0001843988

false

0001843988

2023-08-15

2023-08-15

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

8-K

CURRENT

REPORT

PURSUANT

TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date

of Report (Date of earliest event reported): August 15, 2023

two

(Exact

name of registrant as specified in its charter)

| Cayman

Islands |

|

001-40292 |

|

98-1577238 |

(State

or other jurisdiction

of

incorporation) |

|

(Commission

File Number) |

|

(IRS

Employer

Identification

No.) |

195

US HWY 50, Suite 208

Zephyr

Cove, NV 89448

(Address

of principal executive offices, including zip code)

Registrant’s

telephone number, including area code: (310) 954-9665

None

(Former

name or former address, if changed since last report)

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under

any of the following provisions:

| ☒ |

Written

communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of Each Class |

|

Trading

Symbol(s) |

|

Name

of Each Exchange on Which

Registered |

| Class

A ordinary shares, par value $0.0001 per share |

|

TWOA |

|

New

York Stock Exchange |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405

of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging

growth company ☒

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Item

8.01 Other Events.

On

August 15, 2023, two (NYSE: TWOA), a Cayman Islands exempted company (the “Company”), announced the execution

of a definitive business combination agreement (the “Business Combination Agreement”) with LatAm Logistic Properties

S.A., a company organized under the laws of Panama (“LLP”), for a proposed business combination (the “Business

Combination”). LLP is a leading developer, owner, and manager of institutional quality, class A industrial and logistics

real estate in Central and South America. Pursuant to the Business Combination Agreement, each of the Company and LLP will merge with

newly-formed subsidiaries of a to-be-formed holding company (“Pubco”), which will serve as the parent company

of each of the Company and LLP following the consummation of the Business Combination.

A

copy of the press release announcing the execution of the Business Combination Agreement is furnished as Exhibit 99.1 to this Current

Report on Form 8-K and is incorporated herein by reference.

Attached

as Exhibit 99.2 to this Current Report on Form 8-K and incorporated into this Item 8.01 by reference is the investor presentation that

will be used by the Company and LLP with respect to the transactions contemplated by the Business Combination Agreement.

Attached

as Exhibit 99.3 to this Current Report on Form 8-K and incorporated into this Item 8.01 by reference is the script to the video recording

of the investor presentation that was recorded by the Company and LLP with respect to the transactions contemplated by the Business Combination

Agreement. Please note that certain portions of the investor presentation were revised or updated for immaterial matters after the video

presentation was recorded, and in the event of any conflict between such script or video and the investor presentation attached as Exhibit

99.2 to this Current Report, investors should rely on the investor presentation attached as Exhibit 99.2 to this Current Report.

The

information in this Item 8.01, including Exhibits 99.1, 99.2 and 99.3, is furnished and shall not be deemed “filed” for purposes

of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject

to the liabilities under that section, and shall not be deemed to be incorporated by reference in any filing of the Company under the

Securities Act of 1933, as amended (the “Securities Act”), or the Exchange Act, regardless of any general incorporation

language in such filings. This Current Report on Form 8-K will not be deemed an admission as to the materiality of any information contained

in this Item 8.01, including Exhibits 99.1, 99.2 and 99.3.

Additional

Information About the Transaction and Where to Find It

This

Current Report on Form 8-K relates to a proposed Business Combination between the Company and LLP. This Current Report on Form 8-K does

not constitute an offer to sell or exchange, or the solicitation of an offer to buy or exchange, any securities, nor shall there be any

sale of securities in any jurisdiction in which such offer, sale or exchange would be unlawful prior to registration or qualification

under the securities laws of any such jurisdiction. In connection with the Business Combination, the parties intend to file with the

Securities and Exchange Commission (the “SEC”) a registration statement on Form F-4 (the “Registration Statement”),

which will include a preliminary proxy statement of the Company and a preliminary prospectus of Pubco, and after the Registration Statement

is declared effective, the Company will mail a definitive proxy statement/prospectus relating to the Business Combination to its shareholders.

This communication does not contain all the information that should be considered concerning the Business Combination and is not intended

to form the basis of any investment decision or any other decision in respect of the Business Combination. LLP’S AND THE COMPANY’S

SHAREHOLDERS AND OTHER INTERESTED PERSONS ARE ADVISED TO READ, WHEN AVAILABLE, THE PRELIMINARY PROXY STATEMENT/PROSPECTUS AND THE AMENDMENTS

THERETO AND THE DEFINITIVE PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS FILED IN CONNECTION WITH THE BUSINESS COMBINATION, AS THESE

MATERIALS WILL CONTAIN IMPORTANT INFORMATION ABOUT LLP, THE COMPANY, PUBCO AND THE BUSINESS COMBINATION. After the Registration Statement

is declared effective by the SEC, the definitive proxy statement/prospectus and other relevant materials for the Business Combination

will be mailed to shareholders of the Company as of a record date to be established for voting on the Business Combination. Shareholders

will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other

documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to:

two, 195 US HWY 50, Suite 208, Zephyr Cove, NV 89448; Tel: (310) 954-9665.

Participants

in the Solicitation

The

Company and its directors and executive officers may be deemed participants in the solicitation of proxies from the Company’s shareholders

with respect to the Business Combination. A list of the names of those directors and executive officers of the Company is contained in

the Company’s Current Reports on Form 8-K filed with the SEC on April 6, 2023 and May 3, 2023, which are available free of charge

at the SEC’s web site at www.sec.gov, or by directing a request to: two, 195 US HWY 50, Suite 208, Zephyr Cove, NV 89448; Tel:

(310) 954-9665. Additional information regarding the interests of such participants will be set forth in the Registration Statement when

available.

LLP

and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of

the Company in connection with the Business Combination. A list of the names of such directors and executive officers and information

regarding their interests in the Business Combination will be included in the Registration Statement when available.

Non-Solicitation

This

Current Report on Form 8-K does not constitute, and should not be construed to be, a proxy statement or the solicitation of a proxy,

solicitation of any vote or approval, consent or authorization with respect to any securities or in respect of the proposed Business

Combination described herein and shall not constitute an offer to sell or a solicitation of an offer to buy any securities nor shall

there be any sale of securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration

or qualification under the securities laws of any such state or jurisdiction. No offering of securities shall be made except by means

of a prospectus meeting the requirements of Section 10 of the Securities Act, or an exemption therefrom.

Forward-Looking

Statements

This

Current Report on Form 8-K contains certain statements that may be considered forward-looking statements within the meaning of federal

securities laws. Forward-looking statements include, without limitation, statements about future events or LLP’s, the Company’s

or Pubco’s future financial or operating performance. For example, statements regarding anticipated growth in the industry in which

LLP operates and anticipated growth in demand for LLP’s products and solutions, the anticipated size of LLP’s addressable

market and other metrics, statements regarding the benefits of the Business Combination, and the anticipated timing of the completion

of the Business Combination are forward-looking statements. In some cases, you can identify forward-looking statements by terminology

such as “pro forma,” “may,” “should,” “could,” “might,” “plan,”

“possible,” “project,” “strive,” “budget,” “forecast,” “expect,”

“intend,” “will,” “estimate,” “anticipate,” “believe,” “predict,”

“potential” or “continue,” or the negatives of these terms or variations of them or similar terminology.

These

forward-looking statements regarding future events and the future results of LLP and the Company are based on current expectations, estimates,

forecasts, and projections about the industry in which LLP operates, as well as the beliefs and assumptions of LLP’s management

and the Company’s management. These forward-looking statements are only predictions and are subject to known and unknown risks,

uncertainties, assumptions and other factors beyond LLP’s or the Company’s control that are difficult to predict because

they relate to events and depend on circumstances that will occur in the future. They are neither statements of historical fact nor promises

or guarantees of future performance. Therefore, LLP’s actual results may differ materially and adversely from those expressed or

implied in any forward-looking statements and LLP therefore cautions against relying on any of these forward-looking statements.

These

forward-looking statements are based upon estimates and assumptions that, while considered reasonable by LLP and its management, the

Company and its management, and Pubco and its management as the case may be, are inherently uncertain and are inherently subject to risks

variability and contingencies, many of which are beyond LLP’s, the Company’s or Pubco’s control. Factors that may cause

actual results to differ materially from current expectations include, but are not limited to: (i) the occurrence of any event, change

or other circumstances that could give rise to the termination of negotiations and any subsequent definitive agreements with respect

to the Business Combination; (ii) the outcome of any legal proceedings that may be instituted against LLP, the Company, Pubco or others

following the announcement of the Business Combination and any definitive agreements with respect thereto; (iii) the inability to complete

the Business Combination due to the failure to obtain consents and approvals of the shareholders of the Company, to obtain financing

to complete the Business Combination or to satisfy other conditions to closing, or delays in obtaining, adverse conditions contained

in, or the inability to obtain necessary regulatory approvals required to complete the transactions contemplated by the Business Combination

Agreement; (iv) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable

laws or regulations or as a condition to obtaining regulatory approval of the Business Combination; (v) LLP’s ability to manage

growth; (vi) the ability to meet stock exchange listing standards following the consummation of the Business Combination; (vii) the risk

that the Business Combination disrupts current plans and operations of LLP as a result of the announcement and consummation of the Business

Combination; (viii) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other

things, competition, the ability of Pubco or LLP to grow and manage growth profitably, maintain key relationships and retain its management

and key employees; (ix) costs related to the Business Combination; (x) changes in applicable laws, regulations, political and economic

developments; (xi) the possibility that LLP or Pubco may be adversely affected by other economic, business and/or competitive factors;

(xii) LLP’s estimates of expenses and profitability; (xiii) the failure to realize anticipated pro forma results or projections

and underlying assumptions, including with respect to estimated shareholder redemptions, purchase price and other adjustments; and (xiv)

other risks and uncertainties set forth in the filings by the Company or Pubco with the SEC. There may be additional risks that neither

LLP nor the Company presently know or that LLP and the Company currently believe are immaterial that could also cause actual results

to differ from those contained in the forward-looking statements. Any forward-looking statements made by or on behalf of LLP or the Company

speak only as of the date they are made. Neither LLP nor the Company undertakes any obligation to update any forward-looking statements

to reflect any changes in their respective expectations with regard thereto or any changes in events, conditions or circumstances on

which any such statement is based.

Nothing

in this Current Report on Form 8-K should be regarded as a representation by any person that the forward-looking statements set forth

herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place

undue reliance on forward-looking statements, which speak only as of the date they are made.

Item

9.01. Financial Statements and Exhibits.

| (d) |

Exhibits. |

| |

|

| |

The following exhibits are being filed herewith: |

SIGNATURE

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned hereunto duly authorized.

Dated:

August 15, 2023

| |

two |

| |

|

|

| |

By: |

/s/

Thomas Hennessy |

| |

Name: |

Thomas

Hennessy |

| |

Title: |

Chief

Executive Officer |

Exhibit 99.1

two

and LatAm Logistic Properties S.A. Agree to Combine, Creating a Leading Publicly Traded Developer, Owner, and Manager of Modern Logistics

Real Estate in Central and South America

● LatAm Logistic Properties is one of the only Institutional Industrial Platforms operating across the region, bringing the development of class A warehouses to undersupplied markets

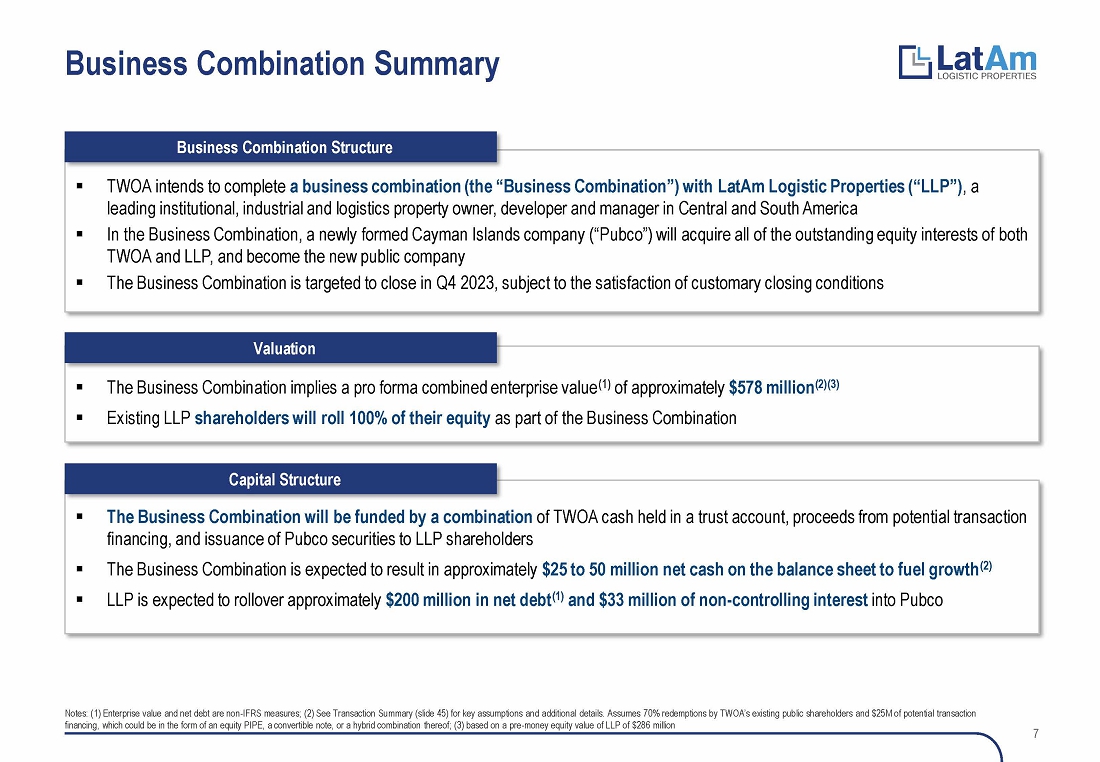

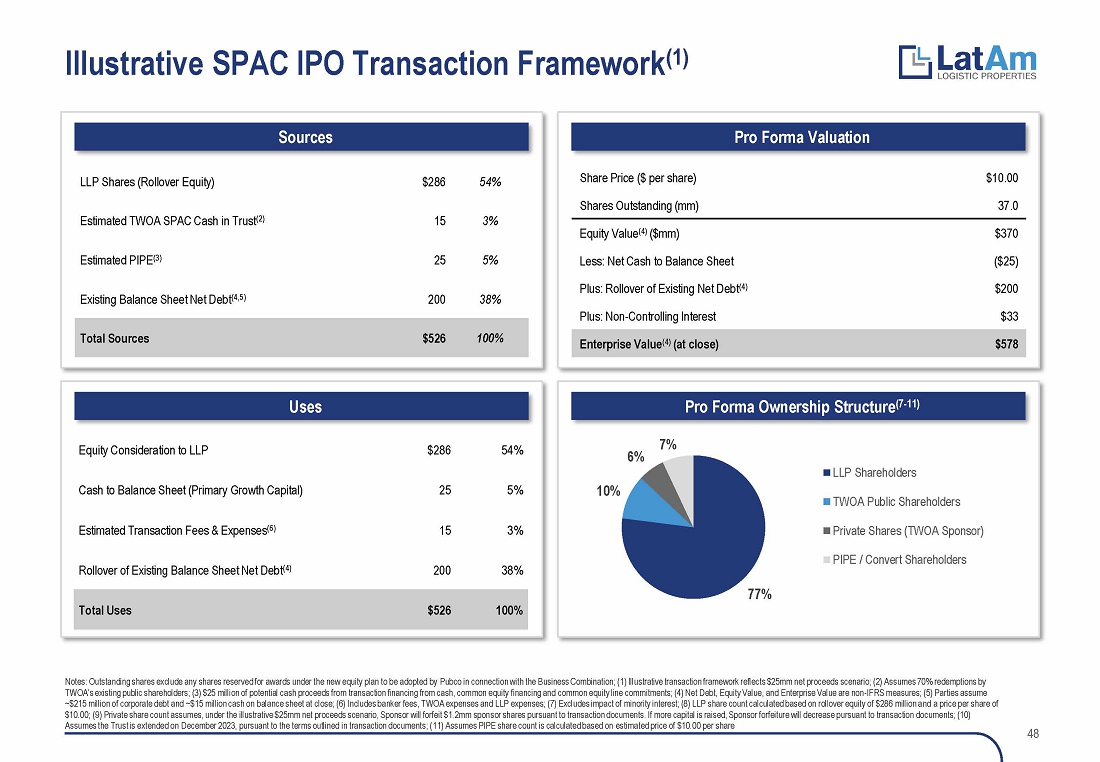

● Estimated post-transaction enterprise value of $578 Million based on a minimum of $25 Million in net cash proceeds to fund growth (assuming 70% redemptions from two’s trust account)

● LatAm Logistic Properties’ management will roll 100% of their existing shares into equity of the combined company

ZEPHYR

COVE, NV and SAN JOSÉ, COSTA RICA, August 15, 2023 – two (NYSE: TWOA) (“TWOA”), a special

purpose acquisition company, and LatAm Logistic Properties S.A. (d/b/a LatAm Logistic Properties) (“LLP”),

a leading developer, owner, and manager of institutional quality, class A industrial and logistics real estate in Central and South America,

have entered into a definitive business combination agreement (the “Business Combination Agreement”), pursuant to which LLP

would become publicly listed on a U.S. stock exchange.

Pursuant

to the Business Combination Agreement, each of LLP and TWOA will merge with newly-formed subsidiaries of a to-be-formed holding company

(“Pubco”) and Pubco will be the parent company of each of the Company and LLP following the consummation of the Business

Combination. Upon the closing of the transactions contemplated by the Business Combination Agreement (the “Business Combination”),

the ordinary shares of Pubco are expected to be listed on the New York Stock Exchange (“NYSE”) under the new ticker symbol

“LLP”. The Business Combination is expected to close in the fourth quarter of 2023, subject to regulatory and both companies’

shareholder approvals, among other customary closing conditions.

LLP

is one of the only vertically integrated logistics real estate platforms operating across Central and South America. LLP’s portfolio

consists of approximately 4.8 million square feet of operating gross leasable area (“GLA”) across a network of 28 facilities

in Costa Rica, Colombia, and Peru, primarily located in high-growth consumption centers with high barriers to entry. LLP’s properties

are designed and developed to offer greater accessibility, security, and maximum optionality, which provides cost efficiencies for its

multi-national and regional customers. With modern specifications, LLP is able to drive operational efficiencies in parallel with technology

advancements for timely delivery of goods, implementing forward-thinking operational processes that provide clients with best-in-class

service. Additionally, LLP’s properties comply with the highest standards of environmental sustainability with EDGE certifications,

a green building standard sponsored by the International Finance Corporation.

“We

believe LLP’s combination with TWOA is a transformational event that will position LLP to realize the massive opportunities driven

by the increased demand for logistics real estate across Central and South America,” said Esteban Saldarriaga, CEO of LLP. “LLP’s

well-established track-record of developing modern class A facilities in a cost-efficient manner provides a unique competitive advantage

to meet the new demand created by nearshoring and e-commerce. We are excited to enter this next phase in our history through the transaction

with TWOA, which will allow us to further capitalize on the macro tailwinds benefiting logistics warehouse facilities. We expect to continue

building out our strong platform across existing and new adjacent geographies with US dollar denominated markets. We believe a NYSE listing

will enable us to secure access to resources to fund these growth opportunities and position LLP for the future.”

Thomas

D. Hennessy, Chairman and CEO of TWOA, commented: “Industrial real estate continues to attract significant capital inflows due

to the macroeconomic tailwinds supporting logistics and distribution demand. As one of the only vertically integrated logistics operating

platforms in its regions, LLP is a dominant player in Central and South America. LLP’s class A US institutional asset quality,

predictable cash flows, growth prospects, and management team’s strong track record offer a compelling opportunity. We are thrilled

to partner with LLP and enter into this business combination.”

Upon

closing of the Business Combination, the senior leadership of Pubco will consist of Thomas McDonald, as Chairman; Esteban Saldarriaga,

as CEO; and Annette Fernández, as CFO.

Transaction

Terms & Financing

The

combined company will have an estimated post-transaction enterprise value of $578 million, based on a pre-money equity value of LLP of

$286 million, with a minimum of $25 million in net cash proceeds from the Business Combination and assuming 70% redemptions by TWOA’s

existing public shareholders. Net proceeds raised from the Business Combination will be used to fund future growth opportunities.

The

Business Combination Agreement has been unanimously approved by the Boards of Directors of both LLP and TWOA.

For

a summary of the material terms of the Business Combination Agreement, as well as a supplemental investor presentation, please see TWOA’s

Current Report on Form 8-K to be filed with the U.S. Securities and Exchange Commission (the “SEC”). Additional information

about the proposed Business Combination will be described in Pubco’s registration statement on Form F-4 to be filed with the SEC,

which will include a proxy statement/prospectus. Pubco and TWOA also will file other documents regarding the proposed Business Combination

with the SEC.

Advisors

BTG

Pactual is acting as exclusive M&A advisor to LLP. Cohen & Company Capital Markets, a division of J.V.B. Financial Group, LLC

(“CCM”), is acting as exclusive financial advisor and lead capital markets advisor to TWOA. Baker & McKenzie LLP is acting

as U.S. counsel to LLP. Ellenoff Grossman & Schole LLP is acting as U.S. counsel to TWOA. Gateway Group is acting as investor relations

advisors to both TWOA and LLP. Dukas Linden Public Relations is acting as public relations advisors to both TWOA and LLP.

Webcast

Information

TWOA

and LLP management will host a webcast to discuss the proposed Business Combination today, August 15, 2023, at 8:00 a.m. Eastern time.

The webcast will be accompanied by a detailed investor presentation. The investor presentation will be available at www.latamlp.com

and www.twoaspac.com.

Date:

August 15, 2023

Time:

8:00 a.m. Eastern time

The

conference call will be broadcast live here. To dial in via telephone see details below.

Toll-free

dial-in number: (800) 715-9871

International

dial-in number: (646) 307-1963

Conference

ID: 6625255

Please

dial the conference telephone number 5 to 10 minutes prior to the start time. An operator will register your name and organization. If

you have any difficulty connecting with the conference call, please contact Gateway Group at (949) 574-3860.

A

recorded replay of the conference call will be available here after 12:00 p.m. Eastern time today,

and

at www.latamlp.com and www.twoaspac.com.

About

LatAm Logistic Properties

LatAm

Logistic Properties, S.A. is a leading developer, owner, and manager of institutional quality, class A industrial and logistics real

estate in Central and South America. LLP’s customers are multinational and regional e-commerce retailers, third-party logistic

operators, business-to-business distributors, and retail distribution companies. LLP’s strong customer relationships and insight

is expected to enable future growth through the development and acquisition of high-quality, strategically located facilities in its

target markets. As of June 30, 2023, LLP consisted of an operating and development portfolio of twenty-eight logistic facilities in Colombia,

Peru and Costa Rica, totaling more than 650,000 square meters of gross leasable area.

About

two

two

is a special purpose acquisition company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition,

stock purchase, reorganization or similar business combination with one or more businesses. For more information, visit twoaspac.com.

Forward-Looking

Statements

This

communication contains certain forward-looking information with respect to the Business Combination, which may not be included in future

public filings or investor guidance. The inclusion of financial statements or metrics in this communication should not be construed as

a commitment by LLP, Pubco or TWOA to provide guidance on such information in the future. Certain statements in this communication may

be considered forward-looking statements within the meaning of federal securities laws. Forward-looking statements include, without limitation,

statements about future events or LLP’s, TWOA’s or Pubco’s future financial or operating performance. For example,

statements regarding anticipated growth in the industry in which LLP operates and anticipated growth in demand for LLP’s products

and solutions, the anticipated size of LLP’s addressable market and other metrics, statements regarding the benefits of the Business

Combination, and the anticipated timing of the completion of the Business Combination are forward-looking statements. In some cases,

you can identify forward-looking statements by terminology such as “pro forma,” “may,” “should,”

“could,” “might,” “plan,” “possible,” “project,” “strive,” “budget,”

“forecast,” “expect,” “intend,” “will,” “estimate,” “anticipate,”

“believe,” “predict,” “potential” or “continue,” or the negatives of these terms or variations

of them or similar terminology.

These

forward-looking statements regarding future events and the future results of LLP, Pubco and TWOA are based on current expectations, estimates,

forecasts, and projections about the industry in which LLP operates, as well as the beliefs and assumptions of LLP’s management.

These forward-looking statements are only predictions and are subject to known and unknown risks, uncertainties, assumptions and other

factors beyond LLP’s, Pubco’s or TWOA’s control that are difficult to predict because they relate to events and depend

on circumstances that will occur in the future. They are neither statements of historical fact nor promises or guarantees of future performance.

Therefore, LLP’s and Pubco’s actual results may differ materially and adversely from those expressed or implied in any forward-looking

statements and LLP, Pubco and Two therefore cautions against relying on any of these forward-looking statements.

These

forward-looking statements are based upon estimates and assumptions that, while considered reasonable by LLP and its management, TWOA

and its management, and Pubco and its management, as the case may be, are inherently uncertain and are inherently subject to risks variability

and contingencies, many of which are beyond LLP’s, TWOA’s or Pubco’s control. Factors that may cause actual results

to differ materially from current expectations include, but are not limited to: (i) the occurrence of any event, change or other circumstances

that could give rise to the termination of negotiations and any subsequent definitive agreements with respect to the Business Combination;

(ii) the outcome of any legal proceedings that may be instituted against LLP, TWOA, Pubco or others following the announcement of the

Business Combination and any definitive agreements with respect thereto; (iii) the inability to complete the Business Combination due

to the failure to obtain consents and approvals of the shareholders of TWOA, to obtain financing to complete the Business Combination

or to satisfy other conditions to closing, or delays in obtaining, adverse conditions contained in, or the inability to obtain necessary

regulatory approvals required to complete the transactions contemplated by the business combination agreement; (iv) changes to the proposed

structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition

to obtaining regulatory approval of the Business Combination; (v) LLP’s and Pubco’s ability to manage growth; (vi) the ability

to meet stock exchange listing standards following the consummation of the Business Combination; (vii) the risk that the Business Combination

disrupts current plans and operations of LLP as a result of the announcement and consummation of the Business Combination; (viii) the

ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition,

the ability of Pubco or LLP to grow and manage growth profitably, maintain key relationships and retain its management and key employees;

(ix) costs related to the Business Combination; (x) changes in applicable laws, regulations, political and economic developments; (xi)

the possibility that LLP or Pubco may be adversely affected by other economic, business and/or competitive factors; (xii) LLP’s

estimates of expenses and profitability; and (xiii) other risks and uncertainties set forth in the filings by TWOA or Pubco with the

SEC. There may be additional risks that neither LLP nor TWOA presently know or that LLP and TWOA currently believe are immaterial that

could also cause actual results to differ from those contained in the forward-looking statements. Any forward-looking statements made

by or on behalf of LLP, TWOA or Pubco speak only as of the date they are made. None of LLP, Pubco or TWOA undertakes any obligation to

update any forward-looking statements to reflect any changes in their respective expectations with regard thereto or any changes in events,

conditions or circumstances on which any such statement is based. Accordingly, attendees and recipients should not place undue reliance

on forward-looking statements due to their inherent uncertainty.

Nothing

in this communication should be regarded as a representation by any person that the forward-looking statements set forth herein will

be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance

on forward-looking statements, which speak only as of the date they are made.

LLP,

TWOA and Pubco disclaim any and all liability for any loss or damage (whether foreseeable or not) suffered or incurred by any person

or entity as a result of anything contained or omitted from this communication and such liability is expressly disclaimed. The recipient

agrees that it shall not seek to sue or otherwise hold LLP, TWOA, Pubco or any of their respective directors, officers, employees, affiliates,

agents, advisors or representatives liable in any respect for the provision of this communication, the information contained in this

communication, or the omission of any information from this communication. Only those particular representations and warranties of LLP,

Pubco or TWOA made in a definitive written agreement regarding the Business Combination (which will not contain any representation or

warranty relating to this communication), when and if executed, and subject to such limitations and restrictions as specified therein,

shall have any legal effect.

Industry

and Market Data

This

communication also contains estimates and other statistical data made by independent parties which they believe to be reliable and by

LLP relating to market size and growth and other data about LLP’s industry. This data involves a number of assumptions and limitations,

and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions, and estimates of the future

performance of the markets in which LLP operates are necessarily subject to a high degree of uncertainty and risk. LLP has not independently

verified the accuracy or completeness of the independent parties’ information. No representation is made as to the reasonableness

of the assumptions made within or the accuracy or completeness of such independent information.

Trademarks

LLP

owns or has rights to various trademarks, service marks and trade names used is connection with the operation of its business. This communication

may also contain trademarks, service marks, trade names and copyrights of other companies or third parties, which are the property of

their respective owners. LLP’s use thereof does not imply an affiliation with, or endorsement by, the owners of such trademarks,

service marks, trade names and copyrights. Solely for convenience, some of the trademarks, service marks, trade names and copyrights

referred to in this communication may be listed without the TM, SM or symbols, but LLP will assert, to the fullest extent under applicable

law, the rights of the applicable owners to these trademarks, service marks, trade names and copyrights.

Additional

Information

This

communication relates to the Business Combination. This communication does not constitute an offer to sell or exchange, or the solicitation

of an offer to buy or exchange, any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, sale

or exchange would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. In connection

with the Business Combination, Pubco intends to file with the SEC a registration statement on Form F-4 containing a preliminary proxy

statement of TWOA and a preliminary prospectus of Pubco, and after the registration statement is declared effective, TWOA will mail a

definitive proxy statement/prospectus relating to the Business Combination to its shareholders. This communication does not contain all

the information that should be considered concerning the Business Combination and is not intended to form the basis of any investment

decision or any other decision in respect of the Business Combination. LLP’s and TWOA’s shareholders and other interested

persons are advised to read, when available, the preliminary proxy statement/prospectus and the amendments thereto and the definitive

proxy statement/prospectus and other documents filed in connection with the Business Combination, as these materials will contain important

information about LLP, TWOA, Pubco and the Business Combination. When available, the definitive proxy statement/prospectus and other

relevant materials for the Business Combination will be mailed to shareholders of TWOA as of a record date to be established for voting

on the Business Combination. Shareholders will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive

proxy statement/prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov,

or by directing a request to: two, 195 US HWY 50, Suite 208, Zephyr Cove, NV 89448; Tel: (310) 954-9665.

Participants

in the Solicitation

TWOA

and its directors and executive officers may be deemed participants in the solicitation of proxies from TWOA’s shareholders with

respect to the Business Combination. A list of the names of those directors and executive officers and a description of their interests

in TWOA is contained in TWOA’s filings with the SEC, which are available free of charge at the SEC’s web site at www.sec.gov,

or by directing a request to: two, 195 US HWY 50, Suite 208, Zephyr Cove, NV 89448; Tel: (310) 954-9665. Additional information regarding

the interests of such participants will be contained in the proxy statement/prospectus for the Business Combination when available.

LLP,

Pubco and their respective directors and executive officers may also be deemed to be participants in the solicitation of proxies from

the shareholders of TWOA in connection with the Business Combination. A list of the names of such directors and executive officers and

information regarding their interests in the Business Combination will be included in the proxy statement/prospectus for the Business

Combination when available.

Investor

Relations Contact:

Gateway

Group, Inc.

Cody

Slach, Matthew Hausch

(949)

574-3860

TWOA@gateway-grp.com

two

Contact:

Nick

Geeza

Chief

Financial Officer

ngeeza@hennessycapitalgroup.com

Media

Relations Contact:

Zach

Kouwe / Kendal Till

Dukas

Linden Public Relations for LatAm Logistic Properties S.A.

+1

646-722-6533

LLP@dlpr.com

Exhibit 99.2

Exhibit

99.3

Script

to Video Recording of the Investor Presentation

Operator

Welcome

to the “two” business combination announcement call. The slide presentation on today’s webcast has been

made available for download.

The

presentation can be found in two’s Current Report on Form 8-K at the website of the U.S. Securities and Exchange Commission at

www.sec.gov. A copy of the business combination agreement will be filed in two’s Current Report on Form 8-K within

four business days after the signing of business combination agreement. The presentation is also available for download on two’s

website at www.twoaspac.com as well as on LatAm Logistics Properties’ website at www.latamlp.com. Today’s call has

been prerecorded and will not include a Q&A session.

Before

we begin, let me remind you that some information provided during this webcast may include forward-looking statements that are based

on estimates and assumptions that, while considered reasonable by LatAm Logistics Properties and two, are subject to risks,

uncertainties, contingencies and other factors which could cause actual results to differ materially from those expressed or implied

by such forward-looking statements. Some of such statements reference financial information of LatAm Logistics Properties, which have

not been audited or reviewed by LatAm Logistics Properties’ auditors, are subject to a wide variety of significant business, economic

and competitive risks and uncertainties, and should not be relied upon as being necessarily indicative of future results. Nothing in

this webcast should be regarded as a representation by any person that the forward-looking statements will be achieved or that any of

the contemplated results of such forward-looking statements will be achieved. We encourage you to carefully review the disclaimers in

the slide presentation.

Forward-looking

statements made on this call are as of August 15, 2023, and we undertake no duty to update them as actual events unfold. Today’s

remarks also include certain non-GAAP financial measures. You can find a reconciliation of such measures in the table included in the

slide presentation.

I

would like to remind everyone that this webcast will be available for replay starting at approximately 12:00 pm ET this afternoon. The

webcast replay is available via the link provided in today’s press release, as well as on two’s website at www.twoaspac.com.

Now,

I would like to turn the call over to the CEO of two, Tom Hennessy. Tom?

Tom

Hennessy

Slide

4

We

are pleased to be here with you today to discuss the proposed business combination of TWO and LatAm Logistic Properties or LLP. I’m

Tom Hennessy, and I serve as the CEO of Two and I’m joined by my partner and CFO, Nick Geeza and from LLP – Esteban Saldarriaga,

the CEO and Annette Fernandez, the CFO.

We

have an exciting and comprehensive 35-minute presentation today. We look forward to sharing it with you.

For

1x1 [We have a 35-minute presentation so we will have ample opportunity for Q&A at the end, but feel free to interrupt us as we go

along.]

Slide

5

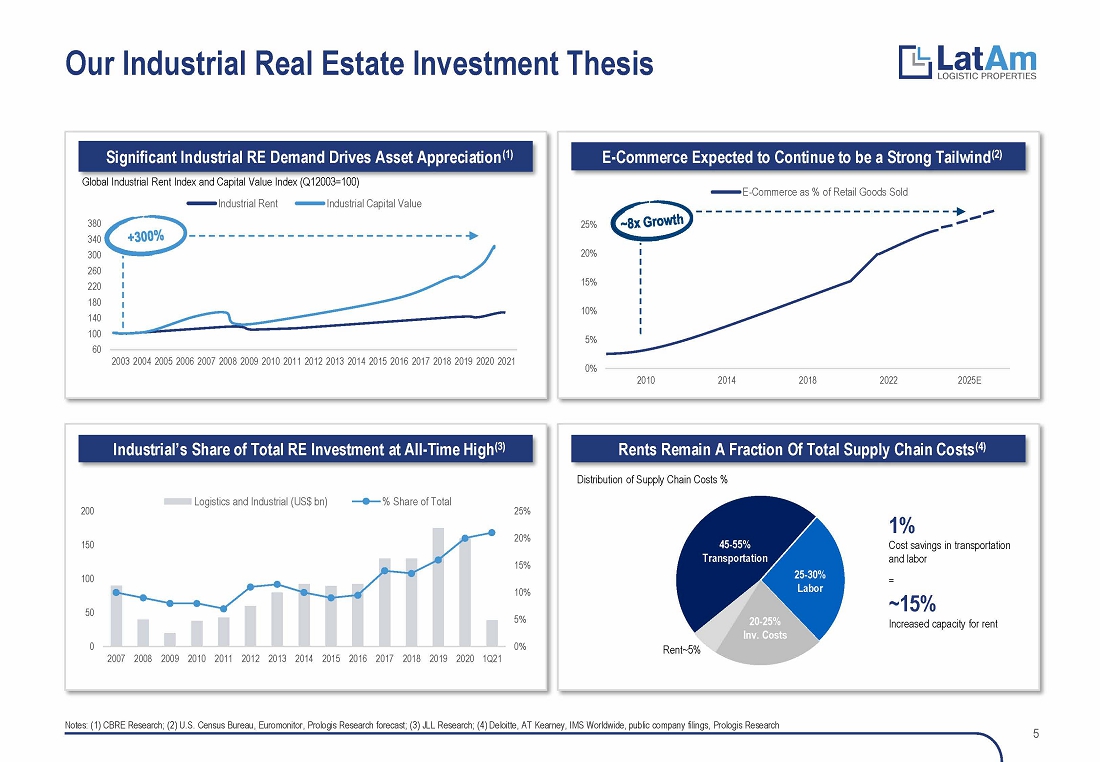

Before

I turn it over to the LLP team, I’d like to take a few minutes to share our industrial real estate investment thesis.

We

have spent a considerable amount of time studying industrial real estate because as the top left chart shows, industrial capital values

have grown over 300% over the past 20 years. This is driven, in large part, by e-commerce, or the Amazon effect or in South America,

the Mercado Libre effect, as shown on the top right. E-commerce relies on class A industrial logistics warehouses and sophisticated distribution

operations. This demand will continue to be a tailwind for industrial asset values.

On

the bottom left, capital inflows follow macro tailwinds. For example, nearly 1 in 4 dollars is now being deployed into U.S. industrial

real estate, up from 1 in 10 dollars, 15 years ago. In other words, industrial RE is taking significant marketshare from other real estate

asset classes like office or retail. Finally, on the bottom right, we think industrial RE has a long runway and lots of room to grow.

Industrial rents remain a fraction of total supply chain costs at only 5%. Meaning rents can grow meaningfully without materially affecting

the profit margins of tenants.

The

global industrial logistics opportunity is massive.

Slide

6

Latam

Logistic Properties is the leading developer, owner and manager of industrial real estate of Class A international institutional quality

in Central and South America. We selected LLP because LLP checks all of our boxes. Number 1, OPERATING MODEL, LLP is the only vertically

integrated logistics operator across multiple markets. Number 2, MARKET POSITION, they are the proven market leader with coveted multinational,

investment grade tenants. Number 3, BUSINESS PLAN. LLP has an attainable business plan with long-term lease contracts. Their business

plan is anchored by a durable competitive advantage through a landbank, tenant pipeline and operating expertise. Number 4, FINANCIAL

PROFILE. LLP has predictable cash flows, proven profit margins and unit economics. Number 5, TEAM. the Company has an accomplished leadership

team with deep industrial and logistics industry expertise. I believe that you will find LLP to be a compelling investment opportunity.

Slide

7

Regarding

the transaction and closing timeline.

●

We expect to close prior to YE 2023 and post-closing, LLP will be listed on NYSE.

On

Valuation…

●

The transaction implies a pro forma enterprise value of $578 million, equating to a 6.5% cap rate based on contracted 2023E NOI.

On

Capital Structure…

●

We have structured the deal to align incentives with our public investors, and to ensure deal certainty. Post-closing, we expect LLP

to be capitalized to fund the future growth opportunities that management will walk through shortly.

Slide

8

With

that, I’m very pleased to introduce Esteban and Annette.

Esteban

Saldarriaga

Slide

8

Thank

you very much, Tom.

| |

● |

My

name is Esteban Saldarriaga, and I am Chief Executive Officer of LatAm Logistics Properties, or LLP for short. Our company is a leading

logistics real estate platform, and I have been involved with it almost since its inception back in 2015. |

| |

|

|

| |

● |

To

start off, I can speak briefly about my background, which lies at the intersection of professional investing and real estate. |

| |

○ |

For

the better part of the last decade, I’ve worked in the Investments Team of Jaguar Growth Partners, a global private equity

firm led by the former CEO of Equity International, with a deep trajectory in real estate operating companies, primarily in the logistics

segment. |

| |

|

|

| |

○ |

Before

that, I held banking and investing roles at major institutions in Latin America, where I had the chance to work in many cross-border

transactions in countries such as Colombia, Peru, Ecuador, Chile and Brazil, among others, AND in multiple sectors, including real

estate, infrastructure and other hard-asset industries. |

Slide

9

| |

● |

Allow

me to first set the table by defining who we are as company. |

| |

● |

LLP

is a leading developer, owner, and manager of Class A logistics real estate in Central and South America. |

| |

|

|

| |

● |

LLP

is the only institutional, and vertically integrated, industrial platform operating across our region. |

| |

|

|

| |

● |

As

a relevant reference, our portfolio assets look like the ones in this picture. |

| |

○ |

Here

you can see one of our logistics parks in Colombia. |

| |

○ |

This

is a big reason why the largest companies in the world choose us, as you’ll see later in the presentation. |

Slide

10

| |

● |

From

a 30-thousand-foot view, LLP is a full service, real estate operating company, catering to markets where no other international player

has been able to achieve scale. |

| |

|

|

| |

● |

We

have taken the time and effort to build a network that currently operates in three countries: Costa Rica, Colombia and Peru. This

is not easy to replicate, and we have internalized this process and made it second nature for us. |

| |

○ |

Roughly

speaking, we have almost five million square feet (or half a million square meters) of operating gross leasable area, or GLA, and

owned or controlled landbank that can take us up to seven million square feet. |

| |

|

|

| |

○ |

Amid

what others might perceive as a challenging backdrop, we have successfully reached approximately 36 million dollars of Net Operating

Income under contract. |

| |

|

|

| |

○ |

And,

we have done so, achieving industry-leading occupancy metrics… built on the back of long-term leases, out of which almost

80%, are denominated in US dollars. |

| |

○ |

The

answer is that we believe our company is at an inflection point where, the macroeconomic effects from nearshoring and e-commerce

are coupling with LLP’s established franchise… and this can be expanded to adjacent markets in the Americas, in hand

with the growth of our tenants. |

Slide

11

| |

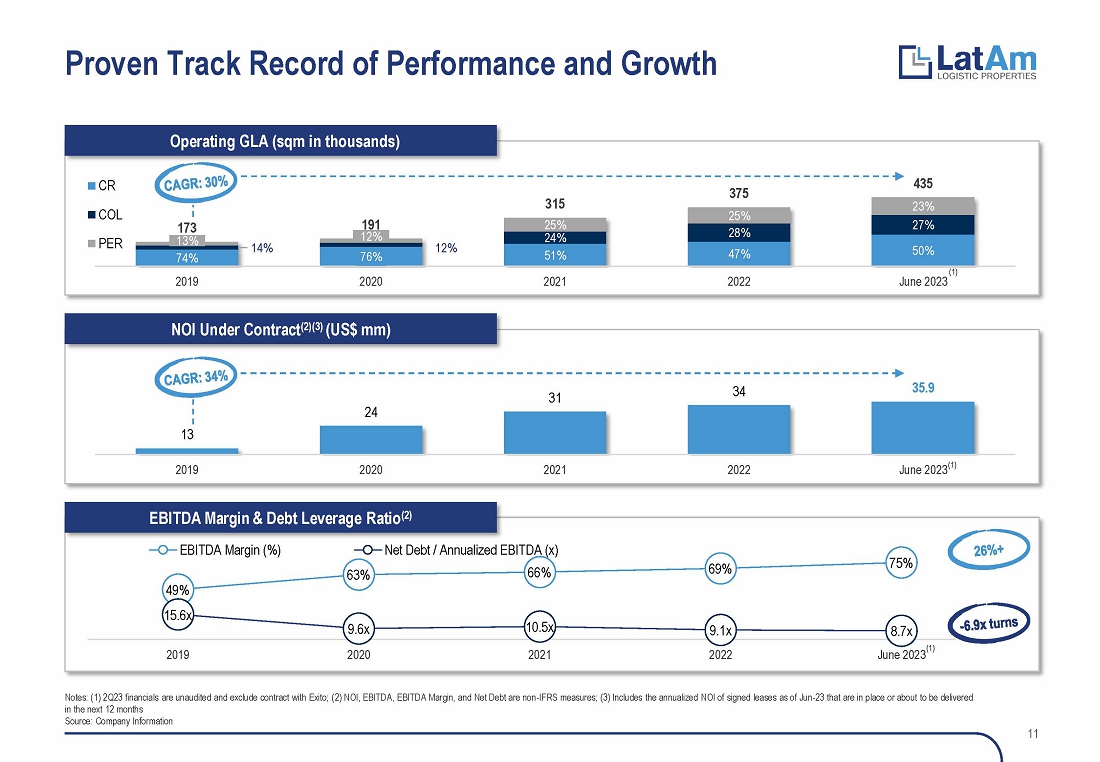

● |

We

have a meaningful track-record of performance. Our growth over the last few years speaks volumes to the embedded dynamics of the

countries we operate in, which are deeply underserved and underpenetrated. |

| |

○ |

We

have multiplied our occupied GLA by 2.5 times since 2019, equating to a compounded annual growth rate of approximately 30%, and in

the same period we have almost tripled our NOI. |

| |

|

|

| |

○ |

As

brought up earlier, most of our NOI is dollarized, and we want to manage our company to keep it that way. |

| |

○ |

Moreover,

we are beginning to see the effects of economies of scale, materialized in our growing EBITDA margins and progressive deleveraging,

typical of a high-growth platform. |

Slide

12

| ● | As

we see on this page. Our new buildings are up to institutional specifications, both inside

and outside, similar to what you can find in the most competitive U.S. markets. |

|

○ | We

have the know-how and capabilities to develop high quality specs in a cost-effective way. |

| ● | Everything

we develop looks like this. Our spaces are characterized by: |

| |

○ |

Minimum

clearing heights of 39 feet throughout the building. |

| |

○ |

Optimized

column spacing to maximize racking layout. |

| |

○ |

Structures

ready to incorporate systems that are compliant with the National Fire Protection Association guidelines. |

| |

○ |

Extra

flat floors with high load capacities. |

| |

○ |

Energy-saving

skylights. |

| |

○ |

And

acoustic and thermal insulation on the roofs. |

Slide

13

| ● | Moving

on to the outside, we have several defining features. |

| |

○ |

While

other mom-and-pop players seek to maximize land coverage, they do so at the expense of having ample truck courts, an adequate number

of parking spaces and appropriate door-to-area ratios. |

| |

○ |

Important

to note as well, we incorporate amenities for our tenants’ employees who work on site. This brings higher work satisfaction

and lowers clients’ headcount turnover. |

| |

● |

Let

me point out that our space is full of optionality, since multiple types of users are suitable for any given space. |

| |

|

|

| |

● |

That

is because our assets are core distributions centers, as opposed to highly specialized manufacturing facilities. From a risk-adjusted

viewpoint, we think we can create a premium since our warehouses are not irreversibly, or uneconomically, customized to any single

tenant. |

| |

|

|

| |

● |

So…

what do these specifications mean for our clients: … it all comes down to efficiency. We can offer up to 67% more pallet positions

per unit of GLA than existing warehouses in our markets. |

| |

|

|

| |

● |

The

simple summary: lower real estate occupancy costs for any given volume of merchandise. |

Slide

14

| |

● |

Moving

over to the next page, we believe we are bringing a differentiated company to the public market landscape. |

| |

● |

We

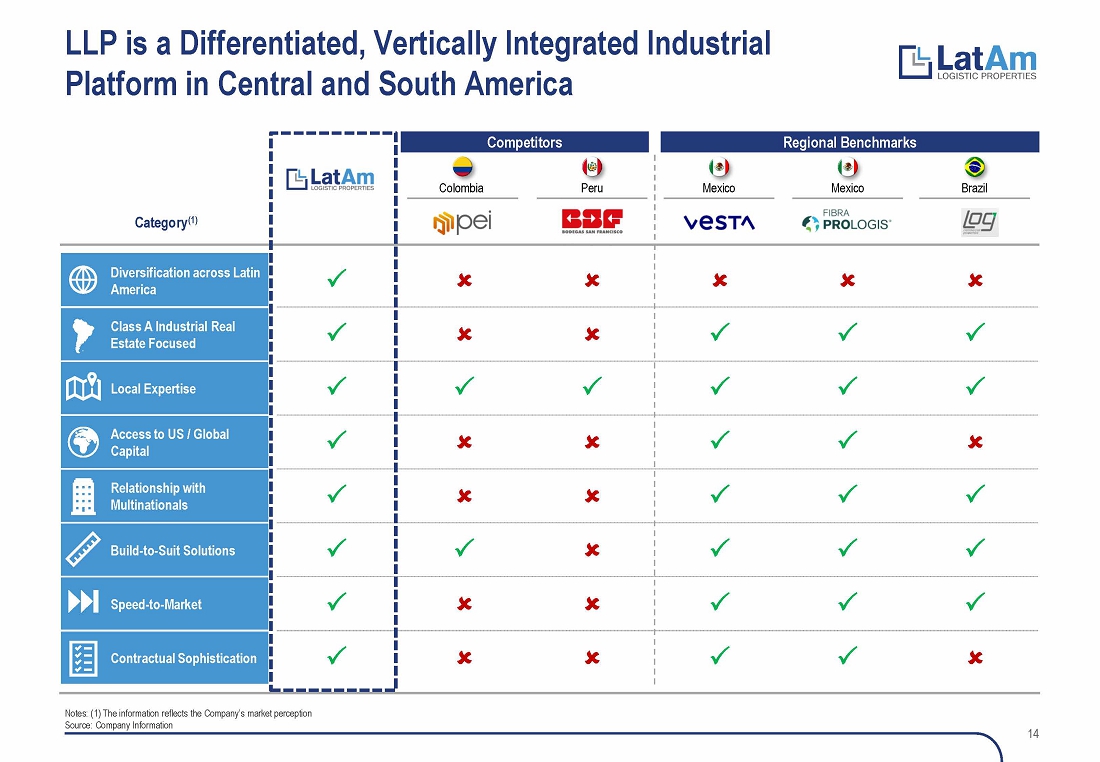

compare favorably with other players in the industrial space in Latin America, |

| |

○ |

First,

LLP is the only vertically integrated company with a multi-country footprint, |

| |

○ |

We

have a keen focus on Class A logistics property, not specialized industrial or manufacturing buildings, |

| |

○ |

We

bring local expertise but retain global access to capital as well as strong relationships with multinational tenants, |

| |

○ |

Fourth,

we offer built-to-suit solutions that not only require development know-how, but also financial expertise. |

| |

○ |

Lastly,

as a company of less than 30 employees in total, we are nimble with our speed to market capabilities and bring to bear the contractual

sophistication present in more developed markets. |

Slide

15

| ● | Transitioning

to our next section… LLP’s Investment Thesis. |

Slide

16

| ● | Our

strategy is straightforward: |

|

○ | We

want to participate in high growth markets, which are quite underserved, and |

|

○ | Keep

proximity to major cities, ports, and airports, with good access to labor for our clients. |

| ● | This

way, we believe, will set our platform for success. |

Slide

17

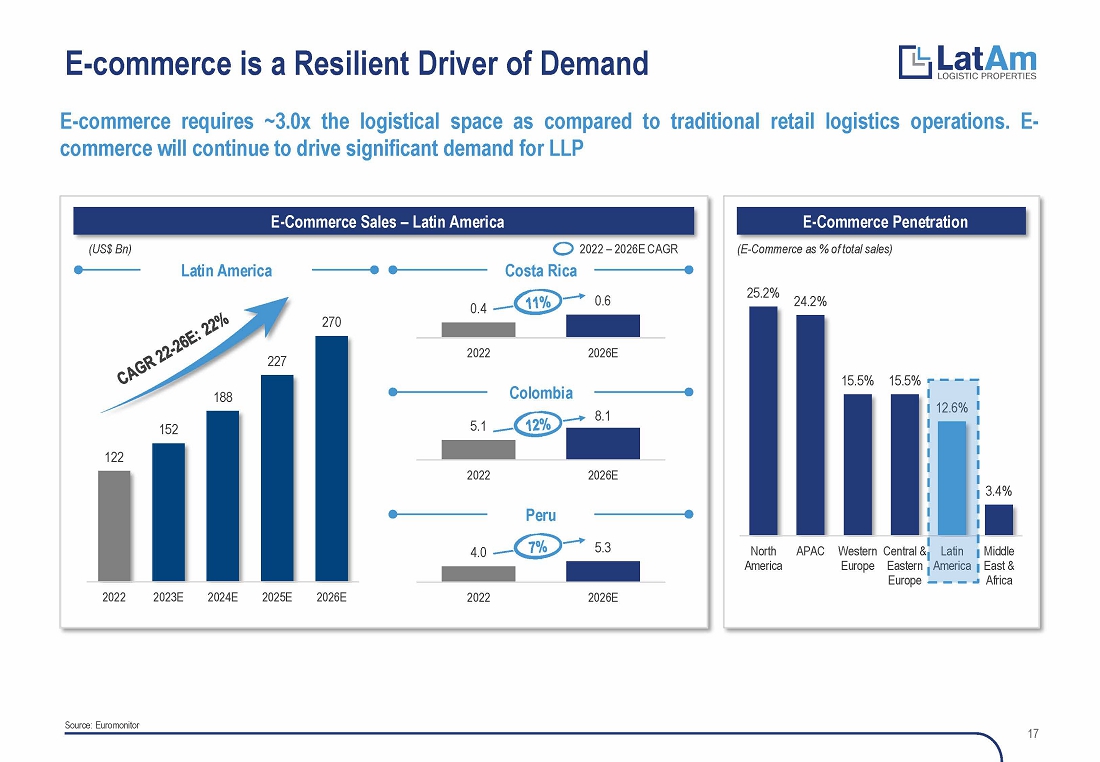

| ● | As

we look through the fundamentals, we can see that e-commerce and nearshoring will be powerful

forces that shape our demand. |

| ○ | Shown

on the left, E-commerce structurally accelerated with the pandemic, expanding at double digit

pace, in markets where penetration is still in its infancy. |

| | | |

| ○ | Players

like Mercado Libre, the Latin American Amazon, are expanding like never before, and traditional

retailers and not standing still either: their omnichannel strategies are also crystallizing

demand for us. |

| | | |

| ○ | Additionally,

there are two less known, but fundamental, aspects that compound to LLP’s benefit: |

| ● | First,

sophisticated operations in today’s digital commerce require modern space and lager

formats, creating a flight to quality away from our local competitors. |

| | | |

| ● | And

secondly, E-commerce uses three (3) times as much logistics space as brick-and-mortar does.

This is due to several factors, such as greater product variety, reverse logistics for exchanges

and returns, and the shift towards direct-to-consumer distribution models. |

Slide

18

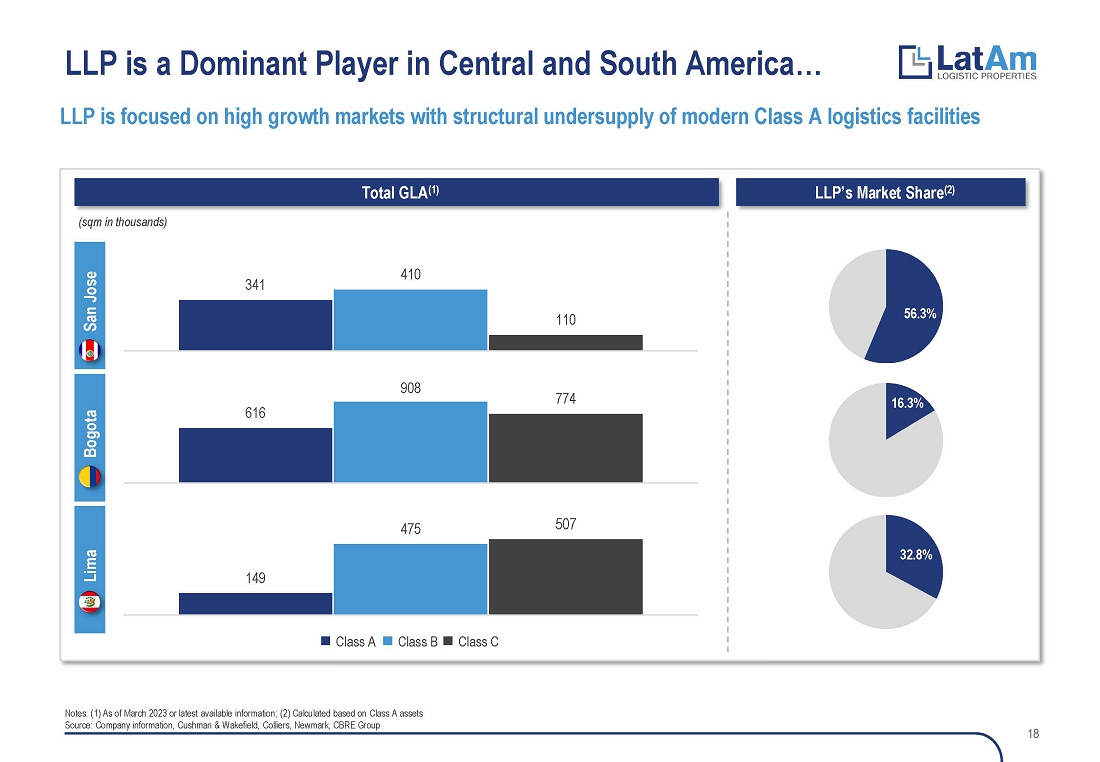

| ● | Moreover,

on the next slide, you can see that LLP is a dominant player in the undersupplied markets

where we operate. |

| ○ | We

have captured the lion share of class A warehouses in capital cities like San Jose, Bogota

and Lima. |

Slide

19

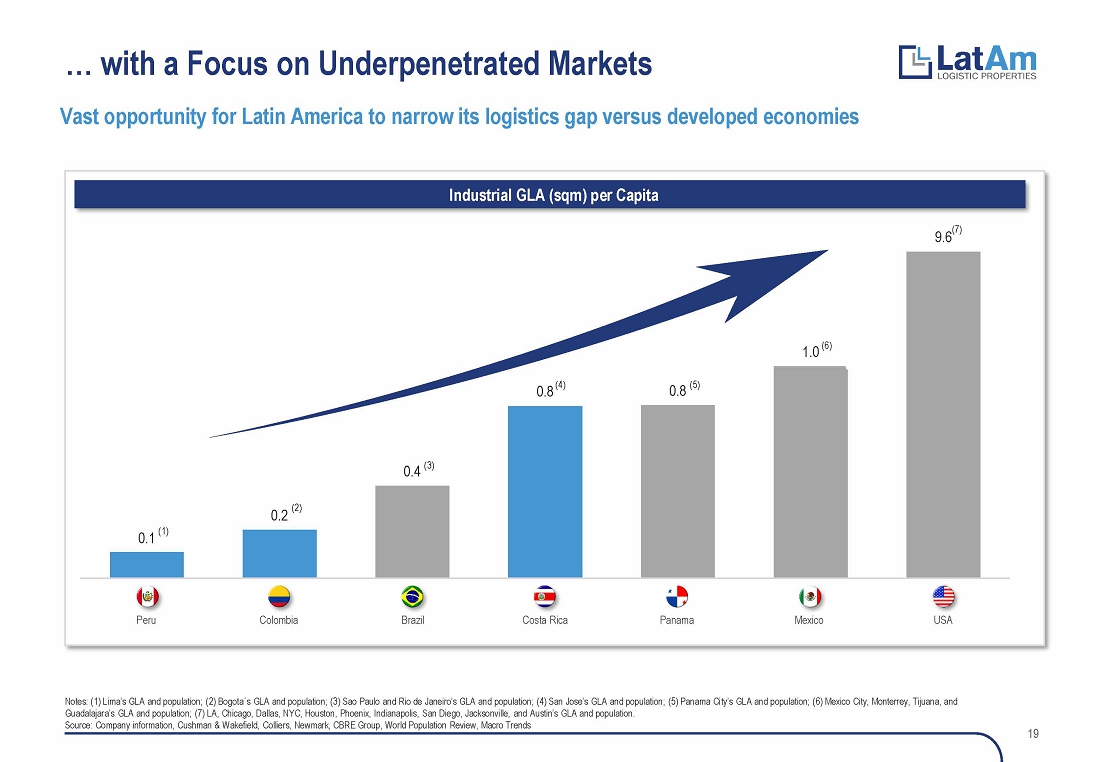

| ○ | And

simultaneously, Central and South America are way behind more developed markets in terms

of logistics GLA per capita, which reveals a major opportunity for us to close that gap. |

Slide

20

| ● | Also,

from a macroeconomic standpoint, middle-class consumption growth is a key propellant in our

markets. |

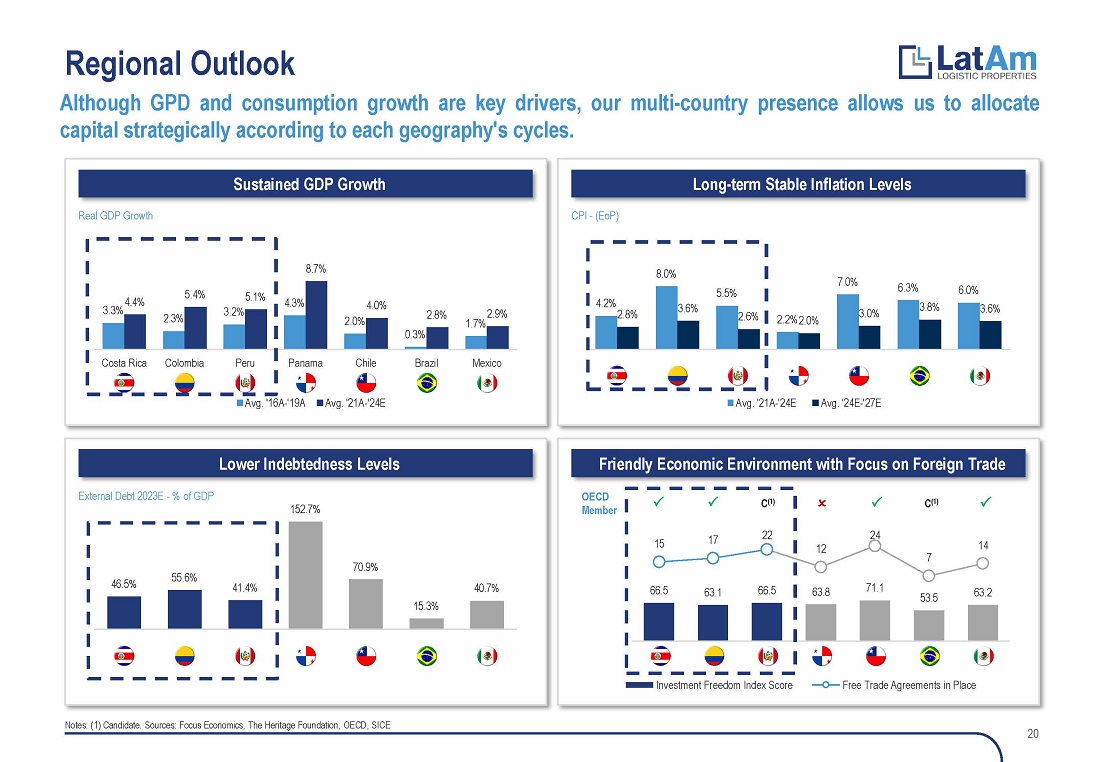

| ○ | We

benefit from sustained GDP growth, as seen on the top left chart. |

| ○ | And

equally important, trade-driven economic policies seek to capitalize on nearshoring trends. |

Slide

21

| ● | This

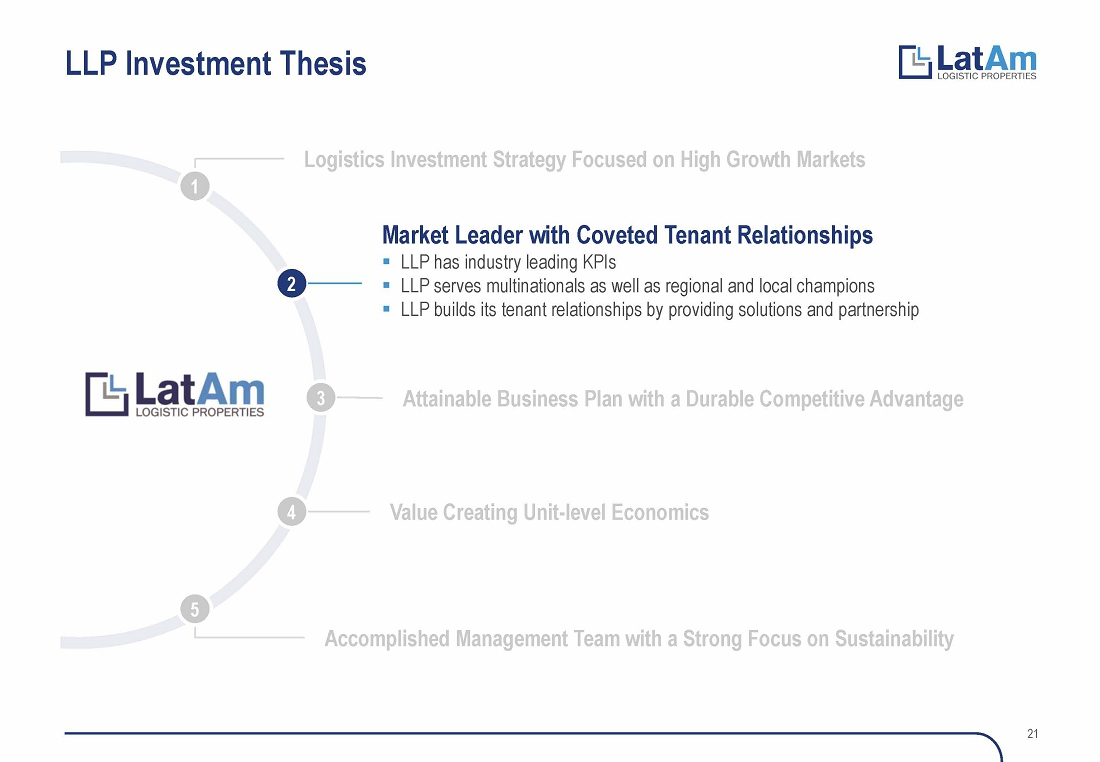

takes us to the second point in LLP’s investment case. |

| ○ | Our

company is a market leader with trusted and highly desirable customer relationships. |

Slide

22

| |

● |

LLP

holds leading KPIs when benchmarked against its industrial peers, coming out ahead in terms of i) pure logistics focus, ii) occupancy,

iii) contract duration, and iv) average rental rates. |

| |

|

|

| |

● |

Also,

we are in line with Mexican peers in terms of US dollar exposure, reaching almost 80% of our asset base. |

| |

|

|

| |

● |

All-in-all,

Vesta is probably our closest comparable. We hold Vesta in very high regard, especially considering our shared history of having

the same investor base. Jaguar, the capital behind LLP, was also an investor in Vesta from 2016 until recently and held a seat on

Vesta’s board for several years. |

Slide

23

| ● | And

pivotal to those performance metrics, are LLP’s coveted tenant relationships, which

include household names, major multinational corporations, and high-credit-quality regional

champions. |

| ○ | We

proudly house logistics for IKEA, Samsung, DHL, Expeditors, Cargill and other well-known

names. |

| ● | These

clients see LLP as a differentiated value proposition, because we i) can serve them in multiple

markets with a single point of contact, ii) offer the best available product and locations,

and iii) provide expansion optionality within our network. |

| ● | Our

purpose is to truly partner with our clients for the long term, with high-level on-going

service, and want to follow and grow with them as they expand in adjacent markets. |

Slide

24

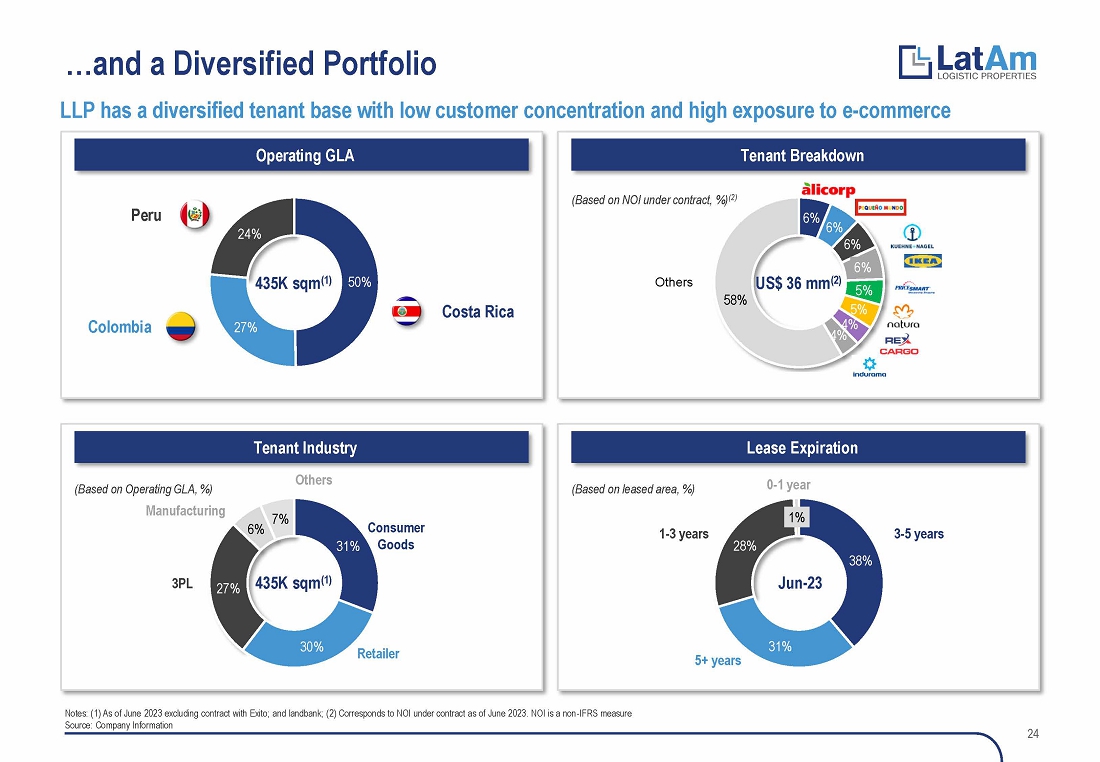

| ● | This

leads me to my next point: At LLP, our aim is to maintain a well-balanced lease portfolio,

carefully analyzed from various perspectives. |

| ○ | As

you can see on the top right, no single customer comprises more than 6% of our NOI. |

| ○ | On

the bottom left, you can see that we strive for a balanced representation of underlying industries,

including consumer goods companies, retailers, and 3PLs. |

| ○ | And,

finally, in terms of lease expiration tenors, we wish to even out the benefits of cashflow

predictability of long-term contracts, with the positive lease spreads we typically capture

as we roll-over our shorter duration leases. |

Slide

25

| ● | To

give you an anecdotal example of what LLP can do and how our relationships travel across

borders, let me mention two cases. |

| ○ | Kuehne

Nagel, the global transportation giant, had their operations in a sub-optimal facility in

Peru and sought a more efficient and green-certified building for their operations

in Colombia. |

| ■ | Given

our capabilities and product quality, we were able to onboard them as a dual market customer

for LLP. Moreover, the relationship has grown from its initial GLA requirement and has expanded

within our parks. |

| ○ | Similarly,

Natura, the Brazilian cosmetics and personal care company, requested high quality specs,

elevated safety standards, and automation-ready warehouses in both Peru and Costa Rica. |

| ● | In

both cases, we were the only provider capable of delivering to their demanding standards

and in two countries simultaneously. |

| | | |

| ● | As

you can imagine, we aspire to have these types of clients expand even further within our

ecosystem. |

Slide

26

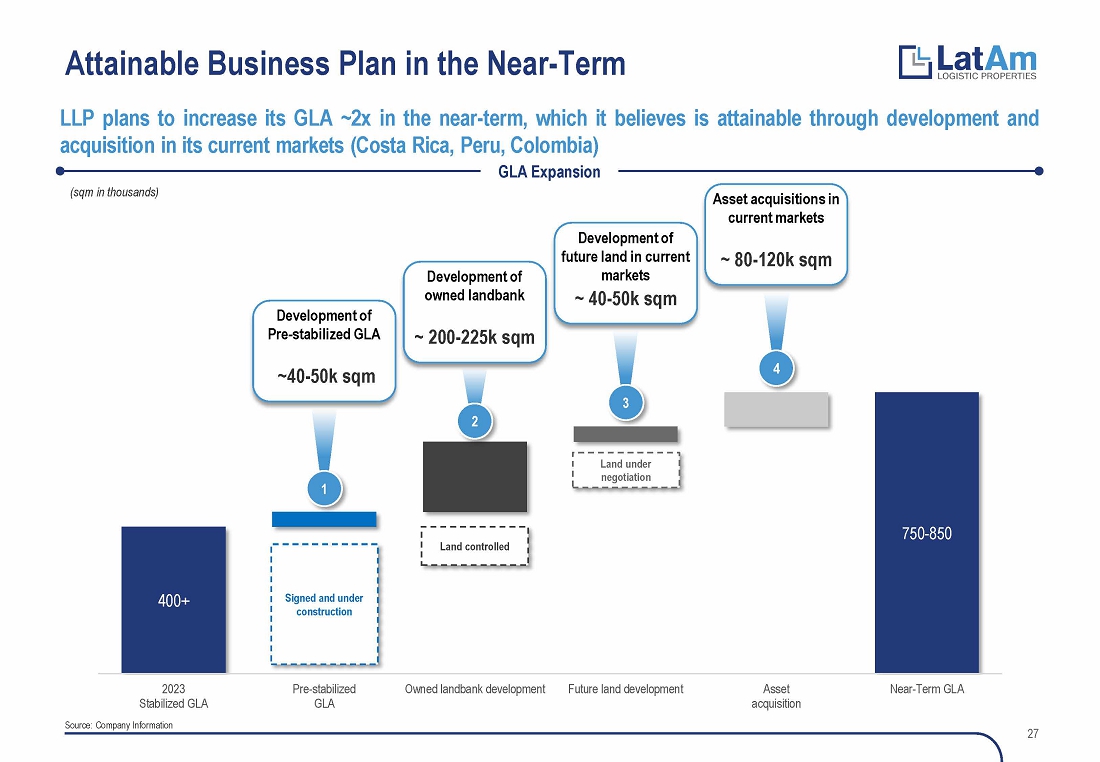

| ● | As

a next stop, I’ll go over our summarized business plan. |

| ● | Our

roadmap for the coming years is straightforward and grounded on a durable competitive advantage. |

Slide

27

| |

○ |

Through

this transaction’s primary capital raise, we aspire to roughly double in size over the next few years. |

| |

|

|

| |

○ |

We

have multiple levers and avenues through which we can materialize our growth. |

| |

|

|

| |

○ |

First,

we expect to deliver in the next few months our pre-stabilized GLA, adding about half a million square feet. |

| |

|

|

| |

○ |

As

a second step, we have immediate growth visibility, thanks to our owned or controlled landbank, which provides an advantage versus

other players. |

| |

|

|

| |

○ |

Furthermore,

as we roll out, our integrated team continues sourcing and feeding our development pipeline of future projects. |

| |

|

|

| |

○ |

And

lastly, by bolting-on strategic acquisitions in dollarized markets where our tenants have expansion plans, we have line of sight

on our expansion strategy. |

| |

|

|

| |

○ |

In

the longer term, we estimate that 60% of our growth will be organic, and 40% inorganic. |

Slide

28

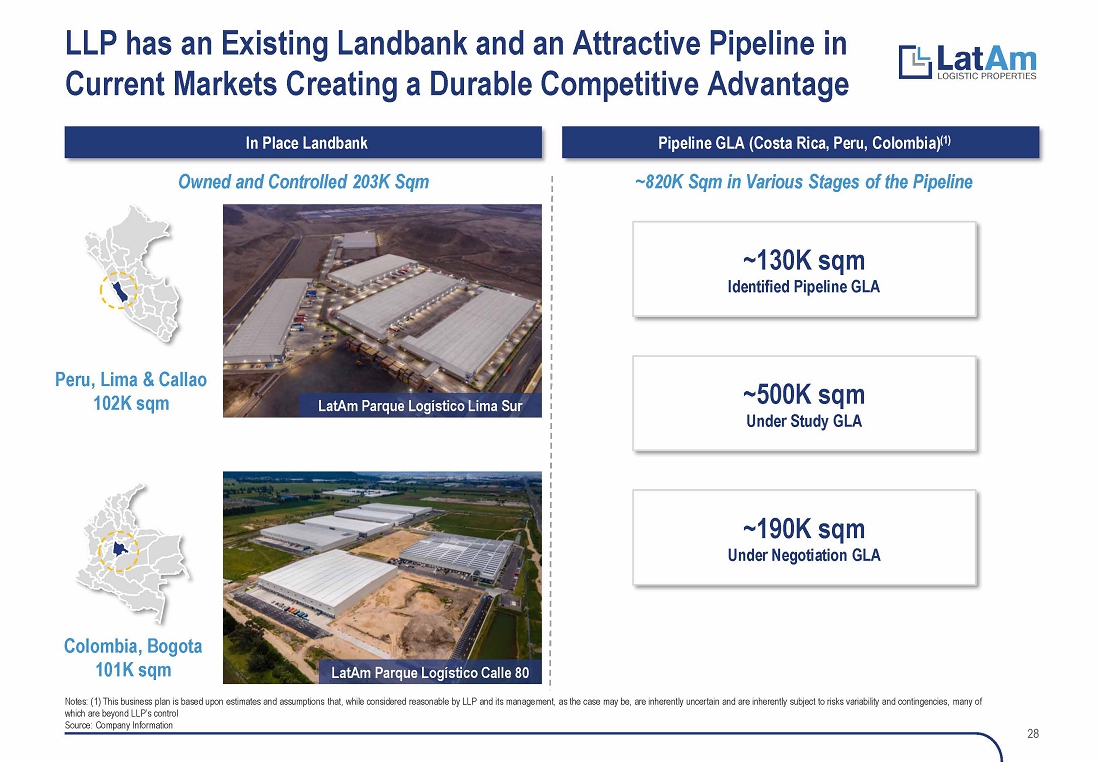

| ● | Related

to our growth plan, let me expand on our land holdings and how they create an advantage versus

our competitors. |

| ● | Importantly,

we have a thoughtful approach for buying land and seek innovative approaches to reduce the

attending carrying cost. |

| ○ | For

example, we have pioneered with long-term land leases, to build modern logistics product

adjacent to the Lima airport in Peru. |

| ● | Also,

due to LLP’s established track record and reputation, landowners proactively approach

us, showing a willingness to engage in land contribution agreements. |

| ○ | This

allows us to secure strategic positions with favorable financing conditions, creating the

potential to enhance returns. |

| ● | With

this strategy, we can demonstrably propose alternatives to our clients and shorten go-to-market

times. |

| ○ | As

referenced earlier, we have owned and controlled a land bank that would allow for the development

of around 2 million sq ft of GLA, and we’re constantly feeding that pipeline. |

| | | |

| ○ | To

illustrate, we have around 8 million sq ft of potential GLA under various stages of review,

just in our current markets. |

Slide

29

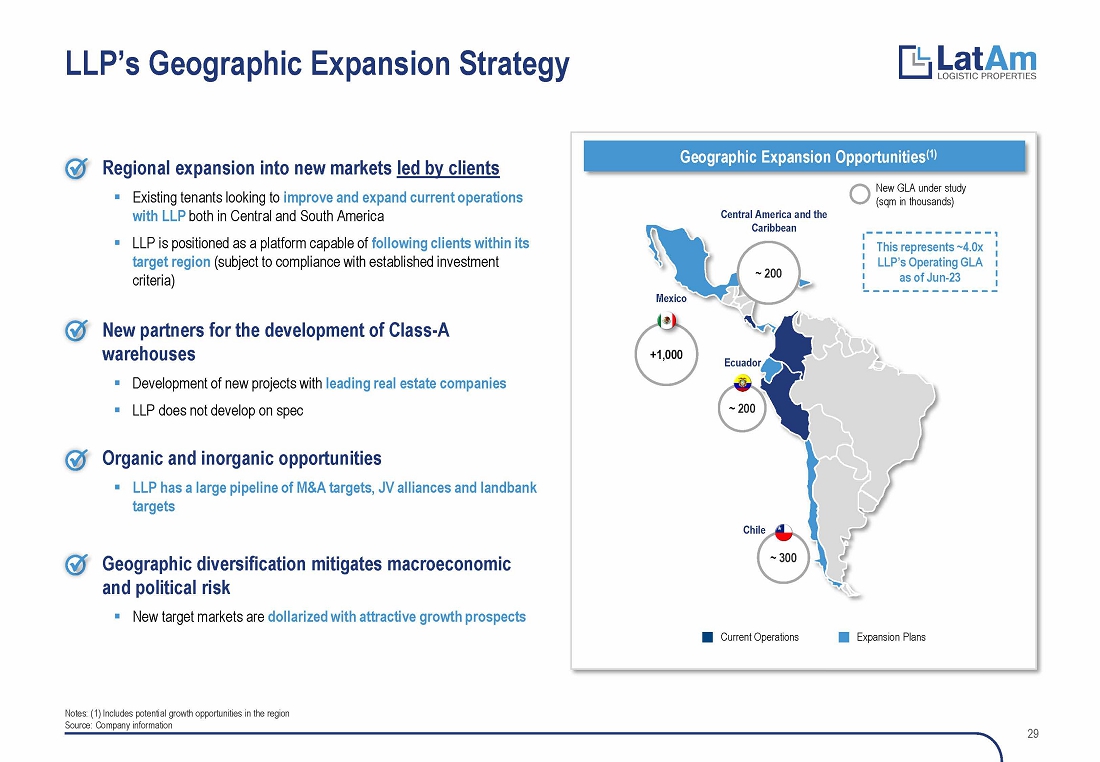

| ● | Now

touching on LLP’s geographic expansion strategy, we have a few simple but effective

guiding principles. |

| ○ | One,

we want to follow our tenants in the markets where their respective businesses are growing. |

| | | |

| ○ | Two,

we want to favor markets with dollar denominated logistics leases, as is the case in Mexico,

Ecuador, Central America and the Caribbean. |

| ■ | For

us, keeping a high dollar denominated asset base will remain paramount. |

| ○ | And

lastly, we want to enter markets where we see a path to achieve a minimum scale of around

one million square feet in about three years after entry. |

Slide

30

| ● | This

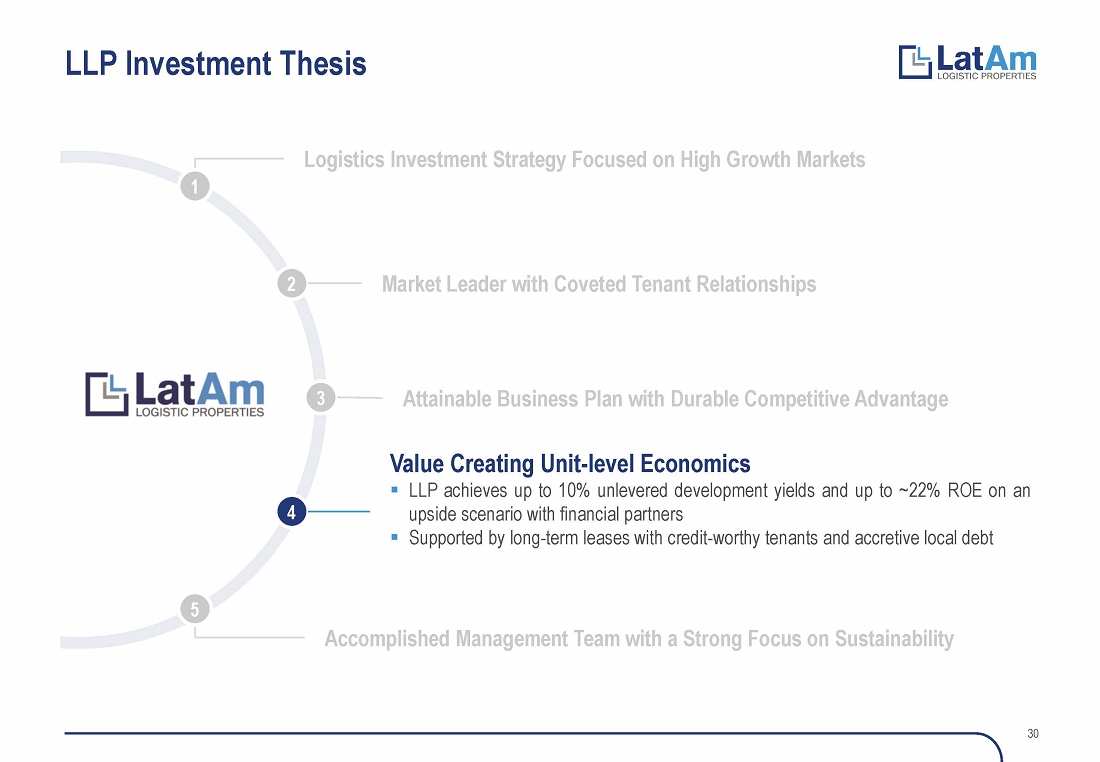

takes us to our next point. Unit economics. |

| ● | At

a granular level, LLP’s business has the potential for highly attractive risk-adjusted

returns. This is the result of strong CAPEX management and the ability to secure predictable

cashflows, via long-term leases, from credit-worthy tenants. |

Slide

31

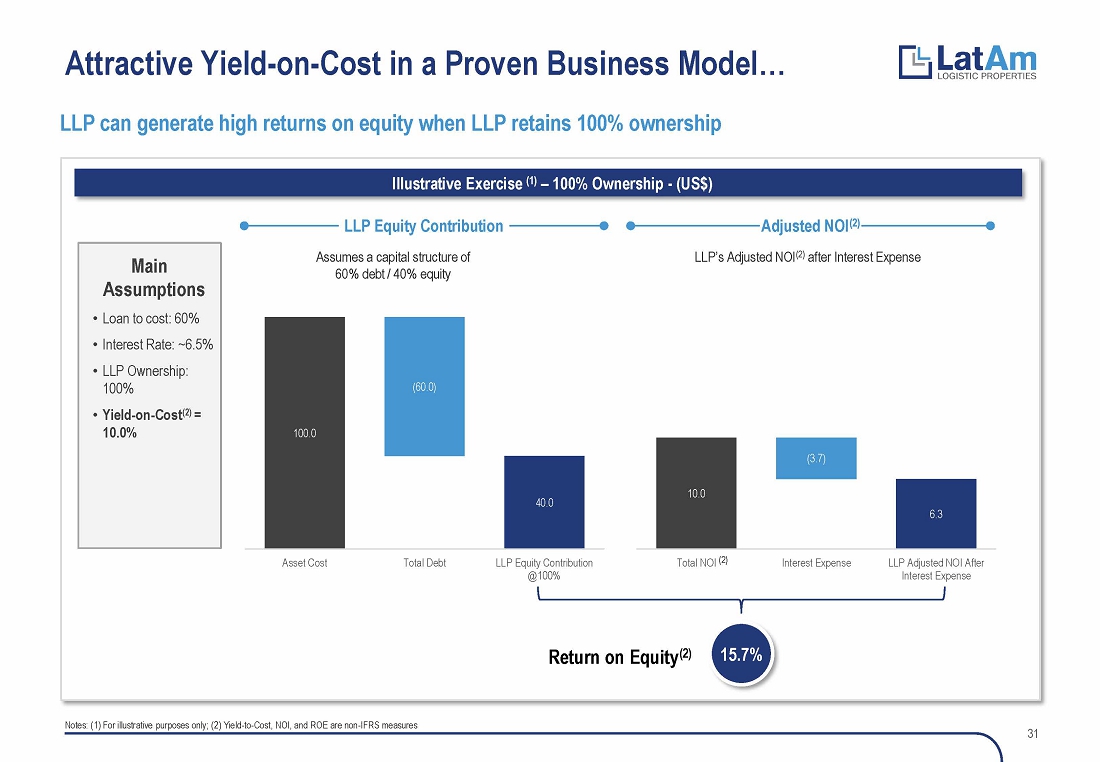

| ● | Organically,

on a standalone basis, LLP can develop assets to double digit unlevered yields. |

| ● | Given

our special market position, we can obtain accretive debt financing for roughly 60% of project

cost, which typically means we can comfortably leverage our equity returns into the mid-to-high

teens on a cash flow basis. |

Slide

32

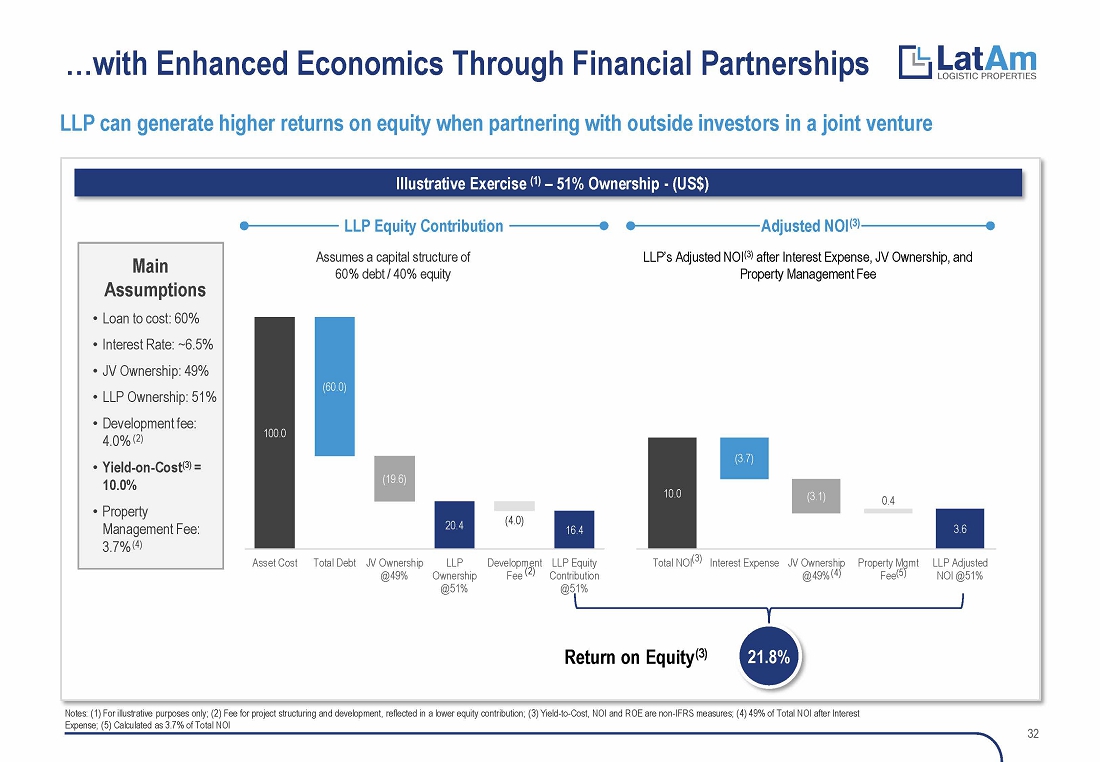

| ● | However,

those returns can be further magnified, at the same time risk is controlled and mitigated. |

| ● | By

securing financial partnerships and Joint Ventures with local equity partners, LLP can charge

for its development and asset management services, creating additional income streams. This

also reduces equity requirements and improves overall return on equity (ROE) for our company. |

| ● | And

to tie it all out, once we account for expected asset appreciation on a fair market value

basis, an additional two to five hundred basis points could be added to the returns you see

on this page. |

Slide

33

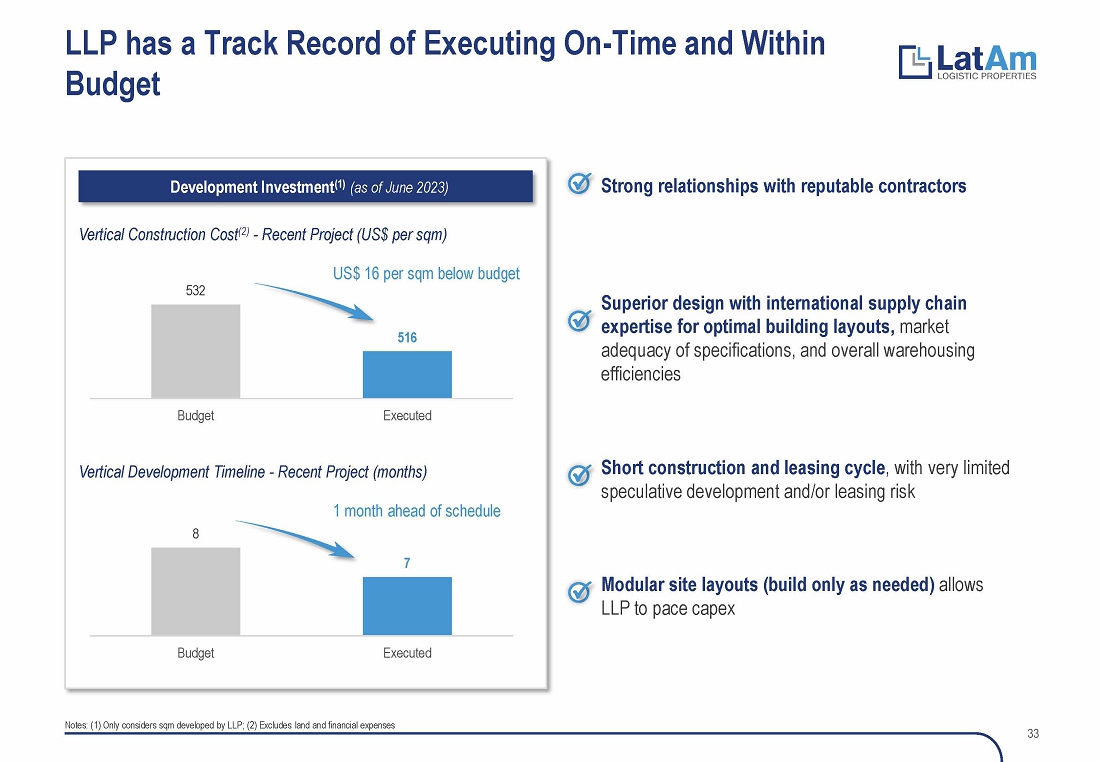

| ● | This

takes me to a crucial point, which is the lynchpin for the returns explained earlier: LLP

has a track record of executing on time and within budget. |

| ○ | For

example, on one of our latest projects, we budgeted 532 dollars of construction costs per

sqm, but we delivered at around 516. |

| | | |

| ○ | Also,

despite supply chain disruptions, we scheduled around 8 months for vertical construction

per building and, on average, we delivered in 7 months. |

| ● | We

have a strong network of local contractors, with whom we have proven results and who strictly

adhere to our Class A specifications. |

| ● | Our

modular layouts give us flexibility to properly pace our demand, typically pre-leasing buildings

before they are finished, and thus maximizing occupancy and capital efficiency. |

Slide

34

| ● | Lastly,

we must highlight our Executive Team and their proven history of delivering results for shareholders,

and in compliance with sustainability objectives. |

Slide

35

| ● | We

believe real estate is predominantly a local game. |

| ● | Our

team is composed of logistic real estate experts, native and based in their markets, with

solid networks, and with a special commitment to serving customers through a long-term and

sustainability lens. |

| ○ | The

team we have today has a longstanding history working together, and our senior executives

have been with the company essentially since its foundation. |

Slide

36

| ● | Importantly

as well, our controlling shareholder, before and after the proposed transaction, is and will

be Jaguar Growth Partners, a global specialist in real estate operating platforms, with roots

that go all the way back to Equity International. |

| ○ | Its

partners and TWO’s management have a prior and established relationship, having known

each other for many years. |

| ○ | And

key to LLP’s DNA, over the last two decades, Jaguar’s partners have not only

built deep experience in Latin America but have also helped build multiple real estate operating

companies, eight of which are in the logistics sector, covering the Andean region, Mexico,

Brazil and even China. |

Slide

37

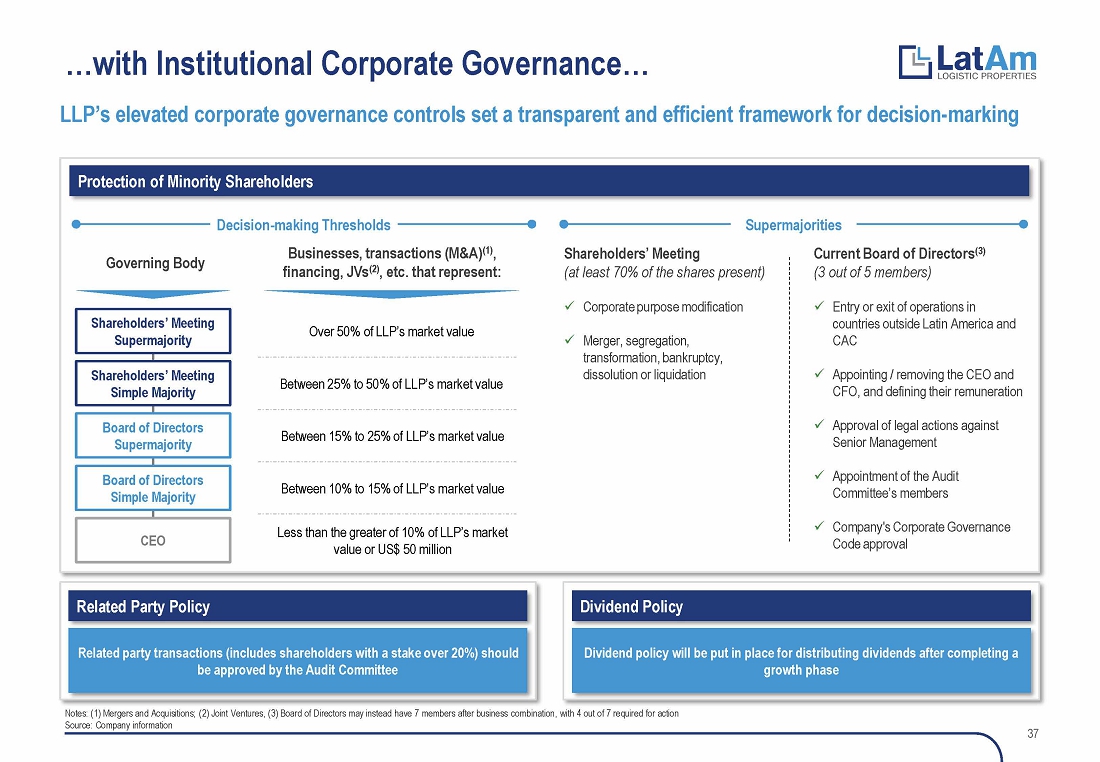

| ● | And

through Jaguar’s involvement we have championed strong governance policies. |

| ○ | The

majority of our directors are independent, and we have a well-defined framework for corporate

decision-making. |

Slide

38

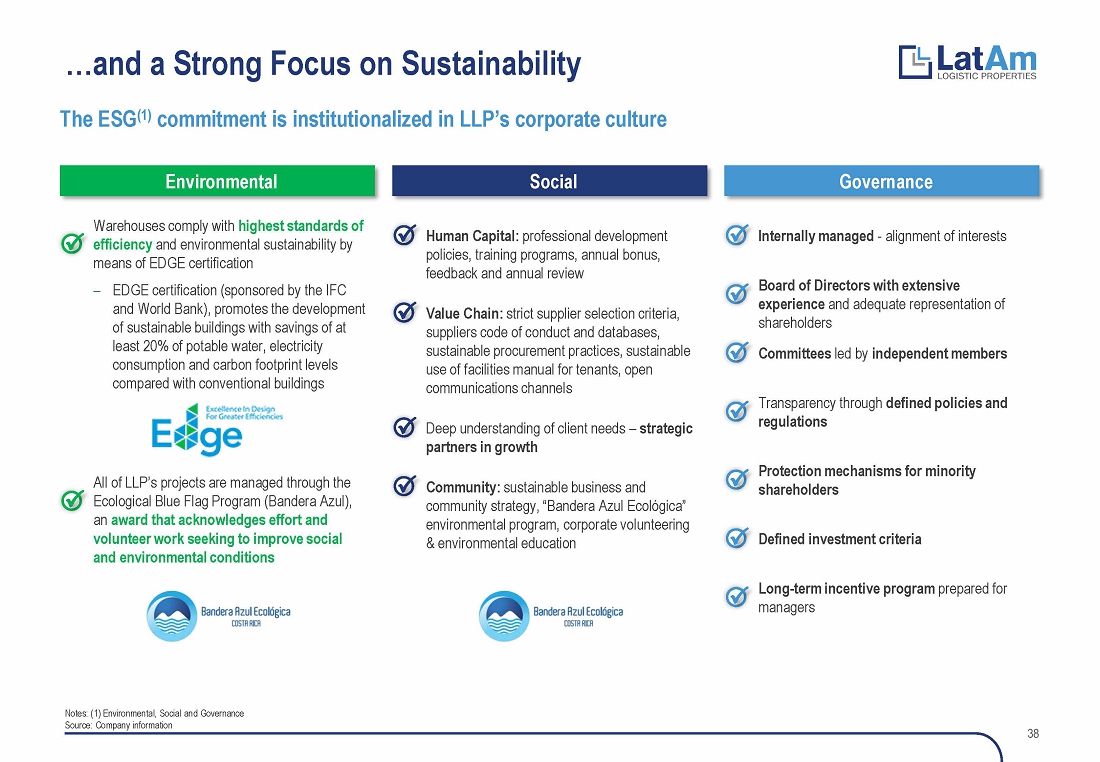

| ● | As

we approach the end of this section, we think it is important to feature LLP’s commitment

to high standards of environmental and social sustainability. |

| ○ | Having

the World Bank’s EDGE certification on all of our new developments is paying dividends,

since multinational clients seek out more responsible solutions and proactively choose providers

that have these differentiators. |

| ○ | Also,

as opposed to what might happen in other markets, our logistic parks are not challenged by

the community but rather embraced as a source of good quality jobs. |

| ■ | LLP

is a good neighbor and has a positive impact in the locations where it operates. |

Slide

38

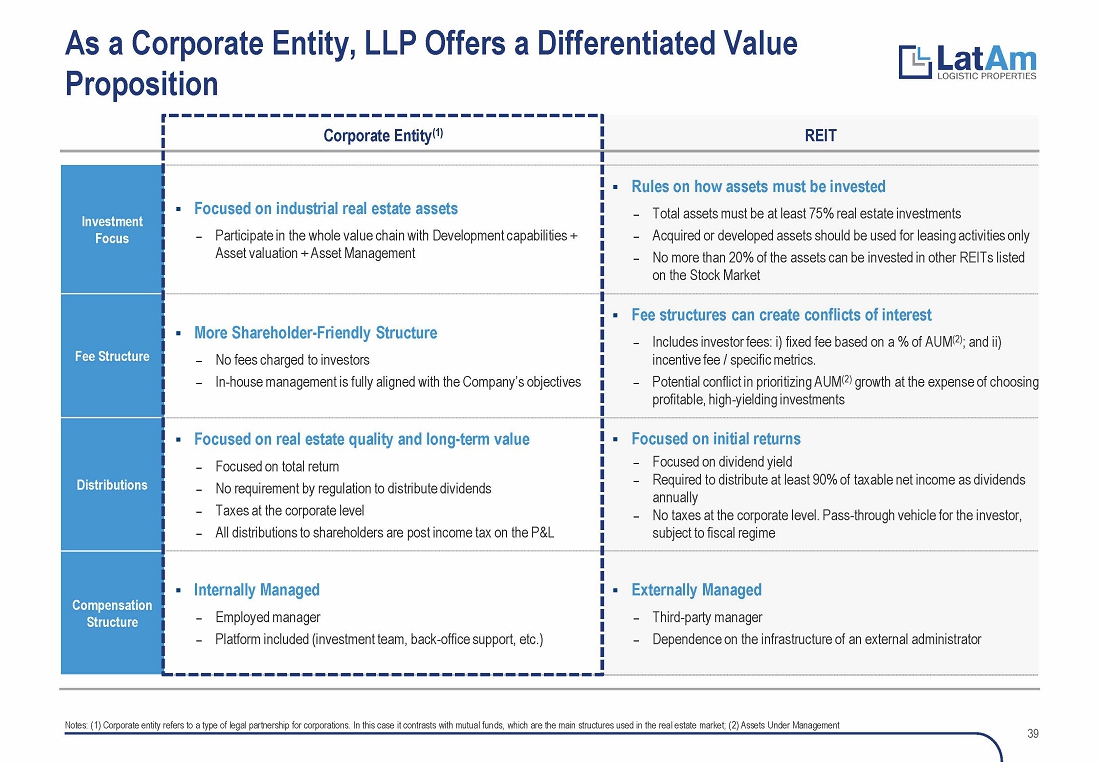

| ● | Finally,

given our growth and development capabilities, we are set up as a C-Corp and not a REIT. |

| ○ | This

is important because it allows us to offer a more compelling investment proposition, with

internalized and aligned management. |

| ○ | And,

very importantly, this positions us to participate throughout the entire value creation chain,

starting with project structuring, financing, development, lease-up, and ongoing asset management. |

[With

that, allow me to pass it on to our CFO, Annette Fernández.]

Annette

Fernandez

Thanks

Esteban,

Before

talking about LLP’s Financial Highlights, I would like to briefly introduce myself. My name is Annette Fernandez and I have been

the CFO of LLP since 2017. I have more than 15 years of experience in the industrial logistic sector with 12 years of experience working

in Prologis in different groups such as financial analysis, accounting, investor relations and capital deployment for the Latin American

region.

Slide

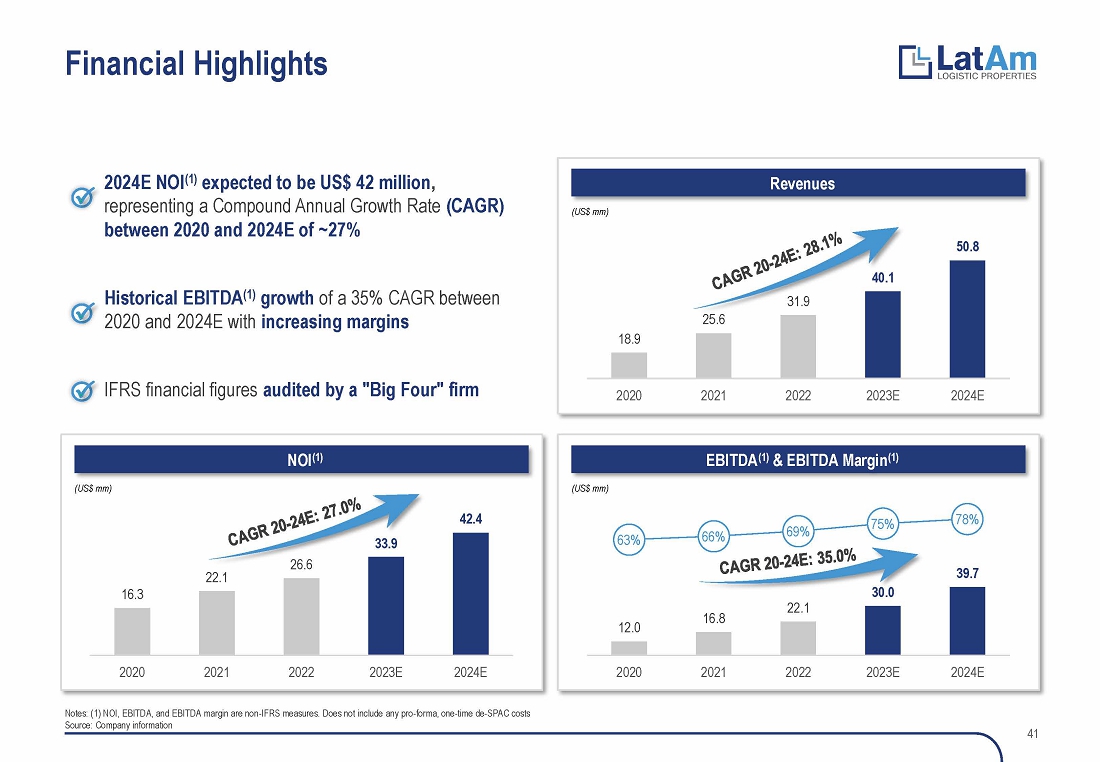

41 - Financial Highlights

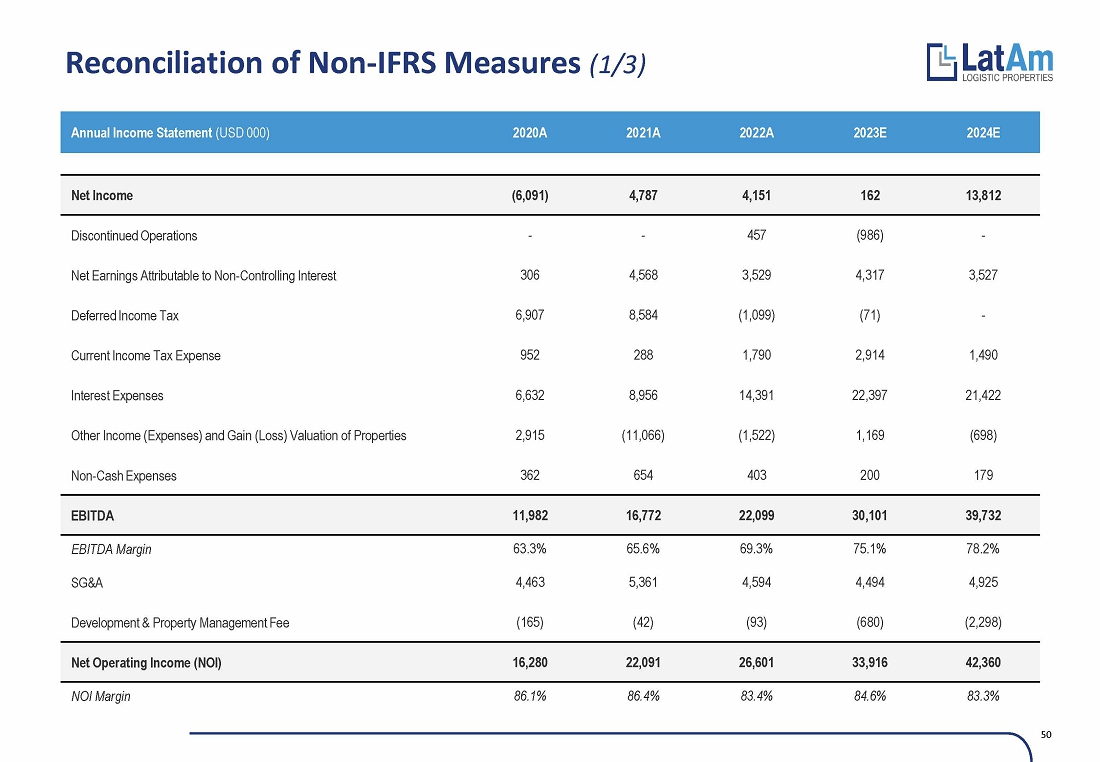

This

slide showcases LLP’s remarkable growth, increasing revenues and a proven track record in execution. Turning our land bank into

production and stabilizing the construction have driven our success in growing revenues, NOI and EBITDA, as well as achieving economies

of scale of the platform.

NOI

from 2020 to 2023 LLP grew a compounded annual growth rate of around 27% due to the stabilization of 215,000 square meters during this

period. The growth in the stabilized portfolio will allow us to achieve in 2023 an estimated 40.1 million dollars in revenues and 33.9

million in NOI.

We

continue to see a high demand for modern logistic real estate in the countries we operate. This high demand for modern logistic real

estate is mainly driven by the continues growth in consumption, e-commerce, supply chain consolidation and flight to quality. As we approach

2024, LLP has high confidence and visibility in achieving 42.4 million dollars of NOI which represents a 25% increase from the NOI estimated

for 2023. The increase in NOI in 2024 will be driven mainly by organic growth through the stabilization of our development platform and

some acquisitions at the back end of the year. I want to point out that LLP annual growth track record have been an average of 25% over

the last three years.

Slide

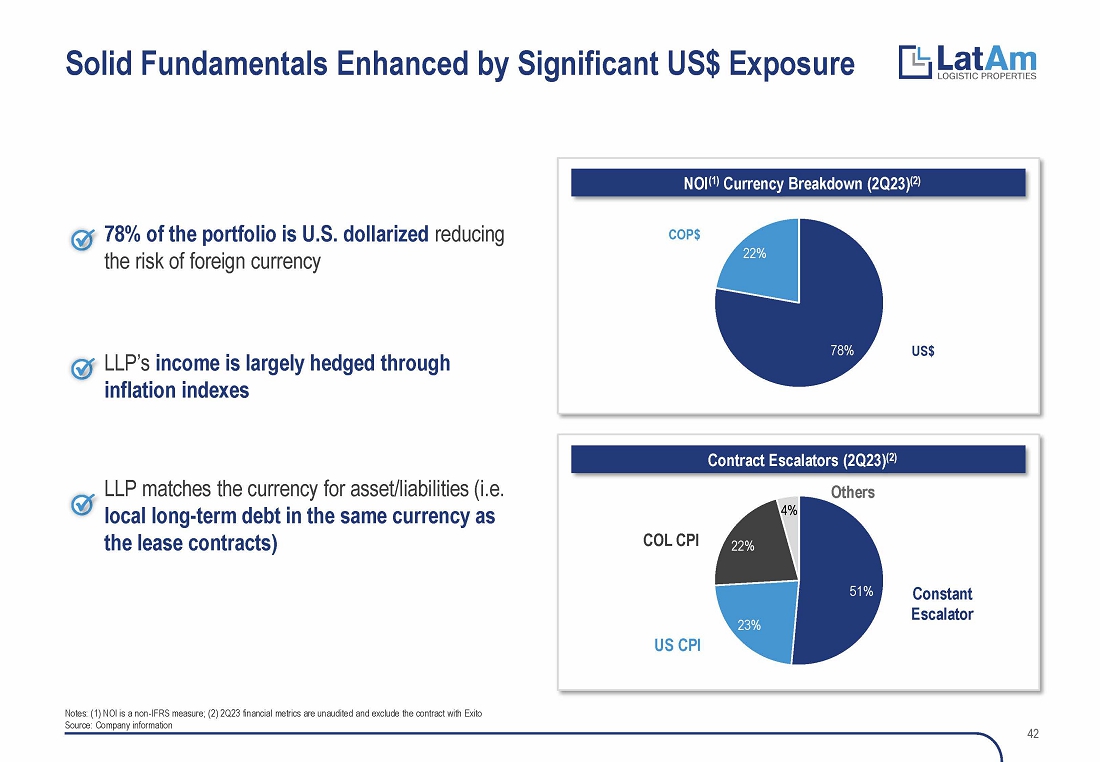

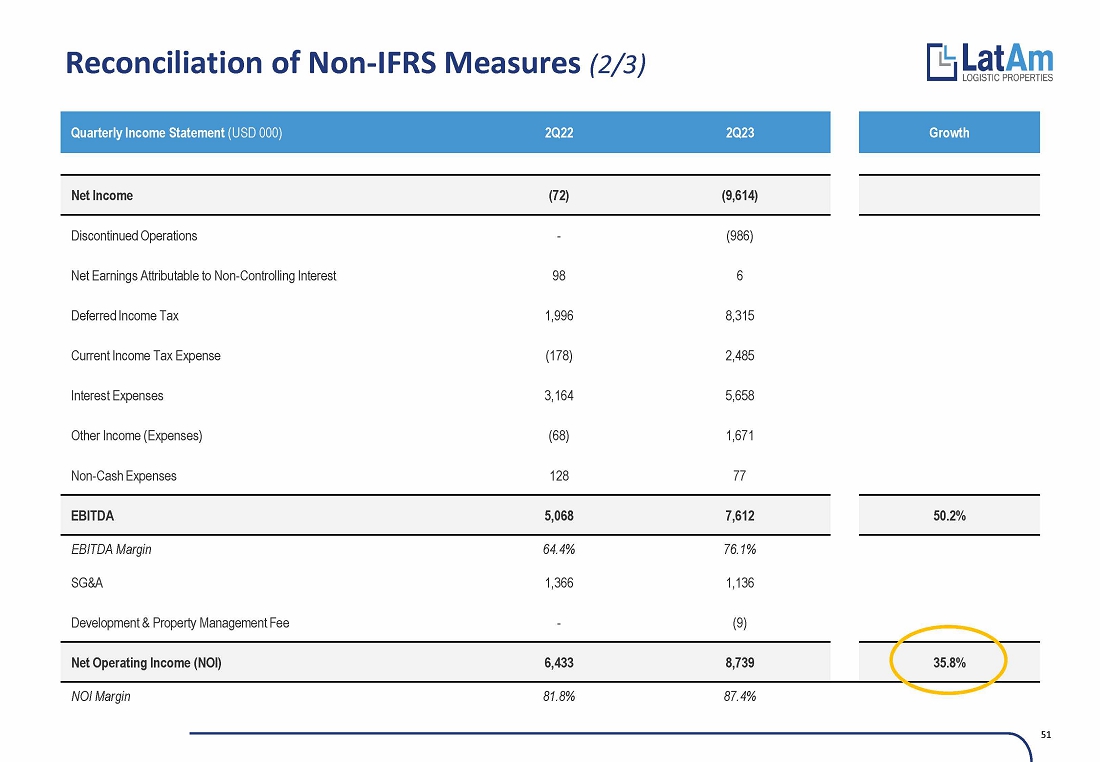

42 - Solid Fundamentals Enhanced by Significant US$ Exposure

The

quality and durability of our revenues comes from (1) Credit Quality of our Tenants, (2) Tenor and Guarantees of our leases, which were

discussed by Esteban earlier and (3) Lease Currency and (4) Inflation protections.

LLP’s

NOI is close to 80% US dollar denominated reducing risk to US investors to foreign currencies and enhances stability in the returns of

the portfolio in dollar terms. Almost all the contracts have annual contractual increases of at least 2.5% with half of them exposed

to either US-CPI in the case of US dollars denominated leases and to Colombia CPI in the case of Colombian leases.

Slide

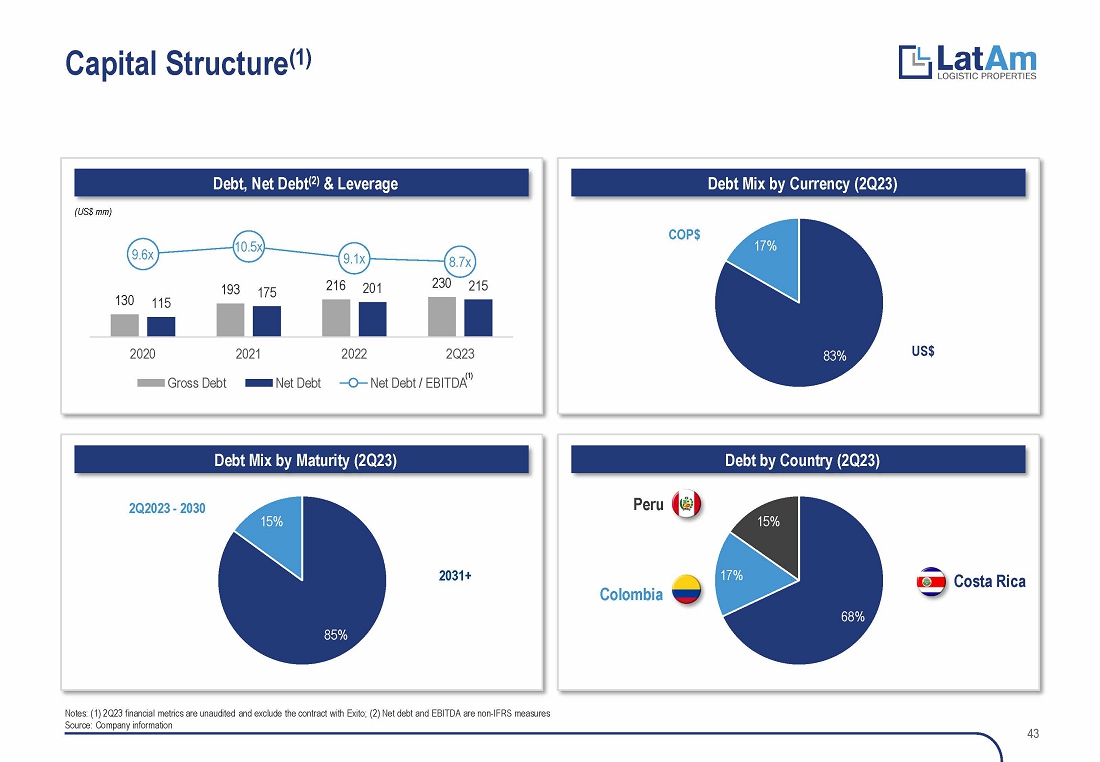

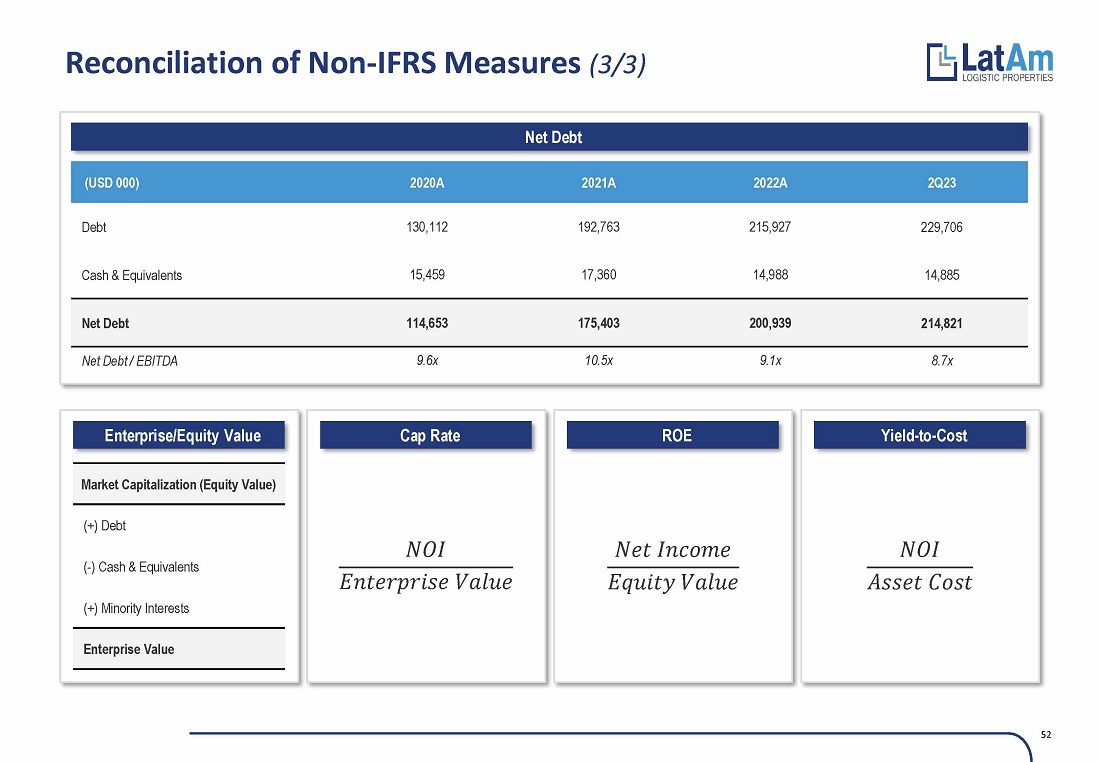

43 – Capital Structure

LLP’s

as a policy tries to avoid currency mismatches between debt and revenues. US dollar debt is placed only in properties with US dollar

denominated leases and Colombian Peso denominated debt is only in properties with Peso denominated leases. This leads us to more than

80% of our debt denominated in US dollar.

The

quality of our portfolio and LLP’s platform institutionality are key to our ability to improve the financial position of LLP. As

an example, earlier this year LLP refinanced US$87 million of the debt portfolio in Costa Rica with a new secured credit facility of

more than US$100 million. This refinancing improved our Balance Sheet by increasing our weighted average debt maturity from 10 years

to 16 years and decreased our overall cost of debt by 140 basis points from the previous quarter.

As

of June 30, 2023, our outstanding net debt is US$215 million from which 85% expires after 2031 and around 45% is fixed for the next two

years at annual interest rate of 6.0%

With

this I will pass the presentation to Nick Geeza to discuss the business combination overview.

Nick

Geeza

Slide

44

Thanks,

Annette and Good afternoon everyone, my name is Nick Geeza, the CFO of T-W-O and I’ll use the remaining time to discuss our business

combination overview.

Slide

45

When

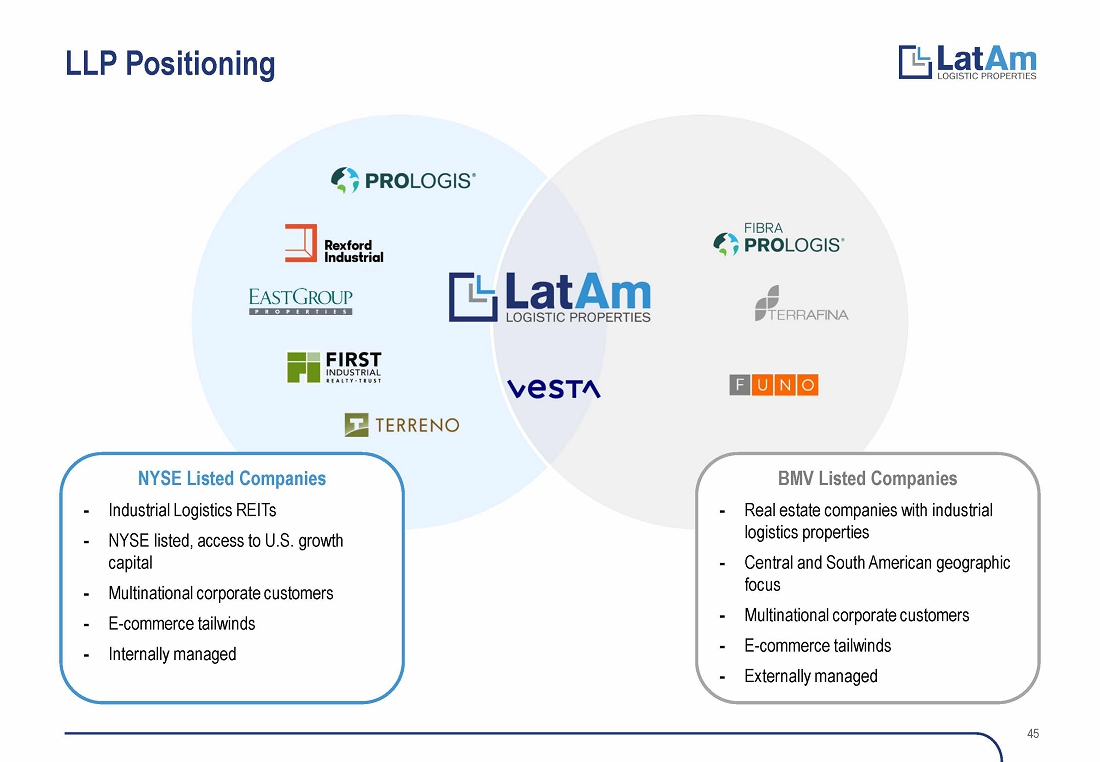

we evaluated public comps, it became clear to us that we should concentrate on LLP’s two defining characteristics: 1) the company’s

focus on customer-first, EDGE certified, modern Class A industrial real estate, which are similar to the NYSE-listed companies on the

left and 2) LLP’s Central and South American geographic presence in underserved, high-growth markets, similar to the Bolsa-listed

companies on the right.

In

the industrial real estate universe, on the left, the listed companies focus on predominantly Class A industrial real estate properties

that are crucial to the supply chain and distribution networks for their clients – generating consistent rental income, maintaining

high occupancy rates and in some cases providing property and asset management services to their tenants.

Regarding

the geographic focus, on the right, we included Mexican Bolsa-listed comps that share a similar business focus. However unlike these

predominantly Mexico-focused companies, we believe LLP benefits from greater geographic diversification across multiple underserved and

high growth markets.

Slide

46

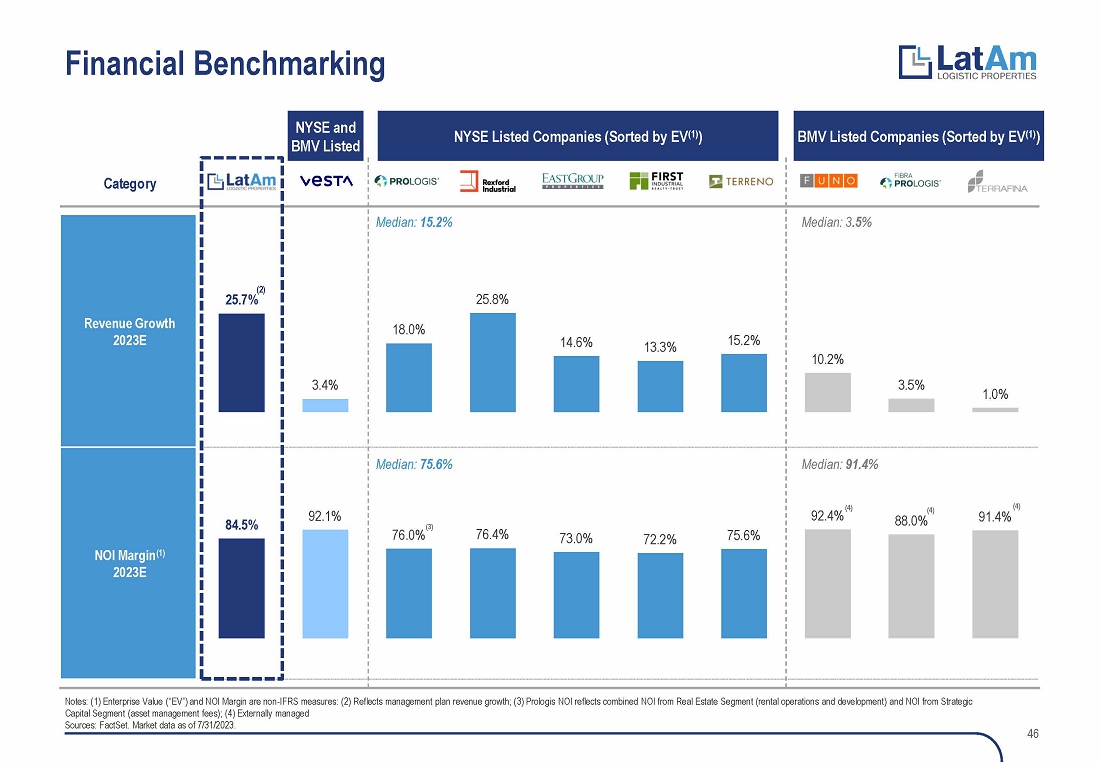

As

shown here, LLP stacks up well on financial benchmarking. On revenue growth, LLP’s expected 2023 growth rate of 25.7% is at the

top end of the range for NYSE listed comps and more than double that of the best performing Bolsa comps.

When

it comes to NOI margin – a key distinction in the comp set is the internally vs externally managed structures of the companies

listed. The NYSE listed companies on the left, similar to LLP, are all internally managed while the Bolsa listed companies on the right

are all externally managed. Here as you can see – LLP outperforms the NYSE peers with higher operating efficiencies.

Slide

47

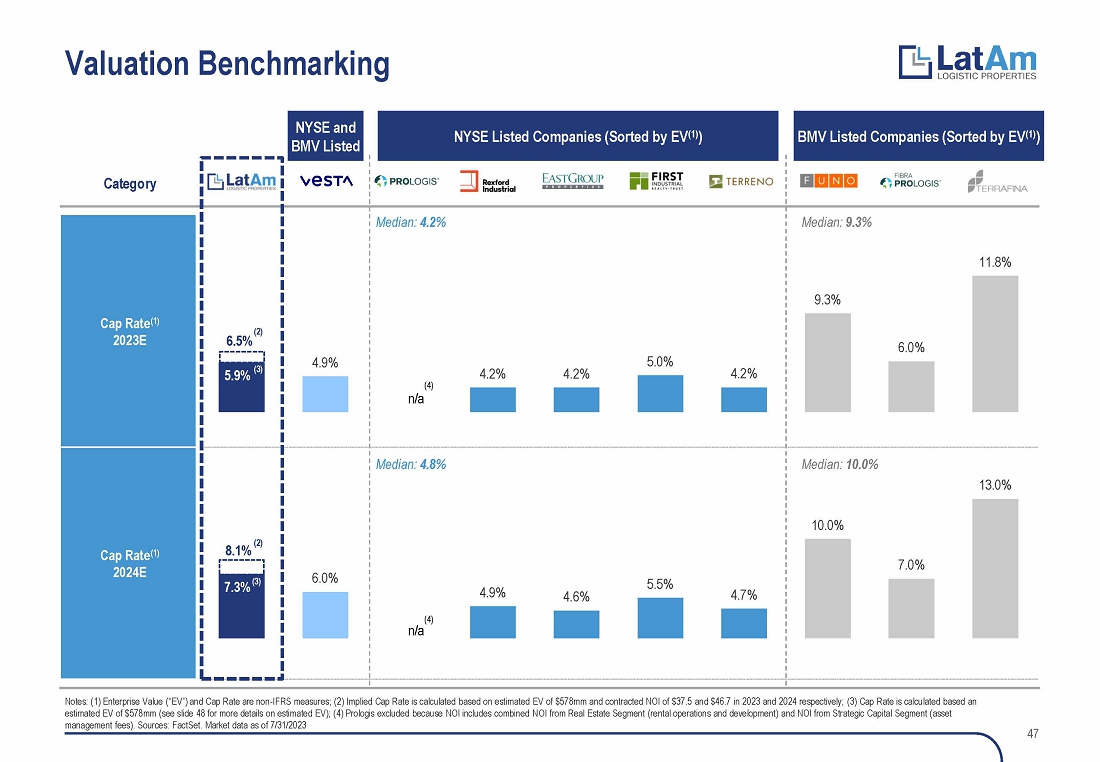

If

we turn to slide 47, we show valuation benchmarking here based on 2023 and 2024 cap rates. LLP offers a compelling return relative to

its peers evidenced by higher cap rates compared to the NYSE listed comps but lower than the median of Bolsa listed companies –

reflecting the company’s lower risk due to its expected NYSE listing where LLP will have greater access to liquidity and global

investors.

Although

LLP’s revenue growth and NOI outperform NYSE peers, the valuation of LLP is priced at a meaningful discount, allowing investors

to participate in its future returns.

Slide

48

Now

on to our transaction summary. On the Sources side, the transaction will be funded with a combination of the following: rolled equity

from existing LLP shareholders and FIF-TEEN MILLION estimated cash in trust. Here we are assuming 70% redemptions and have confidence

in our trust delivery, given our strong investor relationships and the overall improvement in the SPAC market.

I

should also note that T-W-O does not have any outstanding warrants. We believe that this lack of warrants should improve the transaction

execution and post-trading performance. We are targeting $25MM in PIPE from strategic investors, and $200MM of existing net debt, which

as footnoted is asset level debt. There is no corporate level debt at LLP.

On

the Uses side, $25M of cash will go directly to the LLP balance sheet, we are estimating FIFTEEN MILLION for transaction fees and expenses

and the $200MM of net debt rolled over. The resulting pro forma Enterprise Value is $578MM.

To

conclude, we at T-W-O are thrilled to enter into a business combination with LatAm Logistic Properties. We are impressed by LLP’s

vertically integrated operating platform, class A US institutional asset quality, and future growth prospects.

Class

A industrial real estate continues to be a resilient outperforming asset class that benefits from broad macro consumption trends and

we believe our SPAC will provide LLP a path to capitalize on that TAM and the tailwinds that are driving it. And lastly and most importantly,

we believe that Esteban and Annette have the management expertise and the vision to take LLP to the next level as a public company and

create long-term value for shareholders.

Thank

you for your time and we look forward to discussing with you further.

v3.23.2

| X |

- DefinitionBoolean flag that is true when the XBRL content amends previously-filed or accepted submission.

| Name: |

dei_AmendmentFlag |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionFor the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

| Name: |

dei_DocumentPeriodEndDate |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:dateItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

| Name: |

dei_DocumentType |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:submissionTypeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 1 such as Attn, Building Name, Street Name

| Name: |

dei_EntityAddressAddressLine1 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 2 such as Street or Suite number

| Name: |

dei_EntityAddressAddressLine2 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- Definition

+ References

+ Details

| Name: |

dei_EntityAddressCityOrTown |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCode for the postal or zip code

| Name: |

dei_EntityAddressPostalZipCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |