Form 6-K - Report of foreign issuer [Rules 13a-16 and 15d-16]

2023年10月27日 - 9:31PM

Edgar (US Regulatory)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of October, 2023.

Commission File Number 001-38755

Suzano S.A.

(Exact name of registrant as specified in its charter)

SUZANO INC.

(Translation of Registrant’s Name into English)

Av. Professor Magalhaes Neto, 1,752

10th Floor, Rooms 1010 and 1011

Salvador, Brazil 41 810-012

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ⌧ Form 40-F ◻

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ◻

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ◻

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Date: October 27, 2023

| | |

| | SUZANO S.A. |

| | |

| By: | /s/ Marcelo Feriozzi Bacci |

| Name: | Marcelo Feriozzi Bacci |

| Title: | Chief Financial and Investor Relations Officer |

3

Exhibit 99.1

| Eucalyptus fiber |

| agenda

Highlights 3Q23

Business Strategy

Financial Management |

| agenda

Highlights

3Q23 |

| With a new drop, cash cost reaches a lower level

than same quarter last year

1 Excluding Consumer Goods. | 2 Operating Cash Generation = Adjusted EBITDA less Sustaining Capex. | 3 Considers Finnvera credit line. | 4 Net Debt / Adjusted EBITDA in the last twelve months. 4

2.5 million tons

(vs. 2.8 million tons 3Q22 and

2.5 million tons 2Q23)

Pulp:

272 thousand tons

(vs. 299 thousand tons 3Q22 and

263 thousand tons 2Q23)

Paper1

:

Pulp Inventory:

Below optimum

operational levels

Adjusted EBITDA:

Operating cash generation2

:

Cash cost ex-downtimes:

R$3.7 bn

(vs. R$8.6 bn 3Q22 and

R$3.9 bn 2Q23)

R$1.9 bn

(vs. R$7.2 bn 3Q22 and

R$2.2 bn 2Q23)

R$861/ton

(vs. R$883/ton 3Q22 and

R$918/ton 2Q23)

Liquidity3

:

US$11.5 bn

(vs. US$10.7 bn 3Q22 and

R$11.3 bn 2Q23)

Leverage4

:

US$6.3 bn

(vs. US$4.7 bn 3Q22

and US$6.3 bn 2Q23)

Net debt:

2.7x in US$

(vs. 2.1x in US$ 3Q22 and

2.2x in US$ 2Q23)

Operating

Performance

Sales

Volume

Financial

Management |

| agenda

Business

Strategy |

| 6

Challenges of a growing company...

CAPITAL

ALLOCATION & CULTURE |

| Source: ¹illustration based on Founder’s Mentality (Bain & Company)

Agility

Trend towards a

more complex

organization

Net benefits of size

Founder’s mentality¹ HIGH

HIGH

LOW

Focus

Purpose:

Culture drivers

It´s only good for

us if it´s good for

the world

People who inspire

and transform

Create and

share value

Renewing life inspired by trees

Processes

streamlining

&

Leadership

development

Value creation through culture development

Innovation Talent

development

7 |

| Strategic

avenues

Play a leading

role in

sustainability

Be “Best-in-Class” in the

Total Pulp

Cost vision

Maintain

relevance in

Pulp

Expand boldly

into New

Markets

Advance in the

links of the

chain, always

with competitive

advantage |

| Expand boldly

into New

Markets |

| New bio businesses development

Textile

& MFC

Lignine Carbon

& Biomas

Bio oil

& Green energy

1 Excluding Consumer Goods. | 2 Operating Cash Generation = Adjusted EBITDA less Sustaining Capex. | 3 Considers Finnvera credit line. | 4 Net Debt / Adjusted EBITDA in the last twelve months. 10 |

| TOP1

OPEN CORPS INNOVATION ON

PULP & PAPER SECTOR

TOP3

on total ranking

TOP1

BRAZILIAN

INNOVATIVE

COMPANY

MOST RECENT AWARD FROM

BRAZIL’S NATIONAL

CONFEDERATION OF

INDUSTRY (CNI)

Core

business

operations

Universities

&

R&D centers

Start-ups

&

Entrepreneurs

Innovation

Hubs

&

Accelerators

Canada

R&D

Israel

R&D

Brazil

R&D

(4 centers)

China

Innovability

Hub

Suzano Ventures accelerates new bio

businesses and core competitiveness

11 |

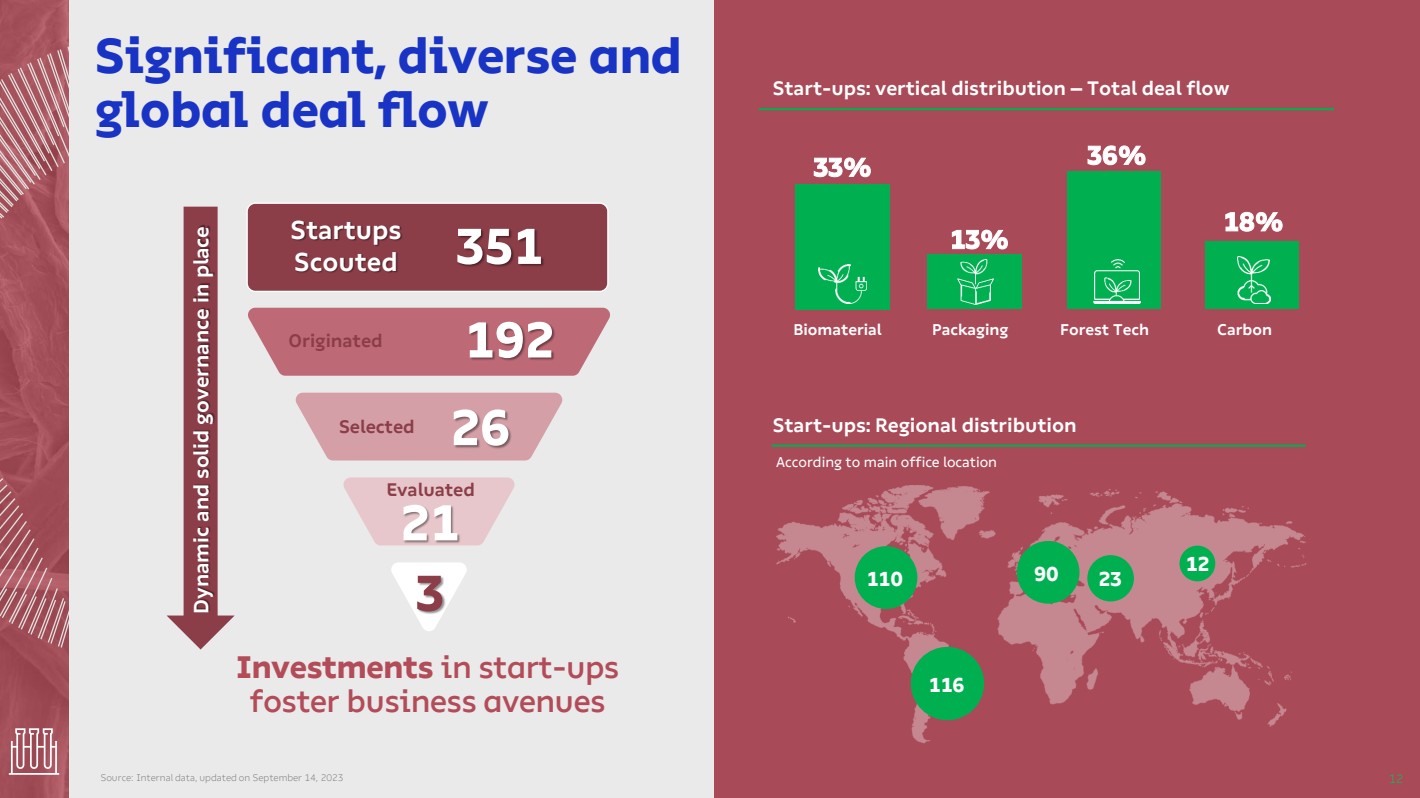

| Significant, diverse and

global deal flow

Source: Internal data, updated on September 14, 2023

Startups

Scouted 351

Investments in start-ups

foster business avenues

Start-ups: vertical distribution – Total deal flow

13%

33% 36%

18%

Biomaterial Packaging Forest Tech Carbon

According to main office location

Start-ups: Regional distribution

110

116

12 90 23

Originated 192

Selected 26

Evaluated

21

Dynamic and solid governance in place

3

12 |

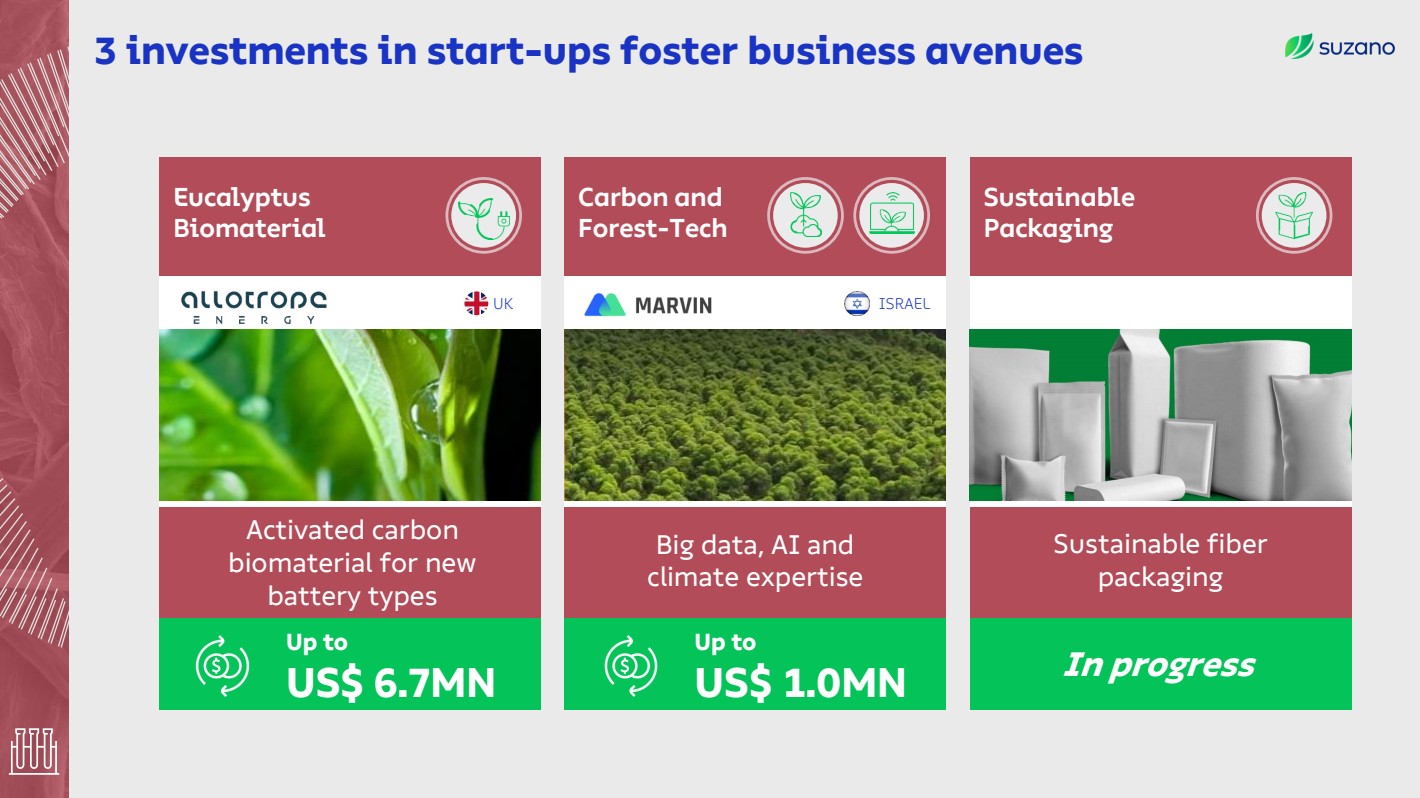

| 3 investments in start-ups foster business avenues

Eucalyptus

Biomaterial

Activated carbon

biomaterial for new

battery types

Up to

US$ 6.7MN

UK

Sustainable

Packaging

Sustainable fiber

packaging

In progress

Carbon and

Forest-Tech

Big data, AI and

climate expertise

Up to

US$ 1.0MN

ISRAEL |

| Be “Best-in-Class”

in the Total Pulp

Cost vision |

| Worldwide, in the long run, will there be enough wood?

According to FAO, consumption increased by 28% in the last three decades,

while wood resources decreased by 4%

Source: FAO (Food and Agriculture Organization) Global forest sector outlook 2050 15

Supply

perspective

Demand

perspective

Ukraine-Russia war

wood trade sanctions

Largest wood importer

but limited area for

expansion

China

Russia

British

Columbia and

US West

New pulp capacities

outpaced plantations

increase

Brazil

Chile

Wildfires

1 MM ha affected since 2017

Wildfires

500 k hectares

burnt in 2017

Indonesia

Wildfires

2.6 MM hectares burnt in 2015

Portugal

and Spain

Japan &

Korea

Increasing

biomass demand

Wildfires

~3.5 MM ha [last 5 years]

Pine beetle

58% of the pine volume

affected

• Climate change impacts

Extreme events

Wildfire

Pests & diseases

• Trade restrictions

• Restrictions to new

plantations

• Biomass for energy

• Construction

applications

• Green steel

• New pulp projects

• Textile wood fiber

growth |

| In Brazil, eucalyptus planted area has not kept up with

the growing demand for wood-based biomass

16 ¹Ibá - Brazilian Tree Industry | ²IBGE - Brazilian Institute for Geography and Statistics | ³S&P Global Average prices of farmland Reforestation, Pastureland, Grains and Sugarcane, in Real Terms | 4Pöyry/AFRY BRL Price Index Stumpage Over Bark – Real Terms.

199

2018 2019 2020 2021 2022 2023

Pulpwood average BRL market price index

eucalyptus4

(base 100 – 2018)

2018 2021

+10%

6.8

7.5

Eucalyptus planted area¹

Million ha

2018 2021

+26%

138

174

Eucalyptus consumption²

Million m³

• Increasing planting costs

• Climate uncertainty and yield

losses in some regions

• New pulp projects

• Biomass to replace natural gas

• Woodchip to grain drying

• Biomass for corn ethanol mills

Farmland Average BRL Price Index3

(Base 100 – 2018) 162

2018 2019 2020 2021 2022 2023

Rising land prices |

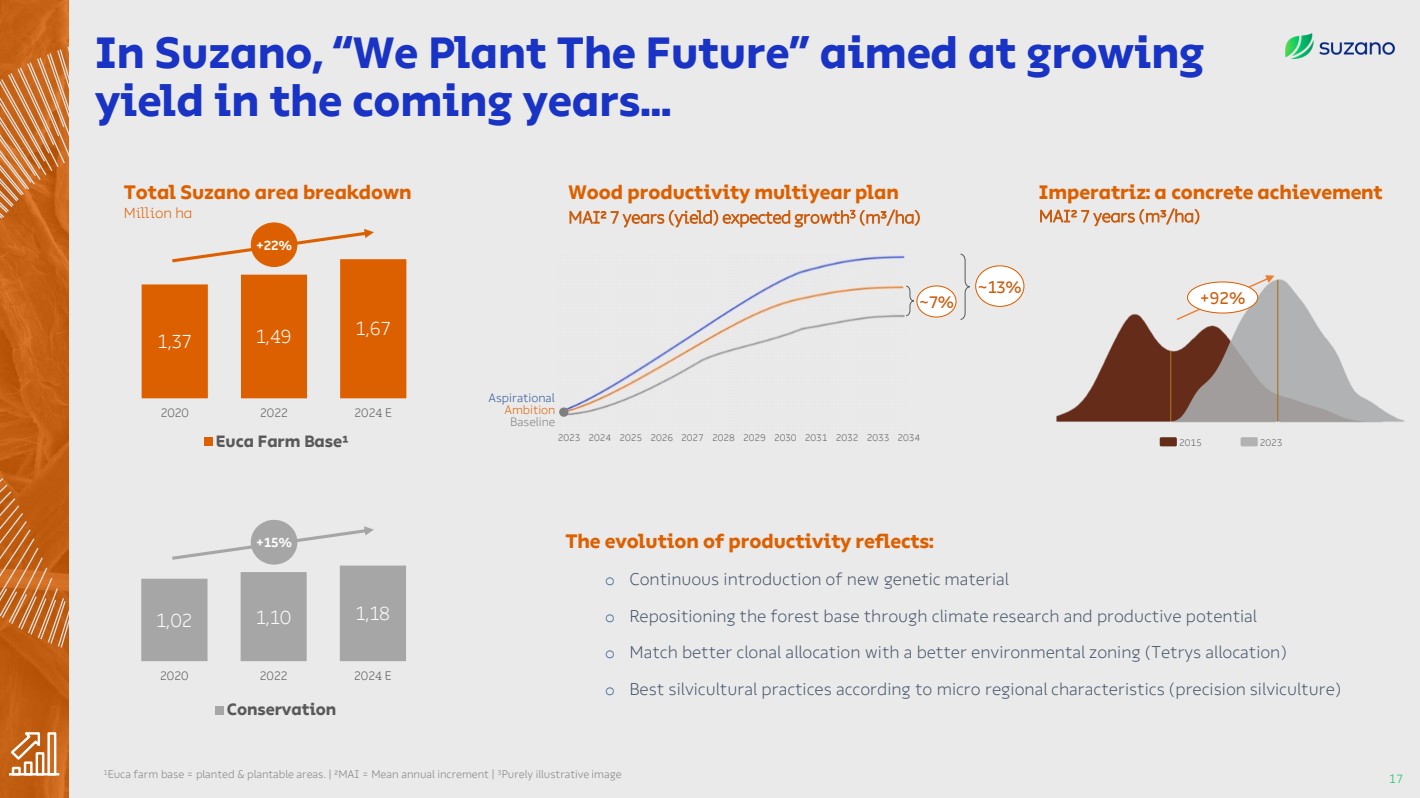

| In Suzano, “We Plant The Future” aimed at growing

yield in the coming years...

17

1Euca farm base = planted & plantable areas. | ²MAI = Mean annual increment | 3Purely illustrative image

1,02 1,10 1,18

2020 2022 2024 E

Conservation

1,37 1,49 1,67

2020 2022 2024 E

Euca Farm Base¹

Total Suzano area breakdown

Million ha

+22%

Wood productivity multiyear plan

MAI² 7 years (yield) expected growth MAI² 7 years (m³/ha) 3

(m³/ha)

~7%

~13%

2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Aspirational

Ambition

Baseline

+92%

2015 2023

Imperatriz: a concrete achievement

The evolution of productivity reflects:

o Continuous introduction of new genetic material

o Repositioning the forest base through climate research and productive potential

o Match better clonal allocation with a better environmental zoning (Tetrys allocation)

o Best silvicultural practices according to micro regional characteristics (precision silviculture)

+15% |

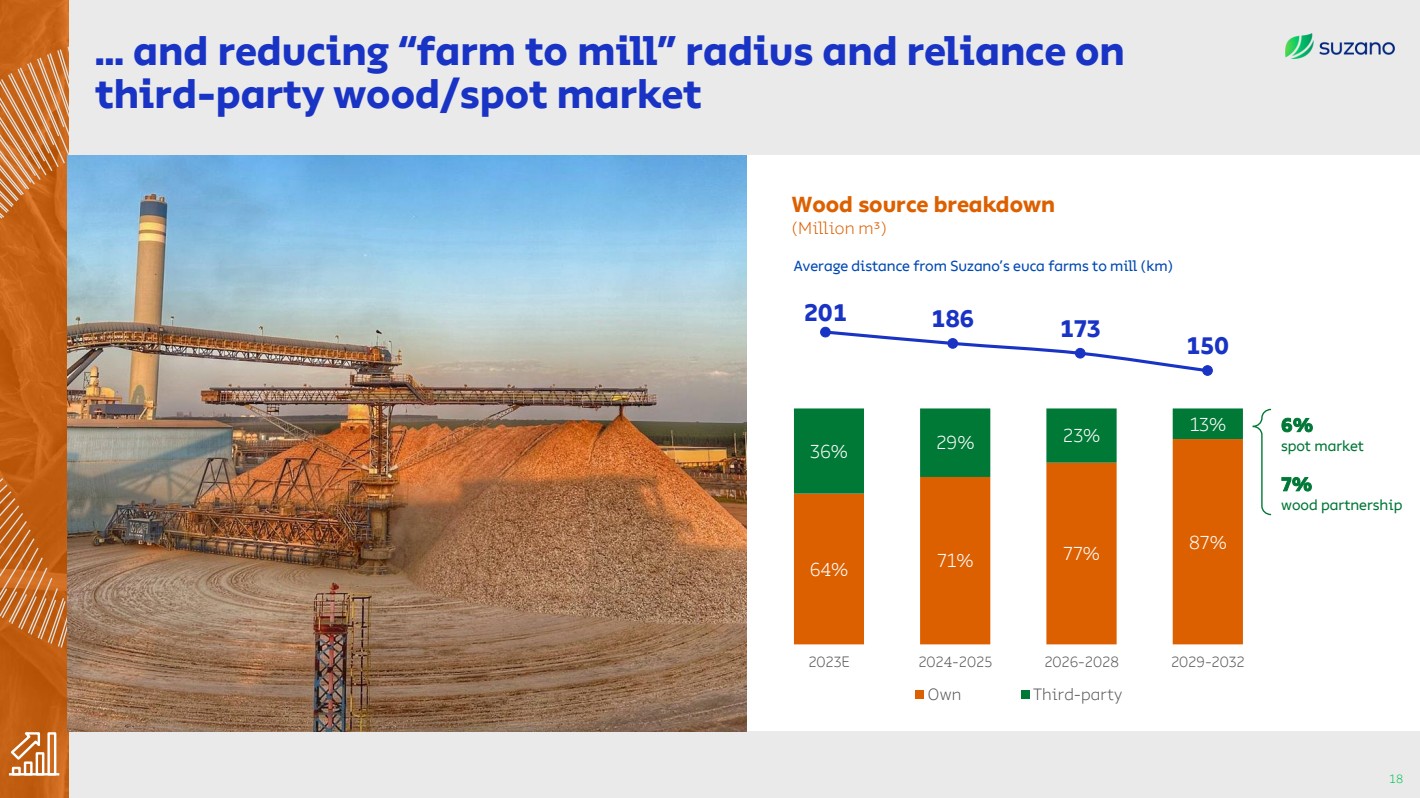

| … and reducing “farm to mill” radius and reliance on

third-party wood/spot market

18

64% 71% 77% 87%

36% 29% 23% 13%

2023E 2024-2025 2026-2028 2029-2032

Own Third-party

Average distance from Suzano’s euca farms to mill (km)

Wood source breakdown

(Million m³)

6%

spot market

7%

wood partnership

201 186 173

150 |

| MS TRÊS LAGOAS

Mill

RIBAS DO

RIO PARDO

Mill

In Mato Grosso do Sul, we are building a new

showcase in terms of wood competitiveness

19

− “Euca Farms” land bank already stablished

− Structural plantation program to be completed by late 2024 / early 2025

− Broadening field silviculture and genetic experiments with continuous

introduction of more productive clones

Cerrado

Uniqueness

Average structural radius: 65 km

Wood inbound logistics: 50% by six-trailer trucks

Flat landscape favoring mechanized plantation

Land base: own land, leases and partnerships. |

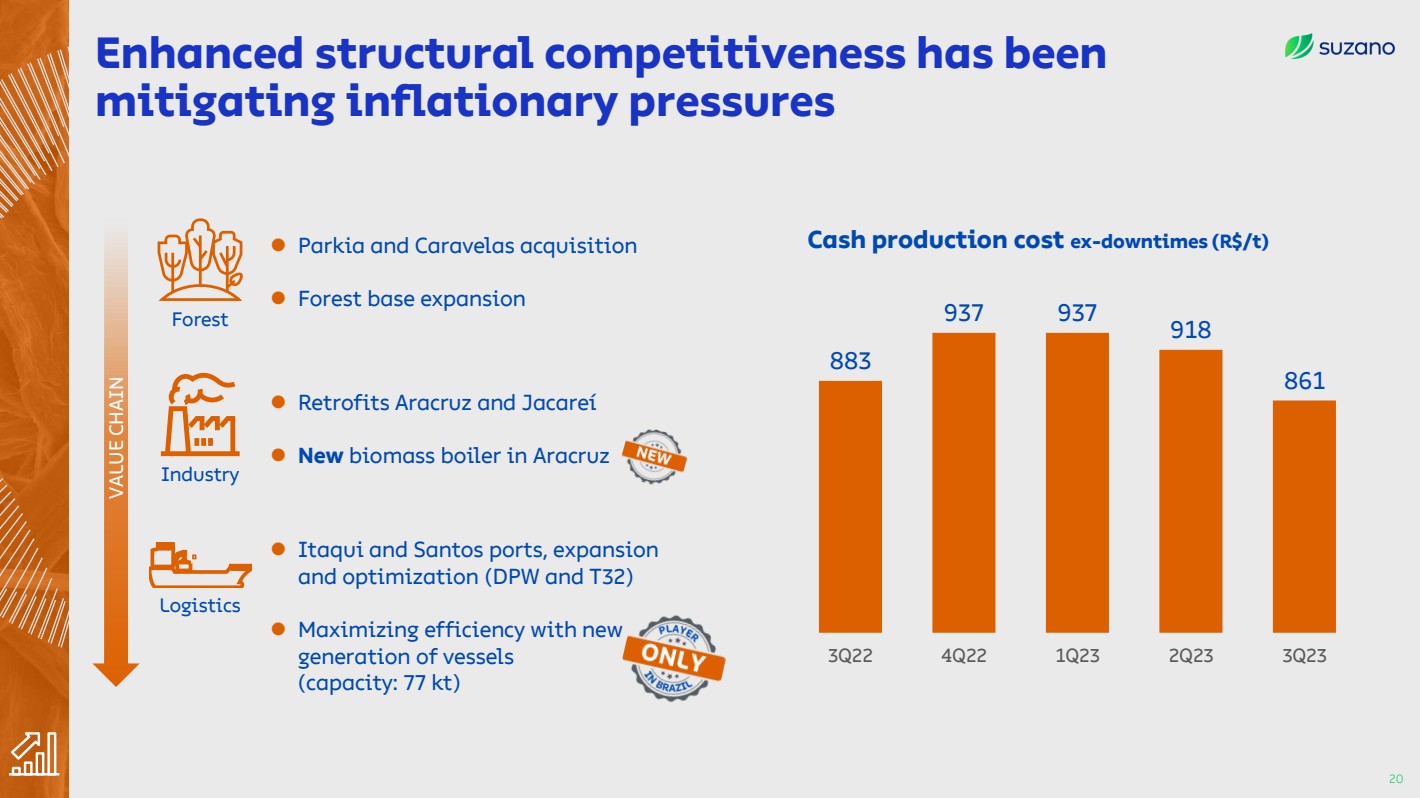

| Enhanced structural competitiveness has been

mitigating inflationary pressures

20

Forest

Industry

Logistics

⚫ Parkia and Caravelas acquisition

⚫ Forest base expansion

⚫ Retrofits Aracruz and Jacareí

⚫ New biomass boiler in Aracruz

⚫ Itaqui and Santos ports, expansion

and optimization (DPW and T32)

⚫ Maximizing efficiency with new

generation of vessels

(capacity: 77 kt)

883

937 937 918

861

3Q22 4Q22 1Q23 2Q23 3Q23

Cash production cost ex-downtimes (R$/t)

VALUE CHAIN |

| Maintain

relevance

in Pulp |

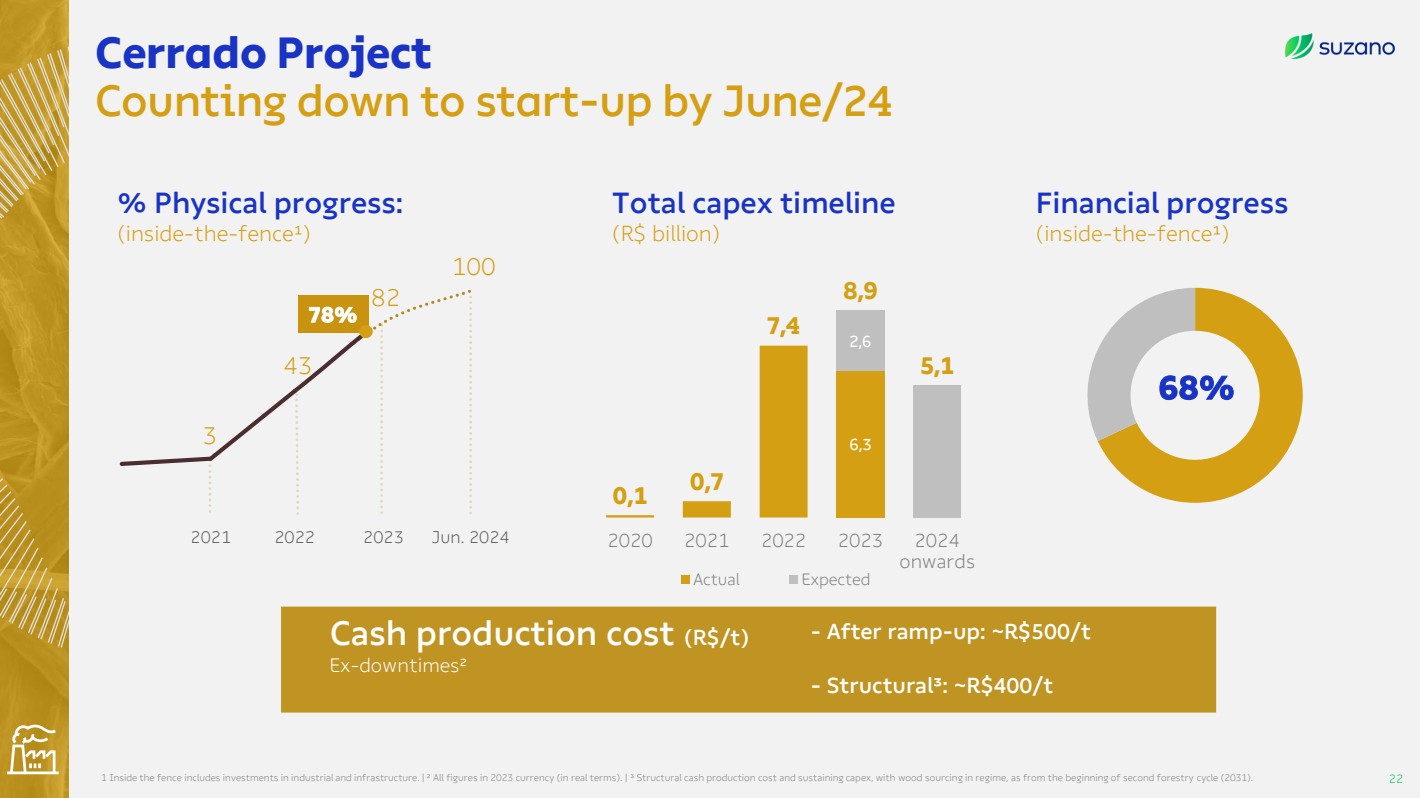

| Cerrado Project

Counting down to start-up by June/24

22

% Physical progress:

(inside-the-fence¹)

3

43

82

100

2021 2022 2023 Jun. 2024

78%

1 Inside the fence includes investments in industrial and infrastructure. | ² All figures in 2023 currency (in real terms). | ³ Structural cash production cost and sustaining capex, with wood sourcing in regime, as from the beginning of second forestry cycle (2031).

68%

Total capex timeline

(R$ billion)

6,3

2,6

0,1 0,7

7,4

8,9

5,1

2020 2021 2022 2023 2024

onwards

Actual Expected

Financial progress

(inside-the-fence¹)

Cash production cost (R$/t)

Ex-downtimes²

- After ramp-up: ~R$500/t

- Structural³: ~R$400/t |

| Cerrado Project

Counting down to a well executed learning curve

23

-

50

100

150

200

250

Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month

10

Month 11Month 12

Accumulated Monthly

Monthly production rate (t/month)

Learning curve

conclusion

Scheduled

downtime 2 MM t

Learning curve of

~9 months |

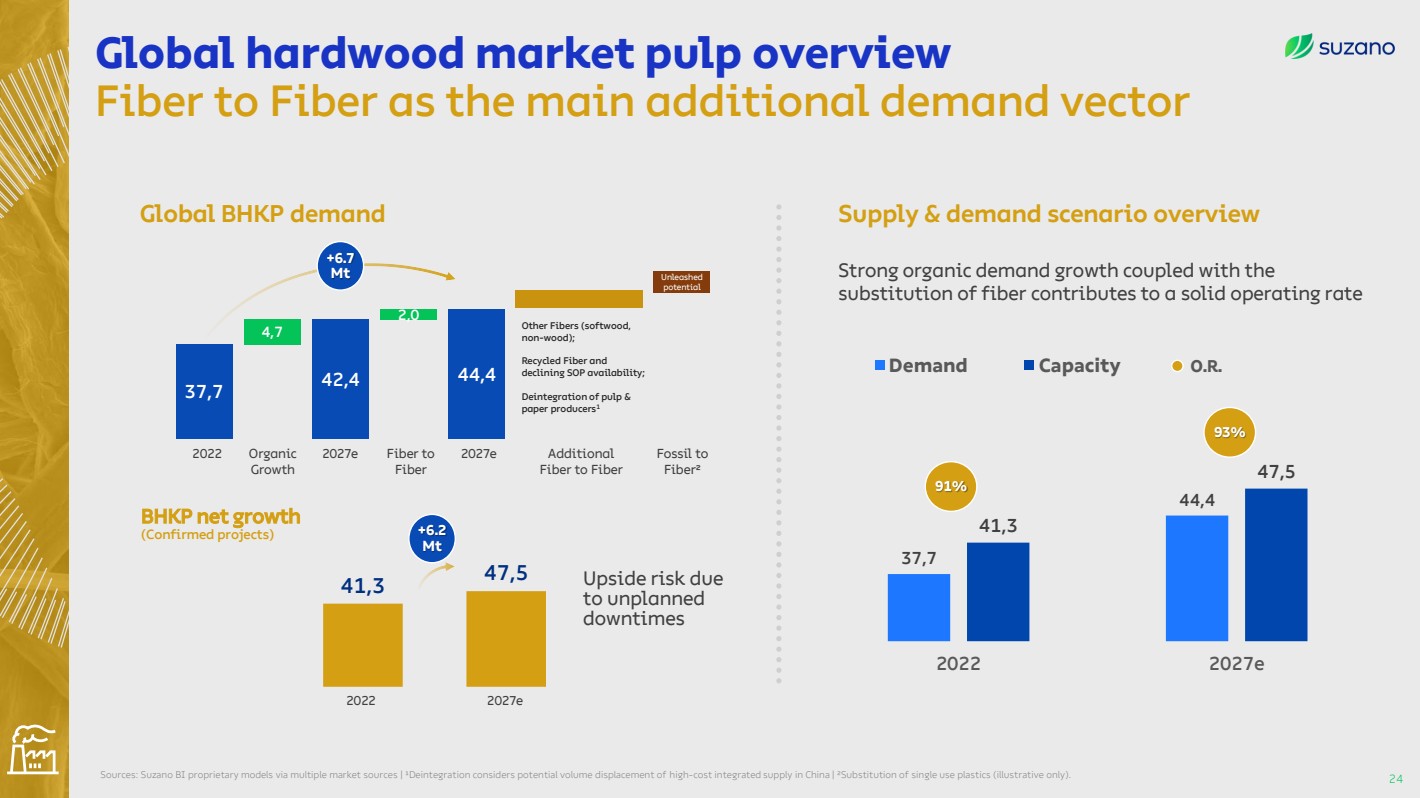

| Global hardwood market pulp overview

Fiber to Fiber as the main additional demand vector

24 Sources: Suzano BI proprietary models via multiple market sources | ¹Deintegration considers potential volume displacement of high-cost integrated supply in China | ²Substitution of single use plastics (illustrative only).

BHKP net growth

(Confirmed projects)

2022 2027e

41,3 47,5

+6.2

Mt

Upside risk due

to unplanned

downtimes

37,7

44,4

41,3

47,5

2022 2027e

Demand Capacity

91%

93%

O.R.

Supply & demand scenario overview

Strong organic demand growth coupled with the

substitution of fiber contributes to a solid operating rate

37,7 42,4 44,4

4,7

2,0

Global BHKP demand

2022 Organic

Growth

2027e Additional

Fiber to Fiber

2027e Fossil to

Fiber²

Fiber to

Fiber

Unleashed

potential

Other Fibers (softwood,

non-wood);

Recycled Fiber and

declining SOP availability;

Deintegration of pulp &

paper producers1

+6.7

Mt |

| 37,7

42,4 44,4

4,7

2,0 Other Fibers

(softwood,

non-wood);

Recycled Fiber

and declining

SOP

availability;

Deintegration

of pulp & paper

producers1

Unleashed

potential

Additional

2022 Organic

Growth

2027e Additional

Fiber to

Fiber

2027e Fossil to

Fiber²

Fossil to

Fiber

Global

BHKP Demand

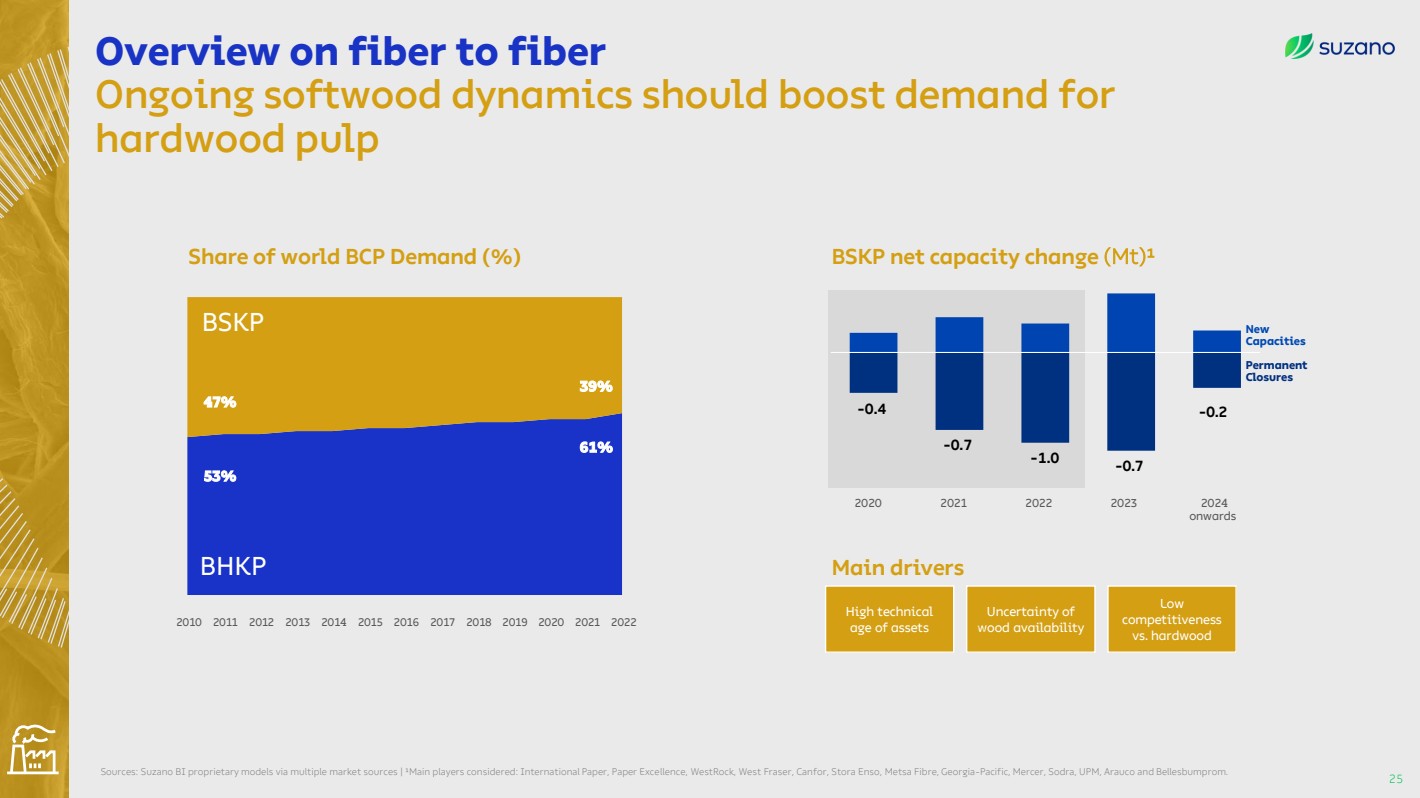

Overview on fiber to fiber

Ongoing softwood dynamics should boost demand for

hardwood pulp

25 Sources: Suzano BI proprietary models via multiple market sources | ¹Main players considered: International Paper, Paper Excellence, WestRock, West Fraser, Canfor, Stora Enso, Metsa Fibre, Georgia-Pacific, Mercer, Sodra, UPM, Arauco and Bellesbumprom.

At least ≈ 6.7 Mt

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

BSKP

BHKP

Share of world BCP Demand (%)

53%

61%

47%

39%

BSKP net capacity change (Mt)¹

0.3

-0.7

0.6

-1.3

0.5

-1.5

1.0

-1.2

0.4

-0.6

-0.7

-0.2

New

Capacities

Permanent

Closures

Main drivers

High technical

age of assets

Uncertainty of

wood availability

Low

competitiveness

vs. hardwood

2020 2021 2022 2023 2024

onwards

-0.4

-0.7

-1.0 |

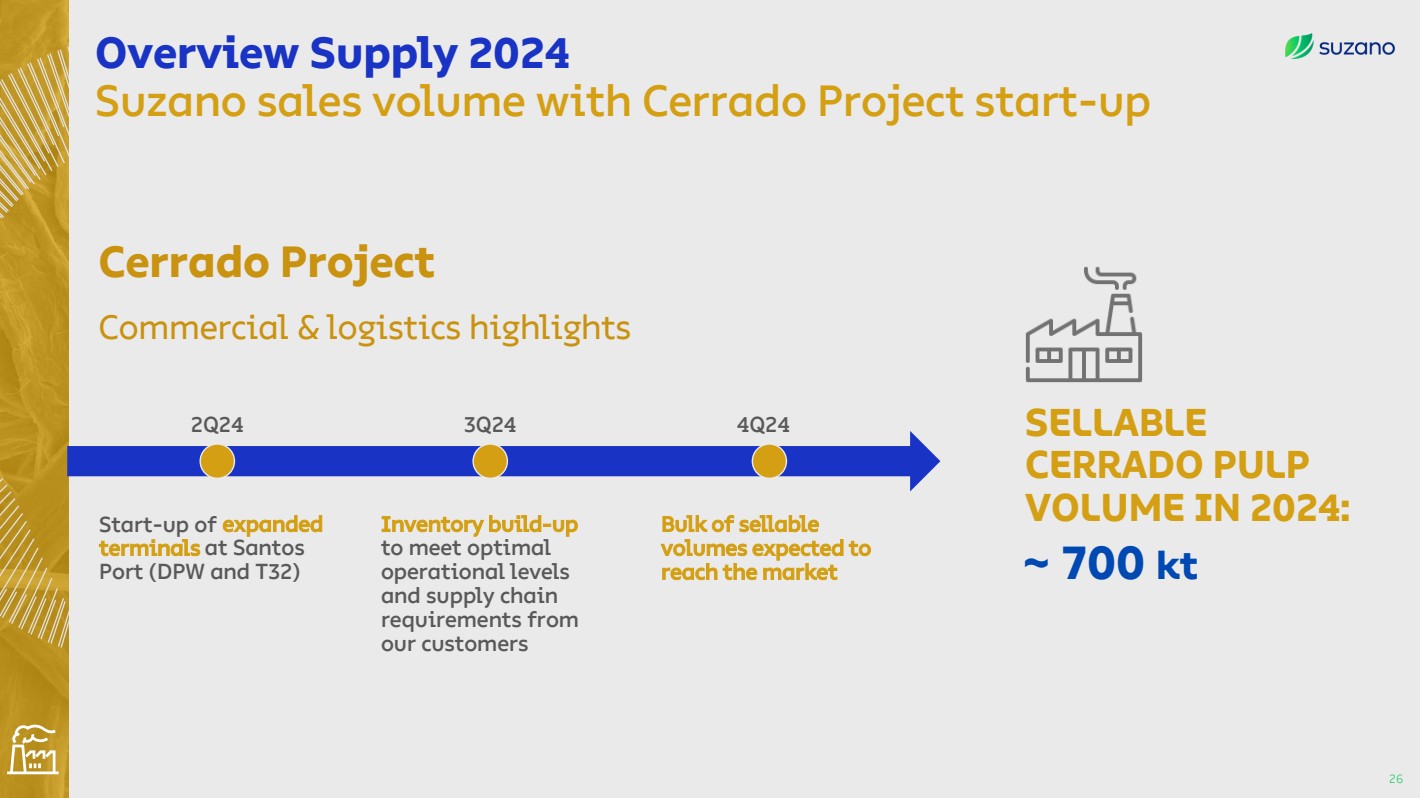

| Overview Supply 2024

Suzano sales volume with Cerrado Project start-up

26

~ 700 kt

SELLABLE

CERRADO PULP

VOLUME IN 2024:

Cerrado Project

Commercial & logistics highlights

2Q24 3Q24

Start-up of expanded

terminals at Santos

Port (DPW and T32)

Inventory build-up

to meet optimal

operational levels

and supply chain

requirements from

our customers

4Q24

Bulk of sellable

volumes expected to

reach the market |

| Marginal Cash Costs

27 Sources: Hawkins Wright and Suzano BI | | 1Avg. Quarterly PIX China calculated using only end of the month values within the quarter | 2Marginal Cash Cost analysis conducted by Hawkins Wright considering only market BHKP

Over the next five years, market volatility could play an important role,

however price valleys should continue to be anchored by marginal cash costs

350

400

450

500

550

600

650

700

750

800

850

900

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20 1Q21 1Q22 1Q23 1Q24

BHKP Price1

Marginal Cash Cost2

3Q23

533 USD/t

3Q23

575 USD/t

4Q24

560 USD/t

Commodities and

Wood availability

can influence future

costs |

| Marginal Cash Costs

28

Current price cycle has fostered an increase in market-related downtimes

69%

31%

FY2021

60%

40%

FY2022

44%

56%

YDE 2023e

(visible full year effect)

1.0

1.3

1.4

Other

Market-related

BHKP unexpected downtimes3

(Market Pulp)

300

350

400

450

500

550

600

650

700

750

800

850

900

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20 1Q21 1Q22 1Q23 1Q24

BHKP Price

Marginal Cash Cost

US$ per ton - CIF China

Global BHKP marginal cost of production, CIF China (Market Pulp)

3Q23

533 USD/t

4Q24

560

USD/t

3Q23

575 USD/t

Sources: Hawkins Wright and Suzano BI | | 1Avg. Quarterly PIX China calculated using only end of the month values within the quarter | 2Marginal Cash Cost analysis conducted by Hawkins Wright considering only market BHKP |

3Downtimes for FY21 and FY22 according with RISI and YTD23 by Suzano Market Intel. |

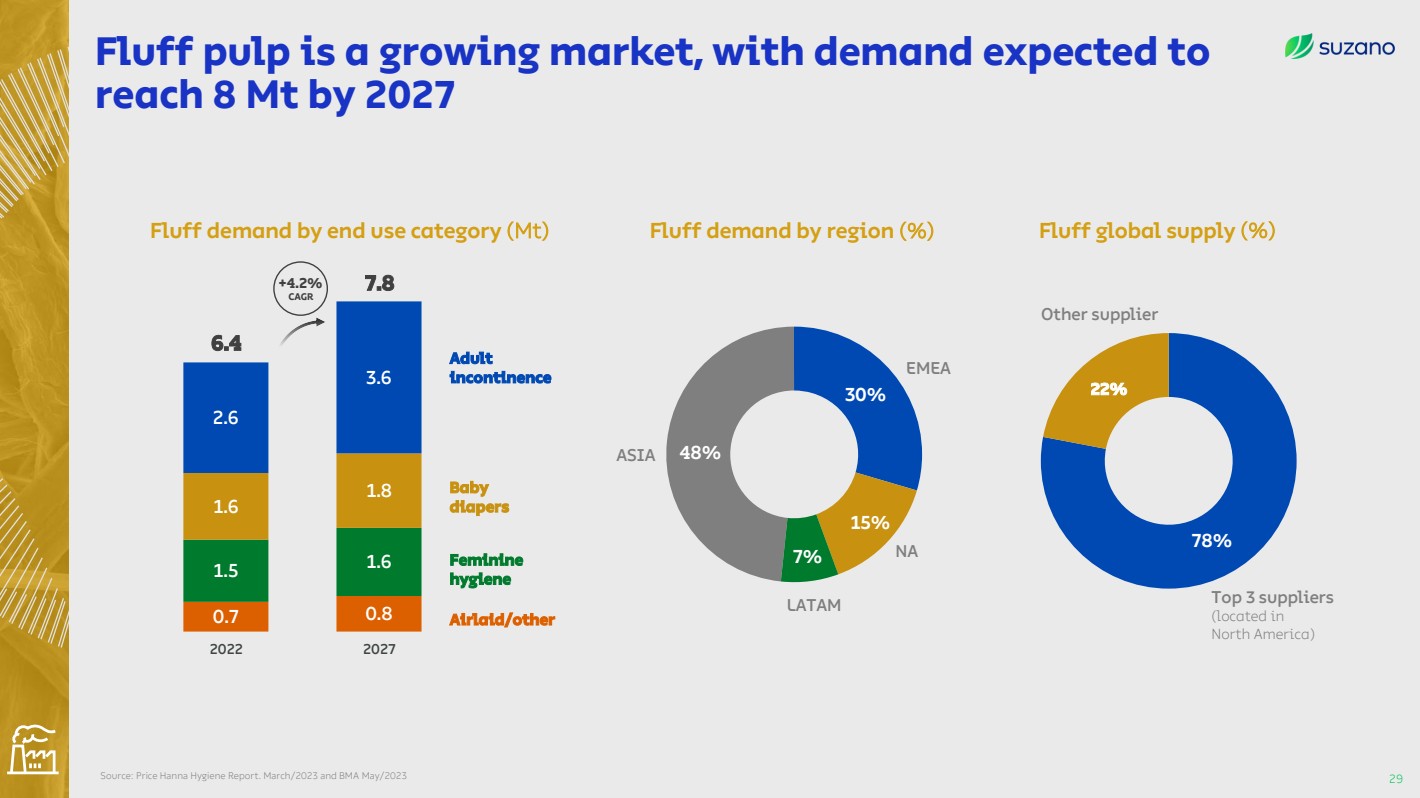

| Fluff pulp is a growing market, with demand expected to

reach 8 Mt by 2027

29 Source: Price Hanna Hygiene Report. March/2023 and BMA May/2023

0.7 0.8

1.5 1.6

1.6

1.8

2.6

3.6

6.4

7.8

2022 2027

Adult

incontinence

Baby

diapers

Feminine

hygiene

Airlaid/other

78%

Top 3 suppliers

(located in

North America)

Other supplier

22%

48%

30%

15%

7%

EMEA

ASIA

NA

LATAM

+4.2%

CAGR

Fluff demand by end use category (Mt) Fluff demand by region (%) Fluff global supply (%) |

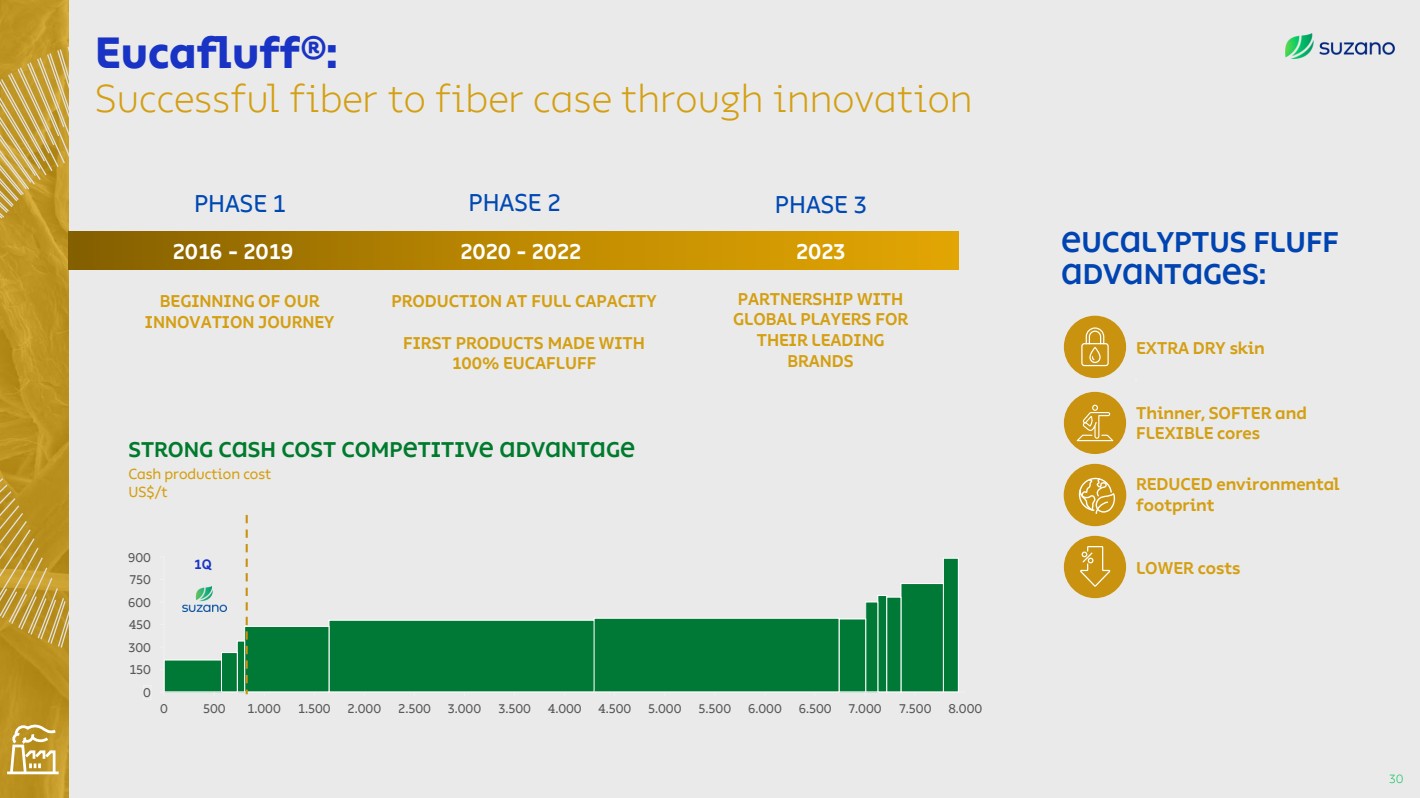

| Eucafluff®:

Successful fiber to fiber case through innovation

30

LOWER costs

REDUCED environmental

footprint

Thinner, SOFTER and

FLEXIBLE cores

Eucalyptus fluff

advantages:

EXTRA DRY skin

0 500 1.000

0

450

8.000

600

150

750

7.000

900

1.500 2.000 2.500 3.000 3.500 4.000 4.500 5.000 5.500 6.000 6.500 7.500

300

1Q

STRONG CASH COST COMPETITIVE ADVANTAGE

Cash production cost

US$/t

BEGINNING OF OUR

INNOVATION JOURNEY

2016 - 2019 2020 - 2022 2023

PARTNERSHIP WITH

GLOBAL PLAYERS FOR

THEIR LEADING

BRANDS

PHASE 1 PHASE 2

PRODUCTION AT FULL CAPACITY

FIRST PRODUCTS MADE WITH

100% EUCAFLUFF

PHASE 3 |

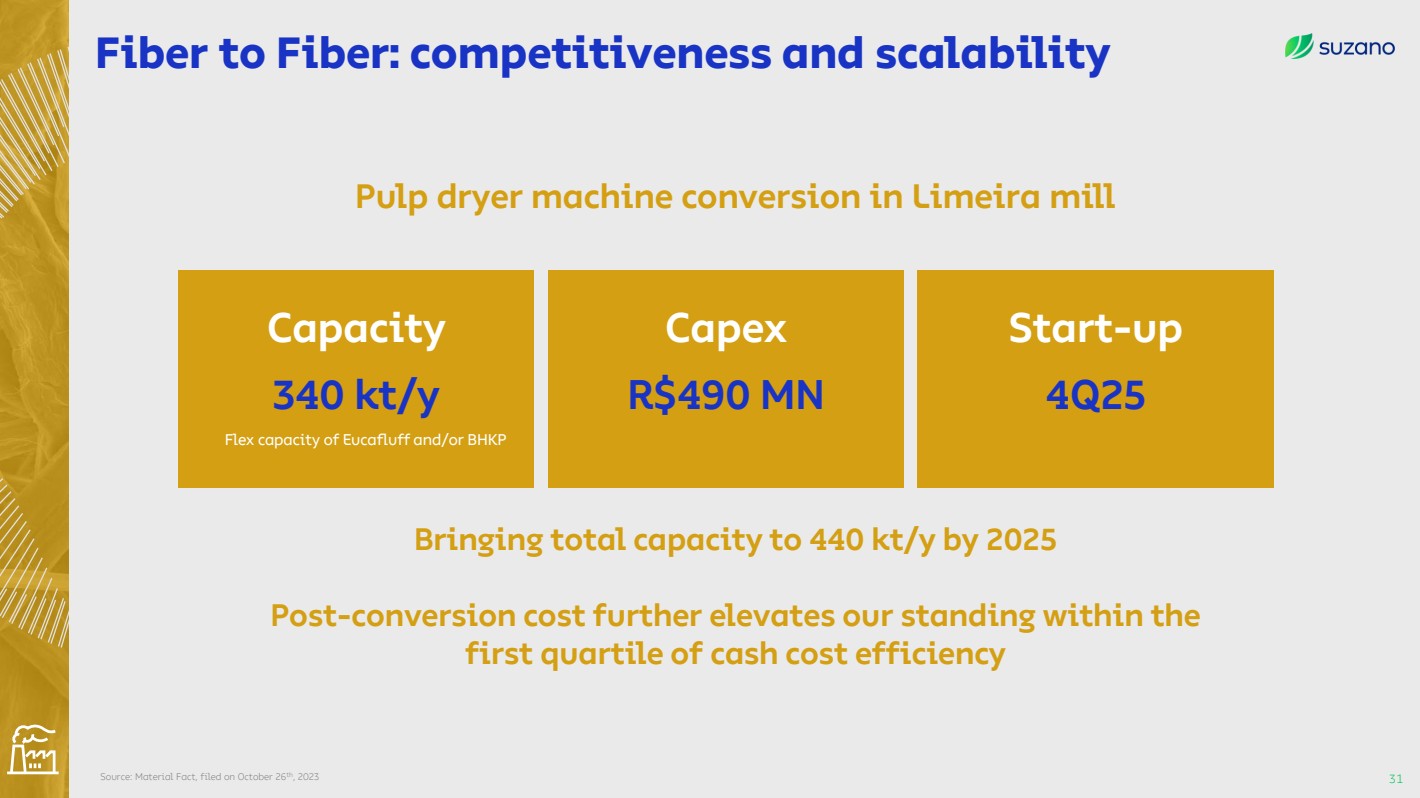

| Source: Material Fact, filed on October 26th, 2023

Fiber to Fiber: competitiveness and scalability

31

Pulp dryer machine conversion in Limeira mill

Capacity

340 kt/y

Flex capacity of Eucafluff and/or BHKP

Bringing total capacity to 440 kt/y by 2025

Post-conversion cost further elevates our standing within the

first quartile of cash cost efficiency

Capex

R$490 MN

Start-up

4Q25 |

| Advance in the

links of the

chain, always

with competitive

advantage |

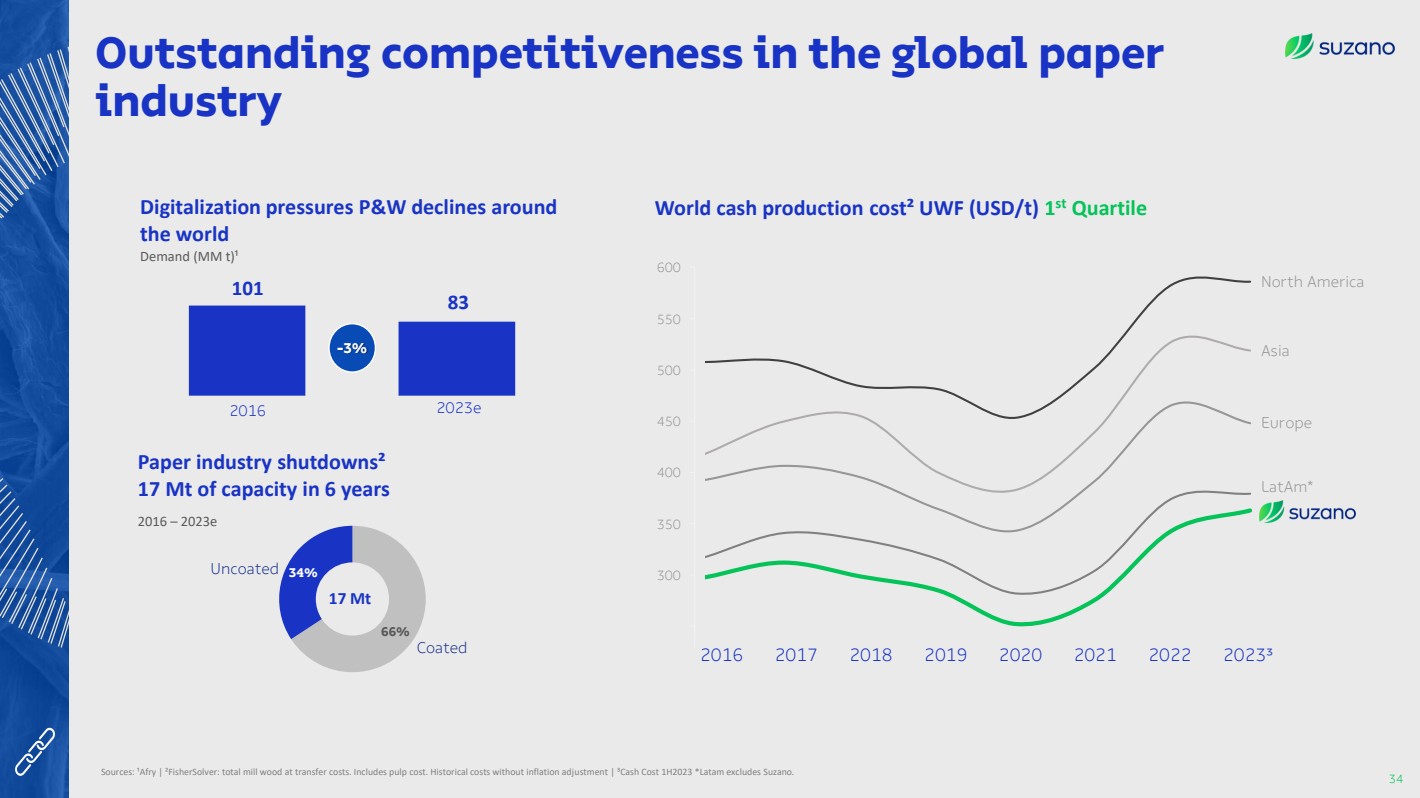

| Paper &

Packaging |

| Sources: ¹Afry | ²FisherSolver: total mill wood at transfer costs. Includes pulp cost. Historical costs without inflation adjustment | ³Cash Cost 1H2023 *Latam excludes Suzano.

2016 2023e

101

83

66%

Coated

Uncoated 34%

Digitalization pressures P&W declines around

the world

17 Mt

2016 – 2023e

Demand (MM t)¹

2016 2017 2018 2019 2020 2021 2022 2023³

300

350

400

450

500

550

600

Europe

LatAm*

North America

Asia

World cash production cost² UWF (USD/t) 1

st Quartile

Paper industry shutdowns²

17 Mt of capacity in 6 years

Outstanding competitiveness in the global paper

industry

34

-3% |

| Sales transformation Suzano+ CRM and

e-commerce

Suzano+ 2.0 Omnichannel

+ AI

Suzano+

LatAm

Value chain

advance and

margin increase

Customer service

and sales process

improvement

Technology

upgrade

Data driven and

customer service

channels

expansion

Customer experience

and customer

centricity

2014 2015 2018 2020 2022 2023

Focused on expanding our customer base

35

Total active costumers (‘000)

17.4 25.7 29.4 35.9 43.2 44.7

LTM

Sep/23 |

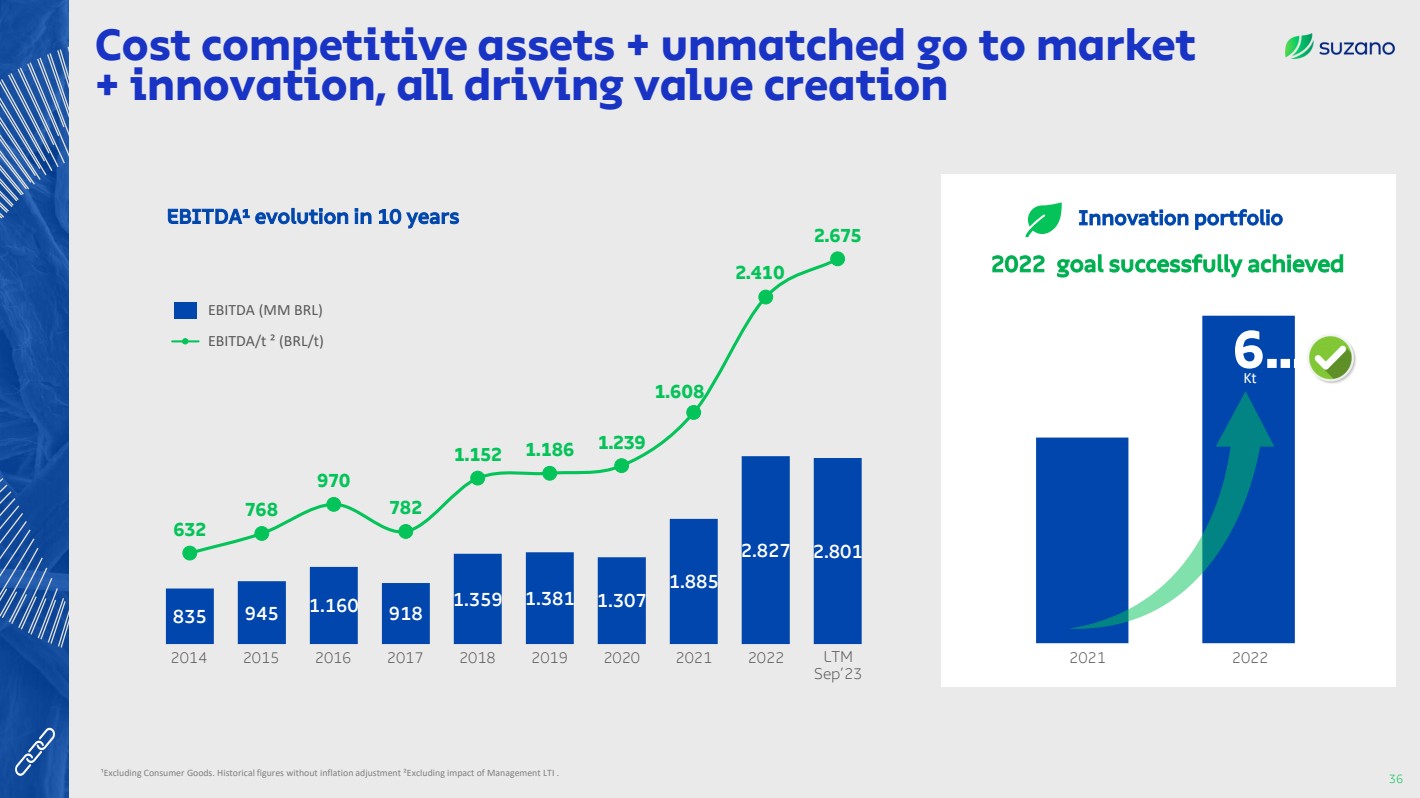

| Cost competitive assets + unmatched go to market

+ innovation, all driving value creation

36

2014 2015 2016 2017 2018 2019 2020 2021 2022

¹Excluding Consumer Goods. Historical figures without inflation adjustment ²Excluding impact of Management LTI .

Innovation portfolio

2022 goal successfully achieved

6…

2021 2022

Kt

835 945 1.160 918

1.359 1.381 1.307

1.885

2.827 2.801

632

768

970

782

1.152 1.186 1.239

1.608

2.410

2.675

EBITDA (MM BRL)

EBITDA/t ² (BRL/t)

EBITDA¹ evolution in 10 years

LTM

Sep’23 |

| Consumer

goods |

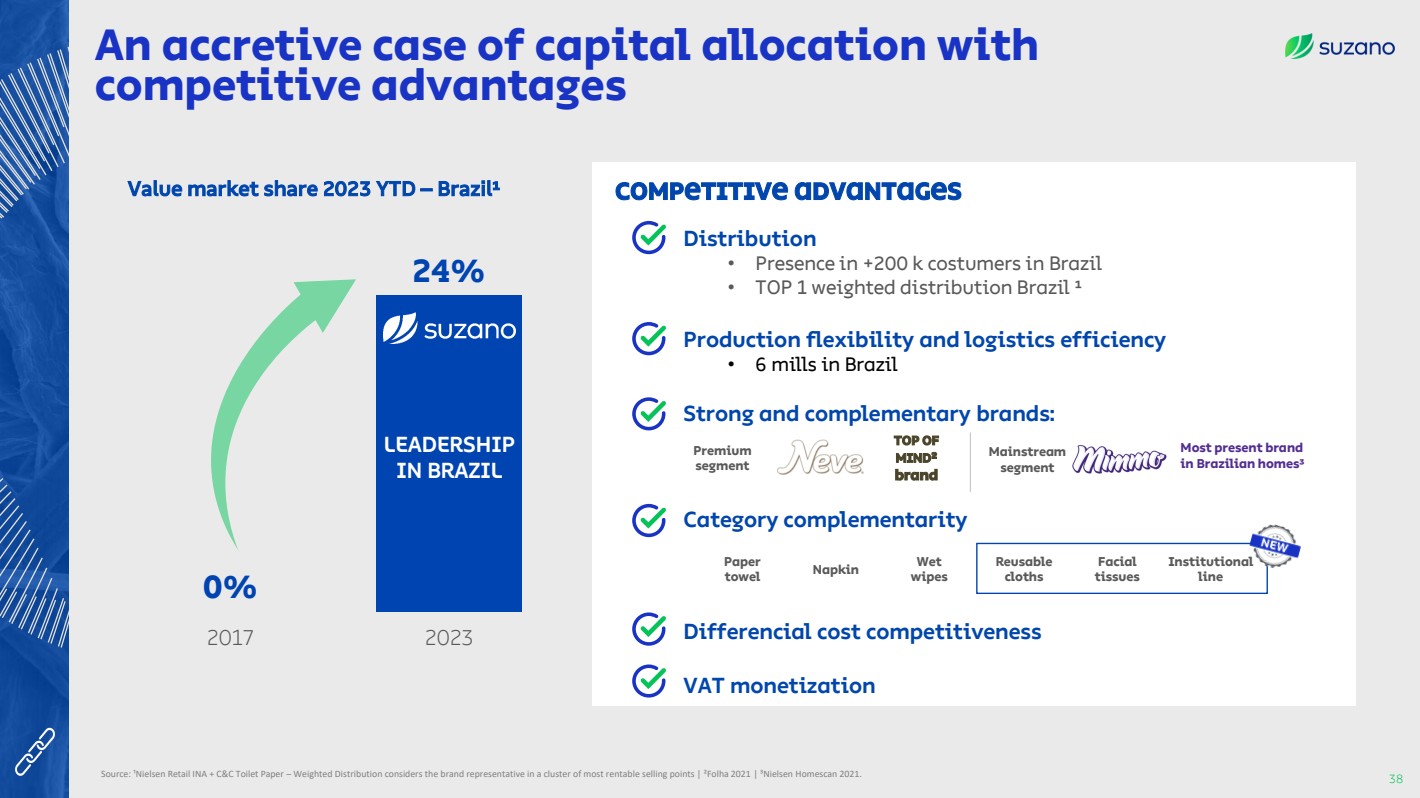

| An accretive case of capital allocation with

competitive advantages

38 Source: ¹Nielsen Retail INA + C&C Toilet Paper – Weighted Distribution considers the brand representative in a cluster of most rentable selling points | ²Folha 2021 | ³Nielsen Homescan 2021.

0%

24%

2017 2023

Value market share 2023 YTD – Brazil¹

LEADERSHIP

IN BRAZIL

COMPETITIVE ADVANTAGES

Distribution

• Presence in +200 k costumers in Brazil

• TOP 1 weighted distribution Brazil ¹

Production flexibility and logistics efficiency

• 6 mills in Brazil

Strong and complementary brands:

Category complementarity

Differencial cost competitiveness

VAT monetization

Most present brand

in Brazilian homes³

Premium

segment

Mainstream

segment

TOP OF

MIND²

brand

Paper

towel Napkin Reusable

cloths

Wet

wipes

Facial

tissues

Institutional

line |

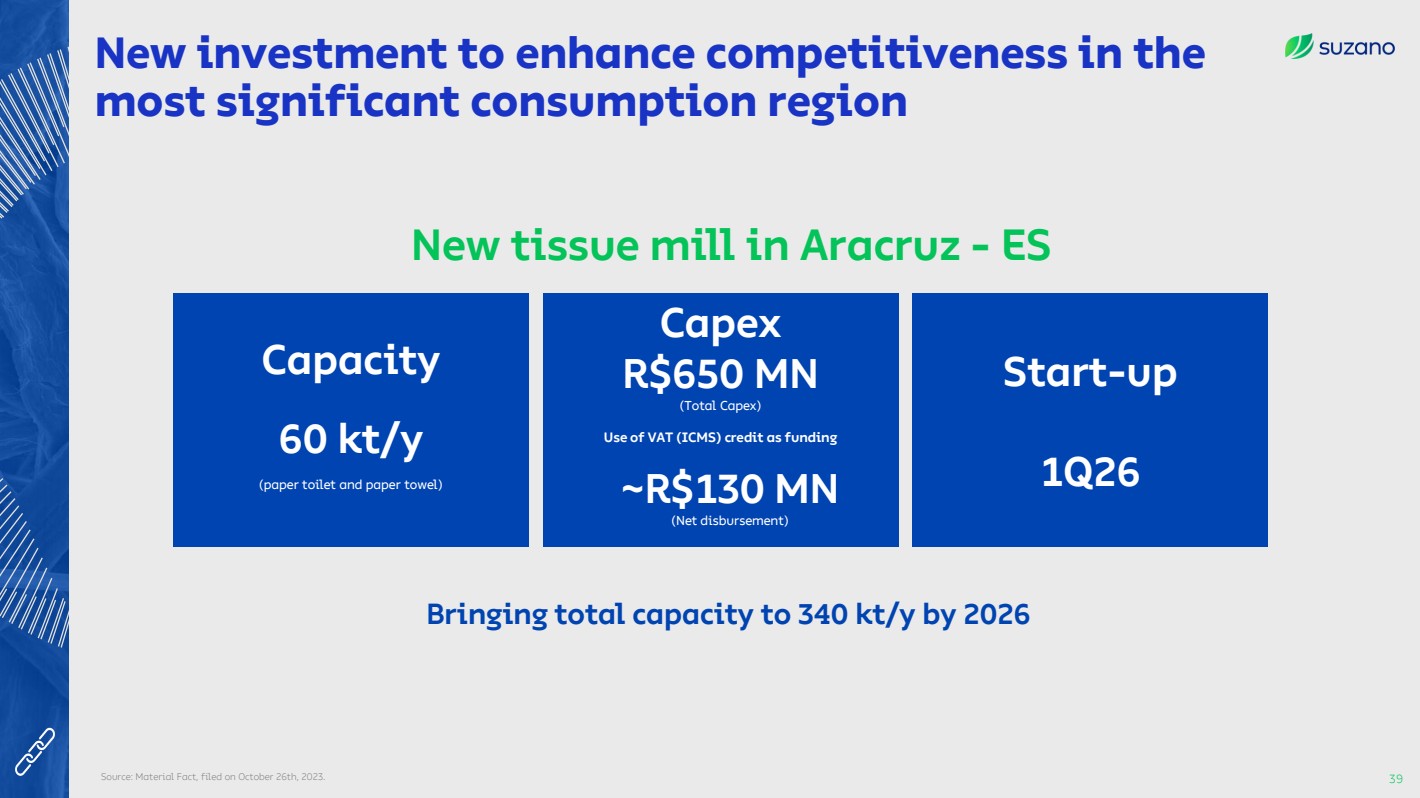

| New investment to enhance competitiveness in the

most significant consumption region

Source: Material Fact, filed on October 26th, 2023. 39

Capacity

60 kt/y

(paper toilet and paper towel)

Bringing total capacity to 340 kt/y by 2026

Start-up

1Q26

Capex

R$650 MN

(Total Capex)

Use of VAT (ICMS) credit as funding

~R$130 MN

(Net disbursement)

New tissue mill in Aracruz - ES |

| Play a

leading role in

sustainability |

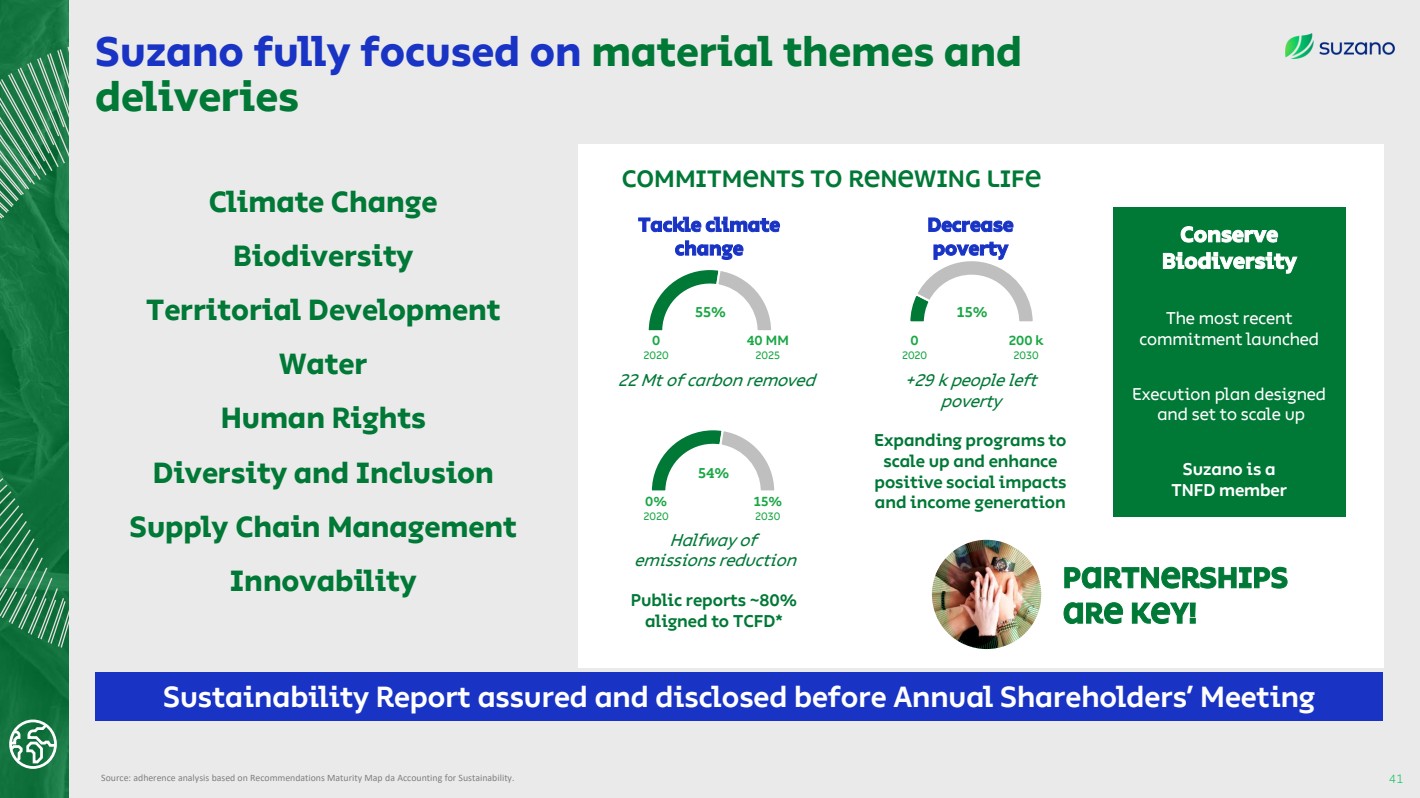

| Suzano fully focused on material themes and

deliveries

41

Climate Change

Biodiversity

Territorial Development

Water

Human Rights

Diversity and Inclusion

Supply Chain Management

Innovability

Commitments to Renewing Life

Source: adherence analysis based on Recommendations Maturity Map da Accounting for Sustainability.

Tackle climate

change

Decrease

poverty

Public reports ~80%

aligned to TCFD*

Expanding programs to

scale up and enhance

positive social impacts

and income generation

Conserve

Biodiversity

Execution plan designed

and set to scale up

Suzano is a

TNFD member

The most recent

commitment launched

Partnerships

are key!

Sustainability Report assured and disclosed before Annual Shareholders’ Meeting

Halfway of

emissions reduction

54%

15%

2030

0%

2020

55% 15%

+29 k people left

poverty

22 Mt of carbon removed

40 MM

2025

0

2020

200 k

2030

0

2020 |

| Cerrado Project

A case towards the SDG Agenda

42

COMMITMENT

Generate

clean energy

Combat climate crisis

&

Conserve biodiversity

Reduce poverty

&

Ensure education

Reduce waste

&

Protect our water

Acting

Pillars:

− Education

− Job generation

− Income generation

− Public administration

− Infrastructure

− Rights protection

− Health

~180 MW avg surplus

Carbon: CO2

/t and MORE FORESTS

Biodiversity: regeneration and

ecological corridors

Greater eco-efficiency |

| agenda

Financial

Management |

| 0

50

100

150

200

250

ECA - Finnvera IFC Local Debentures

(Average)

Source: Bloomberg

Seizing opportunities with diversified funding

sources

44

Estimated cost inside bond yield curve

at Issuance (bps)

0.8 0.6 0.6 Size

(US$ billion)

Issuance Nov/22 Dec/22 Jun-Sep/23

Bond 25

6,53%

Bond 26

6,33%

Bond 27

6,21%

Bond 28

6,66%

Bond 29

6,73%

Bond 30

6,90%

Bond 31

7,07%

Bond 32

7,05% Bond 47

7,57%

Bond 31

3,95%

Bond 32

3,28%

Bond 28

2,70%

2%

3%

4%

5%

6%

7%

8%

0 5 10 15 20 25

Yield (%)

Average Life (y)

Bid Yield for Outstanding Bonds (Oct 23rd, 23)

Yield at Issuance (Bonds issued in 2020-21)

Trendline for Bid Yield (Oct 2nd, 23) |

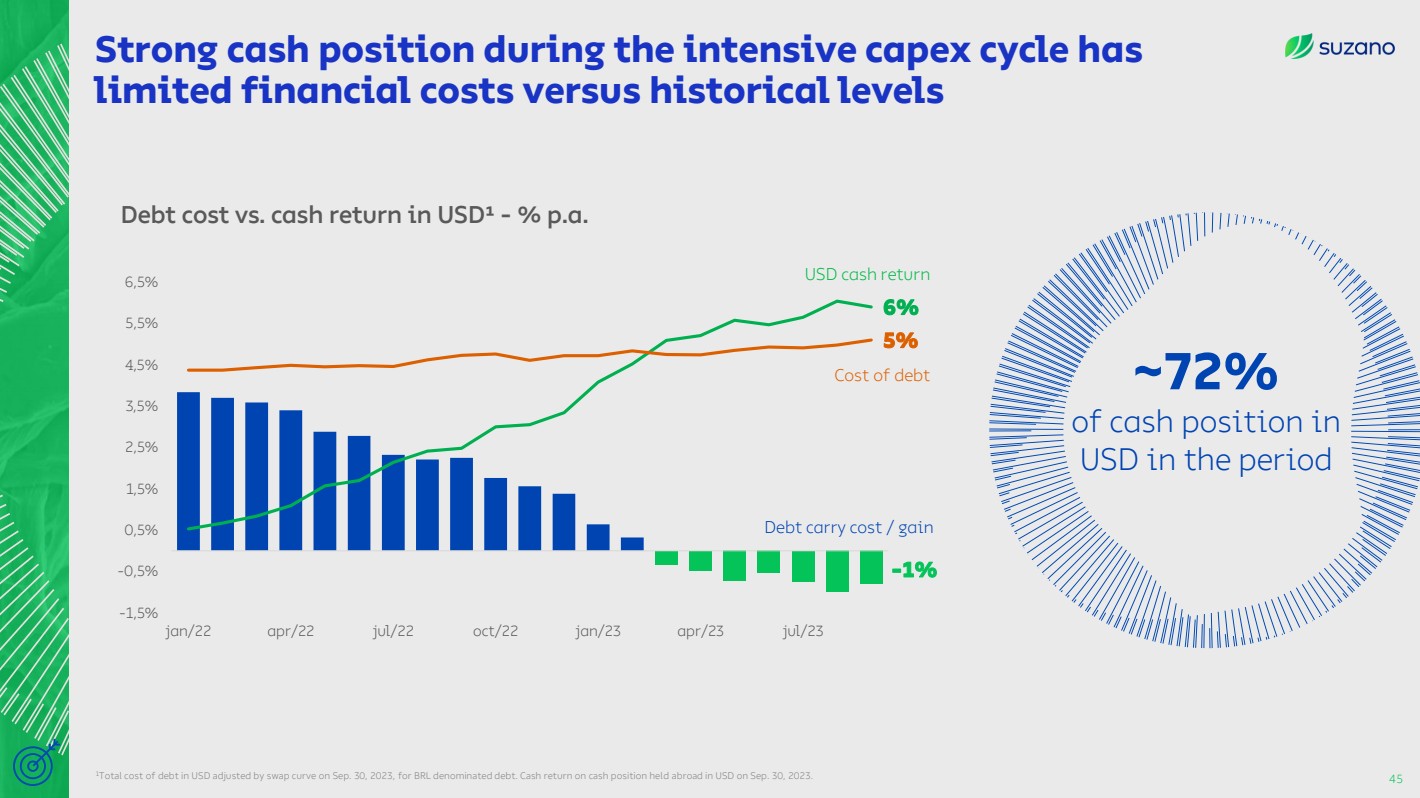

| -1%

6%

5%

-1,5%

-0,5%

0,5%

1,5%

2,5%

3,5%

4,5%

5,5%

6,5%

jan/22 apr/22 jul/22 oct/22 jan/23 apr/23 jul/23

1Total cost of debt in USD adjusted by swap curve on Sep. 30, 2023, for BRL denominated debt. Cash return on cash position held abroad in USD on Sep. 30, 2023.

USD cash return

Cost of debt ~72%

of cash position in

USD in the period

Debt cost vs. cash return in USD¹ - % p.a.

Strong cash position during the intensive capex cycle has

limited financial costs versus historical levels

45

Debt carry cost / gain |

| Cost of carbon emissions

is incorporated into

financial analysis, to

assess risks of future

public policies that may

increase costs for the

company

Financial parameters

Net present value Payback

Shadow price Enabling price

Viability assessment, to

determine under which

carbon market scenario

the project under analysis

becomes accretive.

75%

Capital allocation

ESG criteria in decision making process

46

Modernization CAPEX Scoring

Impacts on

commitments to

Renewing Life

Qualitative &

quantitative

parameters

25% |

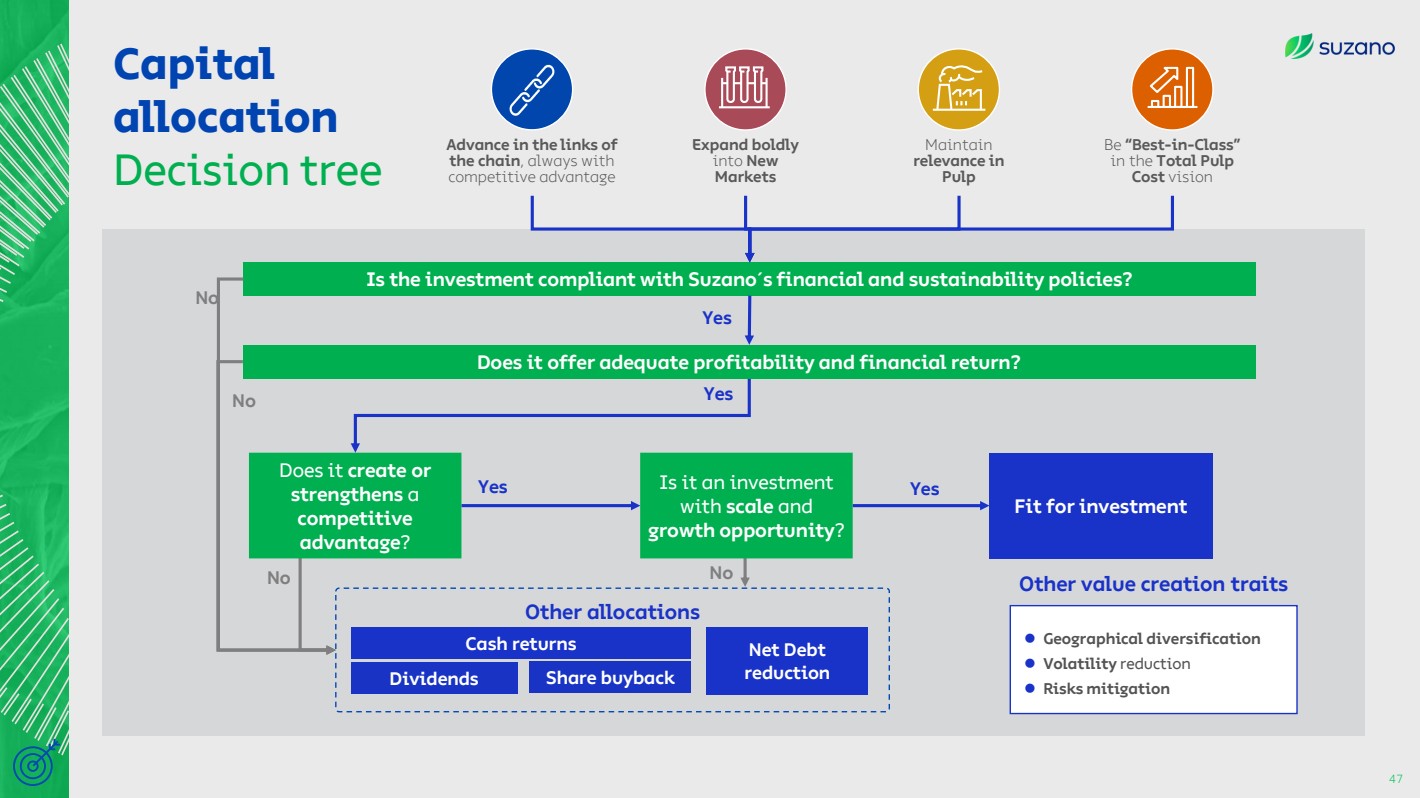

| Capital

allocation

Decision tree

Expand boldly

into New

Markets

Be “Best-in-Class”

in the Total Pulp

Cost vision

Advance in the links of

the chain, always with

competitive advantage

Maintain

relevance in

Pulp

Is it an investment

with scale and

growth opportunity?

⚫ Geographical diversification

⚫ Volatility reduction

⚫ Risks mitigation

No

Does it create or

strengthens a

competitive

advantage?

Share buyback

Cash returns Net Debt

reduction

Other allocations

Yes

Yes Yes

Fit for investment

No Other value creation traits No

Does it offer adequate profitability and financial return?

Is the investment compliant with Suzano´s financial and sustainability policies?

Yes

No

47

Dividends |

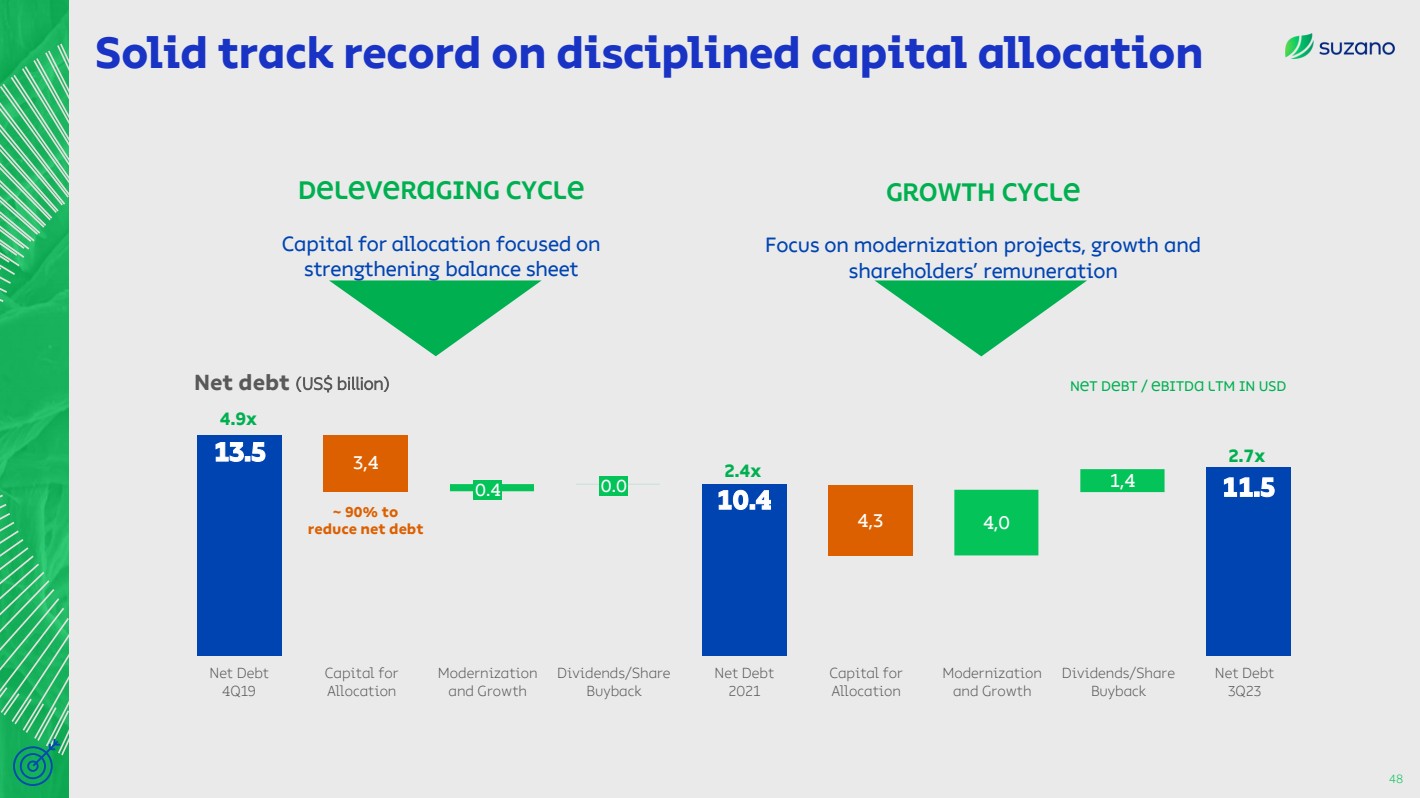

| 13.5

10.4 11.5

3,4

4,3 4,0

1,4

Capital for

Allocation

Dividends/Share

Buyback

Modernization

and Growth

0.4 0.0

Capital for

Allocation

Modernization

and Growth

Dividends/Share

Buyback

Net Debt

3Q23

Net debt (US$ billion)

Deleveraging cycle

Capital for allocation focused on

strengthening balance sheet

Growth cycle

Focus on modernization projects, growth and

shareholders’ remuneration

4.9x

2.4x

2.7x

Net Debt / EBITDA LTM in USD

Solid track record on disciplined capital allocation

48

~ 90% to

reduce net debt

Net Debt

2021

Net Debt

4Q19 |

| 46.40

54.40

Average buyback

price

Share price

Oct/231

:

17%

return

Share buyback program adding value to

shareholders

49 1Closing price of 10/23/2023

Share price (R$)

Buyback volume

60 million

shares

1

st program

(avg. price

R$48.33)

2

nd program

(avg. price

R$46.84)

3

rd program

(avg. price

R$44.02)

2021 2022 2023

35

40

45

50

55

60

65

70

75 |

| How we reached the first 100 years

and will move forward...

Q&A

Financial discipline

Culture and innovability

Accretive capital allocation track record

Recurring investments in competitiveness

Addressable markets expansion

Higher cash generation level, post Cerrado

Shared value as core to business strategy |

| Eucalyptus fiber

ir.suzano.com.br |

Suzano (NYSE:SUZ)

過去 株価チャート

から 4 2024 まで 5 2024

Suzano (NYSE:SUZ)

過去 株価チャート

から 5 2023 まで 5 2024