations avec des tiers, y compris les contrats d'impartition; à la poursuite des affaires; aux erreurs de modélisation; à la gestion de l'information; les risques de liquidité - la possibilité que nous soyons dans l'incapacité de financer la totalité de nos engagements en matière de flux de trésorerie à mesure qu'ils arrivent à échéance; et les autres risques - les changements de normes comptables dans les territoires où nous exerçons nos activités; les risques liés à nos activités internationales, y compris nos coentreprises; aux conditions de marché ayant une incidence sur notre situation sur le plan du capital ou sur notre capacité à mobiliser des capitaux; à la révision à la baisse des notations de solidité financière ou de crédit; et aux questions d'ordre fiscal, y compris les estimations faites et le jugement exercé dans le calcul des impôts.La Compagnie ne s'engage nullement à mettre à jour ni à réviser ses énoncés prospectifs pour tenir compte d'événements ou de circonstances postérieurs à la date du présent document ou par suite d'événements imprévus, à moins que la loi ne l'exige.À propos de la Sun LifeLa Sun Life est une organisation de services financiers de premier plan à l'échelle internationale qui offre aux particuliers et aux institutions des solutions dans les domaines de la gestion d'actifs et de patrimoine, de l'assurance et de la santé. Elle exerce ses activités dans divers marchés du monde, soit au Canada, aux États-Unis, au Royaume-Uni, en Irlande, à Hong Kong, aux Philippines, au Japon, en Indonésie, en Inde, en Chine, en Australie, à Singapour, au Vietnam, en Malaisie et aux Bermudes. Au 31 mars 2026, l'actif total géré de la Sun Life s'élevait à 1,58 T$. Pour plus de renseignements, veuillez visiter le site www.sunlife.com.Les actions de la Financière Sun Life inc. sont inscrites à la Bourse de Toronto (« TSX »), à la Bourse de New York (« NYSE ») et à la Bourse des Philippines (« PSE ») sous le symbole « SLF ». SOURCE Financière Sun Life Inc. - Nouvelles financières Original: La Sun Life annonce ses résultats du premier trimestre de l'exercice 2026

US Market News

2月前

US Market News

2月前

Sun Life Reports First Quarter 2026 ResultsMay 6, 2026 5:01 PM

PR Newswire (US) Sun Life(1) delivered solid earnings in Q1, with strong growth in Asia, Canada, and U.S. Health & Risk Solutions, and an underlying return on equity of 18.6%(2).TORONTO, May 6, 2026 /PRNewswire/ - Sun Life Financial Inc.(1) (TSX: SLF) (NYSE: SLF) announced its results for the first quarter ended March 31, 2026.Underlying net income(2) of $1,050 million increased $5 million from Q1'25.Reported net income(3) of $465 million decreased $463 million or 50% from Q1'25.Underlying EPS(2)(4) of $1.89 increased 4% from Q1'25; reported EPS(4) of $0.84 decreased 48% from Q1'25.Underlying return on equity ("ROE")(2) was 18.6%; reported ROE(2) was 8.2%.Assets under management ("AUM")(2) of $1,575 billion increased $23 billion from Q1'25.SLF Inc. LICAT ratio of 143%(5).Intention to renew our normal course issuer bid to purchase up to 10 million common shares(6).Increase to common share dividend from $0.92 to $0.96 per share."This quarter we delivered strong growth in our protection businesses led by Asia, Canada and U.S. Health and Risk Solutions," said Kevin Strain, President and CEO of Sun Life. "We also added further scale to our asset management platform, deploying over $2.4 billion in capital for the buy-ups of BGO and Crescent Capital and announcing our intention to acquire Bell Partners, a leading U.S. multifamily real estate investment manager and vertically integrated property management business.""At the same time, we continued momentum in advancing our digital and AI strategic objectives, using data, automation and intelligent solutions that simplify experiences, deepen engagement and improve outcomes for our Clients around the world." Financial and Operational Highlights

Quarterly resultsProfitabilityQ1'26????Q1'25

Underlying net income ($ millions)(2)1,0501,045

Reported net income - Common shareholders - before Q1'26 notable items ($ millions)(2)(7)775928

Reported net income - Common shareholders ($ millions)465928

Underlying EPS ($)(2)(4)1.891.82

Reported EPS ($)(4)0.841.62

Underlying ROE(2)18.6 %17.7 %

Reported ROE(2)8.2 %15.7 %GrowthQ1'26?????Q1'25 ??

Asset management gross flows & wealth sales ($ millions)(2)62,36562,221

Asset management net flows & net wealth sales ($ millions)(2)(17,844)(6,154)

Group insurance sales ($ millions)(2)(8)552580

Individual insurance sales ($ millions)(2)(9)1,153874

Assets under management ("AUM") ($ billions)(2)(10)1,5751,552

New business Contractual Service Margin ("CSM") ($ millions)(2)429406Financial StrengthQ1'26?????Q1'25 ??

LICAT ratios (at period end)(5)

Sun Life Financial Inc.143 %149 %

Sun Life Assurance(11)134 %141 %

Financial leverage ratio (at period end)(2)(12)23.2 %20.1 %Financial and Operational Highlights - Quarterly Comparison (Q1'26 vs. Q1'25)($ millions)Q1'26

Sun Life Sun Life Asset