US Market News

2日前

US Market News

2日前

The Radoff-JEC Group Issues Letter to Fellow Seer, Inc. Stockholders Correcting the Company’s Blatant Rewriting of HistoryJuly 8, 2026 6:04 PM

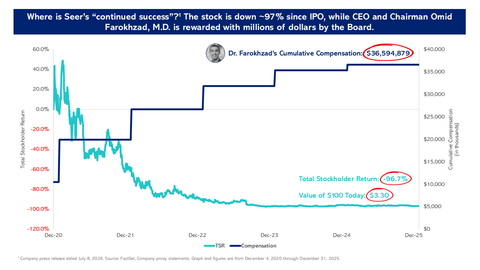

Business Wire Emphasizes that the Radoff-JEC Group Nominees Possess the Necessary Independence and Transaction Experience to Conduct an Objective Review of Strategic Alternatives to Benefit ALL Stockholders Reiterates the Need for Stockholders to Elect Truly Independent and Qualified Directors to Evaluate Chairman and CEO Omid Farokhzad, M.D.’s Acquisition Proposal Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”) today issued a letter to stockholders of Seer, Inc. (NASDAQ: SEER) (“Seer” or the “Company”) ahead of the Company’s July 28, 2026 Annual Meeting of Stockholders. This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260708418902/en/Where is Seer’s “continued success”? The stock is down ~97% since IPO, while CEO and Chairman Omid Farokhzad, M.D. is rewarded with millions of dollars by the Board. The Radoff-JEC Group, which owns approximately 7.7% of Seer’s outstanding common stock, recommends that its fellow stockholders vote “FOR” the election of Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini to ensure the Board of Directors (the “Board”) runs an objective strategic review process aimed at maximizing value for ALL Seer stockholders. *** Fellow Stockholders, There is a real mismatch between what Seer is now saying and how its management and Board have historically acted. The Company is claiming that Seer has been a “success” and that the directors we are seeking to remove are “critical to Seer’s future.”1 But stockholders like us know the truth: Seer has delivered a -97.0% total stockholder return since going public in December 2020.2 Seer has generated cumulative reported losses of more than $465 million since its IPO and virtually zero revenue growth since 2022.3 Seer has burned an average of $51.8 million each year since going public, for a total cash burn of $310.8 million.4 Chairman and CEO Omid Farokhzad, M.D.’s strategic plan – which was presented to the Board – states that Seer will not achieve profitability until 2031, which would be 11 years after the Company went public.5 Dr. Farokhzad has sold over $103 million worth of Seer shares since the IPO – more than the Company’s current market capitalization.6 The Board rewarded Dr. Farokhzad with more than $6 million in average annual pay from 2020 through 2025 – more than half of Seer’s average revenue over the same period, totaling ~$36.5 million in reported compensation.7 Despite Seer’s claim that only two of its seven directors are NOT independent (Dr. Farokhzad and Robert Langer, Sc.D.), in reality, we contend that FIVE of the directors are NOT truly independent. Terrance McGuire and Dipchand Nishar have external business relationships with Dr. Farokhzad. Isaac Ro’s employer is a significant investor in Seer’s controlled company PrognomiQ (where he also serves as a director), so his interests and motivations are not aligned with those of Seer stockholders. These issues, and the actions these directors have exhibited to date, raise serious doubts as to their ability to independently and effectively oversee Dr. Farokhzad or objectively evaluate his proposal to acquire Seer.8 Seer’s Board Cannot Be Trusted to Evaluate Chairman and CEO Farokhzad’s Acquisition Proposal The Board’s misleading statements over the past several months have underscored that it is NOT focused on acting in the best interests of ALL stockholders – but only on doing what’s best for itself and Dr. Farokhzad. Seer’s Egregiously False Claims9 The Facts “Seer has a purpose-built Board of Directors with the expertise needed to guide a category-creating life sciences tools company.” Seer’s seven-member Board contains Dr. Farokhzad and four directors with whom he has external business relationships. Dr. Farokhzad has not only destroyed value at Seer – he has done the same at Senti Biosciences Holdings, Inc., BIND Therapeutics, Inc., Selecta Biosciences, Inc. and Tarveda Therapeutics, Inc. Directors McGuire and Nishar served on the board of Dr. Farokhzad’s SPAC, which combined with Senti Biosciences Holdings, Inc. in 2022 and has since seen its share price decline by more than 98%.10 Is the “purpose” of Seer’s Board to be beholden to Dr. Farokhzad and guide the Company to a -97.0% total stockholder return?11 “Their only desire is to strip Seer of its cash.” We never proposed stripping Seer of its cash. Our three acquisition proposals valued Seer appropriately – it is a microcap business that has consistently burned cash and has underwhelming growth prospects. The cash component of Dr. Farokhzad’s own proposal to acquire Seer is identical to our last offer; yet he does not purport to desire to “strip Seer of its cash.” The Board rejected each of our proposals without engaging with us whatsoever but is now apparently evaluating Dr. Farokhzad’s offer, which we calculate as inferior. “[T]heir nominees raise serious concerns regarding independence and their ability to act in the best interests of all stockholders.” Our nominees are independent from us and have no relationships that would impact their ability to act in the best interests of all stockholders. Dr. Farokhzad, on the other hand, is bidding to acquire Seer and has business relationships with four of the six other sitting directors. The Board has repeatedly bashed our acquisition proposals – which it rejected without engaging – yet has not commented on Dr. Farokhzad’s proposal in its letters to stockholders. Seer’s Board has failed time and again to act in the best interests of all stockholders, whether by failing to engage with us on any of our three acquisition proposals, seeking to preserve Dr. Farokhzad’s super-voting rights or adopting an onerous poison pill. How can stockholders trust that Mr. McGuire, Mr. Nishar, Mr. Ro or Dr. Langer will objectively evaluate Dr. Farokhzad’s proposal when they have financial incentives to support whatever Dr. Farokhzad wants? “Three nominees, one purpose: Sell Seer early.”12 The purpose of our nominees, as we have consistently said, is to act in the best interests of all Seer stockholders, including by advocating for a strategic review process that focuses on ways to maximize stockholder value after years of destruction. As Dr. Farokhzad himself said, “Seer should be private.”13 The Board is now evaluating his proposal, making its comments about us wanting to sell Seer “early” look disingenuous. Vote FOR Independent Directors to Support an Objective Strategic Review We agree with Dr. Farokhzad that Seer should not be a public company. We have submitted three fully financed proposals to acquire Seer for premiums of 33% - 42% to its unaffected share price and a contingent value right that would enable stockholders to further benefit from the disposition of Seer’s assets. The Board chose to reject all three of these offers outright without engaging with us on ANY of them. Then, Dr. Farokhzad submitted a proposal to acquire Seer, and two days later, the Board quickly formed a Special Committee to evaluate his proposal – though it has not disclosed which directors will serve on the Special Committee. We are not opposed to someone who is not us buying Seer. We simply believe Seer should be sold to the highest bidder in a transaction that maximizes value for ALL stockholders – not in a conflict-ridden process led by directors who are chummy with one of the bidders and have demonstrated over the past five-plus years that they cannot create value for Seer stockholders. Voting for Dr. Berman, Mr. Horowitz and Mr. Rinaldini – who are capital allocation and transaction specialists, as the Board itself even admitted14 – is the only way to ensure the Board conducts an independent and objective evaluation of acquisition proposals with the goal of maximizing value for ALL stockholders. Sincerely, Bradley L. Radoff and Michael Torok

Owners of ~7.7% of Seer’s Outstanding Common Stock *** Vote FOR the Radoff-JEC Group’s Nominees – Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini – Today to Support a Credible Strategic Review Process Aimed at Maximizing Value for ALL Seer Stockholders Do NOT Vote for Omid Farokhzad, M.D., Terrance McGuire or Dipchand (Deep) Nishar Questions about how to vote? Contact (888) 368-0379 or info@saratogaproxy.com. Visit www.SaratogaProxy.com/SEER to learn more. 1 Company press release dated July 8, 2026. 2 FactSet. Total stockholder return from December 4, 2020 through April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial proposal to acquire the Company. 3 Company Form 10-K for the year ended December 31, 2025 filed on March 2, 2026. 4 Company Form 10-K filings. Cash burned in operations refers to the sum of net cash used in operating activities, purchases of property and equipment, and proceeds from disposal of property and equipment. 5 Company PRE 14A filed on October 10, 2025. 6 Dr. Farokhzad’s Form 4 filings. Market capitalization as of close on July 2, 2026, prior to the public disclosure of Dr. Farokhzad’s take private offer. 7 Company proxy statements. 8 Company proxy statements. Complaint filed by Bruce Taylor, on behalf of himself and all other similarly situated stockholders of the Company, in the Delaware Court of Chancery on March 2, 2026. 9 Company press release dated July 8, 2026. 10 FactSet. Share price decline from June 9, 2022 through July 8, 2026. 11 FactSet. Total stockholder return from December 4, 2020 through April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial proposal to acquire the Company. 12 Company presentation filed on July 6, 2026. 13 Letter from Dr. Farokhzad dated July 1, 2026 and filed by the Company on July 2, 2026. 14 Company presentation filed on July 6, 2026. View source version on businesswire.com: https://www.businesswire.com/news/home/20260708418902/en/ Greg Lempel

greg@fondrenlp.com or Saratoga Proxy Consulting LLC

John Ferguson / Joseph Mills, 212-257-1311

info@saratogaproxy.com Original: The Radoff-JEC Group Issues Letter to Fellow Seer, Inc. Stockholders Correcting the Company’s Blatant Rewriting of History

US Market News

2週前

The Radoff-JEC Group Releases Presentation Highlighting Why Seer, Inc. Stockholders Should Vote for Boardroom ChangeJune 29, 2026 4:10 PM

Business Wire Details How Chair and CEO Omid Farokhzad, M.D., Compensation Committee Chair Terrance McGuire and Director Deep Nishar Have Burned More Than $310 Million in Cash, Adopted an Anti-Stockholder Poison Pill and Paid Themselves Excessively While Overseeing a 97% Decline in Seer’s Share Price Urges Stockholders to Elect Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini to Help Prevent Further Value Destruction Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”), who collectively own approximately 7.7% of the outstanding shares of Seer, Inc. (NASDAQ: SEER) (“Seer” or the “Company”), today released a presentation detailing the urgent case for boardroom change at Seer. The presentation highlights why stockholders should replace Chair and CEO Omid Farokhzad, M.D., Terrance McGuire and Deep Nishar by electing Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini to the Company’s Board of Directors (the “Board”) at the upcoming annual meeting scheduled to be held on July 28, 2026: Dr. Farokhzad has been the Chair and CEO of Seer since its IPO. Until December of 2025, Dr. Farokhzad effectively had control of Seer through his ownership of nearly 40% of Seer’s total voting power through his then super-voting Class B shares. As such, we believe that Dr. Farokhzad is accountable for ALL of the failures at Seer – from its failed strategy to its operating losses and cash burn, and ultimately, to the 97% decline in Seer’s share price.1 We believe Messrs. McGuire and Nishar have supported the value destruction at Seer by, among other things, failing to hold Dr. Farokhzad accountable as CEO despite witnessing more than five years of his failing strategy and supporting the adoption of a unilateral poison pill seemingly to protect Dr. Farokhzad’s position by weakening the rights of stockholders. As shown in slide 15 of our presentation, since Seer’s IPO, Dr. Farokhzad has sold over $103 million worth of Seer shares.2 Seer’s current market capitalization is only $92.4 million!3 Slide 37 of our presentation highlights that while Seer stockholders were suffering significant losses and the Company was floundering, Dr. Farokhzad – who was being paid millions of dollars by Seer – was spending significant time running a different company (Dynamics Special Purpose Corp.).4 Rather than demand Dr. Farokhzad’s resignation or termination as CEO, Messrs. McGuire and Nishar joined Dr. Farokhzad at the SPAC, enjoying fees and other compensation. Similar to Seer, shares of the publicly traded SPAC (NASDAQ: SNTI) have lost 98.3% of their value since Dr. Farokhzad took it public!5 Our nominees are three independent public company directors who would bring the requisite biotechnology, corporate governance, capital allocation and M&A expertise that we believe is required to unlock value at Seer and oversee a robust strategic review for the benefit of all stockholders. Crucially, Dr. Berman and Messrs. Horowitz and Rinaldini have track records of creating value for stockholders of other companies, are independent of Dr. Farokhzad and would bring objectivity to the boardroom. Vote FOR the Radoff-JEC Group’s Nominees – Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini – Today to Help Prevent Further Value Destruction Do NOT Vote for Omid Farokhzad, M.D., Terrance McGuire or Dipchand (Deep) Nishar Questions about how to vote? Contact (888) 368-0379 or info@saratogaproxy.com Visit www.SaratogaProxy.com/SEER to learn more 1 Share price decline from December 4, 2020 through April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial proposal to acquire the Company.

2 Dr. Farokhzad’s Form 4 filings.

3 Market capitalization per FactSet as of market close on May 20, 2026, the day before the Radoff-JEC Group filed its preliminary proxy statement.

4 Dynamics Special Purpose Corp. filings. Complaint filed by Bruce Taylor, on behalf of himself and all other similarly situated stockholders of the Company, in the Delaware Court of Chancery on March 2, 2026.

5 FactSet. Share price decline from June 9, 2022 through June 25, 2026. View source version on businesswire.com: https://www.businesswire.com/news/home/20260629162416/en/ Greg Lempel

greg@fondrenlp.com or Saratoga Proxy Consulting LLC

John Ferguson / Joseph Mills, 212-257-1311

info@saratogaproxy.com Original: The Radoff-JEC Group Releases Presentation Highlighting Why Seer, Inc. Stockholders Should Vote for Boardroom Change

US Market News

2週前

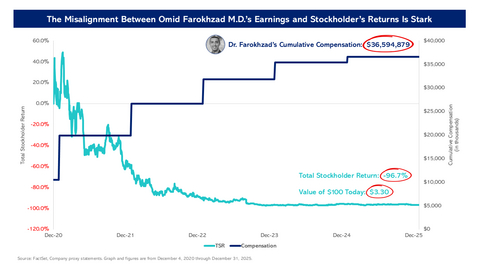

The Radoff-JEC Group Urges Seer, Inc. Stockholders to Vote for Boardroom Change TodayJune 24, 2026 8:45 AM

Business Wire Believes New Independent Directors Are Needed to Correct the Board’s Misaligned Priorities and Prevent Further Value Destruction Reveals Seer’s Board Has Not Responded to the Radoff-JEC Group’s Stockholder-Friendly Offer Made on June 15 to Resolve the Ongoing Proxy Contest, Demonstrating the Board's Focus on its Own Entrenchment Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”), who collectively own approximately 7.7% of the outstanding shares of Seer, Inc. (NASDAQ: SEER) (“Seer” or the “Company”), today issued the following statement. This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260624630276/en/Source: FactSet, Company proxy statements. Graph and figures are from December 4, 2020 through December 31, 2025. Seer’s Board of Directors (the “Board”) has destroyed value for stockholders while enriching Company insiders: The Company has posted a -97.0% share price decline since its December 2020 IPO.1 Seer has generated cumulative reported losses exceeding $465 million since its IPO.2 Seer has delivered virtually no revenue growth over the last three fiscal years, while investing over $160 million.3 The Board has rewarded Chairman and CEO Omid Farokhzad, M.D. with nearly $37 million in cumulative compensation while a stockholder who purchased one share at the time of the IPO ($19.00) would be left with less than $0.63.4 Seer has no plan to create stockholder value under Chairman and CEO Omid Farokhzad, M.D.: Dr. Farokhzad has destroyed more than $1 billion in investor capital across five separate companies, evidence supporting our belief that he is incapable of turning around Seer.5 The strategic plan overseen by the Board anticipates Seer will not achieve profitability until 2031.6 The Board rejected our three proposals to acquire Seer for premiums of 33% - 42% to its unaffected share price and a contingent value right – proposals which we believe provide substantially greater certainty of value creation than the Company’s current strategic plan – without even engaging with us. Seer’s Board has not responded to our proposal to settle this proxy contest: On June 15, 2026, we proposed to end our ongoing proxy contest in exchange for Seer adopting governance enhancements and conducting a tender offer for 20 million shares at $2.50 per share, which would be in line with the Board’s authorized buyback program and management’s statements that there is a “significant dislocation” in the Company’s share price.7 More than a week later, the Board has still not responded to our settlement offer – which it requested in the first place – demonstrating that its priority is not delivering value or governance improvements for stockholders. Instead of focusing on opportunities to maximize value for stockholders as Seer’s share price has consistently traded at a significant discount to net cash, the Board has diluted stockholders by repeatedly issuing large grants of restricted stock units and in-the-money options to Dr. Farokhzad and President and CFO David Horn. Vote FOR the Radoff-JEC Group’s Nominees – Howard H. Berman, Ph.D., Joshua S. Horowitz and Luis E. Rinaldini – Today to Prevent Further Value Destruction Do NOT Vote for Omid Farokhzad, M.D., Terrance McGuire or Dipchand (Deep) Nishar Questions about how to vote? Contact (888) 368-0379 or info@saratogaproxy.com. Visit www.SaratogaProxy.com/SEER to learn more. _________________________________________ 1FactSet. Share price decline from December 4, 2020 through April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial proposal to acquire the Company. 2 The Company’s Form 10-K for the year ended December 31, 2025 filed on March 2, 2026. 3 Company Form 10-K filings. 4 Company proxy statements. FactSet; share price decline from December 4, 2020 through December 31, 2025. 5 Seer, BIND Therapeutics, Inc., Selecta Biosciences, Inc., Tarveda Therapeutics, Inc. and Senti Biosciences Holdings, Inc. 6 Company PRE 14A filed on October 10, 2025. 7 On the Company’s Q1 2026 earnings call held on May 13, 2026, President and CFO David Horn said: “Our opportunistic share repurchase in the quarter reflect our continued belief that there is a significant dislocation in our share price.” View source version on businesswire.com: https://www.businesswire.com/news/home/20260624630276/en/ Greg Lempel

greg@fondrenlp.com or Saratoga Proxy Consulting LLC

John Ferguson / Joseph Mills, 212-257-1311

info@saratogaproxy.com Original: The Radoff-JEC Group Urges Seer, Inc. Stockholders to Vote for Boardroom Change Today

US Market News

1月前

The Radoff-JEC Group Calls on Seer Inc. and Its Advisors to Reevaluate Its Premium Acquisition Proposal in the Best Interests of All StockholdersMay 27, 2026 4:30 PM

Business Wire Corrects the Board’s Flawed Reasons for Rejecting its Credible, Premium Acquisition Offer in Apparent Breach of its Fiduciary Duty Reaffirms its Fully Financed Proposal to Acquire Seer for $2.40 per Share in Cash – a 42% Premium to the Unaffected Share Price – and a CVR for Stockholders to Receive 80% of the Net Proceeds from the Company’s Assets Files Preliminary Proxy Statement to Give Stockholders the Opportunity to Elect Three New Qualified, Independent Directors Who Intend to Advocate for a Strategic Review Process Aimed at Maximizing Value for All Seer Stockholders Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”), who collectively own approximately 7.8% of the outstanding shares of Seer, Inc. (NASDAQ: SEER) (“Seer” or the “Company”), today issued the following open letter to the Company’s independent directors and financial and legal advisors in response to Seer’s apparent bad-faith rejection of the Radoff-JEC Group’s three fully financed proposals to acquire Seer. The Radoff-JEC Group has also filed a preliminary proxy statement to solicit votes for the election of its three nominees – Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini – to the Board at the upcoming 2026 Annual Meeting of Stockholders. *** May 27, 2026 Seer, Inc.

3800 Bridge Parkway, Suite 102

Redwood City, California 94065

Attn: Meeta Gulyani, Terrance McGuire, Dipchand Nishar, Isaac Ro and Nicolas Roelofs, Ph.D.; Perella Weinberg Partners LP; and Wilson Sonsini Goodrich & Rosati, Professional Corporation Dear Independent Members of the Board, Perella Weinberg and Wilson Sonsini, As you are aware, the Radoff-JEC Group has submitted three public proposals to acquire Seer: April 13, 2026: Proposal to acquire the Company for $2.25 per share in cash, a 33% premium to the unaffected closing price, and a contingent value right (“CVR”) for stockholders to receive potential additional value from the sale of Seer’s assets. April 24, 2026: Improved proposal to acquire the Company for $2.35 per share in cash, a 39% premium to the unaffected closing price, and the same CVR. May 14, 2026: Third proposal to acquire the Company for $2.40 per share in cash, a 42% premium to the unaffected closing price, and the same CVR. The Board did not respond to our April 13 proposal, rejected our April 24 proposal without engaging with us and rejected our May 14 proposal – again, without engaging with us. As the fourth-largest stockholder of Seer with a 7.8% ownership stake, we believe it is a potential breach of fiduciary duty for the Board to refuse to engage with a bidding party and reject an acquisition offer that could represent superior value for stockholders compared to what could reasonably be expected under the status quo. In Seer’s May 21, 2026 press release, the Board alleged our proposal “is not in the best interests of Seer stockholders because it significantly undervalues Seer and fails to reflect the value of Seer’s long-term growth prospects.” How can the Board credibly claim this when Seer’s management team – which has failed to create any value for stockholders over the past five and a half years – has not provided a credible standalone plan that would deliver superior value? Since the Board has refused to discuss our proposal with us, denying us an opportunity to address any concerns, we are providing written explanations below for why we believe the Board’s purported reasons for rejecting our bids are not legitimate. Seer’s Reasons for Rejecting Our Bids1 The Radoff-JEC Group’s Views “[T]he Board carefully reviewed the Revised Proposal in consultation with its independent financial and legal advisors. Following a thorough analysis, the Board concluded that the Revised Proposal significantly undervalues Seer.” Given that the Board never spoke to us, it’s difficult to take its “careful” and “thorough” review seriously. Perella Weinberg and Wilson Sonsini’s role appears to be implementing activist defense strategies to help Chair and CEO Omid Farokhzad, M.D. and his allies entrench themselves – not advising the Board on ways to maximize value for all stockholders. When Perella Weinberg calculated the potential value of the Company as a standalone enterprise under Dr. Farokhzad, how did it account for Dr. Farokhzad’s and director Dr. Robert Langer’s record of incinerating more than $1 billion of investor capital across at least five separate companies? “[T]he Second Unsolicited Proposal fails to reflect the value of Seer’s Proteograph Product Suite platform, as well as Seer’s technology leadership, adoption momentum and standalone growth prospects.” Seer is a microcap business that is projected to grow revenue by just 3% this year after burning nearly $16 million in cash in the most recent quarter. The Company posted $2.8 million in revenue in the first quarter of 2026, which represents a -33.3% decline year over year and its lowest first-quarter revenue since 2021. The Company’s first quarter results were so disappointing that its stock – which had risen following our initial acquisition proposal – fell to below the unaffected share price in the days after the earnings report.2 Our proposal, which includes a CVR to enable stockholders to receive 80% of the net proceeds received from any license, sale or other disposition of Seer’s business and assets, will unlock whatever value remains of Seer’s platform and the technology that underpins it. “The Board is confident that Seer’s strategy, platform and team will create value well in excess of the proposal from the Radoff-JEC Group.” The Seer leadership team has detailed its strategy and the market opportunity for its platform in numerous earnings calls, SEC filings, investor presentations and investor conferences. Since the Company’s initial public offering in December 2020, Dr. Farokhzad and his management team have delivered a -97% total stockholder return and burned hundreds of millions of cash while delivering negligible revenue growth.3 There is no evidence to support Dr. Roelofs’ statement. This is a Company that has no business remaining public under the same failed leadership. “As with the Initial Unsolicited Proposal, the Second Unsolicited Proposal was not accompanied by any evidence that the Radoff-JEC Group had access to the funds necessary to consummate the proposed acquisition.” As we stated at the time of submitting them, each of our acquisition proposals were fully financed and subject to very limited confirmatory due diligence. The acquisition proposals could be financed with the cash on the Company’s balance sheet. How can the Board and its advisors declare our offer as highly contingent and lacking funding when they have never reached out to us and when that contradicts the facts of our offer? Independent directors are legally obligated to act in the best interest of all stockholders – not remain complicit in decisions that are apparently being pushed by management and destroying value. As directors and named advisors to a public company, your individual reputations are on the line. We continue to believe that an immediate sale of the Company would be in the best interest of all stockholders and provide immediate value that is at risk of further destruction under the current leadership team. We urge you to reevaluate the merits of our proposal and immediately initiate a credible strategic review process, which should be run by an independent committee of the Board and include engagement with us to discuss our proposal in detail. Because you continue to act in a manner that, in our view, borders on breaching your fiduciary duty, we have no choice but to proceed with a proxy contest to give stockholders the opportunity to elect three new highly qualified, independent directors who would bring significant biotechnology, capital allocation, M&A and public company governance experience to the boardroom. If elected, Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini plan to advocate for a robust strategic review process aimed at maximizing value for all Seer stockholders. We expect stockholders will overwhelmingly vote for change in light of the Company’s abysmal performance, lack of revenue growth and mishandling of our acquisition proposal under the current Board and management team. Sincerely, Bradley L. Radoff and Michael Torok CERTAIN INFORMATION CONCERNING THE PARTICIPANTS Bradley L. Radoff and Michael Torok, together with the other participants named herein (collectively, the “Radoff-JEC Group”), have filed a preliminary proxy statement and accompanying WHITE universal proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit votes for the election of its slate of highly qualified director nominees at the 2026 annual meeting of stockholders of Seer, Inc., a Delaware corporation (the “Company”). THE RADOFF-JEC GROUP STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS, INCLUDING A PROXY CARD, AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR. The participants in the anticipated proxy solicitation are The Radoff Family Foundation (“Radoff Foundation”), Bradley L. Radoff, JEC II Associates, LLC (“JEC II”), The MOS Trust (“MOS Trust”), MOS PTC, LLC (“MOS PTC”), Michael Torok, Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini. As of the date hereof, Radoff Foundation directly beneficially owns 500,000 shares of Class A Common Stock, par value $0.00001 per share, of the Company (“Common Stock”). As of the date hereof, Mr. Radoff directly beneficially owns 2,110,232 shares of Common Stock. Mr. Radoff, as a director of Radoff Foundation, may be deemed to beneficially own the 500,000 shares of Common Stock directly beneficially owned by Radoff Foundation, which, together with the 2,110,232 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 2,610,232 shares of Common Stock beneficially owned by Mr. Radoff. As of the date hereof, JEC II directly beneficially owns 1,167,296 shares of Common Stock. As of the date hereof, MOS Trust directly beneficially owns 215,000 shares of Common Stock. MOS PTC, as the trustee of MOS Trust, may be deemed to beneficially own the 215,000 shares of Common Stock directly beneficially owned by MOS Trust. As of the date hereof, Mr. Torok directly beneficially owns 285,000 shares of Common Stock. Mr. Torok, as the Manager of JEC II and a Manager of MOS PTC, may be deemed to beneficially own the 1,382,296 shares of Common Stock directly beneficially owned in the aggregate by JEC II and MOS Trust, which, together with the 285,000 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 1,667,296 shares of Common Stock beneficially owned by Mr. Torok. As of the date hereof, each of Dr. Berman and Messrs. Horowitz and Rinaldini does not beneficially own any shares of Common Stock. ____________________________ 1 Seer’s April 27, 2026 and May 21, 2026 press releases and 2026 preliminary proxy statement. 2 Bloomberg. On April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial non-binding proposal to acquire the Company, Seer’s share price closed at $1.69. One week after the Company reported Q1 2026 earnings on May 13, 2026, Seer’s share price closed at $1.68 on May 20, 2026. 3 Bloomberg. TSR from December 4, 2020 through the unaffected date of April 10, 2026. View source version on businesswire.com: https://www.businesswire.com/news/home/20260527350891/en/ Greg Lempel

greg@fondrenlp.com Original: The Radoff-JEC Group Calls on Seer Inc. and Its Advisors to Reevaluate Its Premium Acquisition Proposal in the Best Interests of All Stockholders

US Market News

2月前

The Radoff-JEC Group Submits its Third Non-Binding Proposal to Acquire Seer, Inc.May 14, 2026 8:00 AM

Business Wire Proposal Provides Stockholders $2.40 per Share in Cash, a 42% Premium to the Unaffected Share Price, as Well as Potential Additional Value from the Sale of Seer’s Assets via a Contingent Value Right Urges Seer’s Independent Directors and Financial Advisor to Engage with the Radoff-JEC Group Regarding a Transaction and Avoid Further Value Destruction Under Current Leadership Team from Continued Operations Following Woeful Q1 2026 Results Reaffirms its Commitment to Holding the Board Accountable by Electing Three Highly Qualified, Independent Directors Who Are Best Suited to Rebuilding Value at Seer and Overseeing a Credible Strategic Review Process for the Benefit of All Stockholders Bradley L. Radoff and Michael Torok, who collectively own approximately 7.8% of the outstanding shares of Seer, Inc. (NASDAQ: SEER) (the “Company”), today submitted the following improved non-binding proposal to acquire the Company – their third such proposal – for $2.40 per share in cash plus a contingent value right. *** May 14, 2026 Seer, Inc.

3800 Bridge Parkway, Suite 102

Redwood City, California 94065

Attn: Board of Directors Dear Members of the Board, As you are aware, Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”) are significant stockholders of Seer, Inc. (“Seer” or the “Company”), collectively owning approximately 7.8% of the Company’s outstanding shares. Yesterday, Seer reported its first quarter 2026 financial results. Based on the Company’s operating history over the past several years and its dismal guidance for 2026, stockholders were expecting yet another quarter of substantial operating losses, continued cash burn, negligible topline growth and zero evidence of a path to profitability. Chair and CEO Omid Farokhzad, M.D. managed to deliver results that were below those low expectations as the Company burned $15.7 million in the quarter while achieving revenue of a meager $2.8 million. While claiming to have repurchased approximately 1.5 million Class A common shares during the quarter and indicating that the share price is undervalued, the Company granted more than 1.6 million RSUs and nearly 1.2 million options, demonstrating the Board’s willingness to continuously dilute stockholders without regard for the valuation. On April 27, 2026, the Board rejected our revised proposal to acquire the Company. Importantly, neither the Board nor its advisors engaged with us prior to rejecting our offer. We believe the Board’s failure to engage with us explains why the Board’s analysis of our proposal was flawed and why the Board’s conclusion and statements regarding our proposal were, in our opinion, incorrect and misleading to stockholders. To us, this serves as yet another example of the conflicted, failing Board acting solely in the interest of Dr. Farokhzad. We are pleased to submit this further improved, non-binding proposal to acquire 100% of the equity of the Company for $2.40 per share in cash, which represents an immediate 42% premium to the Company’s unaffected share price, plus a contingent value right (“CVR”) representing the right for stockholders to receive 80% of the net proceeds received from any license, sale or other disposition of Seer’s business and assets, including PrognomiQ. To be clear, our offer is not speculative or contingent. Our offer does not undervalue Seer. In fact, the structure of our proposal is designed to ensure that stockholders receive full and fair value for their investment in Seer by way of a CVR providing the proceeds from an open auction process for the Company’s business and assets. We believe our proposal offers stockholders many valuable things that the Board’s current strategy does not, including: certainty, accountability and a realistic framework for maximizing remaining value while insulating stockholders from continued value destruction under the leadership of Dr. Farokhzad. During the first quarter of this year alone, the tangible value destroyed was nearly $16 million – an annualized pace of approximately $1.14/share on a stock that closed yesterday at $1.77/share. We kindly request the Board consider the track record of Dr. Farokhzad as it evaluates subjecting stockholders to continued losses and cash burn while pursuing his failed strategy. Based upon our analysis, Dr. Farokhzad has (a) destroyed more than $1 billion in investor capital across Seer, BIND Therapeutics, Selecta Biosciences, Tarveda Therapeutics and Senti Biosciences, and (b) while Dr. Farokhzad continues to talk about Seer’s progress and potential, he cannot escape the fact that the proceeds he has received from sales of Seer stock exceed the Company’s current market capitalization. We could expand on this topic, but we believe your fellow director Robert Langer, Sc.D. is well positioned to detail the many failures of Dr. Farokhzad as he has participated in (at least) five spectacular failures with him. We urge the Board to fulfill its fiduciary obligations by engaging seriously with us regarding our proposal and by providing stockholders with a transparent evaluation process. Entrenchment and continued adherence to a failed operating strategy are not acceptable to stockholders. We also demand that the Board refrain from any acquisitions until after the upcoming Annual Meeting where stockholders will have an opportunity to express their views at the ballot box regarding the future of the Company. We are concerned that as the Board realizes the current strategy is pointless, it will allow management to reboot its ambitions by using stockholder capital. This cannot happen and will not be tolerated. Our improved offer does not expire until May 29, 2026, and we urge the independent members of the Board and its financial advisor to engage with us and negotiate a transaction that will benefit all stockholders while rescuing the Company from its inevitable destruction – if it follows the trajectory of Dr. Farokhzad’s other companies – under Dr. Farokhzad’s leadership. Whether the Board engages with us or not, we will give stockholders the opportunity to hold the incumbent Board accountable at the upcoming Annual Meeting for years of value destruction and poor operating results. Stockholders will be able to elect three new, independent and qualified directors – Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini – who bring the requisite public company governance, capital allocation and M&A expertise to rebuild value at Seer and oversee a credible strategic review process for the benefit of all stockholders. Sincerely, Bradley L. Radoff and Michael Torok CERTAIN INFORMATION CONCERNING THE PARTICIPANTS Bradley L. Radoff and Michael Torok, together with the other participants named herein (collectively, the “Radoff-JEC Group”), intends to file a preliminary proxy statement and accompanying WHITE universal proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit votes for the election of its slate of highly qualified director nominees at the 2026 annual meeting of stockholders of Seer, Inc., a Delaware corporation (the “Company”). THE RADOFF-JEC GROUP STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS, INCLUDING A PROXY CARD, AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR. The participants in the anticipated proxy solicitation are expected to be The Radoff Family Foundation (“Radoff Foundation”), Bradley L. Radoff, JEC II Associates, LLC (“JEC II”), The MOS Trust (“MOS Trust”), MOS PTC, LLC (“MOS PTC”), Michael Torok, Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini. As of the date hereof, Radoff Foundation directly beneficially owns 500,000 shares of Class A Common Stock, par value $0.00001 per share, of the Company (“Common Stock”). As of the date hereof, Mr. Radoff directly beneficially owns 2,110,232 shares of Common Stock. Mr. Radoff, as a director of Radoff Foundation, may be deemed to beneficially own the 500,000 shares of Common Stock directly beneficially owned by Radoff Foundation, which, together with the 2,110,232 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 2,610,232 shares of Common Stock beneficially owned by Mr. Radoff. As of the date hereof, JEC II directly beneficially owns 1,167,296 shares of Common Stock. As of the date hereof, MOS Trust directly beneficially owns 215,000 shares of Common Stock. MOS PTC, as the trustee of MOS Trust, may be deemed to beneficially own the 215,000 shares of Common Stock directly beneficially owned by MOS Trust. As of the date hereof, Mr. Torok directly beneficially owns 285,000 shares of Common Stock. Mr. Torok, as the Manager of JEC II and a Manager of MOS PTC, may be deemed to beneficially own the 1,382,296 shares of Common Stock directly beneficially owned in the aggregate by JEC II and MOS Trust, which, together with the 285,000 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 1,667,296 shares of Common Stock beneficially owned by Mr. Torok. As of the date hereof, each of Dr. Berman and Messrs. Horowitz and Rinaldini does not beneficially own any shares of Common Stock. View source version on businesswire.com: https://www.businesswire.com/news/home/20260514534941/en/ Greg Lempel

greg@fondrenlp.com Original: The Radoff-JEC Group Submits its Third Non-Binding Proposal to Acquire Seer, Inc.

US Market News

3月前

The Radoff-JEC Group Submits Improved Non-Binding Proposal to Acquire Seer, Inc.April 24, 2026 7:00 AM

Business Wire

Proposal Provides Stockholders $2.35 per Share in Cash, a 39% Premium to the Unaffected Closing Price, as Well as Potential Additional Value from the Sale of Seer’s Assets via a Contingent Value Right

Proposal Provides Stockholders Immediate and Significant Value While Avoiding Further Value Destruction from Continued Abysmal Operating Results

Criticizes the Board for Failing to Engage With the Radoff-JEC Group Regarding its Acquisition Proposal

Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group”), who collectively own approximately 7.6% of the outstanding shares of Seer, Inc. (NASDAQ: SEER) (“Seer” or the “Company”), today submitted the following improved non-binding proposal to acquire the Company for $2.35 per share in cash plus a contingent value right.

***

April 24, 2026

Seer, Inc.

3800 Bridge Parkway, Suite 102

Redwood City, California 94065

Attn: Board of Directors

Dear Members of the Board,

As you are aware, Bradley L. Radoff and Michael Torok (together with certain of their affiliates, the “Radoff-JEC Group” or “we”) are significant stockholders of Seer, Inc. (“Seer” or the “Company”), collectively owning approximately 7.6% of the Company’s outstanding shares.

On April 13, 2026, we submitted a fully financed proposal that we believe provides stockholders with downside protection from continued poor business performance and a path to full value by way of a contingent value right (“CVR”). While the Board of Directors (the “Board”) and its advisors were able to hastily enact a seemingly unlawful poison pill within days of our initial Schedule 13D filing,1 it has now been two weeks and the Board has still not even contacted us regarding our acquisition proposal.

Our view remains straightforward: Seer has failed as a public company in every way under the current leadership team, including a share price decline of over 90% since its IPO,2 cumulative reported losses exceeding $465 million3 and virtually no revenue growth. Seer’s complete failure has occurred while numerous industry participants have succeeded: Olink (acquired by Thermo Fisher), PreOmics and Biognosys (acquired by Bruker), Akoya Biosciences (acquired by Quanterix) and Somalogic (acquired by Illumina). Just last week, Alamar Biosciences had a successful initial public offering that valued the company at over $1.5 billion.4 While Board Chair and CEO Omid Farokzhad, M.D. has consistently blamed Seer’s lack of revenue growth over the past half-decade on macroeconomic headwinds and other factors outside of the Company’s control, it is notable that Alamar Biosciences’ revenue grew from $25.1 million in 2024 to $74.2 million in 2025.5

Based on numerous conversations we have had with industry participants, we do not believe Seer will succeed as an independent publicly traded company. This view is supported by Seer’s consistent lack of revenue growth, astronomical operating losses, forward-looking guidance of more of the same dismal results, and the increasing competitive and other pressures from successful, growing companies in its industry. A comparison between Alamar Biosciences and Seer further validates that conclusion – Alamar Biosciences raised and invested less money than Seer while it grew from zero revenue to a 2026 run-rate that exceeds $100 million per year. During that time, Seer burned over $200 million in cash to increase revenue from $15.5 million in 2022 to a mere $16.6 million in 2025.

We continue to believe that although Seer has destroyed tremendous stockholder value to date, it is not too late to salvage value from its assets, capabilities and intellectual property. With that in mind, we are pleased to submit this improved, non-binding proposal to Seer’s Board to acquire 100% of the equity of the Company for $2.35 per share in cash, which represents a 39% premium to the unaffected closing price on April 10, 2026, plus a CVR representing the right for stockholders to receive 80% of the net proceeds received from any license, sale, or other disposition of Seer’s business and assets, including PrognomiQ.

Our proposal is subject to limited confirmatory due diligence and based on the availability of at least $215 million of net cash and cash equivalents at closing. We remain prepared to provide the Company with a substantial non-performance fee to give the Board and fellow stockholders assurance that we will complete the acquisition of Seer on the agreed-upon terms and conditions. Additionally, we are prepared to invest $10 million in the Company. We are ready to move forward and close expeditiously – our proposal is not subject to any financing conditions.

Baker Botts L.L.P. and Olshan Frome Wolosky LLP are acting as our legal advisors, and we are prepared to complete due diligence and negotiate a definitive merger agreement by May 18, 2026. We expect that the Board will promptly meet with us and seriously consider our improved proposal in accordance with its fiduciary duties. We look forward to receiving a response regarding the Board’s willingness and availability to discuss our improved proposal no later than 5:00pm ET on May 2, 2026, at which point our offer will expire.

Sincerely,

Bradley L. Radoff and Michael Torok

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

Bradley L. Radoff and Michael Torok, together with the other participants named herein (collectively, the “Radoff-JEC Group”), intends to file a preliminary proxy statement and accompanying WHITE universal proxy card with the Securities and Exchange Commission (“SEC”) to be used to solicit votes for the election of its slate of highly qualified director nominees at the 2026 annual meeting of stockholders of Seer, Inc., a Delaware corporation (the “Company”).

THE RADOFF-JEC GROUP STRONGLY ADVISES ALL STOCKHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS, INCLUDING A PROXY CARD, AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR.

The participants in the anticipated proxy solicitation are expected to be The Radoff Family Foundation (“Radoff Foundation”), Bradley L. Radoff, JEC II Associates, LLC (“JEC II”), The MOS Trust (“MOS Trust”), MOS PTC, LLC (“MOS PTC”), Michael Torok, Howard H. Berman, Joshua S. Horowitz and Luis E. Rinaldini.

As of the date hereof, Radoff Foundation directly beneficially owns 500,000 shares of Class A Common Stock, par value $0.00001 per share, of the Company (“Common Stock”). As of the date hereof, Mr. Radoff directly beneficially owns 2,110,232 shares of Common Stock. Mr. Radoff, as a director of Radoff Foundation, may be deemed to beneficially own the 500,000 shares of Common Stock directly beneficially owned by Radoff Foundation, which, together with the 2,110,232 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 2,610,232 shares of Common Stock beneficially owned by Mr. Radoff. As of the date hereof, JEC II directly beneficially owns 1,167,296 shares of Common Stock. As of the date hereof, MOS Trust directly beneficially owns 215,000 shares of Common Stock. MOS PTC, as the trustee of MOS Trust, may be deemed to beneficially own the 215,000 shares of Common Stock directly beneficially owned by MOS Trust. As of the date hereof, Mr. Torok directly beneficially owns 285,000 shares of Common Stock. Mr. Torok, as the Manager of JEC II and a Manager of MOS PTC, may be deemed to beneficially own the 1,382,296 shares of Common Stock directly beneficially owned in the aggregate by JEC II and MOS Trust, which, together with the 285,000 shares of Common Stock he directly beneficially owns, constitutes an aggregate of 1,667,296 shares of Common Stock beneficially owned by Mr. Torok. As of the date hereof, each of Dr. Berman and Messrs. Horowitz and Rinaldini does not beneficially own any shares of Common Stock.

____________________

1 On March 13, 2026, the Company amended its Tax Benefit Preservation Plan, dated as of February 26, 2026 (the “Poison Pill”), to moot a stockholder’s challenge to the Poison Pill in the Delaware Court of Chancery.

2 Share price decline from December 4, 2020 through April 10, 2026, the trading day immediately prior to the Radoff-JEC Group’s submission of its initial non-binding proposal to acquire the Company.

3 The Company’s Form 10-K for the year ended December 31, 2025.

4 Reuters article (“Alamar Biosciences valued at $1.5 billion as shares jump in Nasdaq debut”) dated April 17, 2026.

5 Alamar Biosciences Form S-1 dated March 27, 2026.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260424350279/en/

Greg Lempel

greg@fondrenlp.com

Original: The Radoff-JEC Group Submits Improved Non-Binding Proposal to Acquire Seer, Inc.

Hot Features

Hot Features

glenn1919

4日前

glenn1919

4日前

iHub News

4日前

iHub News

4日前

Monksdream

1年前

Monksdream

1年前

メールアドレスで登録

メールアドレスで登録