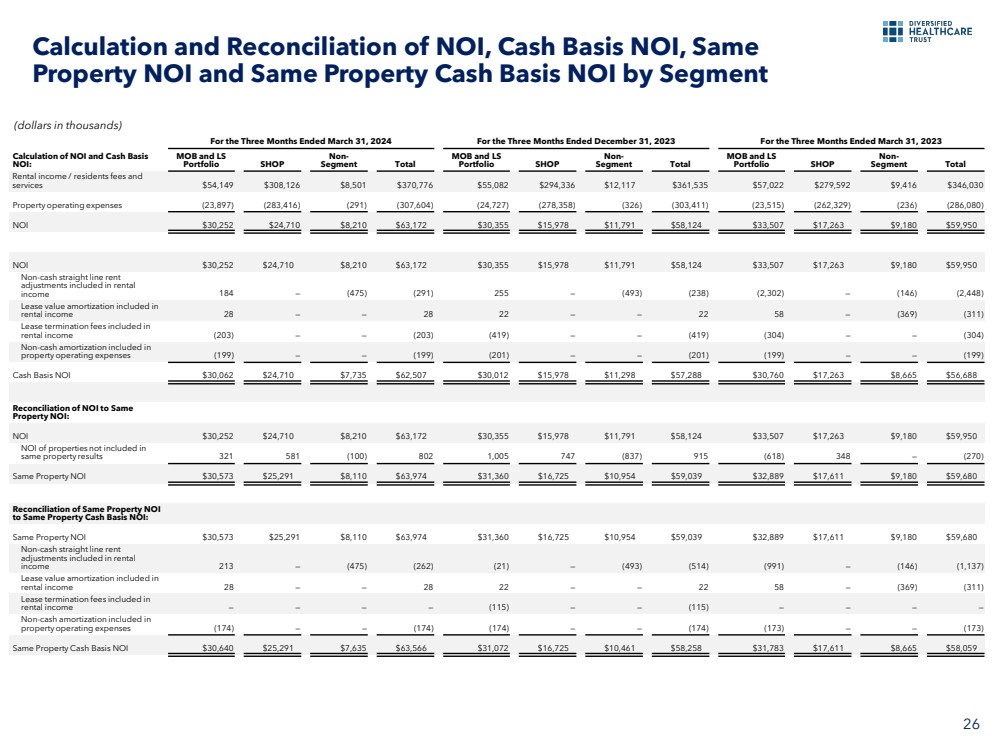

| 2626

For the Three Months Ended March 31, 2024 For the Three Months Ended December 31, 2023 For the Three Months Ended March 31, 2023

Calculation of NOI and Cash Basis

NOI:

MOB and LS

Portfolio SHOP Non-Segment Total

MOB and LS

Portfolio SHOP Non-Segment Total

MOB and LS

Portfolio SHOP Non-Segment Total

Rental income / residents fees and

services $54,149 $308,126 $8,501 $370,776 $55,082 $294,336 $12,117 $361,535 $57,022 $279,592 $9,416 $346,030

Property operating expenses (23,897) (283,416) (291) (307,604) (24,727) (278,358) (326) (303,411) (23,515) (262,329) (236) (286,080)

NOI $30,252 $24,710 $8,210 $63,172 $30,355 $15,978 $11,791 $58,124 $33,507 $17,263 $9,180 $59,950

NOI $30,252 $24,710 $8,210 $63,172 $30,355 $15,978 $11,791 $58,124 $33,507 $17,263 $9,180 $59,950

Non-cash straight line rent

adjustments included in rental

income 184 — (475) (291) 255 — (493) (238) (2,302) — (146) (2,448)

Lease value amortization included in

rental income 28 — — 28 22 — — 22 58 — (369) (311)

Lease termination fees included in

rental income (203) — — (203) (419) — — (419) (304) — — (304)

Non-cash amortization included in

property operating expenses (199) — — (199) (201) — — (201) (199) — — (199)

Cash Basis NOI $30,062 $24,710 $7,735 $62,507 $30,012 $15,978 $11,298 $57,288 $30,760 $17,263 $8,665 $56,688

Reconciliation of NOI to Same

Property NOI:

NOI $30,252 $24,710 $8,210 $63,172 $30,355 $15,978 $11,791 $58,124 $33,507 $17,263 $9,180 $59,950

NOI of properties not included in

same property results 321 581 (100) 802 1,005 747 (837) 915 (618) 348 — (270)

Same Property NOI $30,573 $25,291 $8,110 $63,974 $31,360 $16,725 $10,954 $59,039 $32,889 $17,611 $9,180 $59,680

Reconciliation of Same Property NOI

to Same Property Cash Basis NOI:

Same Property NOI $30,573 $25,291 $8,110 $63,974 $31,360 $16,725 $10,954 $59,039 $32,889 $17,611 $9,180 $59,680

Non-cash straight line rent

adjustments included in rental

income 213 — (475) (262) (21) — (493) (514) (991) — (146) (1,137)

Lease value amortization included in

rental income 28 — — 28 22 — — 22 58 — (369) (311)

Lease termination fees included in

rental income — — — — (115) — — (115) — — — —

Non-cash amortization included in

property operating expenses (174) — — (174) (174) — — (174) (173) — — (173)

Same Property Cash Basis NOI $30,640 $25,291 $7,635 $63,566 $31,072 $16,725 $10,461 $58,258 $31,783 $17,611 $8,665 $58,059

(dollars in thousands)

Calculation and Reconciliation of NOI, Cash Basis NOI, Same

Property NOI and Same Property Cash Basis NOI by Segment |