SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

RULE 13E-3 TRANSACTION STATEMENT UNDER SECTION 13(E)

OF THE SECURITIES EXCHANGE ACT OF 1934

Vacasa, Inc.

(Name of the Issuer)

Vacasa, Inc.

Vacasa Holdings LLC

Casago Holdings, LLC

Vista Merger Sub II Inc.

Vista Merger Sub LLC

Casago Global, LLC

Roofstock, Inc.

MHRE STR II, LLC

TRT Investors 37, LLC

SLP V Venice Feeder I, L.P.

SLP Venice Holdings. L.P.

SLP V Aggregator GP, L.L.C.

Silver Lake Technology Associates V, L.P.

SLTA V (GP), L.L.C.

Silver Lake Group, L.L.C

RW Vacasa AIV L.P.

RW Industrious Blocker L.P.

Riverwood Capital Partners II (Parallel-B) L.P.

RCP III Vacasa AIV L.P.

RCP III Blocker Feeder L.P.

Riverwood Capital Partners III (Parallel-B) L.P.

RCP III (A) Blocker Feeder L.P.

RCP III (A) Vacasa AIV L.P.

Level Equity Opportunities Fund 2015, L.P.

Level Equity Opportunities Fund 2018, L.P.

LEGP II AIV(B), L.P.

LEGP I VCS, LLC

LEGP II VCS, LLC

Level Equity – VCS Investors, LLC

(Names of Persons Filing Statement)

Class A Common Stock, par value $0.00001 per share

(Title of Class of Securities)

91854V 206

(CUSIP Number of Class of Securities)

| | | | | | | | | | | | |

Vacasa, Inc.

Vacasa Holdings LLC

Robert W. Greyber

Chief Executive Officer

830 NW 13th Avenue

Portland, OR 97209

(503) 946-3650 | | | Casago Holdings, LLC

Vista Merger Sub II Inc.

Vista Merger Sub LLC

Casago Global, LLC

15475 N Greenway Hayden Loop, Suite B2

Scottsdale, AZ 85260

(877) 290-4447 | | | Roofstock, Inc.

2001 Broadway, 4th Floor

Oakland, CA 94612

(800) 466-4116 | | | MHRE STR II, LLC

4143 Maple Avenue,

Suite 300

Dallas, TX 75219

(214) 651-6220 | | | TRT Investors 37, LLC

4001 Maple Avenue,

Suite 600

Dallas, TX 75219

(214) 283-8500 |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | SLP V Venice Feeder I, L.P.

SLP Venice Holdings. L.P.

SLP V Aggregator GP, L.L.C.

Silver Lake Technology

Associates V, L.P.

SLTA V (GP), L.L.C.

Silver Lake Group, L.L.C.

c/o Silver Lake

55 Hudson Yards

550 West 34th Street,

40th Floor

New York, NY 10001

(212) 981-5600 | | | RW Vacasa AIV L.P.

RW Industrious Blocker L.P.

Riverwood Capital Partners II (Parallel-B) L.P.

RCP III Vacasa AIV L.P.

RCP III Blocker Feeder L.P.

Riverwood Capital Partners III

(Parallel-B) L.P.

RCP III (A) Blocker Feeder L.P.

RCP III (A) Vacasa AIV L.P.

c/o Riverwood Capital

70 Willow Road, Suite 100

Menlo Park, CA 94025

(650) 618-7300 | | | Level Equity Opportunities

Fund 2015, L.P.

Level Equity Opportunities

Fund 2018, L.P.

LEGP II AIV(B), L.P.

LEGP I VCS, LLC

LEGP II VCS, LLC

Level Equity – VCS Investors, LLC

c/o Level Equity Management, LLC

140 East 45th Street, 42nd Floor

New York, NY 10017

(212) 459-7225 | | | |

| | | | | | | | | | | | |

(Name, Address, and Telephone Numbers of Person Authorized to Receive Notices and Communications on Behalf of the Persons Filing Statement)

With copies to:

| | | | | | | | | | | | |

Lande A. Spottswood

D. Alex Robertson

Vinson & Elkins L.L.P.

845 Texas Avenue,

Suite 4700

Houston, TX 77002

(713) 758-2222

and

Justin Hamill

Michael Anastasio

Latham & Watkins LLP

1271 Avenue of the Americas

New York, NY 10020

(202) 906-1252 | | | Christopher M. Barlow

Skadden, Arps, Slate, Meagher & Flom LLP

One Manhattan West

New York, NY 10001

(212) 735-3000 | | | Steven Levine

Fenwick & West LLP

801 California Street

Mountain View,

CA 94041

(650) 335-7847 | | | David Lange

Winston & Strawn LLP

2121 N Pearl Street,

Suite 900

Dallas, TX 75201

(214) 453-6436 | | | David Lange

Winston & Strawn LLP

2121 N Pearl Street,

Suite 900

Dallas, TX 75201

(214) 453-6436 |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Eric Issadore

Ropes & Gray LLP

Three Embarcadero Center

San Francisco, CA 94111

(415) 315-1231 | | | Naveed Anwar

Simpson Thacher & Bartlett LLP

2475 Hanover Street

Palo Alto, CA 94304

(650) 251-5162 | | | Oreste Cipolla

Goodwin Procter LLP

The New York Times Building

620 Eighth Avenue

New York, NY 10018

(212) 459-7225 | | | |

This statement is filed in connection with (check the appropriate box):

| | | | | | | | | |

| | | a. | | | ☒ | | | The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. |

| | | b. | | | ☐ | | | The filing of a registration statement under the Securities Act of 1933. |

| | | c. | | | ☐ | | | A tender offer. |

| | | d. | | | ☐ | | | None of the above. |

| | | | | | | | | |

Check the following box if the soliciting materials or information statement referred to in checking box (a) are preliminary copies: ☒

Check the following box if the filing is a final amendment reporting the results of the transaction: ☐

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of this transaction, passed upon the merits or fairness of this transaction, or passed upon the adequacy or accuracy of the disclosure in this transaction statement on Schedule 13E-3. Any representation to the contrary is a criminal offense.

INTRODUCTION

This Transaction Statement on Schedule 13E-3 (this “Transaction Statement”) is being filed with the U.S. Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), jointly by the following persons (each, a “Filing Person,” and collectively, the “Filing Persons”): (1) Vacasa, Inc., a Delaware corporation (“Vacasa” or the “Company”) and the issuer of the Class A common stock, par value $0.00001 per share (the “Class A Common Stock”) that is the subject of the Rule 13e-3 transaction; (2) Vacasa Holdings LLC, a Delaware limited liability company (“Vacasa LLC”); (3) Casago Holdings, LLC, a Delaware limited liability company (“Parent”); (4) Vista Merger Sub II Inc., a Delaware corporation and a wholly owned subsidiary of Parent (“Company Merger Sub”); (5) Vista Merger Sub LLC, a Delaware limited liability company and a wholly owned subsidiary of Parent (“LLC Merger Sub” and, together with Company Merger Sub, “Merger Subs”); (6) Casago Global, LLC, a Delaware limited liability company; (7) Roofstock, Inc., a Delaware corporation; (8) TRT Investors 37, LLC, a Texas limited liability company; (9) MHRE STR II, LLC, a Delaware limited liability company; (10) SLP V Venice Feeder I, L.P., a Delaware limited partnership; (11) SLP Venice Holdings L.P., a Delaware limited partnership; (12) SLP V Aggregator GP, L.L.C., a Delaware limited liability company; (13) Silver Lake Technology Associates V, L.P., a Delaware limited partnership; (14) SLTA V (GP), L.L.C., a Delaware limited liability company; (15) Silver Lake Group, L.L.C., a Delaware limited liability company; (16) RW Vacasa AIV L.P., a Delaware limited partnership; (17) RW Industrious Blocker L.P., a Delaware limited partnership; (18) Riverwood Capital Partners II (Parallel - B) L.P., an Ontario limited partnership; (19) RCP III Vacasa AIV L.P., a Delaware limited partnership; (20) RCP III Blocker Feeder L.P., a Delaware limited partnership; (21) Riverwood Capital Partners III (Parallel - B) L.P., a Cayman Islands exempted limited partnership; (22) RCP III (A) Blocker Feeder L.P., a Delaware limited partnership; (23) RCP III (A) Vacasa AIV L.P., a Delaware limited partnership; (24) Level Equity Opportunities Fund 2015, L.P., a Delaware limited partnership; (25) Level Equity Opportunities Fund 2018, L.P., a Delaware limited partnership; (26) LEGP II AIV(B), L.P., a Delaware limited partnership; (27) LEGP I VCS, LLC, a Delaware limited liability company; (28) LEGP II VCS, LLC, a Delaware limited liability company; and (29) Level Equity-VCS Investors, LLC, a Delaware limited liability company (each of (10), (11) and (16) through (29), a “Rollover Stockholder”, and collectively, the “Rollover Stockholders”).

This Transaction Statement relates to the Agreement and Plan of Merger, dated as of December 30, 2024 (including all exhibits and documents attached thereto, and as it may be amended from time to time, the “Merger Agreement”), by and among Parent, Company Merger Sub, LLC Merger Sub, Vacasa LLC and the Company. The Merger Agreement provides that, subject to the terms and conditions set forth in the Merger Agreement and the applicable provisions of the General Corporation Law of the State of Delaware (the “DGCL”), (i) LLC Merger Sub will merge with and into Vacasa LLC (the “LLC Merger”), with Vacasa LLC surviving such merger as a subsidiary of Parent and (ii) immediately after the LLC Merger, Company Merger Sub will merge with and into Vacasa (the “Company Merger” and, together with the LLC Merger, the “Mergers”), with Vacasa surviving such merger as a wholly owned subsidiary of Parent and Vacasa LLC indirectly becoming a wholly owned subsidiary of Parent.

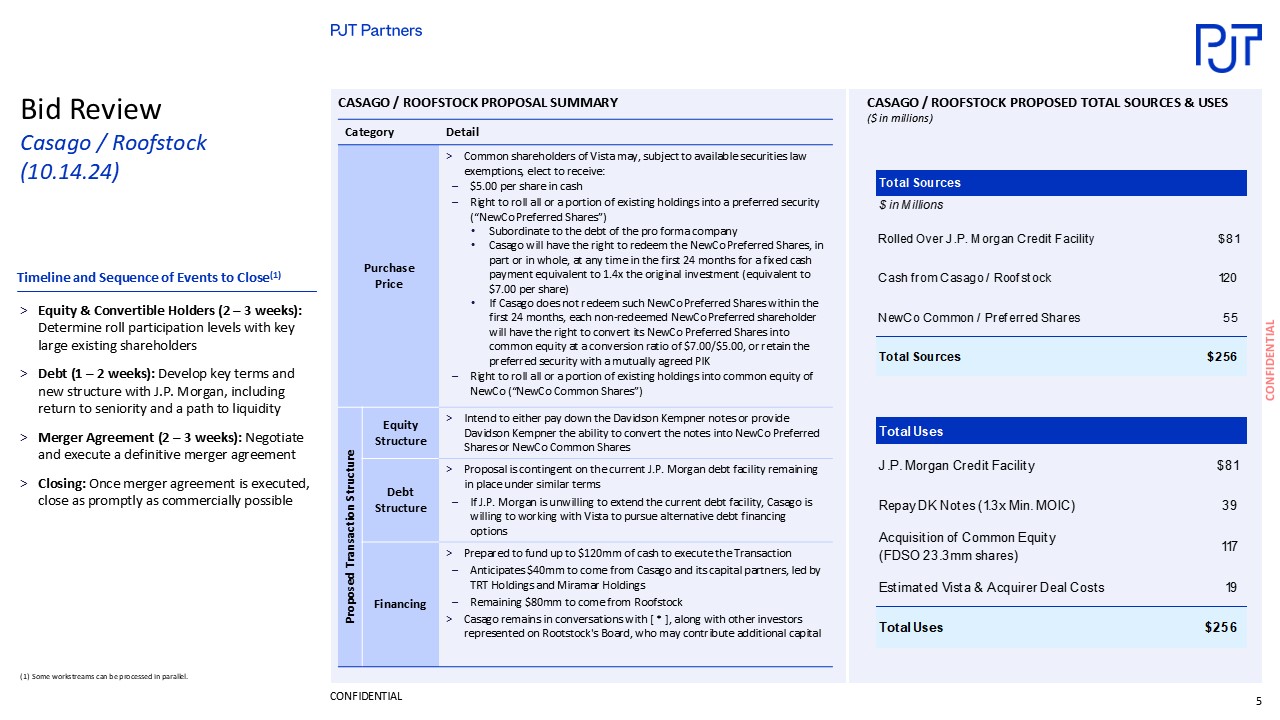

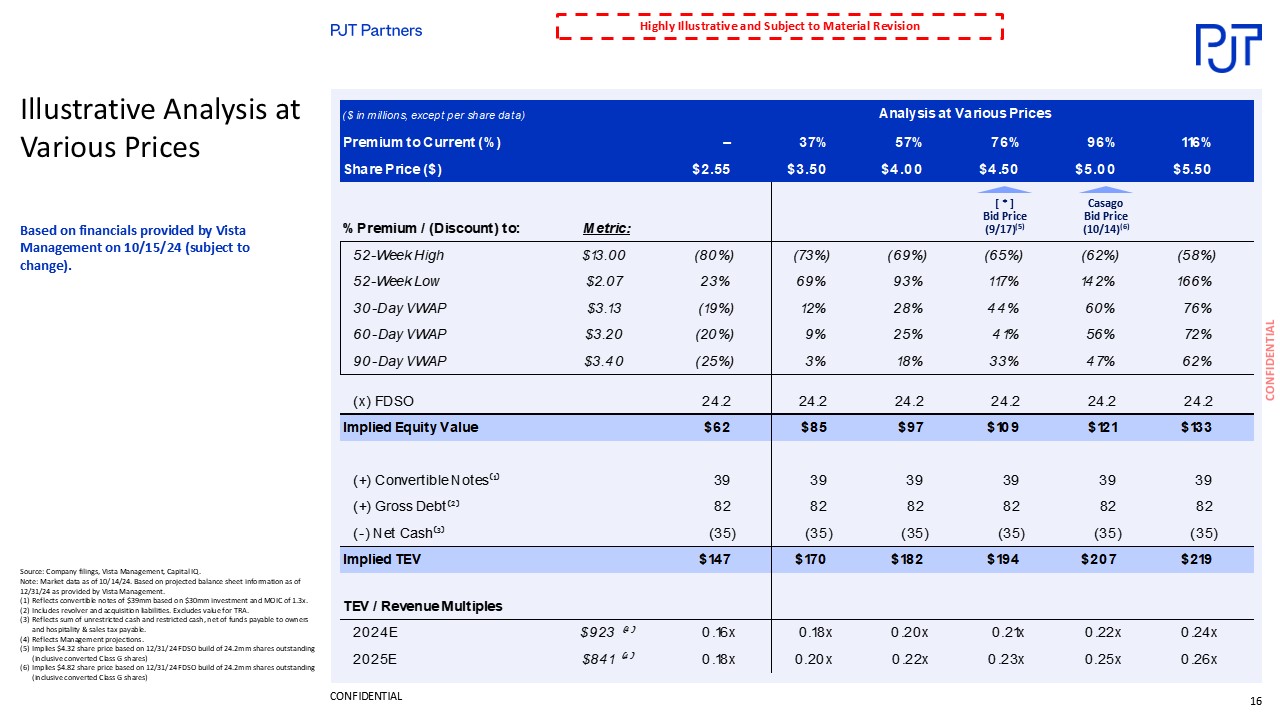

Upon the consummation of the Company Merger, on the terms and subject to the conditions set forth in the Merger Agreement, each share of Class A Common Stock issued and outstanding immediately prior to the effective time of the Company Merger (the “Company Merger Effective Time”) (other than certain excluded shares of Class A Common Stock and the Rollover Stock, but including each share of Class A Common Stock resulting from (i) the redemption of limited liability company units (other than the Class G limited liability company units) of Vacasa LLC (the “Common Units”) and (ii) the issuance of Class A Common Stock upon conversion of Class G Common Stock, par value $0.00001 per share, of Vacasa (“Class G Common Stock”)) will be converted into the right to receive $5.02 in cash, without interest, subject to potential downward adjustment in accordance with the terms and conditions set forth in the Merger Agreement (the “Merger Consideration”) after giving effect to any required withholding taxes. The Merger Consideration is subject to potential downward adjustment based on (i) the number of homes under management by Vacasa and its subsidiaries as of twelve business days prior to the anticipated closing date (the “Adjustment Measurement Date”) and (ii) Vacasa’s Liquidity (as defined in Vacasa’s Credit Agreement) as of the most recently available calculation of Liquidity within seven days of the Adjustment Measurement Date. Vacasa will issue a press release prior to the closing of the Mergers announcing the final Merger Consideration.

The Merger Consideration will not be paid in respect of (i) any shares of Class A Common Stock, Class B common stock, par value $0.00001 per share, of Vacasa (the “Class B Common Stock”) and Class G Common Stock held by Vacasa as treasury stock or owned by Parent or Merger Subs and any such shares owned by any direct or indirect wholly owned subsidiary of Parent or Merger Subs, in each case as of immediately prior to the Company Merger Effective Time (and excluding any Rollover Shares (as defined below)), which will cease to be outstanding, be automatically cancelled without payment of any consideration therefor or any conversion thereof and cease to exist, (ii) certain shares of Class A Common Stock held by the Rollover Stockholders (the “Rollover Shares”), which will be contributed to Parent immediately prior to the Vacasa LLC Units Redemption pursuant to the Support Agreements entered into in connection with the Merger Agreement (such contribution of Rollover Shares together with the contribution to Parent of certain Common Units (such contributed Common Units, the “Rollover Units”), the “Rollover”) and (iii) shares of Class A Common Stock held by holders who have not consented to the adoption of the Merger Agreement in writing and who have properly exercised appraisal rights with respect to their shares in accordance with, and who have complied with, Section 262 of the DGCL.

In connection with the Merger Agreement, MHRE STR II, LLC, TRT Investors 37, LLC and Roofstock, Inc. (the “Guarantors”) have delivered to Vacasa (i) a limited guarantee in favor of Vacasa and pursuant to which the Guarantors are guaranteeing certain obligations of Parent and Merger Subs in connection with the Merger Agreement and (ii) an executed equity commitment letter between Parent and the Guarantors pursuant to which the Guarantors have, together, committed to invest sufficient funds in Parent to finance a portion of the Merger Consideration.

The board of directors of Vacasa (the “Board”) formed a special committee of the Board comprised solely of disinterested and independent directors (the “Special Committee”), which, among other things, reviewed, evaluated and negotiated the Merger Agreement and the transactions contemplated by the Merger Agreement, including the Mergers, in consultation with its independent legal and financial advisors and, where appropriate, with Vacasa’s management and Vacasa’s legal advisors. The Special Committee, as more fully described in the accompanying Proxy Statement (as defined below), unanimously (i) determined that the Merger Agreement, the Support Agreements and the transactions contemplated thereby, including the Mergers, are fair to, and in the best interests of, Vacasa and the holders of Class A Common Stock, Class B Common Stock and Class G Common Stock (“Company Stock”) (in their capacity as such), excluding the Rollover Stockholders (collectively, the “Unaffiliated Stockholders”), (ii) recommended that the Board approve and declare advisable the Merger Agreement and the transactions contemplated thereby, including the Mergers, and determined that the Merger Agreement and the transactions contemplated thereby, including the Mergers, are fair to, and in the best interests of, Vacasa and the Unaffiliated Stockholders and (iii) recommended that, subject to Board approval, the Board submit the Merger Agreement to the stockholders of Vacasa for their adoption and recommend that the stockholders of Vacasa vote in favor of the adoption of the Merger Agreement.

The Board (acting on the unanimous recommendation of the Special Committee) has (i) determined that the Merger Agreement, the Support Agreements and the transactions contemplated by the Merger Agreement, including the Mergers, are fair to, and in the best interests of, Vacasa, the Unaffiliated Stockholders, Vacasa LLC and its members, (ii) approved and declared advisable the Merger Agreement and the transactions contemplated thereby, including the Mergers, (iii) authorized and approved the execution, delivery and performance by Vacasa and Vacasa LLC of the Merger Agreement and the consummation of transactions contemplated thereby, including the Mergers, upon the terms and subject to the conditions contained therein, (iv) directed that the adoption of the Merger Agreement be submitted to a vote of the stockholders of Vacasa at a meeting of the stockholders of Vacasa, and (v) recommended that the stockholders of Vacasa vote in favor of the adoption of the Merger Agreement.

Concurrently with the filing of this Transaction Statement, the Company is filing with the SEC a proxy statement (the “Proxy Statement”) under Regulation 14A of the Exchange Act, pursuant to which the Board is soliciting proxies from stockholders of the Company in connection with the Mergers. The Proxy Statement is attached hereto as Exhibit (a)(1). A copy of the Merger Agreement is attached to the Proxy Statement as Annex A and is incorporated herein by reference. As of the date hereof, the Proxy Statement is in preliminary form, and is subject to completion or amendment. Terms used but not defined in this Transaction Statement have the meanings assigned to them in the Proxy Statement.

Pursuant to General Instruction F to Schedule 13E-3, the information in the Proxy Statement, including all annexes thereto, is expressly incorporated by reference herein in its entirety, and responses to each item herein

are qualified in their entirety by the information contained in the Proxy Statement. The cross-references below are being supplied pursuant to General Instruction G to Schedule 13E-3 and show the location in the Proxy Statement of the information required to be included in response to the items of Schedule 13E-3.

While each of the Filing Persons acknowledges that the Mergers are a “going private” transaction for purposes of Rule 13e-3 under the Exchange Act, the filing of this Transaction Statement shall not be construed as an admission by any Filing Person, or by any affiliate of a Filing Person, that the Company is “controlled” by any of the Filing Persons and/or their respective affiliates.

The information concerning Vacasa contained in, or incorporated by reference into, this Transaction Statement and the Proxy Statement was supplied by Vacasa. Similarly, all information concerning each other Filing Person contained in, or incorporated by reference into, this Transaction Statement and the Proxy Statement was supplied by such Filing Person.

Item 1.

| Summary Term Sheet |

Regulation M-A Item 1001

The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

Item 2.

| Subject Company Information |

Regulation M-A Item 1002

(a) Name and address. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“The Parties to the Merger Agreement”

(b) Securities. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“The Special Meeting—Record Date; Shares Entitled to Vote; Quorum”

“Important Information Regarding Vacasa”

“Important Information Regarding Vacasa—Security Ownership of Certain Beneficial Owners and Management”

(c) Trading market and price. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Important Information Regarding Vacasa—Market Price of Vacasa Class A Common Stock”

(d) Dividends. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Important Information Regarding Vacasa—Dividends”

“The Merger Agreement—Conduct of Vacasa’s Business Pending the Mergers”

(e) Prior public offerings. The information set forth in the Proxy Statement under the following caption is incorporated herein by reference:

“Important Information Regarding Vacasa—Prior Public Offerings”

(f) Prior stock purchases. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Important Information Regarding Vacasa—Prior Public Offerings”

“Important Information Regarding Vacasa—Transactions in Vacasa Class A Common Stock”

“Important Information Regarding Vacasa—Past Contracts, Transactions, Negotiations and Agreements”

Item 3.

| Identity and Background of Filing Person |

Regulation M-A Item 1003

(a) — (c) Name and Address of Each Filing Person; Business and Background of Entities; Business and Background of Natural Persons. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary—The Parties to the Merger Agreement”

“The Parties to the Merger Agreement”

“Important Information Regarding Vacasa”

“Important Information Regarding the Filing Parties”

“Where You Can Find More Information”

Item 4. Terms of the Transaction

Regulation M-A Item 1004

(a)(1) Material terms. Tender offers. Not applicable

(a)(2) Mergers or Similar Transactions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Required Stockholder Approval for the Mergers”

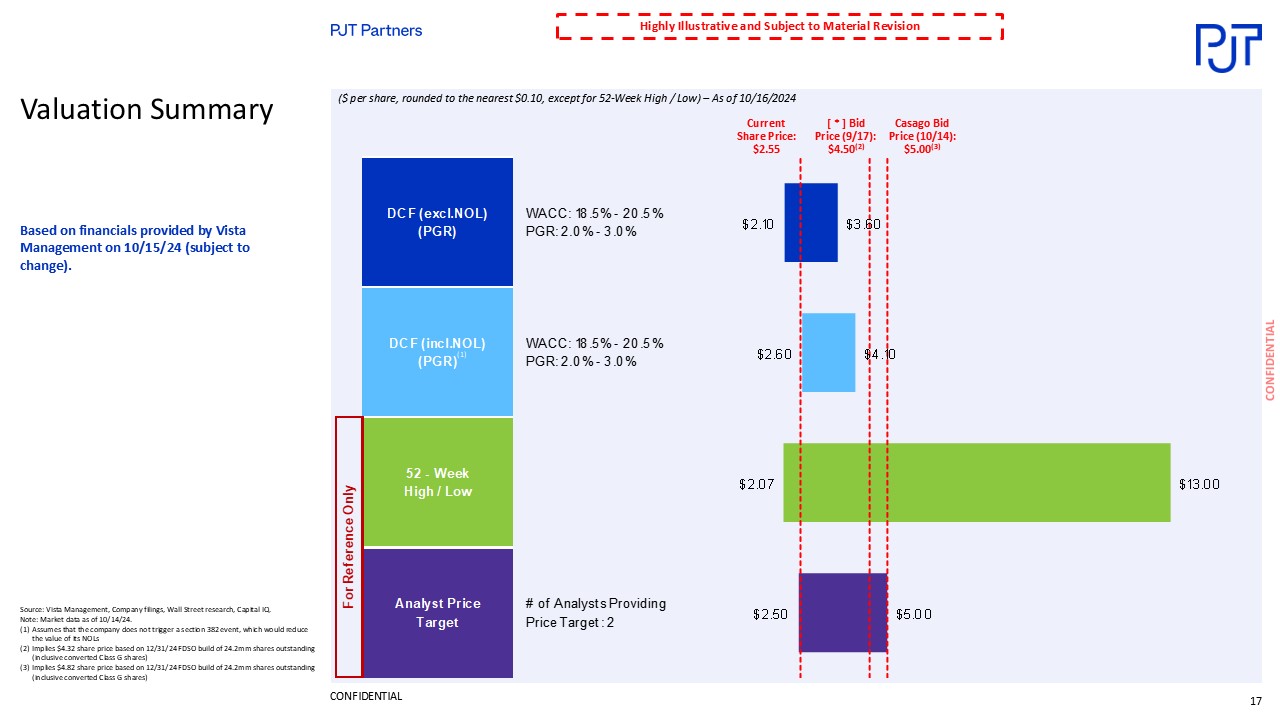

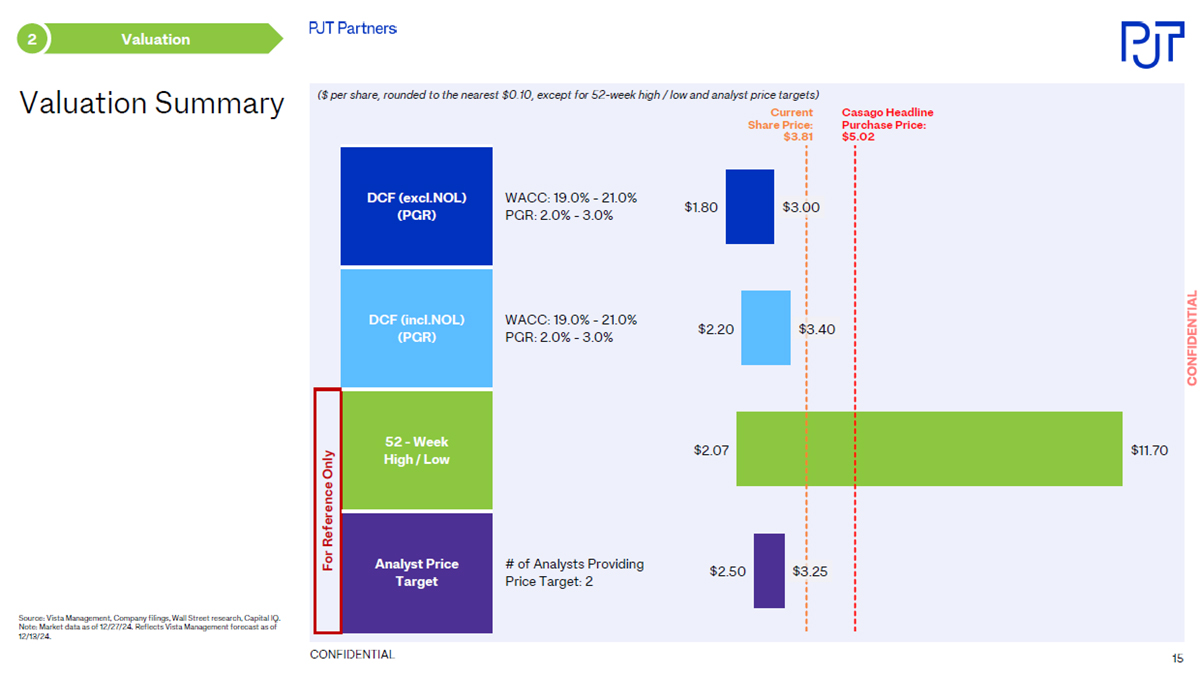

“Special Factors—Opinion of PJT Partners”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Plans for Vacasa After the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Certain Company Financial Forecasts”

“Special Factors—Anticipated Accounting Treatment”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Special Factors—Material U.S. Federal Income Tax Consequences of the Vacasa LLC Units Redemption and the Company Merger”

“The Special Meeting—Votes Required”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“The Merger Agreement—Merger Consideration Adjustment”

“The Merger Agreement—Merger Consideration Adjustment Procedures”

“The Merger Agreement—Surrender and Payment Procedures”

“The Merger Agreement—Stockholders Meeting”

“The Merger Agreement—Conditions to the Mergers”

Annex A—Agreement and Plan of Merger

Annex B—Opinion of PJT Partners

(c) Different terms. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“The Merger Agreement—Merger Consideration Adjustment”

“The Merger Agreement—Merger Consideration Adjustment Procedures”

“The Merger Agreement—Surrender and Payment Procedures”

“The Merger Agreement—Indemnification; Directors’ and Officers’ Insurance”

“Support Agreements”

“Tax Receivable Agreement Amendment”

Annex A—Agreement and Plan of Merger

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

Annex F—Amendment No. 1 to Tax Receivable Agreement

(d) Appraisal rights. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary—Appraisal Rights”

“Questions and Answers About the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Appraisal Rights”

(e) Provisions for unaffiliated security holders. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Provisions for Unaffiliated Security Holders”

(f) Eligibility for listing or trading. Not applicable.

Item 5.

| Past Contacts, Transactions, Negotiations and Agreements |

Regulation M-A Item 1005

(a)(1) - (2) Transactions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“Support Agreements”

“Tax Receivable Agreement Amendment”

“Important Information Regarding Vacasa—Prior Public Offerings”

“Important Information Regarding Vacasa—Transactions in Vacasa Class A Common Stock”

“Important Information Regarding Vacasa—Past Contracts, Transactions, Negotiations and Agreements”

“Important Information Regarding the Filing Parties”

Annex A—Agreement and Plan of Merger

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

Annex F—Amendment No. 1 to Tax Receivable Agreement

(b) - (c) Significant corporate events; Negotiations or contacts. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“The Merger Agreement”

“Support Agreements”

“Tax Receivable Agreement Amendment”

Annex A—Agreement and Plan of Merger

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

Annex F—Amendment No. 1 to Tax Receivable Agreement

(e) Agreements involving the subject company’s securities. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“The Merger Agreement”

“Support Agreements”

“Tax Receivable Agreement Amendment”

“Important Information Regarding Vacasa—Transactions in Vacasa Class A Common Stock”

“Important Information Regarding Vacasa—Past Contracts, Transactions, Negotiations and Agreements”

Annex A—Agreement and Plan of Merger

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

Annex F—Amendment No. 1 to Tax Receivable Agreement

Item 6.

| Purposes of the Transaction and Plans or Proposals |

Regulation M-A Item 1006

(b) Use of securities acquired. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Plans for Vacasa After the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“The Merger Agreement—Effects of the Mergers; Directors and Officers; Certificate of Incorporation; Bylaws”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“The Merger Agreement—Merger Consideration Adjustment”

“The Merger Agreement—Merger Consideration Adjustment Procedures”

“The Merger Agreement—Surrender and Payment Procedures”

“The Merger Agreement—Conduct of Vacasa’s Business Pending the Mergers”

Annex A—Agreement and Plan of Merger

(c)(1) - (8) Plans. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Purposes and Reasons of the Filing Parties for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Plans for Vacasa After the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“The Merger Agreement—Effects of the Mergers; Directors and Officers; Certificate of Incorporation; Bylaws”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“The Merger Agreement—Merger Consideration Adjustment”

“The Merger Agreement—Merger Consideration Adjustment Procedures”

“The Merger Agreement—Surrender and Payment Procedures”

“The Merger Agreement—Conduct of Vacasa’s Business Pending the Mergers”

“Support Agreements”

“Tax Receivable Agreement Amendment”

“Important Information Regarding Vacasa”

Annex A—Agreement and Plan of Merger

Item 7.

| Purposes, Alternatives, Reasons and Effects |

Regulation M-A Item 1013

(a) Purposes. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Purposes and Reasons of the Filing Parties for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Plans for Vacasa After the Mergers”

“Special Factors—Certain Effects of the Mergers”

(b) Alternatives. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Purposes and Reasons of the Filing Parties for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

(c) Reasons. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Purposes and Reasons of the Filing Parties for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Certain Company Financial Forecasts”

Annex B—Opinion of PJT Partners

(d) Effects. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Purposes and Reasons of the Filing Parties for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Plans for Vacasa After the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Special Factors—Fees and Expenses”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“Special Factors—Material U.S. Federal Income Tax Consequences of the Vacasa LLC Units Redemption and the Company Merger”

“The Merger Agreement—Effects of the Mergers; Directors and Officers; Certificate of Incorporation; Bylaws”

“The Merger Agreement—Treatment of Class A Common Stock and Class B Common Stock and Company Equity Awards”

“The Merger Agreement—Merger Consideration Adjustment”

“The Merger Agreement—Merger Consideration Adjustment Procedures”

“The Merger Agreement—Surrender and Payment Procedures”

“The Merger Agreement—Conduct of Vacasa’s Business Pending the Mergers”

“The Merger Agreement—Indemnification; Directors’ and Officers’ Insurance”

“Appraisal Rights”

Annex A—Agreement and Plan of Merger

Annex B—Opinion of PJT Partners

Item 8.

| Fairness of the Transaction |

Regulation M-A Item 1014

(a) - (b) Fairness; Factors considered in determining fairness. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Provisions for Unaffiliated Security Holders”

Annex B—Opinion of PJT Partners

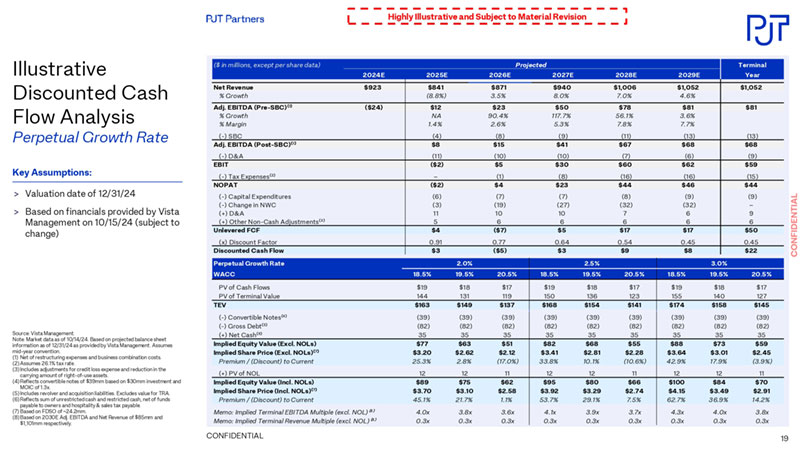

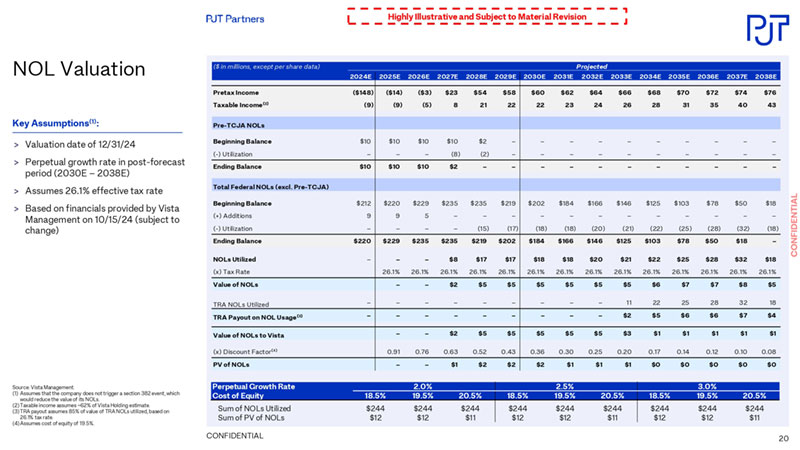

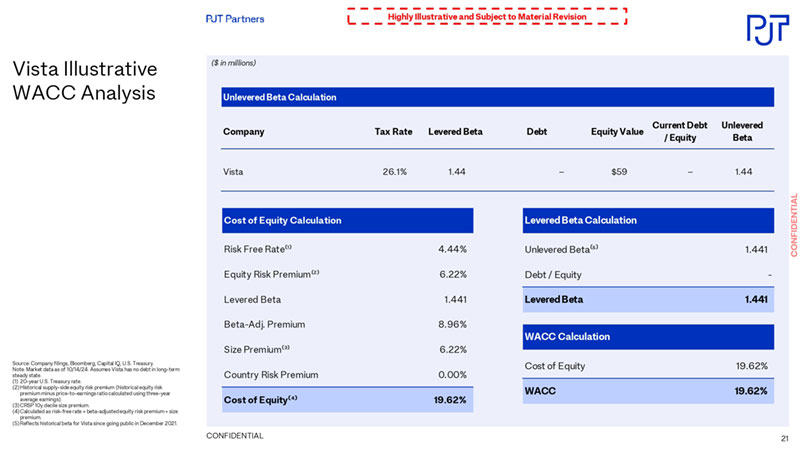

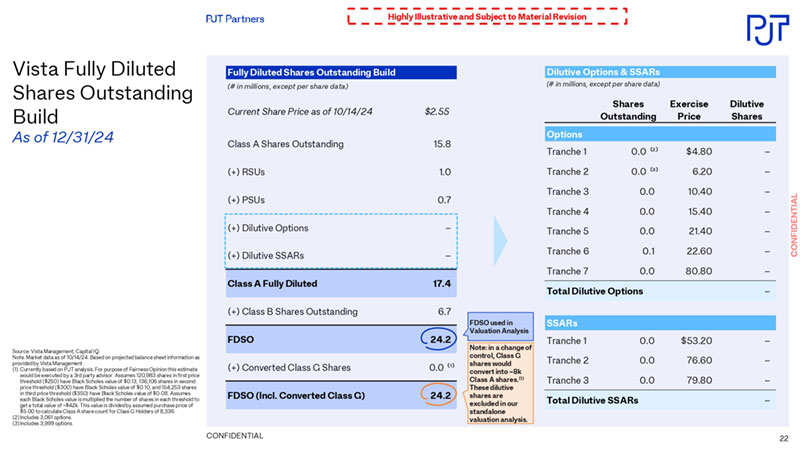

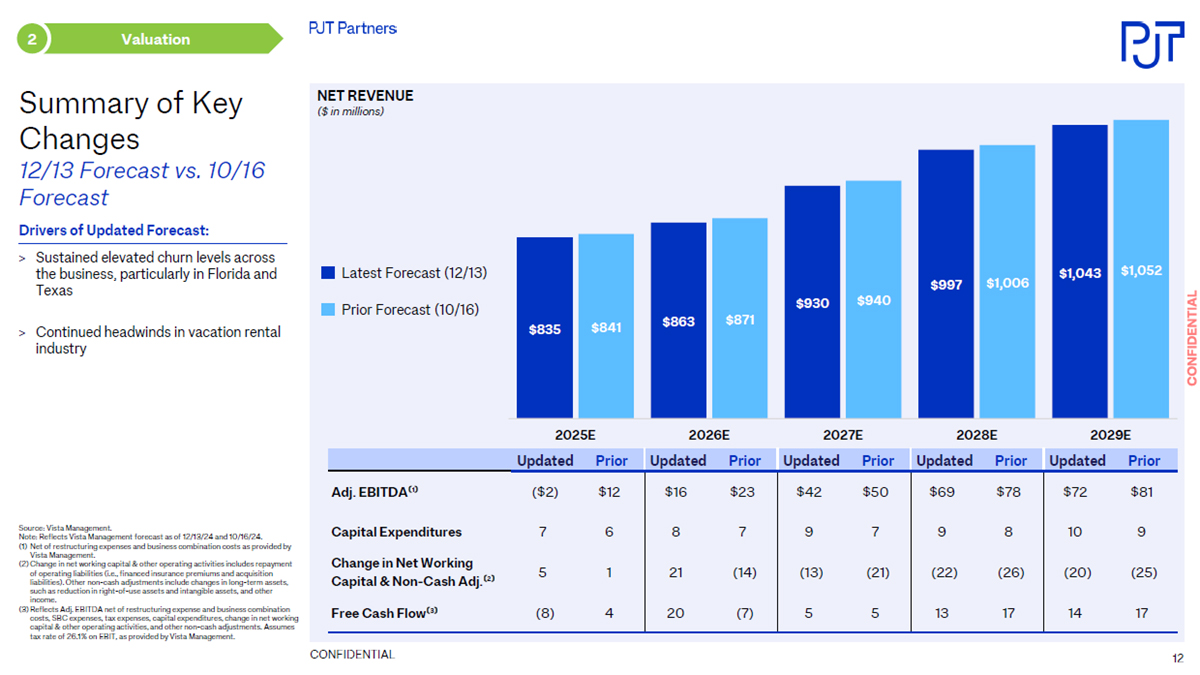

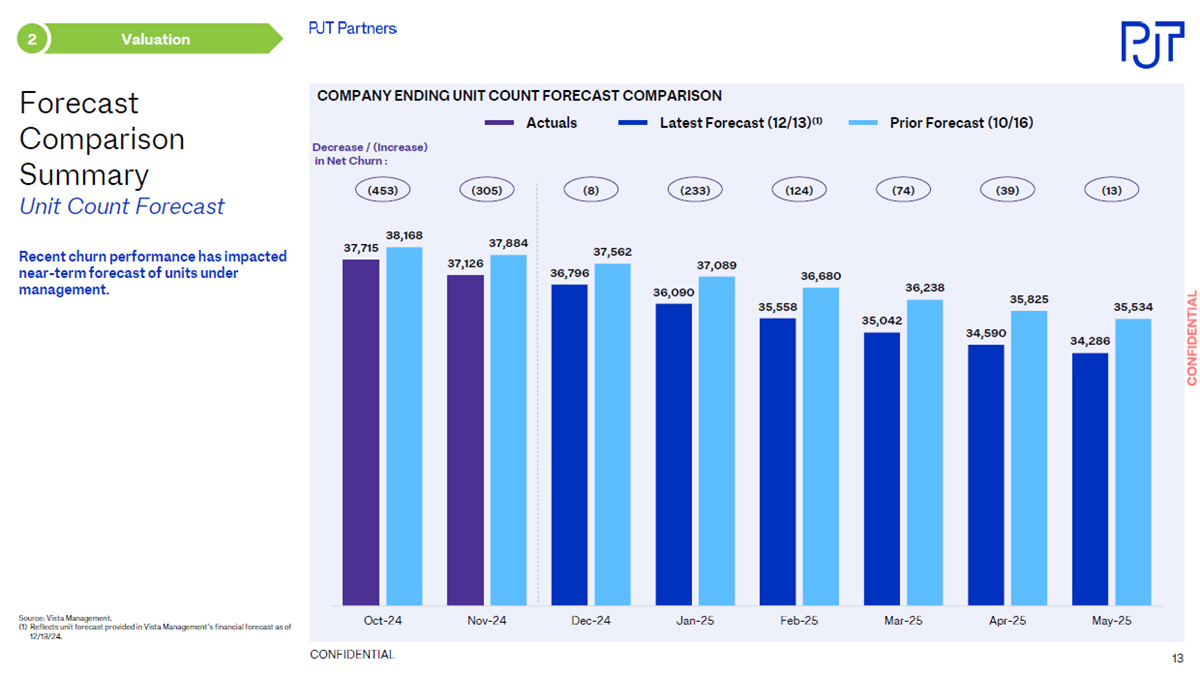

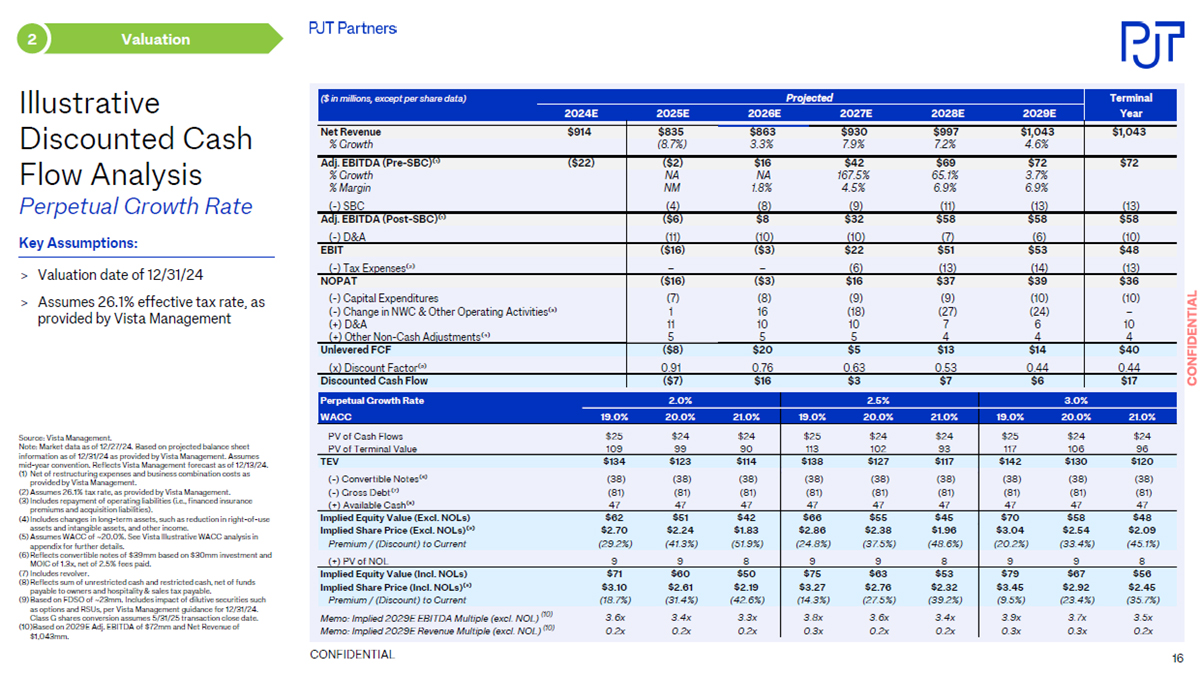

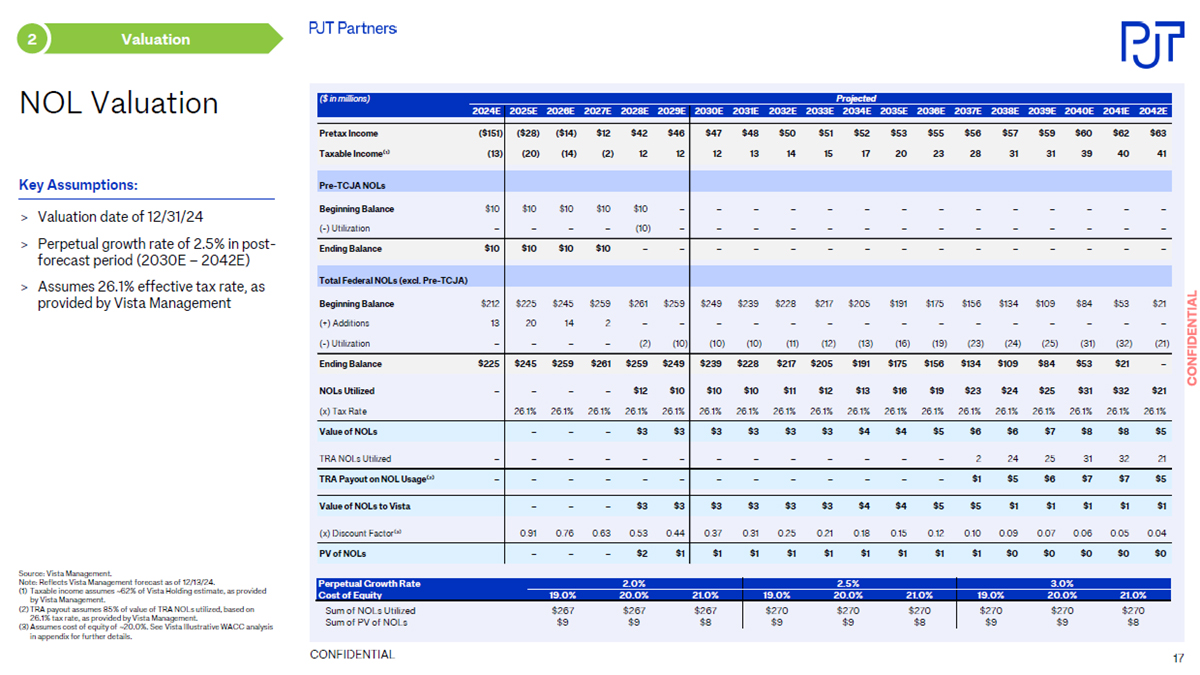

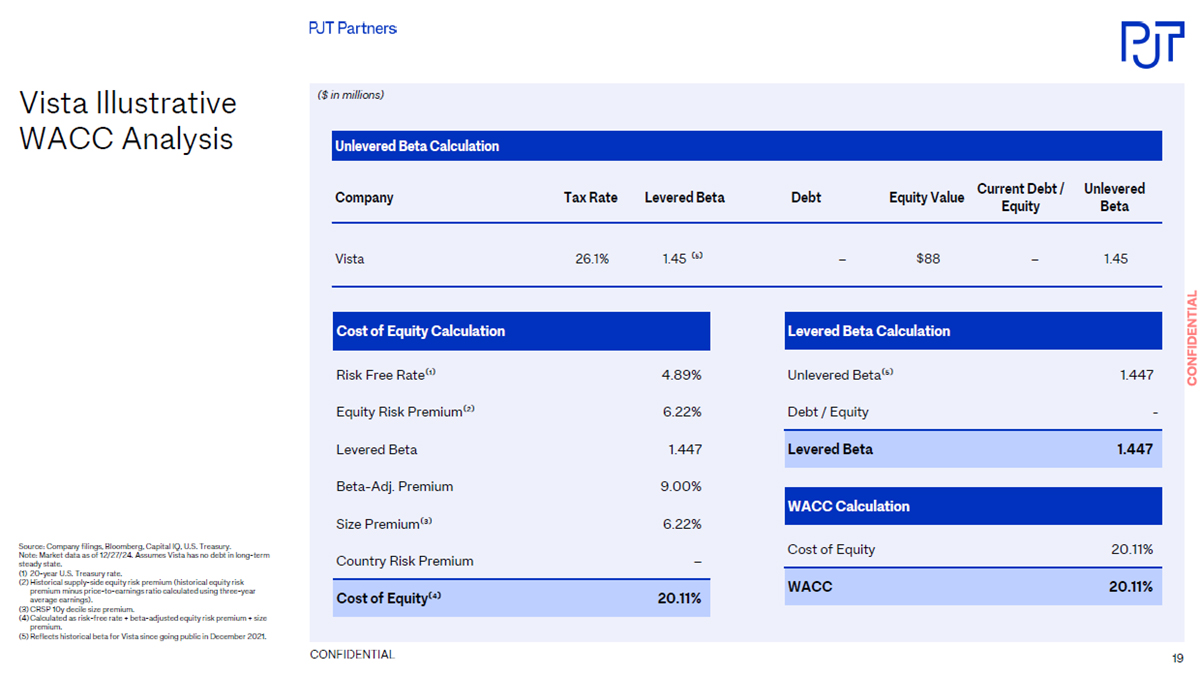

The discussion materials to the Special Committee dated October 17, 2024, November 5, 2024, December 8, 2024, December 9, 2024 and December 29, 2024, each prepared by PJT Partners and reviewed by the Special Committee, are filed as Exhibits (c)(ii) – (c)(vi) and are incorporated herein by reference.

(c) Approval of security holders. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Required Stockholder Approval for the Mergers”

“The Special Meeting—Votes Required”

“The Merger Agreement—Stockholders Meeting”

“The Merger Agreement—Conditions to the Mergers”

Annex A—Agreement and Plan of Merger

(d) Unaffiliated representative. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Provisions for Unaffiliated Security Holders”

(e) Approval of directors. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Position the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Proposal 1: The Merger Proposal”

(f) Other offers. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

Item 9.

| Reports, Opinions, Appraisals and Negotiations |

Regulation M-A Item 1015

(a) - (b) Report, opinion or appraisal; Preparer and summary of the report, opinion or appraisal. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Opinion of PJT Partners”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Where You Can Find More Information”

Annex B—Opinion of PJT Partners

The discussion materials to the Special Committee dated October 17, 2024, November 5, 2024, December 8, 2024, December 9, 2024 and December 29, 2024, each prepared by PJT Partners and reviewed by the Special Committee, are filed as Exhibits (c)(ii) – (c)(vi) and are incorporated herein by reference.

(c) Availability of documents. The reports, opinions or appraisals referenced in this Item 9 will be made available for inspection and copying at the principal executive offices of the Company during its regular business hours by any interested equity holder of the Company or by a representative who has been so designated in writing.

Item 10.

| Source and Amounts of Funds or Other Consideration |

Regulation M-A Item 1007

(a) - (b), (d) Source of funds; Conditions; Borrowed funds. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Financing”

“The Merger Agreement—Conduct of Vacasa’s Business Pending the Mergers”

“The Merger Agreement—Conditions to the Mergers”

“The Merger Agreement—Equity Financing”

Annex A—Agreement and Plan of Merger

Equity Commitment Letter, dated as of December 30, 2024, from Roofstock, Inc., MHRE STR II, LLC and TRT Investors 37, LLC, is attached hereto as Exhibit (b)(i) and is incorporated herein by reference.

(c) Expenses. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Certain Effects on the Company if the Mergers are Not Completed”

“Special Factors—Fees and Expenses”

“Special Factors—Opinion of PJT Partners”

“The Merger Agreement—Company Termination Fee”

“The Merger Agreement—Parent Termination Fee”

“The Merger Agreement—Expenses”

“The Special Meeting—Solicitation of Proxies”

Annex A—Agreement and Plan of Merger

Annex B—Opinion of PJT Partners

Item 11.

| Interest in Securities of the Subject Company |

Regulation M-A Item 1008

(a) Securities ownership. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Support Agreements”

“Important Information Regarding Vacasa”

“Important Information Regarding Vacasa—Security Ownership of Certain Beneficial Owners and Management”

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

(b) Securities transactions. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Background of the Mergers”

“The Merger Agreement”

“Support Agreements”

“Important Information Regarding Vacasa—Prior Public Offerings”

“Important Information Regarding Vacasa—Transactions in Vacasa Class A Common Stock”

Annex A—Agreement and Plan of Merger

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

Item 12.

| The Solicitation or Recommendation |

Regulation M-A Item 1012

(d) Intent to tender or vote in a going-private transaction. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Intent of Vacasa’a Directors and Executive Officers to Vote in Favor of the Mergers”

“Support Agreements”

“The Merger Agreement—Vote of the Rollover Stockholders”

Annex C—Silver Lake Support Agreement

Annex D—Riverwood Support Agreement

Annex E—Level Equity Support Agreement

(e) Recommendation of others. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

Item 13.

| Financial Statements |

Regulation M-A Item 1010

(a) Financial information. The audited consolidated financial statements set forth in Item 8 of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 are incorporated herein by reference. The unaudited condensed consolidated financial statements set forth in Item 1 of the Company Quarterly Report on Form 10-Q for the fiscal quarter ended September 30, 2024 are incorporated herein by reference.

The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Special Factors—Certain Effects of the Mergers”

“Special Factors—Certain Company Financial Forecasts”

“Important Information Regarding Vacasa—Book Value Per Share”

“Where You Can Find More Information”

(b) Pro forma information. Not applicable.

Item 14.

| Persons/Assets, Retained, Employed, Compensated or Used |

Regulation M-A Item 1009

(a) - (b) Solicitations or recommendations; Employees and corporate assets. The information set forth in the Proxy Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Mergers”

“Special Factors—Background of the Mergers”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Mergers”

“Special Factors—Position of the Purchaser Filing Parties as to the Fairness of the Mergers”

“Special Factors—Position of the Rollover Filing Parties as to the Fairness of the Mergers”

“Special Factors—Interests of Our Directors and Executive Officers in the Mergers”

“Special Factors—Fees and Expenses”

“The Special Meeting—Solicitation of Proxies”

Item 15.

| Additional Information |

Regulation M-A Item 1011

(b) Golden Parachute Compensation. Not applicable.

(c) Other material information. The information set forth in the Proxy Statement, including all annexes thereto, is incorporated herein by reference.

Regulation M-A Item 1016

The following exhibits are filed herewith:

| | | |

| | | Preliminary Proxy Statement of Vacasa, Inc. (included in the Schedule 14A filed on January 31, 2025 and incorporated herein by reference). |

| | | Form of Proxy Card (included in the Proxy Statement and incorporated herein by reference). |

| | | Letter to Stockholders (included in the Proxy Statement and incorporated herein by reference). |

| | | Notice of Special Meeting of Stockholders (included in the Proxy Statement and incorporated herein by reference). |

| | | Press Release announcing the Proposed Transaction (included in Schedule 14A filed on December 30, 2024 and incorporated herein by reference). |

| | | Email to Employees (included in Schedule 14A filed on December 30, 2024 and incorporated herein by reference). |

| | | Frequently Asked Questions for Employees (included in Schedule 14A filed on December 30, 2024 and incorporated herein by reference). |

| | | Current Report on Form 8-K, dated December 31, 2024 (included in Schedule 14A filed on December 31, 2024 and incorporated herein by reference). |

| | | Equity Commitment Letter, dated as of December 30, 2024, entered into by Roofstock, Inc., MHRE STR II, LLC, and TRT Investors 37, LLC. |

| | | Limited Guarantee, dated as of December 30, 2024, entered into by Roofstock, Inc., MHRE STR II, LLC, and TRT Investors 37, LLC in favor of Vacasa, Inc. |

| | | Opinion of PJT Partners LP, dated December 30, 2024 (included as Annex B to the Proxy Statement and incorporated herein by reference). |

| | | Discussion materials to the Special Committee, dated October 17, 2024, prepared by PJT Partners LP and reviewed by the Special Committee. |

| | | Discussion materials to the Special Committee, dated November 5, 2024, prepared by PJT Partners LP and reviewed by the Special Committee. |

| | | Discussion materials to the Special Committee, dated December 8, 2024, prepared by PJT Partners LP and reviewed by the Special Committee. |

| | | Discussion materials to the Special Committee, dated December 9, 2024, prepared by PJT Partners LP and reviewed by the Special Committee. |

| | | Discussion materials to the Special Committee, dated December 29, 2024, prepared by PJT Partners LP and reviewed by the Special Committee. |

| | | Agreement and Plan of Merger, dated as of December 30, 2024, by and among Casago Holdings, LLC, Vista Merger Sub II Inc., Vista Merger Sub LLC, Vacasa Holdings LLC and Vacasa, Inc. (included as Annex A to the Proxy Statement and incorporated herein by reference). |

| | | Support Agreement, dated as of December 30, 2024, by and among SLP V Venice Feeder I, L.P., SLP Venice Holdings, L.P., Casago Holdings, LLC and Vacasa, Inc. (included as Annex C to the Proxy Statement and incorporated herein by reference). |

| | | Support Agreement, dated as of December 30, 2024, by and among RW Vacasa AIV L.P., RW Industrious Blocker L.P., RCP III Vacasa AIV L.P., Riverwood Capital Partners II (Parallel-B) L.P., Riverwood Capital Partners III (Parallel-B) L.P., RCP III (A) Vacasa AIV L.P., RCP III Blocker Feeder L.P., RCP III (A) Blocker Feeder L.P., Casago Holdings, LLC and Vacasa, Inc. (included as Annex D to the Proxy Statement and incorporated herein by reference). |

| | | Support Agreement, dated as of December 30, 2024, by and among Level Equity Opportunities Fund 2015, L.P., Level Equity Opportunities Fund 2018, L.P., LEGP II AIV(B), L.P., LEGP I VCS, LLC, LEGP II VCS, LLC, Level Equity – VCS Investors, LLC, Casago Holdings, LLC and Vacasa, Inc. (included as Annex E to the Proxy Statement and incorporated herein by reference). |

| | | Amendment No. 1 to the Tax Receivable Agreement, dated as of December 30, 2024, by and among Vacasa, Inc., Vacasa Holdings LLC, SLP Venice Holdings, L.P. and the Holders parties thereto (included as Annex F to the Proxy Statement and incorporated herein by reference). |

| | | |

| | | |

| | | Interim Investors Agreement, dated as of December 30, 2024, by and among Casago Global, LLC, Casago Holdings, LLC, the Rollover Stockholders and the other parties appearing on the signature pages thereto and any person that executes a joinder thereto in such capacity in accordance with the terms thereof. |

| | | Section 262 of the Delaware General Corporation Law. |

(g) | | | None. |

| | | Filing Fee Table. |

| | | |

*

| Certain portions of this exhibit marked with “[*]” have been redacted and separately filed with the Securities and Exchange Commission pursuant to a request for confidential treatment. |

SIGNATURES

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | VACASA, INC. |

| | | | | | | | | |

| | | By: | | | /s/ Robert W. Greyber |

| | | | | | Name: | | | Robert W. Greyber |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

| | | |

| | | VACASA HOLDINGS LLC |

| | | | | | | | | |

| | | By: | | | /s/ Robert W. Greyber |

| | | | | | Name: | | | Robert W. Greyber |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | CASAGO HOLDINGS, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Steve Schwab |

| | | | | | Name: | | | Steve Schwab |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

| | | |

| | | VISTA MERGER SUB II INC. |

| | | | | | | | | |

| | | By: | | | /s/ Steve Schwab |

| | | | | | Name: | | | Steve Schwab |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

| | | |

| | | VISTA MERGER SUB LLC |

| | | | | | | | | |

| | | By: | | | /s/ Steve Schwab |

| | | | | | Name: | | | Steve Schwab |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

| | | |

| | | CASAGO GLOBAL, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Steve Schwab |

| | | | | | Name: | | | Steve Schwab |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | ROOFSTOCK, INC. |

| | | | | | | | | |

| | | By: | | | /s/ Gary Beasley |

| | | | | | Name: | | | Gary Beasley |

| | | | | | Title: | | | Chief Executive Officer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | MHRE STR II, LLC |

| | | | | | | | | |

| | | By: | | | MHRE Partners, LP,

a Delaware limited partnership |

| | | | | | | |

| | | By: | | | MHRE Partners GP, LLC,

a Delaware limited liability company

its General Partner |

| | | | | | | | | |

| | | By: | | | /s/ Randy P. Evans |

| | | | | | Name: | | | Randy P. Evans |

| | | | | | Title: | | | Vice President and Treasurer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | TRT INVESTORS 37, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Paul A. Jorge |

| | | | | | Name: | | | Paul A. Jorge |

| | | | | | Title: | | | Vice President and Secretary |

| | | | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | | |

| | | SLP V VENICE FEEDER I, L.P. | |

| | | | | | | |

| | | By: | | | Silver Lake Technology Associates V, L.P., its general partner | |

| | | By: | | | SLTA V (GP), L.L.C., its general partner | |

| | | By: | | | Silver Lake Group, L.L.C., its managing member | |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

| | | SLP VENICE HOLDINGS, L.P. | |

| | | | | | | |

| | | By: | | | SLP V Aggregator GP, L.L.C. |

| | | By: | | | Silver Lake Technology Associates V, L.P.,

its general partner |

| | | By: | | | SLTA V (GP), L.L.C., its general partner |

| | | By: | | | Silver Lake Group, L.L.C., its managing member |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

| | | SLP V AGGREGATOR GP, L.L.C. | |

| | | | | | | |

| | | By: | | | Silver Lake Technology Associates V, |

| | | | | | L.P., its managing member | |

| | | By: | | | SLTA V (GP), L.L.C., its general partner | |

| | | By: | | | Silver Lake Group, L.L.C., its managing member | |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

| | | SILVER LAKE TECHNOLOGY

ASSOCIATES V, L.P. | |

| | | | | | | |

| | | By: | | | SLTA V (GP), L.L.C., its general partner | |

| | | By: | | | Silver Lake Group, L.L.C., its managing member | |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

| | | SLTA V (GP), L.L.C. | |

| | | | | | | |

| | | By: | | | Silver Lake Group, L.L.C., its managing member | |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

| | | SILVER LAKE GROUP, L.L.C. | |

| | | | | | | |

| | | By: | | | /s/ Joerg Adams | |

| | | Name: | | | Joerg Adams | |

| | | Title: | | | Managing Director | |

| | | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | | |

| | | RW INDUSTRIOUS BLOCKER L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital II L.P., its general partner |

| | | By: | | | Riverwood Capital GP II Ltd., its general partner | |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | RW VACASA AIV L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital II L.P., its general partner |

| | | By: | | | Riverwood Capital GP II Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | RIVERWOOD CAPITAL PARTNERS II (PARALLEL-B) L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital II L.P., its general partner |

| | | By: | | | Riverwood Capital GP II Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | RIVERWOOD CAPITAL II L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital GP II Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | RIVERWOOD CAPITAL GP II LTD. | |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | RCP III (A) BLOCKER FEEDER L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital III L.P., its general partner |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

[Signature Page to SC 13E-3]

| | | | |

| | | RCP III BLOCKER FEEDER L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital III L.P., its general partner |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | | |

| | | RCP III VACASA AIV L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital III L.P., its general partner |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | | |

| | | RCP III (A) VACASA AIV L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital III L.P., its general partner |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | | |

| | | RIVERWOOD CAPITAL PARTNERS III (PARALLEL-B) L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital III L.P., its general partner |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | | |

| | | RIVERWOOD CAPITAL III L.P. | |

| | | | | | | |

| | | By: | | | Riverwood Capital GP III Ltd., its general partner |

| | | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks | |

| | | Name: | | | Jeffrey T. Parks | |

| | | Title: | | | Director | |

| | | | | | | |

| | | |

| | | RIVERWOOD CAPITAL GP III LTD. |

| | | | | | |

| | | By: | | | /s/ Jeffrey T. Parks |

| | | Name: | | | Jeffrey T. Parks |

| | | Title: | | | Director |

| | | | | | |

[Signature Page to SC 13E-3]

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in this statement is true, complete and correct.

Dated as of January 31, 2025

| | | |

| | | LEVEL EQUITY OPPORTUNITIES

FUND 2015, L.P. |

| | | | | | | | | |

| | | By: | | | Level Equity Partners II (GP), L.P.

its general partner |

| | | By: | | | Level Equity Associates II, LLC

its general partner |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

| | | LEVEL EQUITY OPPORTUNITIES

FUND 2018, L.P. |

| | | | | | | | | |

| | | By: | | | Level Equity Partners IV (GP), L.P.

its general partner |

| | | By: | | | Level Equity Associates IV, LLC

its general partner |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

| | | LEGP II AIV(B), L.P. |

| | | | | | | | | |

| | | By: | | | Level Equity Partners II (GP), L.P.

its general partner |

| | | By: | | | Level Equity Associates II, LLC

its general partner |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

| | | LEGP I VCS, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

| | | LEGP II VCS, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

| | | |

| | | LEVEL EQUITY – VCS INVESTORS, LLC |

| | | | | | | | | |

| | | By: | | | /s/ Nathan Linn |

| | | | | | Name: | | | Nathan Linn |

| | | | | | Title: | | | Chief Operating Officer |

| | | | | | | | | |

[Signature Page to SC 13E-3]

Exhibit (b)(i)

December 30, 2024

Casago Holdings, LLC

15475 N Greenway Hayden Loop, Suite B2

Scottsdale, AZ 85260-1616

Attention: Joseph Riley

Email: joseph@patriotfamilyhomes.com

Re: Equity Financing Commitment

Ladies and Gentlemen:

Reference is made to the Agreement and Plan of Merger, dated as of the date hereof (as amended, restated, supplemented or otherwise modified from time to time, the “

Agreement”),

by and among Casago Holdings, LLC, a Delaware limited liability company (“

Parent”),

Vista Merger Sub II Inc., a Delaware corporation and wholly owned Subsidiary of Parent (“

Company Merger Sub”), Vista Merger

Sub LLC, a Delaware limited liability company and wholly owned Subsidiary of Parent (“

LLC Merger Sub” and collectively with Company Merger Sub, “

Merger Subs”), Vacasa, Inc., a Delaware corporation (the “

Company”) and Vacasa

Holdings LLC, a Delaware limited liability company (“

Company LLC”). Capitalized terms used and not defined herein but defined in the Agreement shall have the meanings ascribed to them in the Agreement. This letter is

being

delivered by each of the undersigned “Equity Investors” set forth on

Annex A hereto (each, an “

Equity Investor”) to Parent in connection with the execution of the Agreement.

1.

Commitment.

This letter confirms the

irrevocable commitment of each Equity Investor, on a several (and not joint or joint and several) basis, subject to the conditions set forth herein, to purchase (or cause an assignee permitted by the terms of

Section 4(a) hereof to purchase) at

the Closing (if and when such Closing is required to occur under Section 1.3 of the Agreement), directly or indirectly, equity of Parent (such equity of Parent, the “

Subject Equity Securities”) for a cash amount equal to the “

Commitment

Amount” set forth opposite such Equity Investor’s name on

Annex A hereto (each such amount, as may be reduced pursuant to the penultimate sentence of this

Section 1, an “

Equity Financing Commitment” and the aggregate Equity

Financing Commitments, the “

Aggregate Equity Financing Commitment”), solely for the purpose of Parent funding the payment of, together with the proceeds of the Rollover, (i) the aggregate consideration required to be paid by Parent at the

Closing under the Agreement (including the payments required to be made by Parent under Section 4.2 and Section 4.7 of the Agreement), and (ii) all fees and expenses required to be paid by Parent at the Closing or thereafter under the Agreement in

connection with the transactions contemplated by the Agreement, in each case, if and only to the extent required to be funded by Parent at or prior to the Closing pursuant to the Agreement (collectively, the “

Required Parent Payments”) and not

for any other purpose;

provided that to the extent an Equity Investor syndicates or otherwise assigns a portion of its Equity Financing Commitment in accordance with

Section 4(a), its Equity Financing Commitment shall be proportionally

reduced by the portion of such Equity Financing Commitment syndicated or assigned to such assignee.

Notwithstanding anything to the contrary in this letter, the Equity Investors may change each Equity Investor’s Equity

Financing Commitment without the consent of any other party hereto (other than the Equity Investor whose Equity Financing Commitment is to be changed);

provided that the sum of the Equity Investors’ Equity Financing Commitments shall remain, in

the aggregate, equal to the Aggregate Equity Financing Commitment and any such change shall not relieve any Equity Investor of its obligations under this letter (including with respect to such Equity Investor’s Equity Financing Commitment) nor

reasonably be expected to impede or delay the Mergers. The parties hereto understand and agree that (A) no Equity Investor (together with its permitted assigns) shall under any circumstances be obligated to purchase any equity or debt securities of, or

make any other payment to or investment in, Parent or any other Person, other than the purchase of the Subject Equity Securities pursuant to the terms hereof for an aggregate purchase price equal to such Equity Investor’s Equity Financing Commitment,

and (B) the funding of each Equity Financing Commitment will occur contemporaneously with or immediately prior to the Closing.

The obligation of each Equity Investor (together with its permitted assigns) to fund such Equity

Investor’s Equity Financing Commitment at the Closing is subject to the terms of this letter and each of the following conditions: (1) the satisfaction or waiver by Parent, and the continued satisfaction or waiver by Parent, of all of the conditions to

Parent’s obligations to effect the Closing set forth in Article VII of the Agreement (other than those conditions that by their nature are to be satisfied at the Closing, each of which is capable of being satisfied) and Parent otherwise being required

to consummate the Closing pursuant to the terms of the Agreement and (2) the prior or substantially contemporaneous contribution of each of the Rollover Stockholders that has entered into a Support Agreement of all of such Rollover Stockholder’s

Rollover Equity to Parent (or any direct or indirect parent entity thereof), in each case, as specified in such Rollover Stockholder’s Support Agreement. The amount to be funded under this letter will be reduced in the manner designated by

Parent only to the extent that

Parent does not require all of the equity financing contemplated by the Aggregate Equity Financing Commitment (whether as a result of proceeds of the Rollover or

otherwise) in order to consummate the transactions contemplated by the Agreement and fulfill all of its payment obligations thereunder;

provided, that any such reduction shall be applied pro rata across all Commitment Amounts. Notwithstanding

anything to the contrary herein, in no event shall any Equity Investor be obligated to (x) fund such Equity Investor’s Equity Financing Commitment at any time hereunder unless each of the conditions set forth in this

Section 1 is satisfied and

(y) contribute to, purchase or otherwise provide funds to Parent (or otherwise) in an amount (in the aggregate) in excess of such Equity Investor’s Equity Financing Commitment.

2.

Termination. This letter and the Equity Investors’ obligation to fund all or any portion of such Equity Investor’s Equity

Financing Commitment will terminate automatically and immediately upon the earliest to occur of:

(a) the valid termination of the Agreement in accordance with its terms;

(b) the consummation of the Closing or, if later, the final determination of the Adjusted Merger Consideration, but only upon the payment in full

of all Required Parent Payments; and

(c) without limiting any rights of Parent under the Agreement, the assertion in writing in any claim, litigation or other similar formal

proceeding, by the Company or any of its Affiliates or representatives of any claim, action, complaint, suit, demand, request for relief or proceeding of any nature (whether in equity, tort, contract or otherwise)

(collectively, a “Proceeding”) against any Equity Investor, Parent or any other Parent Related Party (as defined below) in connection with or relating to this letter, the Guarantee by the Equity Investors in favor of the Company, dated as of

the date hereof (the “Guarantee”), the Agreement or any of the transactions contemplated hereby or thereby (including in respect of any oral representations made or alleged to be made in connection therewith) other than a Proceeding only

asserting Non-Prohibited Claims (as defined below); provided, that, any such termination pursuant to this clause (c) shall only be effective if, prior to any such termination, Parent has first delivered a written notice to the Company

pursuant to Section 15 requesting that such claim be withdrawn, dismissed or amended either (at the election of Parent) to remove such claim or remove Parent, any Equity Investor or any Parent Related Party (as applicable) and such claim is

not irrevocably and unconditionally withdrawn, dismissed or amended to remove such claim or remove Parent, any Equity Investor or any Parent Related Party (as applicable) within five (5) Business Days after

such written notice is delivered.

Upon termination of this letter pursuant to this Section 2 and except as set forth in the Guarantee, neither the Equity Investors nor any of their respective representatives or

assignees shall have any further obligations or liabilities hereunder with respect to the Aggregate Equity Financing Commitment, which shall become null and void ab initio. Parent shall use reasonable efforts

to promptly notify the Equity Investors upon obtaining actual knowledge of a purported or valid termination of the Merger Agreement by a party thereto.

3.

Representations and Warranties. Each Equity Investor hereby represents and warrants, on a several (and not joint or joint

and several) basis, to Parent and the Company that: (a) it is a legal entity duly organized, validly existing and in good standing (with respect to jurisdictions that recognize the concept of good standing) under the applicable Laws of the jurisdiction

of its organization; (b) it has all requisite power and authority to execute, deliver and perform its obligations under this letter; (c) the execution, delivery and performance of this letter by it has been duly and validly authorized and approved by

all necessary entity action by it, and no other proceedings or actions are necessary therefor; (d) assuming due execution and delivery by the other parties hereto, this letter has been duly and validly executed and delivered by it and constitutes a

valid and legally binding obligation of it, enforceable against it in accordance with the terms of this letter, subject to the Remedies Exceptions; (e) the consents, approvals, authorizations, permits of, filings with and notifications to, any

Governmental Authority if any, necessary for the due execution, delivery and performance of this letter by it have been obtained or made and all conditions thereof have been duly complied with, and no other action by, and no notice to or filing with,

any Governmental Authority is required in connection with the execution, delivery or performance of this letter; (f) all funds necessary to fulfill such Equity Investor’s Equity Financing Commitment (taking into account any portion thereof validly

assigned to any other person in accordance with the terms hereof) shall be available to such Equity Investor at such time as such Equity Investor’s applicable Equity Financing Commitment becomes due and payable; and (g)

the

execution, delivery and performance of this letter by it does not and will not violate its organizational documents.

4.

Assignment; Amendments and Waivers; Entire Agreement.

(a) The rights and obligations under this letter may not be assigned or delegated (whether by operation

of law, merger, consolidation or otherwise) by any party hereto without the prior written consent of the other parties hereto, and any attempted assignment shall be null and void and of no force or effect. Notwithstanding the foregoing, each of the

Equity Investors may assign all or a portion of its obligations to fund such Equity Investor’s Equity Financing Commitment to any (i) Affiliate of such Equity Investor (other than Parent or any Subsidiary thereof), (ii) other Equity Investor or (iii)

other third-party equity investor;

provided that no such assignment shall (a) relieve such Equity Investor of its obligations hereunder except to the extent actually performed or satisfied by the assignee nor (b) reasonably be expected to

impede or delay the Mergers or increase the risk of not obtaining any approval from a Governmental Authority necessary to consummate the Mergers.

(b) This letter may not be amended, and no provision hereof waived or modified, except by a written instrument signed, in the case of an amendment,

by each of the parties hereto and the Company, and in the case of a waiver, by the party against whom the waiver is to be effective and the Company.

(c) Together with the Guarantee, this letter contains all of the terms and conditions agreed to by the parties hereto relating to the subject

matter hereof and constitutes the entire agreement and supersedes all prior and contemporaneous agreements, negotiations, correspondence, undertakings, communications and understandings, both written and oral, among or between the parties hereto or

their representatives with respect to the transactions contemplated thereby (other than the Agreement and the other agreements referred to herein or therein as being entered into in connection with the Agreement).

5.

No Third Party Beneficiaries. This

letter shall be binding solely on, and inure solely to the benefit of, the parties hereto and their respective successors and permitted assigns and nothing set forth in this letter (except as expressly set forth immediately below) shall be construed to

confer upon or give to any Person, other than the parties hereto and their respective successors and permitted assigns, any benefits, rights or remedies under or by reason of, or any rights to enforce or cause Parent to enforce, the Equity Financing

Commitments or any provisions of this letter;

provided,

however, that (a) Parent Related Parties (as defined below) are express, intended third-party beneficiaries of

Section 6(a) hereof; and (b) the Company is an express,

intended third party beneficiary of (x) the rights specified in its name in

Sections 3,

4,

6(b), and

9 of this letter and (y) the rights of Parent under

Section 1 solely in the event that the Company is entitled,

in accordance with, and subject to, the express terms and conditions of Section 9.6 of the Agreement, to enforce Parent’s obligation to effect the Closing and cause the Equity Financing to be funded by each of the Equity Investors in accordance with

the terms and conditions of this letter. In no event may the Company, the Company’s equity holders or any of their respective Affiliates or Representatives or any other Person (other than Parent at the direction of the Equity Investors in their sole

discretion) enforce any aspect of this letter if the Parent Termination Fee becomes due and payable in accordance with Section 8.2 of the Agreement and the Obligations (as defined in the Guarantee) in respect of the Parent Termination Fee have been

paid under (and in accordance with) the Guarantee and the Agreement.

6.

Limited Recourse; Enforcement.

(a) Notwithstanding anything that may be expressed or implied in this letter or any document or instrument delivered in connection

herewith, Parent, by its acceptance of the benefits of the Equity Financing Commitments provided herein, and the Company, in its capacity as a third party beneficiary solely as and to the extent specified in, and on the terms and subject to the