UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM 10-K/A

(Amendment No.

1)

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2022

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission

file number: 000-545793

| COSMOS GROUP HOLDINGS INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada | | 90-1177460 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization) | | Identification No.) |

37/F,

Singapore Land Tower

50

Raffles Place

Singapore 048623

(Address

of principal executive offices and zip code)

Registrant’s

telephone number, including area code: + 65 6829 7017

Securities

registered pursuant to Section 12(b) of the Act: None

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, $0.001 par value

Title

of each class

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes

☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒

No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting

company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company”

in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| | | Emerging growth company | ☐ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether

any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the

registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

No ☒

Indicate

the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| Common Stock | | Outstanding at November 30, 2023 |

| Common Stock, $0.001 par value per share | | 1,878,203,782 shares |

The aggregate market value of the 148,109,730 shares of Common Stock

of the registrant held by non-affiliates on June 30, 2022, based on the price at which the common stock sold on the last business day

of the registrant’s second quarter, is $740,548,650.

DOCUMENTS

INCORPORATED BY REFERENCE: None

EXPLANATORY NOTE

Cosmos Group Holdings Inc. is filing this

Amendment No.1 to its Annual Report on Form 10-K (this “Amendment”), to amend its Annual Report on Form 10-K for the year

ended December 31, 2022, originally filed with the Securities and Exchange Commission (the “SEC”), on April 17, 2023 (the

“Original Filing”), to amend and restate the original filing with modifications as necessary to reflect the restatements.

The following items have been amended to reflect the restatements:

Part II, Item 7, Management’s Discussion and Analysis of

Financial Condition and Results of Operations

Part II,

Item 8. Financial Statements and Supplementary Data

Part II, Item 9. Changes in and Disagreements with Accountants

on Accounting and Financial Disclosure

Part IV, Item 15. Exhibits and Financial Statement Schedules

In

addition, the Company’s Chief Executive Officer and Chief Financial Officer provided new certifications dated as of the date of

this Amendment in connection with this Amendment (Exhibits 31.1 and 32.1) hereto.

Except

as described above, this Amendment does not, and does not purport to amend, update or restate the information in any other item of the

Form 10-K or reflect any events that have occurred after the filing of the original Form 10-K.

TABLE

OF CONTENTS.

INTRODUCTORY

COMMENT

We

are a Nevada holding company with operations conducted through our wholly owned subsidiaries based in Hong Kong and Singapore. Our investors

hold shares of common stock in Cosmos Group Holdings Inc., the Nevada holding company. This structure presents unique risks as our investors

may never directly hold equity interests in our Hong Kong subsidiary and will be dependent upon contributions from our subsidiaries to

finance our cash flow needs. Our ability to obtain contributions from our subsidiaries are significantly affected by regulations promulgated

by Hong Kong and Singaporean authorities. Any change in the interpretation of existing rules and regulations or the promulgation of new

rules and regulations may materially affect our operations and or the value of our securities, including causing the value of our securities

to significantly decline or become worthless. For a detailed description of the risks facing the Company associated with our structure,

please refer to “Risk Factors – Risk Relating to Doing Business in Hong Kong.” set forth herein.

Cosmos

Group Holdings Inc. and our Hong Kong subsidiaries are not required to obtain permission from the Chinese authorities including the China

Securities Regulatory Commission, or CSRC, or Cybersecurity Administration Committee, or CAC, to operate or to issue securities to foreign

investors. However, in light of the recent statements and regulatory actions by the People’s Republic of China (“the PRC”)

government, such as those related to Hong Kong’s national security, the promulgation of regulations prohibiting foreign ownership

of Chinese companies operating in certain industries, which are constantly evolving, and anti-monopoly concerns, we may be subject to

the risks of uncertainty of any future actions of the PRC government in this regard including the risk that we inadvertently conclude

that such approvals are not required, that applicable laws, regulations or interpretations change such that we are required to obtain

approvals in the future, or that the PRC government could disallow our holding company structure, which would likely result in a material

change in our operations, including our ability to continue our existing holding company structure, carry on our current business, accept

foreign investments, and offer or continue to offer securities to our investors. These adverse actions could cause the value of our common

stock to significantly decline or become worthless. We may also be subject to penalties and sanctions imposed by the PRC regulatory agencies,

including the Chinese Securities Regulatory Commission, if we fail to comply with such rules and regulations, which would likely adversely

affect the ability of the Company’s securities to continue to trade on the Over-the-Counter Bulletin Board, which would likely

cause the value of our securities to significantly decline or become worthless.

There

may be prominent risks associated with our operations being in Hong Kong. For example, as a U.S.-listed Hong Kong public company,

we may face heightened scrutiny, criticism and negative publicity, which could result in a material change in our operations and

the value of our common stock. It could also significantly limit or completely hinder our ability to offer or continue to offer securities

to investors and cause the value of such securities to significantly decline or be worthless. Additionally, changes in Chinese internal

regulatory mandates, such as the M&A rules, Anti-Monopoly Law, and Data Security Law, may target the Company’s corporate structure

and impact our ability to conduct business in Hong Kong, accept foreign investments, or list on an U.S. or other foreign exchange. Recently,

the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance

notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed

overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding

the efforts in anti-monopoly enforcement, The business of our subsidiaries are not subject to cybersecurity review with the Cyberspace

Administration of China, or CAC, given that: (i) we do not have one million individual online users of our products and services in Hong

Kong; (ii) we do not possess a large amount of personal information in our business operations. In addition, we are not subject

to merger control review by China’s anti-monopoly enforcement agency due to the level of our revenues which provided from us and

audited by our auditor and the fact that we currently do not expect to propose or implement any acquisition of control of, or decisive

influence over, any company with revenues within China of more than Renminbi (“RMB”) 400 million. Currently, these statements

and regulatory actions have had no impact on our daily business operations, the ability to accept foreign investments and list our securities

on an U.S. or other foreign exchange. However, since these statements and regulatory actions are new, it is highly uncertain how soon

legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations

and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will

have on our daily business operation, the ability to accept foreign investments and list our securities on an U.S. or other foreign exchange.

For a detailed description of the risks facing the Company and associated with our operations in Hong Kong, please refer to “Risk

Factors – Risk Factors Relating to Doing Business in Hong Kong.” set forth herein.

The

recent joint statement by the SEC and PCAOB, and the Holding Foreign Companies Accountable Act (HFCAA) all call for additional and more

stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S.

auditors who are not inspected by the PCAOB. Trading in our securities may be prohibited under the HFCAA if the PCAOB determines that

it cannot inspect or investigate completely our auditor, and that as a result, an exchange may determine to delist our securities. On

June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act which would reduce the number of consecutive

non-inspection years required for triggering the prohibitions under the HFCAA from three years to two thus reducing the time before our

securities may be prohibited from trading or being delisted. On December 2, 2021, the U.S. Securities and Exchange Commission adopted

rules to implement the HFCAA. Pursuant to the HFCAA, the Public Company Accounting Oversight Board (PCAOB) issued its report notifying

the Commission that it is unable to inspect or investigate completely accounting firms headquartered in mainland China or Hong Kong due

to positions taken by authorities in mainland China and Hong Kong. Our auditor is based in Nigeria and is subject to PCAOB inspection.

It is not subject to the determinations announced by the PCAOB on December 16, 2021. However, in the event the Nigerian authorities subsequently

take a position disallowing the PCAOB to inspect our auditor, then we would need to change our auditor to avoid having our securities

delisted. On August 26, 2022, the China Securities Regulatory Commission, or CSRC, the Ministry of Finance of the PRC, and the PCAOB

signed a Statement of Protocol, or the Protocol, governing inspections and investigations of audit firms based in China and Hong Kong.

Pursuant to the Protocol, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and

has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB determined that the PCAOB was able to

secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and

voted to vacate its previous determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate

the PCAOB’s access in the future, the PCAOB will consider the need to issue a new determination. Notwithstanding the foregoing,

in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, then such lack of inspection

could cause our securities to be delisted from the stock exchange. On June 22, 2021, the U.S. Senate passed the Accelerating Holding

Foreign Companies Accountable Act and on December 29, 2022, the Consolidated Appropriations Act was signed into law by President Biden,

which contained, among other things, an identical provision to Accelerating Holding Foreign Companies Accountable Act and amended the

Holding Foreign Companies Accountable Act by requiring the SEC to prohibit an issuer’s securities from trading on any U.S. stock

exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three, thus reducing the time before

our Ordinary Shares may be prohibited from trading or delisted. The delisting of our Ordinary Shares, or the threat of their being delisted,

may materially and adversely affect the value of your investment. The SEC is assessing how to implement other requirements of the HFCAA,

including the listing and trading prohibition requirements described above. Future developments in respect of increasing U.S. regulatory

access to audit information are uncertain, as the legislative developments are subject to the legislative process and the regulatory

developments are subject to the rule-making process and other administrative procedures. While we understand that there has been dialogue

among the CSRC, the SEC and the PCAOB regarding the inspection of PCAOB-registered accounting firms in Mainland China, there can be no

assurance that we will be able to comply with requirements imposed by U.S. regulators if there is significant change to current political

arrangements between Mainland China and Hong Kong, or if any component of our auditor’s work papers become located in Mainland

China in the future. Delisting of our Ordinary Shares likely would force holders of our Ordinary Shares to sell their Ordinary Shares.

The market price of our Ordinary Shares could be adversely affected as a result of anticipated negative impacts of these executive or

legislative actions upon, regardless of whether these executive or legislative actions are implemented and regardless of our actual operating

performance.

Please see “Risk Factors - The Holding Foreign Companies Accountable

Act requires the Public Company Accounting Oversight Board (PCAOB) to be permitted to inspect the issuer’s public accounting firm within

three years. This three-year period will be shortened to two years if the Accelerating Holding Foreign Companies Accountable Act is enacted.

There are uncertainties under the PRC Securities Law relating to the procedures and requisite timing for the U.S. securities regulatory

agencies to conduct investigations and collect evidence within the territory of the PRC. If the U.S. securities regulatory agencies are

unable to conduct such investigations, they may suspend or de-register our registration with the SEC and delist our securities from applicable

trading market within the US.” set forth herein.

In

addition to the foregoing risks, we face various legal and operational risks and uncertainties arising from doing business in Hong Kong

as summarized below and in “Risk Factors — Risks Relating to Doing Business in Hong Kong” set forth herein.

| |

● |

Adverse changes in economic

and political policies of the PRC government could have a material and adverse effect on overall economic growth in China and Hong

Kong, which could materially and adversely affect our business. Please see “Risk Factors - We face the risk that changes

in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in Hong Kong and

the profitability of such business.” and “Substantial uncertainties and restrictions with respect to the

political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business

that we may be able to conduct in the PRC and accordingly on the results of our operations and financial condition.”

set forth herein. |

| |

|

|

| |

● |

We

are a holding company with operations conducted through our wholly owned subsidiaries based in Hong Kong and Singapore. This structure

presents unique risks as our investors may never directly hold equity interests in our Hong Kong subsidiary and will be dependent

upon contributions from our subsidiaries to finance our cash flow needs. Any limitation on the ability of our subsidiaries to make

payments to us could have a material adverse effect on our ability to conduct business. We do not anticipate paying dividends in

the foreseeable future; you should not buy our stock if you expect dividends. Please see “Risk Factors - Because our

holding company structure creates restrictions on the payment of dividends, our ability to pay dividends is limited. |

| |

|

|

| |

● |

PRC

regulation of loans to and direct investments in PRC entities by offshore holding companies may delay or prevent us from using the proceeds

of this offering to make loans or additional capital contributions to our operating subsidiaries in Hong Kong. Substantial uncertainties

exist with respect to the interpretation of the PRC Foreign Investment Law and how it may impact the viability of our current corporate

structure, corporate governance and business operations. Please see ‘Risk Factors - PRC regulation of loans to and direct investment

in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the

proceeds we receive from offshore financing activities to make loans to or make additional capital contributions to our Hong Kong subsidiaries,

which could materially and adversely affect our liquidity and our ability to fund and expand business.” set forth herein. |

| |

|

|

| |

● |

In

light of China’s extension of its authority into Hong Kong, the Chinese government can change Hong Kong’s rules and regulations

at any time with little to no advance notice, and can intervene and influence our operations and business activities in Hong Kong.

We are currently not required to obtain approval from Chinese authorities to list on U.S. exchanges. However, if our subsidiaries

or the holding company were required to obtain approval in the future, or we erroneously conclude that approvals were not required,

or we were denied permission from Chinese authorities to operate or to list on U.S. exchanges, we will not be able to continue listing

on a U.S. exchange and the value of our common stock would likely significantly decline or become worthless, which would materially

affect the interest of the investors. There is a risk that the Chinese government may intervene or influence our operations at any

time, or may exert more control over offerings conducted overseas and/or foreign investment in Hong Kong-based issuers, which could

result in a material change in our operations and/or the value of our securities. Further, any actions by the Chinese government

to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers would

likely significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value

of such securities to significantly decline or be worthless. Please see “Risk Factors - We face the risk that changes

in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the Hong Kong

and the profitability of such business.” and “Substantial uncertainties and restrictions with respect to

the political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business

that we may be able to conduct in Hong Kong and accordingly on the results of our operations and financial condition.”

and “The Chinese government exerts substantial influence over the manner in which we must conduct our business activities.

We are currently not required to obtain approval from Chinese authorities to list on U.S. exchanges. However, to the extent that

the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers over

time and if our PRC subsidiaries or the holding company were required to obtain approval in the future and were denied permission

from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our

common stock may significantly decline or become worthless, which would materially affect the interest of the investors.” set

forth herein. |

| |

● |

Governmental

control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment. |

| |

|

|

| |

● |

We

may become subject to a variety of laws and regulations in the PRC regarding privacy, data security, cybersecurity, and data protection.

We may be liable for improper use or appropriation of personal information provided by our customers. Please see “Risk

Factors - The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We

are currently not required to obtain approval from Chinese authorities to list on U.S exchanges. However, to the extent that the

Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers over time

and if our PRC subsidiaries or the holding company were required to obtain approval in the future and were denied permission from

Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our common

stock may significantly decline or become worthless, which would materially affect the interest of the investors.”

set forth herein. |

| |

|

|

| |

● |

Under

the Enterprise Income Tax Law of the PRC (“EIT Law”), we may be classified as a “Resident Enterprise” of

China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders. Please see “Risk

Factors - Our global income may be subject to PRC taxes under the PRC Enterprise Income Tax Law, which could have a material adverse

effect on our results of operations.” set forth herein. |

| |

|

|

| |

● |

Failure

to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our

PRC resident Shareholders to personal liability, may limit our ability to acquire Hong Kong and PRC companies or to inject capital

into our Hong Kong subsidiary, may limit the ability of our Hong Kong subsidiaries to distribute profits to us or may otherwise materially

and adversely affect us. |

| |

|

|

| |

● |

The

recent joint statement by the SEC and PCAOB, and the HFCAA all call for additional and more stringent criteria to be applied to emerging

market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the

PCAOB. Trading in our securities may be prohibited under the HFCAA if the PCAOB determines that it cannot inspect or investigate

completely our auditor, and that as a result an exchange may determine to delist our securities. On June 22, 2021, the U.S. Senate

passed the Accelerating Holding Foreign Companies Accountable Act which would reduce the number of consecutive non-inspection years

required for triggering the prohibitions under the HFCAA from three years to two thus reducing the time before our securities may

be prohibited from trading or being delisted. On December 2, 2021, the U.S. Securities and Exchange Commission adopted rules to implement

the HFCAA. Pursuant to the HFCAA, the Public Company Accounting Oversight Board (PCAOB) issued its report notifying the Commission

that it is unable to inspect or investigate completely accounting firms headquartered in mainland China or Hong Kong due to positions

taken by authorities in mainland China and Hong Kong. Our auditor is not subject to the determinations announced by the PCAOB

on December 16, 2021. However, in the event the Nigerian authorities subsequently take a position disallowing the PCAOB to inspect

our auditor, then we would need to change our auditor to avoid having our securities delisted. Please see “Risk Factors

- The Holding Foreign Companies Accountable Act requires the Public Company Accounting Oversight Board (PCAOB) to be permitted to

inspect the issuer’s public accounting firm within three years. This three-year period will be shortened to two years if the

Accelerating Holding Foreign Companies Accountable Act is enacted. There are uncertainties under the PRC Securities Law relating

to the procedures and requisite timing for the U.S. securities regulatory agencies to conduct investigations and collect evidence

within the territory of the PRC. If the U.S. securities regulatory agencies are unable to conduct such investigations, they may suspend

or de-register our registration with the SEC and delist our securities from applicable trading market within the US.”

set forth herein. |

| |

● |

You

may be subject to PRC income tax on dividends from us or on any gain realized on the transfer of shares of our common stock. Please

see “Risk Factors - Dividends payable to our foreign investors and gains on the sale of our shares of common stock by

our foreign investors may become subject to tax by the PRC.” set forth herein. |

| |

|

|

| |

● |

We

face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies.

Please see “Risk Factors - We and our shareholders face uncertainties with respect to indirect transfers of equity interests

in PRC resident enterprises by their non-PRC holding companies.” set forth herein. |

| |

|

|

| |

● |

COSG

is organized under the laws of the State of Nevada as a holding company that conducts its business through a number of subsidiaries

organized under the laws of foreign jurisdictions such as Hong Kong, Singapore and the British Virgin Islands. This may have an

adverse impact on the ability of U.S. investors to enforce a judgment obtained in U.S. Courts against these entities, bring actions

in Hong Kong against us or our management or to effect service of process on the officers and directors managing the foreign

subsidiaries. Please see “Risk Factors - It may be difficult for stockholders to enforce any judgment obtained in the

United States against us, which may limit the remedies otherwise available to our stockholders.” set forth

herein. |

| |

|

|

| |

● |

U.S.

regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China. |

| |

|

|

| |

● |

There

are significant uncertainties under the EIT Law relating to the withholding tax liabilities of our PRC subsidiary, and dividends

payable by our PRC subsidiary to our offshore subsidiaries may not qualify to enjoy certain treaty benefits. Please see “Risk

Factors - Our global income may be subject to PRC taxes under the PRC Enterprise Income Tax Law, which could have a material adverse

effect on our results of operations.” set forth herein. |

References in this report to the “Company” and “COSG,”

refer to Cosmos Group Holdings Inc., a Nevada company. References to the “Group”, “we,” “us” and “our”

refer to Cosmos Group Holdings Inc and all of its subsidiaries on a consolidated basis. Where reference to a specific entity is required,

the name of such specific entity will be referenced.

Transfers

of Cash to and from Our Subsidiaries

Cosmos

Group Holdings Inc. is a Nevada holding company with no operations of its own. We conduct our operations in Hong Kong primarily through

our subsidiaries in Hong Kong and Singapore. We may rely on dividends to be paid by our Hong Kong and Singapore subsidiaries to fund

our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders,

to service any debt we may incur and to pay our operating expenses. In order for us to pay dividends to our shareholders, we will

rely on payments made from our Hong Kong and Singapore subsidiaries to Cosmos Group Holdings Inc. To date, our subsidiaries have not

made any transfers, dividends or distributions to Cosmos Group Holdings Inc. and Cosmos Group Holdings Inc. has not made any transfers,

dividends or distributions to our subsidiaries or to U.S. investors.

We

do not intend to make dividends or distributions to investors of Cosmos Group Holdings Inc. in the foreseeable future.

We

currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not

anticipate declaring or paying any dividends in the foreseeable future. Any future determination related to our dividend policy will

be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements,

contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions

contained in any future financing instruments.

Cosmos

Group Holdings Inc. (Nevada corporation)

Subject

to the Nevada Revised Statutes and our bylaws, our board of directors may authorize and declare a dividend to shareholders at such time

and of such an amount as they think fit if they are satisfied, on reasonable grounds, that immediately following the dividend the value

of our assets will exceed our liabilities and we will be able to pay our debts as they become due. There is no further Nevada statutory

restriction on the amount of funds which may be distributed by us by dividend. Accordingly, Cosmos Group Holdings Inc. is permitted

under the Nevada laws to provide funding to our subsidiaries in Singapore and Hong Kong through loans or capital contributions without

restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval and filing requirements.

Singapore

and Hong Kong Subsidiaries

Our

Hong Kong subsidiaries and our Singapore subsidiary are also permitted under the laws of Hong Kong and Singapore to provide funding to

Cosmos Group Holdings Inc. through dividend distribution without restrictions on the amount of the funds. If our Hong Kong and Singapore

subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends

or make other distributions to us. To date, our subsidiaries have not made any transfers, dividends or distributions to Cosmos Group

Holdings Inc. and Cosmos Group Holdings Inc. has not made any transfers, dividends or distributions to our subsidiaries.

Under

the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends

paid by us. The laws and regulations of the PRC do not currently have any material impact on transfer of cash from Cosmos Group Holdings

Inc. to our Hong Kong subsidiaries or from our Hong Kong subsidiaries to Cosmos Group Holdings Inc. There are no restrictions or limitation

under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong

Kong or across borders and to U.S investors.

PRC

Laws

Current

PRC regulations permit PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined

in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside

at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered

capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare

fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory

reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings

of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the

date of this report, we do not have any PRC subsidiaries.

The

PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC.

Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency

for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future,

the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are

unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock.

Cash

dividends, if any, on our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes,

any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding

tax at a rate of up to 10.0%.

If

in the future we have PRC subsidiaries, certain payments from such PRC subsidiaries to Hong Kong subsidiaries will be subject to PRC

taxes, including business taxes and VAT. As of the date of this report, we do not have any PRC subsidiaries and our Hong Kong subsidiaries

have not made any transfers, dividends or distributions nor do we expect to make such transfers, dividends or distributions in the foreseeable

future.

Pursuant

to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax

Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident

enterprise owns no less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements

must be satisfied, including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends;

and (b) the Hong Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding

its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority

to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case

basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and

enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC

subsidiary to its immediate holding company. As of the date of this report, we do not have a PRC subsidiary. In the event that we acquire

or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our

Hong Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In such event,

we plan to inform the investors through SEC filings, such as a current report on Form 8-K, prior to such actions. See “Risk

Factors – Risk Factors Relating to Doing Business in Hong Kong.” set forth herein.

CAUTIONARY

NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This

Annual Report on Form 10-K includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of

1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended that are not historical facts, and involve risks

and uncertainties that could cause actual results to differ materially from those expected and projected. All statements, other than

statements of historical facts, included in this Form 10-K including, without limitation, statements in the “Market Overview”

and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s

market projections, financial position, business strategy and the plans and objectives of management for future operations, events or

developments which the Company expects or anticipates will or may occur in the future, including such things as future capital expenditures

(including the amount and nature thereof); expansion and growth of the Company’s business and operations; and other such matters are

forward-looking statements. These statements are based on certain assumptions and analyses made by the Company in light of its experience

and its perception of historical trends, current conditions and expected future developments, as well as other factors it believes are

appropriate under the circumstances. However, whether actual results or developments will conform with the Company’s expectations and

predictions is subject to a number of risks and uncertainties, including general economic, market and business conditions; the business

opportunities (or lack thereof) that may be presented to and pursued by the Company; changes in laws or regulation; and other factors,

most of which are beyond the control of the Company.

These

forward-looking statements can be identified by the use of predictive, future-tense or forward-looking terminology, such as “believes,”

“anticipates,” “expects,” “estimates,” “plans,” “may,” “will,” or similar

terms. These statements appear in a number of places in this filing and include statements regarding the intent, belief or current expectations

of the Company, and its directors or its officers with respect to, among other things: (i) trends affecting the Company’s financial condition

or results of operations for its limited history; (ii) the Company’s business and growth strategies; and, (iii) the Company’s financing

plans. Investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve significant

risks and uncertainties, and that actual results may differ materially from those projected in the forward-looking statements as a result

of various factors. Such factors that could adversely affect actual results and performance include, but are not limited to, the Company’s

limited operating history, potential fluctuations in quarterly operating results and expenses, government regulation, technological change

and competition. For information identifying important factors that could cause actual results to differ materially from those anticipated

in the forward-looking statements, please refer to the Risk Factors section herein.

Consequently,

all of the forward-looking statements made in this Form 10-K are qualified by these cautionary statements and there can be no assurance

that the actual results or developments anticipated by the Company will be realized or, even if substantially realized, that they will

have the expected consequence to or effects on the Company or its business or operations. The Company assumes no obligations to update

any such forward-looking statements.

PART

I

ITEM

1. DESCRIPTION OF BUSINESS.

History

Cosmos Group Holdings Inc.was

incorporated in the state of Nevada on August 14, 1987, under the name Shur De Cor, Inc. and engaged in developing certain mining claims.

In April 1999, Shur De Cor merged with Interactive Marketing Technology, a New Jersey corporation that was engaged in the business of

developing and direct marketing of consumer products. As the surviving company, Shur De Cor changed its name to Interactive Marketing

Technology, Inc. Shur De Cor’s then management resigned and the management of Interactive New Jersey became the Company’s

management. The prior management of Shur De Cor retained Shur De Cor’s business and assets. After that acquisition, the Company,

through a wholly owned subsidiary, IMT’s Plumber, Inc., produced, marketed, and sold a licensed product called the Plumber’s

Secret, which was discontinued in fiscal 2001. In May 2002, the Company ceased to actively pursue its product development and marketing

business and actively sought to either acquire a third party, merge with a third party or pursue a joint venture with a third party in

order to re-enter its former business of development and direct marketing of proprietary consumer products in the United States and worldwide.

On November 17, 2004, the Company

acquired MPL, a company organized under the laws of the British Virgin Islands, and its subsidiaries in accordance with the terms of a

Share Exchange Agreement executed by the parties (the “2004 Agreement”). In connection with the acquisition, the Company issued

an aggregate of 109,623,006 shares of its common stock to Imperial International Limited, a company incorporated under the laws of the

British Virgin Islands (“Imperial”), the sole shareholder of MPL, in exchange for 100% of the issued and outstanding shares

of MPL capital stock (the “2004 Share Exchange”). Upon completion of the share exchange, MPL became the Company’s wholly

owned subsidiary and the Company’s former owner transferred control of the Company to Imperial. The Company relied on Rule 506 of

Regulation D of the Securities Act of 1933, as amended (the “Act”), in regard to the shares that the Company issued pursuant

to the 2004 Share Exchange. The Company treated this transaction as a qualified “business combination” as defined by Rule

501(d). The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D promulgated under, the Act

in issuing the Company’s securities.

We

were incorporated in the state of Nevada on August 14, 1987, under the name Shur De Cor, Inc. and engaged in developing certain mining

claims. In April 1999, Shur De Cor merged with Interactive Marketing Technology, a New Jersey corporation that was engaged in the business

of developing and direct marketing of consumer products. As the surviving company, Shur De Cor changed its name to Interactive Marketing

Technology, Inc. Shur De Cor’s then management resigned and the management of Interactive New Jersey became the Company’s management.

The prior management of Shur De Cor retained Shur De Cor’s business and assets. After that acquisition, the Company, through a

wholly owned subsidiary, IMT’s Plumber, Inc., produced, marketed, and sold a licensed product called the Plumber’s Secret, which was

discontinued in fiscal 2001. In May 2002, the Company ceased to actively pursue its product development and marketing business and actively

sought to either acquire a third party, merge with a third party or pursue a joint venture with a third party in order to re-enter its

former business of development and direct marketing of proprietary consumer products in the United States and worldwide.

On

November 17, 2004, the Company acquired MPL, a company organized under the laws of the British Virgin Islands, and its subsidiaries in

accordance with the terms of a Share Exchange Agreement executed by the parties (the “2004 Agreement”). In connection with

the acquisition, the Company issued an aggregate of 109,623,006 shares of its common stock to Imperial International Limited, a company

incorporated under the laws of the British Virgin Islands (“Imperial”), the sole shareholder of MPL, in exchange for 100%

of the issued and outstanding shares of MPL capital stock (the “2004 Share Exchange”). Upon completion of the share exchange,

MPL became the Company’s wholly owned subsidiary and the Company’s former owner transferred control of the Company to Imperial.

The Company relied on Rule 506 of Regulation D of the Securities Act of 1933, as amended (the “Act”), in regard to the shares

that we issued pursuant to the 2004 Share Exchange. The Company treated this transaction as a qualified “business combination”

as defined by Rule 501(d). The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D promulgated

under, the Act in issuing the Company’s securities.

In

connection with the 2004 Share Exchange, the Company: (i) changed its name from Interactive Marketing Technology, Inc. to China Artists

Agency, Inc.; (ii) obtained a new stock symbol, “CAAY”, and CUSIP Number, effective on December 21, 2004; (iii) increased its

authorized common stock to 200,000,000 shares; (iv) effectuated a 1 for 1.69 reverse stock split; and (v) spun off the Company’s

existing business into a separate public company, All Star Marketing, Inc., a Nevada corporation (“All Star”). All Star was

formed as a wholly owned subsidiary of the Company. The Spin-off was satisfied by means of a pro-rata share dividend to the Company’s

shareholders of record as of December 10, 2004. The purpose of the Spin-Off was to allow the subsidiary to operate as a separate public

company and raise working capital through the sale of its own equity. This allowed the Company’s management to focus on its business,

while at the same time, allowing the spun-off company to have greater exposure by trading as an independent public company. Additionally,

the shareholders and the market would then more easily identify the results and performance of the Company as a separate entity from

that of All Star. In August 2005, the Company changed its name to China Entertainment Group, Inc. and effective August 9, 2005, obtained

a new stock symbol “CGRP”, and CUSIP Number.

Effective

July 22, 2010, the Company merged with Safe and Secure TV Channel, LLC, a Delaware limited liability company (the “Merger”).

In connection with the Merger, the management of the Company resigned and was replaced by the management and principals of Safe and Secure

TV Channel, LLC. The holders of interests in Safe and Secure TV Channel, LLC exchanged their interests for approximately 50.2% of the

issued and outstanding stock of the Company. In September 2010, the Company effectuated a 9.85 for one stock split to shareholders of

record as of August 23, 2010. After the Merger, the Company became a television network and multimedia information and distribution company

focused on serving the homeland security and emergency preparedness industry.

On

February 15, 2016, the Company sold to Asia Cosmos Group Limited, a private limited liability company incorporated under the laws of

British Virgin Islands (“ACOSG”), 10,000,000 shares of its common stock at a per share price of $0.027. ACOSG’s sole

shareholder is Miky Wan. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation

S promulgated under the Act in selling the Company’s securities to ACOSG. In connection with the private placement to ACOSG, a

change of control occurred and Bryan Glass resigned from his position as President, Secretary, Treasurer and Chairman of the Company.

Miky

Wan was appointed to serve as Chief Executive Officer, Chief Operating Officer, President and Director, effective February 19, 2016.

Effective

February 26, 2016, the Company changed its name to Cosmos Group Holdings Inc. and filed a Certificate of Amendment to such effect with

the Nevada Secretary of State. The name change and the related stock symbol change to “COSG” were approved by the Financial

Industry Regulatory Authority on March 31, 2016. The Company also increased the number of its authorized common stock, par value $0.001,

from 90,000,0000 shares to 500,000,000 and its preferred stock, par value $0.001, from 10,000,000 to 30,000,000 shares.

On

January 13, 2017, the Company sold 200,000,000 shares of its common stock to ACOSG at a per share price of $0.001 per share for aggregate

consideration of US $200,000. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or

Regulation S promulgated under the Act in selling the Company’s securities to ACOSG.

Acquisition

of Lee Tat, Our Logistics Business

On

May 12, 2017, the Company acquired all of the issued and outstanding shares of Lee Tat from Mr. Koon Wing Cheung, Lee Tat’s sole

shareholder, in exchange for 219,222,938 shares of its issued and outstanding common stock. In connection with the Lee Tat acquisition,

Miky Wan resigned from her positions as Chief Executive Officer and Chief Operating Officer and Koon Wing Cheung and Yongwei Hu were

appointed to serve as our Chief Executive Officer and Chief Operating Officer, respectively, and also as directors of the Company. The

Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under

the Act in selling the Company’s securities to the shareholders of Lee Tat.

Termination

of Our Artificial Intelligence Educational Content Business

Acquisition

and Rescission of Acquisition of HKHL

On

July 19, 2019, the Company acquired 5,100 Ordinary Shares of Hong Kong Healthtech Limited, a limited company organized under the laws

of Hong Kong (“HKHL”), from Wing Lok Jonathan So pursuant to the terms of a Share Exchange Agreement (the “Share Exchange

Agreement”). Such securities represented approximately 51% of the issued and outstanding securities of HKHL. As consideration,

the Company issued 6,232,951 shares of its common stock, at a per share price of US$8.99. As a result of such acquisition, the Company

entered into the AI Education business of developing and delivering educational content.

In

connection with the Share Exchange, the Company entered into employment agreements with the following individuals in connection with

their appointment to the offices set forth next to their names:

| Tze Wai Albert Yip |

Chief Financial Officer |

| Wing Lok Jonathan So |

Chief Strategy Officer |

| Kai Chi Wong |

Chief Operating Officer |

On

December 27, 2019, the parties mutually terminated the Share Exchange Agreement and IP License Agreement. As a result, 5,100 Ordinary

Shares of HKHL were returned to Wing Lok Jonathan So and the 6,232,951 shares of our common stock issued in exchange therefor were returned

to us for cancellation. In connection with the termination, on December 30, 2019, Kai Chi Wong resigned from his position as Chief Operating

Officer of the Company. Koon Wing Cheung transferred to Kai Chi Wong 215,369 shares of Common Stock of the Company as a token of appreciation

of Mr. Wong’s contribution to the Company.

The

Company ultimately exited from the AI Education business in the first quarter of 2020. As a result,

| ● | The

Employment Agreement, dated July 19, 2019, by and between Cosmos Group Holdings Inc. and

Wing Lok Jonathan So was terminated by the parties thereto effective on March 31, 2020, and

Mr. Tze Wai Albert Yip resigned from his position as the Chief Financial Officer, effective

on 30 April 2020. |

| |

● |

Syndicate

Capital (Asia) Limited returned 1,503,185 shares of the Company’s common stock (of the 2,149,293, shares previously transferred

to Syndicate Capital (Asia) Limited from Koon Wing Cheung), with the balance of the 646,108 shares retained by Syndicate Capital

(Asia) Limited as consideration for Mr. Tze Wai Albert Yip’s contributions to the Company. |

Change

in Control

On

June 14, 2021, Asia Cosmos Group Limited, an entity controlled by our former Chief Executive Officer, and Koon Wing Cheung agreed to

sell 6,230,618 and 8,149,670 shares, respectively, of our common stock to Chan Man Chung for a total purchase price of four hundred twenty

thousand dollars (US$420,000). The common stock being sold constitutes sixty-six and seventy-seven hundredth percent (66.77%) of the

issued and outstanding shares of our common stock. The sellers relied on the exemption from registration pursuant to Section 4(2) of,

and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to Dr. Chan. The funds came

from the personal funds of Dr. Chan, and was not the result of a loan. The closing occurred June 28, 2021.

In

connection with such sale, Miky Wan, our former CEO, President and CFO resigned from her positions as a director and sole executive officer

of the Company. Concurrently therewith, Messrs. Chan Man Chung, Lee Ying Chiu Herbert and Tan Tee Soo were appointed to the Company’s

Board of Directors and Chan Man Chung was appointed to serve as the CEO, CFO and Secretary of the Company.

Acquisition

of Massive Treasure Limited and Entities

On

June 17, 2021, the Company entered into a Share Acquisition Agreement (the “Share Acquisition Agreement”), by and among the

Company, Massive Treasure Limited (“Massive Treasure”), a British Virgin Islands corporation, and the holders of ordinary

shares of Massive Treasure. Under the terms and conditions of the Share Acquisition Agreement, the Company offered to issue 1,078,269,470

shares of common stock of the Company, in consideration for all the issued and outstanding shares in Massive Treasure. Lee Ying Chiu

Herbert, our director, is the beneficial holder of 47,500 common shares, or 95%, of the issued and outstanding shares of Massive Treasure.

The Company will also issue 55,641,014 shares to complete the acquisitions of 12 business entities with Massive Treasure has signed.

As

of the date of this report, these acquisitions consummated on September 17, 2021 with 800,000,000 shares of common stock pending to be

issued to Lee Ying Chiu Herbert.

On December 15, 2022,

the Company entered into a Settlement Agreement with Lee Ying Chiu Herbert, our former director

and current controlling shareholder (“Dr. Lee”), pursuant to which the Company and Dr. Lee agreed to settle the matter of

800,000,000 shares of common stock of the Company due to Dr. Lee (the “Unissued Securities”) pursuant to the terms of that

certain Share Acquisition Agreement, dated June 17, 2021 (the “Share Acquisition Agreement”), by and among the Company, Massive

Treasure Limited (“Massive Treasure”), a British Virgin Islands corporation and holding company of numerous operating subsidiaries,

and the holders of ordinary shares of Massive Treasure. Pursuant to the terms of the Settlement Agreement, the Company and Dr. Lee agreed

to the following, among other things, as settlement in full of the Unissued Securities:

| (1) | The Company

will issue to Dr. Lee 400,000,000 shares of its common stock at a per share value of $0.001; |

| (2) | The Company shall cause

the transfer to Dr. Lee or his designees all the assets and liabilities of following entities as such assets and liabilities are described

in the financial statements of the Company as of November 30, 2022: |

| i) | Coinllectibles Limited, (BVI

company number: 2067445), a company incorporated in the British Virgin Islands, with registered address at Mandar House, 3rd Floor, Johnson’s

Ghut, Tortola, British Virgin Islands and its branch, (Singapore company registration number: T21FC0080G); |

| | | |

| ii) | Coinllectibles (HK) Limited,

(Hong Kong business registration number: 72228307), a company incorporated in Hong Kong, with registered address at 7/F, K11 Atelier Victoria

Dockside, 18 Salisbury Road, Tsim Sha Tsui, Hong Kong; and |

| | | |

| iii) | Coinllectibles Wealth

Limited, (Hong Kong business registration number: 70756483), a company incorporated in

Hong Kong, with registered address at 7/F, K11 Atelier Victoria Dockside, 18 Salisbury Road, Tsim Sha Tsui, Hong Kong. |

| (3) | The Company

and Dr. Lee agreed to the allocation of certain inventories, accounts payables, and intellectual properties. |

Acquisition

of Art Collectibles

Recent

Purchases of Collectibles and Acquisition of subsidiaries

On

July 23, 2021, the Company and Lee Ying Chiu Herbert, our director, entered into a Sale and Purchase Agreement pursuant to which the

Company agreed to purchase Fifty-Five (55) sets of art collectibles for HK$10,344,000, payable through the issuance of 180,855 shares

of common stock of the Company (the “Shares”). The sale consummated on August 13, 2021. It is our understanding that Dr.

Lee is not a U.S. Person within the meaning of Regulations S. Accordingly, the Shares were sold pursuant to the exemption provided by

Section 4(a)(2) of the Securities Act of 1933, as amended, and Regulation S promulgated thereunder.

On

October 15, 2021, Massive Treasure, a subsidiary of Cosmos Group Holdings Inc., the Company, NFT Limited (“NFT”), a British

Virgin Island limited liability company, and the shareholders of NFT (collectively, the “NFT Shareholders”) agreed to entered

into a Share Exchange Agreement Version 2021001 (the “Agreement”) which is available on the web site of http://www.coinllectibles.art,

pursuant to which Massive Treasure agreed to acquire 51% of NFT through the issuance of 2,350,229 shares of common stock of the Company

(the “Shares”). The specifics of such share exchange are further set forth in that certain Confirmation dated October 15,

2021, by and among the Shareholders, NFT, the Company and Massive Treasure (the “Confirmation”). The consummation of the

Agreement occurred upon the issuance of the Shares to the NFT Shareholders on October 22, 2021. NFT beneficially owns Talk+, a

messaging and cryptocurrency-focused mobile application which seeks to simplify the crypto usage experience by allowing users to send

crypto through instant messages to other individuals. We hope that the inclusion of Talk+ will enable us to attract more non-crypto

native users and broaden our community reach.

NFT beneficially owns Talk+, a

messaging and cryptocurrency-focused mobile application which seeks to simplify the crypto usage experience by allowing users to send

crypto through instant messages to other individuals. The app provided users with the ability to access their own cryptocurrencies that

were obtained independent of the Company by acting as a portal. However, the app did not allow for transfer of cryptocurrencies and all

cryptocurrencies accessed by the end-user remains with the end-user, and are not transferred or held by the Company at any time. We hope

that the inclusion of Talk+ will enable us to attract more non-crypto native users and broaden our community reach.

On

October 25, 2021, Coinllectibles Private Limited (“Coinllectibles”), a subsidiary of Cosmos Group Holdings Inc., and the

Company entered into two Sale and Purchase Agreements (the “Agreements”) with two artists, pursuant to which Coinllectibles

agreed to purchase collectible art items for £260,000 and US$100,000, payable through the issuance of 43,633 and 12,500 shares

of common stock of the Company respectively, at a per share price of $4.00, and £130,000 and US$50,000 in cash payable after

the respective collectible art item has been sold by Coinllectibles. The consummation of the Agreements occurs upon the issuance of the

Shares to the respective artists on October 29, 2021.

On

February 10, 2022, the Company consummated the acquisition of 80% of the issued and outstanding securities of Grand Gallery Limited, a Hong Kong

limited liability company engaged in the business of selling traditional art and collectible pieces, through the issuance of 153,060

shares of our common stock, at a valuation of $4.00 per share. We believe that this acquisition will strengthen our DOT business by expanding

our access to buyers of arts and collectibles.

Other

Activities

In

March 2022, we launched a new sports division in our MetaMall and partnering with a former NBA basketball player as president of Coinllectible

Sports. We hope to exploit our DOT technology and the metaverse to bring innovation to the sports space, bridge the intersection of our

DOT technology and Sports memorabilia to improve experiences for fans, athletes, teams, events and partners.

Our

Business

COSG is a Nevada holding company

with operations conducted through our subsidiaries based in Singapore and Hong Kong. The Company, through its subsidiaries, is engaged

in two business segments: (i) the physical arts and collectibles business, and (ii) the financing/money lending business. The Company

currently does not have any customers that are from the United States or any U.S. person nor is the Company specifically targeting customers

from the United States. However, the Company’s operation of an online market place for collectibles and fine art is accessible online

by interested parties and may potentially be accessed by users located in the United States.

The Company’s business focused

on physical artworks and collectibles, while utilizing blockchain and NFT technologies to create a documents of title and a transparent

ledger for each artwork or collectible to enhance the overall experience of each collector in order to facilitate sale transaction logistics.

Through our physical arts and collectibles business, we provide authentication, valuation and certification (“AVC”) service,

sale and purchase, hire purchase, financing, custody, security and exhibition (“CSE”) services to art and collectibles buyers

through traditional methods as well as through leveraging blockchain technology through the creation of Digital Ownership Tokens (“DOTs”).

We initially intend to focus on customers located in Hong Kong and expand throughout Asia and the rest of the world.

We

conduct our DOT operations from Singapore. In Singapore, cryptocurrencies and the custodianship of such cryptocurrencies are not specifically

regulated. Cryptocurrency exchanges and trading of cryptocurrencies are legal, but not considered legal tender. To the extent that cryptocurrencies

or tokens are considered “capital market products” such as securities, spot foreign exchange contracts, derivatives and the

like, they will be subject to the jurisdiction of the Monetary Authority of Singapore (“MAS”), Securities and Futures Act,

anti-money laundering and combating the financing of terrorism laws and requirements. To the extent that tokens are deemed “digital

payment tokens,” they will be subject to the Payment Services Act of 2019 which, among other things, require compliance with anti-money

laundering and combating the financing of terrorism laws and requirements. According to the Payment Services Act of 2019, “digital

payment token” means any digital representation of value (other than an excluded digital representation of value) that (a) is expressed

as a unit; (b) is not denominated in any currency, and is not pegged by its issuer to any currency; (c) is, or is intended to be, a medium

of exchange accepted by the public, or a section of the public, as payment for goods or services or for the discharge of a debt; (d)

can be transferred, stored or traded electronically; and (e) satisfies such other characteristics as the Authority may prescribe. Our

DOTs, therefore, are not securities or digital payment tokens subject to these acts.

We generally do not

maintain custody of the DOTs or crypto assets. Where possible, we adopt a “sell then mint” process, where the DOTs are not

minted unless they have been sold. This is in line with how legal documents are created where an Assignment is only drafted and signed

after a sale of a property (e.g., scanned copies of an Assignment can be created in PDF form thereafter). The DOT merely a digital ownership

title to a physical item. Subsequent to the transfer of Coinllectibles Limited, Coinllectibles (HK) Limited and Coinllectibles Wealth

Limited to Dr. Lee pursuant to the Settlement Agreement between the Company and Dr. Lee dated December 15, 2022, the Company no longer

minted any DOTs, and any DOTs sold by the Company as ownership documents in association with the underlying physical artwork or collectible

are obtained from a third party.

Before the DOTs are sold, we store the underlying physical art pieces in

our warehouse. We have purchased insurance that covers the art pieces stored in our warehouse. After the DOTs are sold, customers can

choose to ship out the underlying art pieces or not. If customers want to ship out the art pieces, they will have to pay for the shipping

and insurance fees.

The Company did not engage in

the business of purchasing, holding or trading crypto currencies. We receive fiat and cryptocurrency from the sale of art and collectibles

and collection of transaction fees derived from the secondary and subsequent sales of the collectibles. During the financial period

up to the transfer of Coinllectibles Limited, Coinllectibles (HK) Limited and Coinllectibles Wealth Limited to Dr. Lee pursuant to the

Settlement Agreement between the Company and Dr. Lee dated December 15, 2022, the Company accepted crypto currencies such as ETH, BNB,

USDT, BUSD, MATIC and OKT. In order to minimize the risk of price fluctuation in cryptocurrency, after we receive the cryptocurrencies

we will recognize the value by immediately exchange them into US dollar or stable currencies that are pegged with US dollar. Subsequent

to the Settlement Agreement dated December 15, 2022, the Company only accepted stable coins such as USDT, BUSD and MATIC. For crypto-payments,

in compliance with our AML Policy, we have automatically blocked off transactions from all sanctioned jurisdictions.

Meanwhile, the Company

did not offer stablecoins to its customers as a product and its business remained focused on physical artworks and collectibles. The stablecoins

were utilized to pay for the Company’s marketing and IT development expenses, including expenses associated with the minting process.

For the fiscal year ended December 31, 2022, crypto assets held by the Company was approximately 0.03% of its total assets.

Where possible, we disposed

the crypto assets as soon as we have received them. On the rare occasion that we do have custody of these assets, we keep them in an online

multi-signatory wallet in the MultiSig system we developed so that they could be listed on our platform. When these DOTs are sold, the

ownership of the DOTs is transferred to the buyer. The MultiSig system is developed internally by our Company for the purpose of holding

DOTs in a multi-signatory wallet where multiple wallet holders , instead of a single wallet holder, are needed to approve any transaction.

During the financial reporting period, there were only 6 wallet holders who had access to the multi-signatory wallet and at least 3 wallet

holders’ approvals are required to process transactions. This reduced the risk of losing DOT from the loss or destruction of a single

private key of the wallet, and the risk of DOT being stolen or destroyed by a single wallet holder.

The Company’s

Talk+ messaging app was developed to assist end-users who were not familiar with cryptocurrencies. The app provided users with the ability

to access their own cryptocurrencies that were obtained independent of the Company by acting as a portal. However, the app did not allow

for transfer of cryptocurrencies and all cryptocurrencies accessed by the end-user remains with the end-user, and are not transferred

or held by the Company at any time.

We conduct our financing/money

lending business through our Hong Kong subsidiaries which are licensed under Hong Kong’s Money Lenders Ordinance. Our Hong Kong

subsidiaries primarily provide unsecured personal loan financings to private individuals. We also have a small portfolio of mortgage loans.

Revenue is generated from interest received from the provision of loans to private individual customers.

There

may be prominent risks associated with our operations being in Hong Kong. We may be subject to the risks of uncertainty of any future

actions of the PRC government including the risk that the PRC government could disallow our holding company structure, which may result

in a material change in our operations, including our ability to continue our existing holding company structure, carry on our current

business, accept foreign investments, and offer or continue to offer securities to our investors. These adverse actions could change

the value of our common stock to significantly decline or become worthless. We may also be subject to penalties and sanctions imposed

by the PRC regulatory agencies, including the Chinese Securities Regulatory Commission, if we fail to comply with such rules and regulations,

which could adversely affect the ability of the Company’s securities to continue to trade on the Over-the-Counter Bulletin Board,

which may cause the value of our securities to significantly decline or become worthless.

As

a U.S.-listed company with operations in Hong Kong, we may face heightened scrutiny, criticism and negative publicity, which could result

in a material change in our operations and the value of our common stock. It could also significantly limit or completely hinder our

ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Additionally, changes in Chinese internal regulatory mandates, such as the M&A rules, Anti-Monopoly Law, and the soon to be effective

Data Security Law, may target the Company’s corporate structure and impact our ability to conduct business in Hong Kong, accept

foreign investments, or list on an U.S. or other foreign exchange. For a detailed description of the risks facing the Company and the

offering associated with our operations in Hong Kong, please refer to “Risk Factors – Risk Factors Relating to Our Operations

in Hong Kong” as herein.

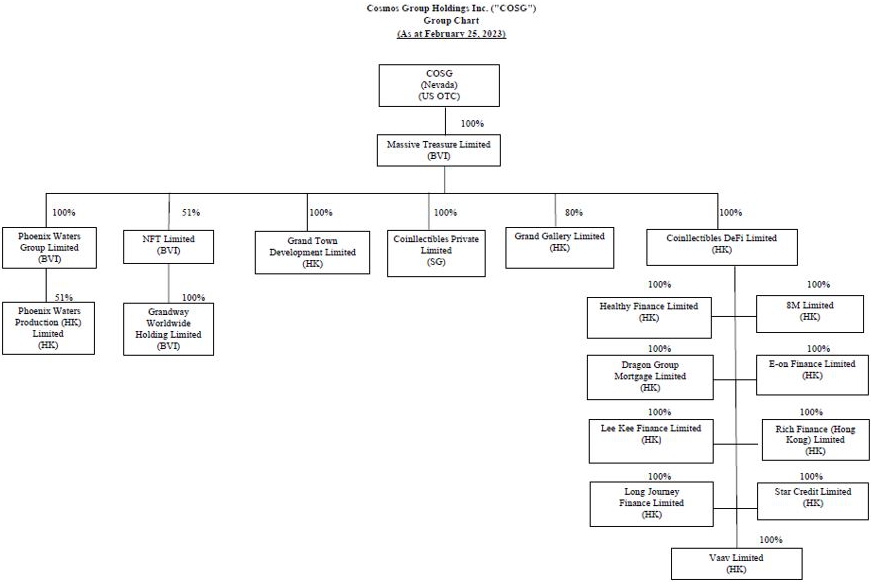

Our corporate organization

chart as at December 31, 2022 is below:

Note

1: In May 2021, Massive Treasure entered into a Share Swap Letter Agreement (the “100% Share Swap Letter”) with

the shareholders of each of E-on Finance Limited (“E-on”) and 8M Limited (“8M”) to acquire 100% of each of

E-on and 8M for 20,110,604 and 10,055,302 shares of common stock of COSG respectively based upon the closing price of the common

stock of COSG as of the date of signing of the 100% Share Swap Letter and determined in accordance with the terms of the 100% Share

Swap Letter on the date. The acquisition of E-on and 8M consummated in May 2021. Thereon, COSG issued 10,256,409 shares and

5,128,204 shares to the shareholders of E-on and 8M respectively. COSG is obligated to issue 9,854,195 and 4,927,098 shares on the

first anniversary of the closing of the acquisition to the former shareholders of E-on and 8M respectively, subject to certain

clawback provisions. E-on and 8M are obligated to meet certain financial milestones in each of the two year anniversaries following

the closing. Failure to meet such milestones will result in a clawback of the shares issued to the former shareholders. On the

second anniversary of the closing, if E-on or 8M exceeds the aggregate financial milestone set for the two years, the former

shareholders thereof shall be entitled to additional shares of COSG as determined in accordance with the 100% Share Swap

Letter.

Note

2: In May and June 2021, Massive Treasure entered into a Share Swap Letter Agreement (the “51% Share Swap

Letter”) with the shareholders of each of the entities to acquire 51% of the issued and outstanding securities of

the entities for an aggregate amount of 23,589,736 shares of COSG’s common stock as set forth below (the “First Tranche

Shares”), based upon the closing price of the common stock of COSG as of the date of signing the 51% Share Swap Letter and

determined in accordance with the terms of the 51% Share Swap Letter. The acquisition of the entities consummated in May and June

2021. Thereon, COSG issued the First Tranche Shares. On the first anniversary of the closing, COSG is obligated to issue

a second tranche of shares of its common stock, based upon the closing price of its shares as of the fifth business day prior to

such first anniversary as determined in accordance with the terms of the 51% Share Swap Letter (the “Second Tranche

Shares”). Upon the issuance of the Second Tranche Shares, each of the entities will deliver the remaining 49% of

the issued and outstanding securities to COSG to become wholly owned subsidiaries of COSG. Each of the entities are obligated to

meet certain financial milestones in each of the two year anniversaries following the closing. Failure to meet such milestones will

result in a clawback of the shares issued to the former shareholders. On the second anniversary of the closing, if any entity

exceeds the aggregate financial milestone set for the two years, the former shareholders thereof shall be entitled to additional

shares of COSG as determined in accordance with the 51% Share Swap Letter.

On December 15, 2022,

the Company entered into a Settlement Agreement with Lee Ying Chiu Herbert, our former director and current controlling shareholder (“Dr.

Lee”), pursuant to which the Company and Dr. Lee agreed to settle the matter of Unissued Securities due to Dr. Lee the Share Acquisition

Agreement, by and among the Company, Massive Treasure, and the holders of ordinary shares of Massive Treasure. Pursuant to the terms