UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or Section 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

September 29, 2023

Power & Digital

Infrastructure Acquisition II Corp.

(Exact name of registrant as specified in its charter)

| Delaware |

|

001-441151 |

|

86-2962208 |

(State or other jurisdiction of

incorporation or organization) |

|

(Commission File Number) |

|

(I.R.S. Employer

Identification Number) |

321 North Clark Street, Suite 2440

Chicago, IL 60654

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Registrant’s telephone number, including area

code: (312) 262-5642

Not Applicable

(Former name or former address, if changed since last

report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligation to the registrant under any of the following provisions:

| ☒ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading Symbols |

|

Name of each exchange on which registered |

| Units, each consisting of one share of Class A Common Stock and one-half of one redeemable warrant |

|

XPDBU |

|

The Nasdaq Stock Market LLC |

| Class A common stock, par value $0.0001 per share |

|

XPDB |

|

The Nasdaq Stock Market LLC |

| Warrants included as part of the units, each whole warrant exercisable for one share of Class A Common Stock at an exercise price of $11.50 |

|

XPDBW |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company

as defined in Rule 405 of the Securities Act of 1933 or Rule 12b-2 of the Securities Exchange Act of 1934.

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act.

Item 1.01 Entry into a Material Definitive Agreement.

Investment Agreement

On September 29, 2023,

Power & Digital Infrastructure Acquisition II Corp. (“XPDB”) entered into an Investment Agreement (the “Investment

Agreement”) with Montana Technologies LLC (“Montana”), Contemporary Amperex Technology Co., Limited (“CATL”),

CATL US Inc., an affiliate of CATL (“CATL US”) and Contemporary Amperex Technology USA Inc. an affiliate of CATL (“CATL

USA,” and, together with CATL US and CATL, the “CATL Parties”), pursuant to which the CATL Parties agreed, among other

things, that they will not, directly or indirectly, (i) acquire any additional units of XPDB following the consummation of its proposed

business combination with Montana (the “Business Combination,” and such surviving company, the “Post-Combination Company”),

(ii) seek election to, or to place a representative on, Montana’s board of managers or the board of directors of the Post-Combination

Company, or (iii) acquire any securities of the Post-Combination Company if, following such acquisition, the CATL Parties and their

affiliates would hold, in the aggregate, an interest in the Post-Combination Company of greater than 9.8% on either an economic or

voting basis (the “CATL Ownership Limit”). In the event the CATL Parties and their affiliates exceed the CATL Ownership Limit,

the CATL Parties have agreed, following written notice from the Post-Combination Company, to divest within five business days such

number of Post-Combination Company securities as shall be necessary to cause the CATL Ownership Limit not to be exceeded. In addition,

at any time the CATL Ownership Limit is exceeded, the CATL Parties have agreed to vote any voting power they hold in excess of 9.8% in

accordance with the recommendation of the board of directors of the Post-Combination Company.

The CATL Parties agreed that they will not, and will cause their affiliates not to, access, obtain, or seek to access or obtain

Montana or the Post-Combination Company’s trade secrets, know-how, or other confidential, proprietary, or competitively sensitive

information (excluding any such information that Montana is obligated to provide to CATL US, CAMT, or CAMT’s subsidiaries pursuant

to that certain Amended and Restated Joint Venture Agreement for CAMT, dated as of September 29, 2023, by and among Montana, CAMT

Climate Solutions, Ltd. (“CAMT”) and CATL US), including by reverse engineering, or seeking to reverse engineer, any of Montana’s

products.

Montana has agreed to use its reasonable best efforts to assist CATL USA

in selling, prior to the consummation of the Business Combination, units of Montana representing at least 2% of Montana's issued and outstanding

units at a price per unit that is not materially lower than the price per unit implied by the valuation of Montana in connection with

the Business Combination. In so assisting CATL USA, Montana is not obligated to incur any expenses or grant any concessions, nor is it

obligated to prioritize any sale by CATL USA over its own capital raising or financing activities.

The Investment Agreement

contains customary representations and warranties and may be terminated only with the written consent of the parties thereto.

The foregoing summary of

the Investment Agreement is qualified in its entirety by reference to the text of the Investment Agreement, which is attached as Exhibit

10.1 hereto and incorporated herein by reference.

Item 7.01 Regulation FD Disclosure.

Furnished herewith as Exhibit

99.1 and incorporated into this Item 7.01 by reference is the investor presentation to be presented to certain potential investors in

connection with the Business Combination.

The information set forth below

under this Item 7.01, including the exhibits attached hereto, is intended to be furnished and shall not be deemed “filed”

for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to

the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the the United States Securities

Act of 1933 (the “Securities Act”) or the Exchange Act, except as expressly set forth by specific reference in such filing.

Additional Information about the Proposed Transactions

and Where to Find It

In connection with the proposed

Business Combination, XPDB has filed a registration statement on Form S-4 (as amended to date, the “Registration Statement”)

that includes a preliminary prospectus and preliminary proxy statement of XPDB. The proxy statement/prospectus is not yet effective.

The definitive proxy statement/prospectus, when it is declared effective by the U.S. Securities and Exchange Commission (the “SEC”),

will be sent to all XPDB stockholders as of a record date to be established for voting on the proposed Business Combination and the other

matters to be voted upon at a meeting of XPDB’s stockholders to be held to approve the proposed Business Combination and other

matters (the “Special Meeting”). XPDB may also file other documents regarding the proposed Business Combination with the

SEC. The definitive proxy statement/final prospectus will contain important information about the proposed Business Combination and the

other matters to be voted upon at the Special Meeting and may contain information that an investor will consider important in making

a decision regarding an investment in XPDB’s securities. Before making any voting decision, investors and security holders of XPDB

and other interested parties are urged to read the Registration Statement and the proxy statement/prospectus and all other relevant documents

filed or that will be filed with the SEC in connection with the proposed Business Combination as they become available because they will

contain important information about the proposed Business Combination.

Investors and security holders will also be able to obtain free

copies of the definitive proxy statement/final prospectus and all other relevant documents filed or that will be filed with the SEC by

XPDB through the website maintained by the SEC at www.sec.gov, or by directing a request to XPDB, 321 North Clark Street, Suite

2440, Chicago, IL 60654 or by contacting Morrow Sodali LLC, XPDB’s proxy solicitor, for help, toll-free at (800) 662-5200 (banks

and brokers can call collect at (203) 658-9400).

INVESTMENT

IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY

PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION

TO THE CONTRARY IS A CRIMINAL OFFENSE.

Participants in the Solicitation

XPDB, Montana and certain of their

respective directors, executive officers may be deemed participants in the solicitation of proxies from XPDB’s stockholders with

respect to the proposed Business Combination. A list of the names of those directors and executive officers of XPDB and a description

of their interests in XPDB is set forth in XPDB’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports

on Form 8-K. Additional information regarding the interests of those persons and other persons who may be deemed participants in the proposed

Business Combination may be obtained by reading the Registration Statement. The documents described in this paragraph are available free

of charge at the SEC’s website at www.sec.gov, or by directing a request to XPDB, 321 North Clark Street, Suite 2440, Chicago,

IL 60654. Additional information regarding the names and interests of such participants will be contained in the Registration Statement

for the proposed Business Combination when available.

Forward-Looking Statements

Certain

statements in this Report on Form 8-K (this “Report”) may be considered “forward-looking statements” as defined

in the Private Securities Litigation Reform Act of 1995 and within the meaning of the federal securities laws with respect to the proposed

Business Combination between XPDB and Montana, including statements regarding the benefits of the proposed Business Combination, the anticipated

timing of the proposed Business Combination, the likelihood and ability of the parties to successfully consummate the proposed Business

Combination, the amount of funds available in the trust account as a result of shareholder redemptions or otherwise, the impact, cost

and performance of the AirJouletm technology once commercialized, the services offered by Montana and the markets in which

Montana operates, business strategies, debt levels, industry environment, potential growth opportunities and the effects of regulations

and XPDB’s or Montana’s projected future results. These forward-looking statements generally are identified by the words “believe,”

“predict,” “project,” “potential,” “expect,” “anticipate,” “estimate,”

“intend,” “strategy,” “future,” “forecast,” “opportunity,” “target,”

“plan,” “may,” “should,” “will,” “could,” “would,” “should,”

“will be,” “will continue,” “will likely result,” and similar expressions (including the negative

versions of such words or expressions).

Forward-looking

statements are predictions, projections and other statements about future events that are based on current expectations and assumptions

and, as a result, are subject to risks and uncertainties. Many factors could cause actual future events to differ materially from the

forward-looking statements in this document, including but not limited to: (i) the risk that the proposed Business Combination may not

be completed in a timely manner or at all, which may adversely affect the price of XPDB securities; (ii) the risk that the proposed Business

Combination may not be completed by XPDB’s business combination deadline and the potential failure to obtain an extension of the

business combination deadline if sought by XPDB; (iii) the failure to satisfy the conditions to the consummation of the proposed Business

Combination, including the approval of the proposed Business Combination by XPDB’s stockholders, the satisfaction of the minimum

aggregate transaction proceeds amount following redemptions by XPDB’s public stockholders and the receipt of certain governmental

and regulatory approvals; (iv) the failure to obtain financing to complete the proposed Business Combination and to support the future

working capital needs of Montana; (v) the effect of the announcement or pendency of the proposed Business Combination on Montana’s

business relationships, performance, and business generally; (vi) risks that the proposed Business Combination disrupts current plans

of Montana and potential difficulties in Montana’s employee retention as a result of the proposed Business Combination; (vii) the

outcome of any legal proceedings that may be instituted against XPDB or Montana related to the agreement and the proposed Business Combination;

(viii) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws

or regulations or as a condition to obtaining regulatory approval of the Business Combination; (ix) the ability to maintain the listing

of XPDB’s securities on the NASDAQ; (x) the price of XPDB’s securities, including volatility resulting from changes in the

competitive and highly regulated industries in which Montana plans to operate, variations in performance across competitors, changes in

laws and regulations affecting Montana’s business and changes in the combined capital structure; (xi) the ability to implement business

plans, forecasts, and other expectations after the completion of the proposed Business Combination, including the possibility of cost

overruns or unanticipated expenses in development programs, and the ability to identify and realize additional opportunities; (xii) the

enforceability of Montana’s intellectual property, including its patents, and the potential infringement on the intellectual property

rights of others, cyber security risks or potential breaches of data security; and (xiii) other risks and uncertainties set forth in the

section entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” in XPDB’s Annual

Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K that are available on the website of the Securities

and Exchange Commission (the “SEC”) at www.sec.gov and other documents filed, or to be filed with the SEC by XPDB,

including the Registration Statement. The foregoing list of factors is not exhaustive. There may be additional risks that neither XPDB

or Montana presently know or that XPDB or Montana currently believe are immaterial that could also cause actual results to differ from

those contained in the forward-looking statements. You should carefully consider the foregoing factors and the other risks and uncertainties

that will be described in XPDB’s definitive proxy statement contained in the Registration Statement, including those under “Risk

Factors” therein, and other documents filed by XPDB from time to time with the SEC. These filings identify and address other important

risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements.

Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking

statements, and XPDB and Montana assume no obligation and, except as required by law, do not intend to update or revise these forward-looking

statements, whether as a result of new information, future events, or otherwise. Neither XPDB nor Montana gives any assurance that either

XPDB or Montana will achieve its expectations.

Item 9.01 Financial Statements and Exhibits.

(d)

| Exhibit |

|

Description |

| 10.1 |

|

Investment Agreement, dated as of September 29, 2023, by and among Montana Technologies LLC, Power & Digital Infrastructure Acquisition II Corp., Contemporary Amperex Technology Co., Limited, CATL US INC. and Contemporary Amperex Technology USA Inc. (incorporated by reference to Exhibit 10.15 to Amendment No. 1 to the Registration Statement filed with the SEC on October 2, 2023). |

| 99.1 |

|

Investor Presentation, dated October 4, 2023. |

| 104 |

|

Cover Page Interactive Data File (embedded within Inline XBRL document). |

SIGNATURE

Pursuant to the requirements of the Securities Exchange

Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: October 4, 2023

| |

POWER& DIGITAL INFRASTRUCTURE ACQUISITION

II CORP. |

| |

|

|

| |

By: |

/s/ Patrick C. Eilers |

| |

Name: |

Patrick C. Eilers |

| |

Title: |

Chief Executive Officer |

5

Exhibit 99.1

SUSTAINABLY MEETING THE CHALLENGES OF WATER SUPPLY AND COMFORT COOLING

Basis of Presentation These presentation materials (“Presentation Materials”) are provided for informational purposes only and have been prepared to assist interested parties in a proposed private placement in making their own evaluation with respect to an investment in connection with a potential business combination among Montana Technologies LLC ("Montana Technologies“ or “MT”), Power & Digital Infrastructure Acquisition II Corp . ("XPDB") and the other parties thereto and related transactions (the "Potential Business Combination") and for no other purpose . By accepting, reviewing or reading these Presentation Materials, you will be deemed to have agreed to the obligations and restrictions set out below . No Offer or Solicitation These Presentation Materials and any oral statements made in connection with these Presentation Materials do not constitute an offer to sell, or a solicitation of an offer to buy, or a recommendation to purchase, any securities in any jurisdiction, or the solicitation of any vote, consent or approval in any jurisdiction in connection with the Potential Business Combination or any related transactions, nor shall there be any sale, issuance or transfer of any securities in any jurisdiction where, or to any person to whom, such offer, solicitation or sale may be unlawful under the laws of such jurisdiction . These Presentation Materials do not constitute either advice or a recommendation regarding any securities . No offering of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933 , as amended (the "Securities Act") or an exemption therefrom . No Representations and Warranties No representations or warranties, express, implied or statutory, are given in, or in respect of, these Presentation Materials, and no person may rely on the information contained in these Presentation Materials . Any data on past performance or modeling contained herein is not an indication as to future performance . This data is subject to change . Each recipient agrees and acknowledges that these Presentation Materials are not intended to form the basis of any investment decision by such recipient and do not constitute investment, tax or legal advice . Recipients of these Presentation Materials are not to construe its contents, or any prior or subsequent communications from or with XPDB, Montana Technologies, or their respective representatives as investment, legal or tax advice . Each recipient should seek independent third party legal, regulatory, accounting and/or tax advice regarding these Presentation Materials . In addition, these Presentation Materials do not purport to be all - inclusive or to contain all of the information that may be required to make a full analysis of Montana Technologies or the Potential Business Combination . Recipients of these Presentation Materials should each make their own evaluation of Montana Technologies, and of the relevance and adequacy of the information and should make such other investigations as they deem necessary . XPDB and Montana Technologies assume no obligation to update the information in these Presentation Materials . Each recipient also acknowledges and agrees that the information contained in these Presentation Materials (i) is preliminary in nature and is subject to change, and any such changes may be material and (ii) should be considered in the context of the circumstances prevailing at the time and has not been, and will not be, updated to reflect material developments which may occur after the date of these Presentation Materials . To the fullest extent permitted by law, in no circumstances will Montana Technologies, XPDB, or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of these Presentation Materials, its contents, its omissions, reliance on the information contained within it or on opinions communicated in relation thereto or otherwise arising in connection therewith . These Presentation Materials discuss trends and markets that Montana Technologies' leadership team believes will impact the development and success of Montana Technologies based on its current understanding of the marketplace and each recipient acknowledges this information is preliminary in nature and subject to change . Industry and Market Data Industry and market data used in these Presentation Materials, including information about Montana Technologies' total addressable market, has been obtained from third - party industry publications and sources as well as from research reports prepared for other purposes . Neither XPDB nor Montana Technologies has independently verified the data obtained from these sources and cannot assure you of the reasonableness of any assumptions used by these sources or the data's accuracy or completeness . DISCLAIMERS

Forward Looking Statements Certain statements in these Presentation Materials may be considered “forward - looking statements” as defined in the Private Securities Litigation Reform Act of 1995 and within the meaning of the federal securities laws with respect to the proposed business combination between XPDB and Montana Technologies, including statements regarding the benefits of the proposed business combination, the anticipated timing of the proposed business combination, the likelihood and ability of the parties to successfully consummate the proposed business combination, the amount of funds available in the trust account as a result of shareholder redemptions or otherwise, the impact, cost and performance of the AirJoule tm technology once commercialized, the services offered by Montana Technologies and the markets in which Montana Technologies operates, business strategies, debt levels, industry environment, potential growth opportunities, the effects of regulations and XPDB’s or Montana Technologies’ projected future results . These forward - looking statements generally are identified by the words “believe,” “predict,” “project,” “potential,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “forecast,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “should,” “will be,” “will continue,” “will likely result,” and similar expressions (including the negative versions of such words or expressions) . Forward - looking statements are predictions, projections and other statements about future events that are based on current expectations and assumptions and, as a result, are subject to risks and uncertainties . Many factors could cause actual future events to differ materially from the forward - looking statements in this document, including but not limited to : (i) the risk that the proposed business combination may not be completed in a timely manner or at all, which may adversely affect the price of XPDB securities ; (ii) the risk that the proposed business combination may not be completed by XPDB’s business combination deadline and the potential failure to obtain an extension of the business combination deadline if sought by XPDB ; (iii) the failure to satisfy the conditions to the consummation of the proposed business combination, including the approval of the proposed business combination by XPDB’s stockholders, the satisfaction of the minimum aggregate transaction proceeds amount following redemptions by XPDB’s public stockholders and the receipt of certain governmental and regulatory approvals ; (iv) the failure to obtain financing to complete the proposed business combination and to support the future working capital needs of Montana Technologies ; (v) the effect of the announcement or pendency of the proposed business combination on Montana Technologies’ business relationships, performance, and business generally ; (vi) risks that the proposed business combination disrupts current plans of Montana Technologies and potential difficulties in Montana Technologies’ employee retention as a result of the proposed business combination ; (vii) the outcome of any legal proceedings that may be instituted against XPDB or Montana Technologies related to the agreement and the proposed business combination ; (viii) changes to the proposed structure of the business combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the business combination ; (ix) the ability to maintain the listing of the XPDB’s securities on the NASDAQ ; (x) the price of XPDB’s securities, including volatility resulting from changes in the competitive and highly regulated industries in which Montana Technologies plans to operate, variations in performance across competitors, changes in laws and regulations affecting Montana Technologies’ business and changes in the combined capital structure ; (xi) the ability to implement business plans, forecasts, and other expectations after the completion of the proposed business combination, including the possibility of cost overruns or unanticipated expenses in development programs, and the ability to identify and realize additional opportunities ; (xii) the enforceability of Montana Technologies’ intellectual property, including its patents, and the potential infringement on the intellectual property rights of others, cyber security risks or potential breaches of data security ; and (xiii) other risks and uncertainties set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward - Looking Statements” in XPDB’s Annual Reports on Form 10 - K, Quarterly Reports on Form 10 - Q and Current Reports on Form 8 - K that are available on the website of the Securities and Exchange Commission (the “SEC”) at www . sec . gov and other documents filed, or to be filed with the SEC by XPDB, including the Registration Statement on Form S - 4 initially filed by XPDB with the SEC on August 8 , 2023 (as the same may be amended, the “Registration Statement”) . The foregoing list of factors is not exhaustive . There may be additional risks that neither XPDB or Montana Technologies presently know or that XPDB or Montana Technologies currently believe are immaterial that could also cause actual results to differ from those contained in the forward - looking statements . You should carefully consider the foregoing factors and the other risks and uncertainties that will be described in XPDB’s definitive proxy statement contained in the Registration Statement (as defined below), including those under “Risk Factors” therein, and other documents filed by XPDB from time to time with the SEC . These filings identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward - looking statements . Forward - looking statements speak only as of the date they are made . Readers are cautioned not to put undue reliance on forward - looking statements, and XPDB and Montana Technologies assume no obligation and, except as required by law, do not intend to update or revise these forward - looking statements, whether as a result of new information, future events, or otherwise . Neither XPDB nor Montana Technologies gives any assurance that either XPDB or Montana Technologies will achieve its expectations . DISCLAIMERS

Trademarks These Presentation Materials contain trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners . The use or display of third parties' trademarks, service marks, trade names or products in these Presentation Materials are not intended to, and do not imply, a relationship with XPDB or Montana Technologies, an endorsement or sponsorship by or of XPDB or Montana Technologies, or a guarantee that Montana Technologies or XPDB will work or will continue to work with such third parties . Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in these Presentation Materials may appear without the TM, SM, R or C symbols, but such references are not intended to indicate, in any way, that XPDB, Montana Technologies, or the any third - party will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights . Financial Information The financial information and data contained in this Presentation is unaudited and does not conform to Regulation S - X promulgated under the Securities Act . Accordingly, such information and data may be adjusted in or may be presented differently in any proxy statement or registration statement to be filed by XPDB with the SEC . Additional Information about the Proposed Transaction and Where to Find It In connection with the proposed business combination, XPDB has filed with the SEC the Registration Statement, which includes a preliminary prospectus and preliminary proxy statement of XPDB . The definitive proxy statement/final prospectus and other relevant documents will be sent to all XPDB stockholders as of a record date to be established for voting on the proposed business combination and the other matters to be voted upon at a meeting of XPDB’s stockholders to be held to approve the proposed business combination and other matters (the “Special Meeting”) . XPDB may also file other documents regarding the proposed business combination with the SEC . The definitive proxy statement/final prospectus will contain important information about the proposed business combination and the other matters to be voted upon at the Special Meeting and may contain information that an investor will consider important in making a decision regarding an investment in XPDB’s securities . Before making any voting decision, investors and security holders of XPDB and other interested parties are urged to read the Registration Statement and the proxy statement/prospectus and all other relevant documents filed or that will be filed with the SEC in connection with the proposed business combination as they become available because they will contain important information about the proposed business combination . Investors and security holders will also be able to obtain free copies of the definitive proxy statement/final prospectus and all other relevant documents filed or that will be filed with the SEC by XPDB through the website maintained by the SEC at www . sec . gov, or by directing a request to XPDB, 321 North Clark Street, Suite 2440 , Chicago, IL 60654 , or by contacting Morrow Sodali LLC, XPDB’s proxy solicitor, for help, toll - free at ( 800 ) 662 - 5200 (banks and brokers can call collect at ( 203 ) 658 - 9400 ) . INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN . ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE . Participants in the Solicitation XPDB, Montana Technologies and certain of their respective directors and executive officers may be deemed participants in the solicitation of proxies from XPDB’s stockholders with respect to the proposed business combination . A list of the names of those directors and executive officers of XPDB and a description of their interests in XPDB is set forth in XPDB’s Annual Reports on Form 10 - K, Quarterly Reports on Form 10 - Q and Current Reports on Form 8 - K . Additional information regarding the interests of those persons and other persons who may be deemed participants in the proposed business combination may be obtained by reading the Registration Statement . The documents described in this paragraph are available free of charge at the SEC’s website at www . sec . gov, or by directing a request to XPDB, 321 North Clark Street, Suite 2440 , Chicago, IL 60654 . DISCLAIMERS

Risk Factors For a non - exhaustive description of the risks relating to an investment in a private placement in connection with the Potential Business Combination please review "Risk Factors" at the end of this presentation . Changes and Additional Information in Connection with SEC Filings The information in these Presentation Materials has not been reviewed by the SEC and certain information may not comply in certain respects with SEC rules . As a result, the information in the Registration Statement may differ from these Presentation Materials to comply with SEC rules . The Registration Statement will include substantial additional information about Montana Technologies and XPDB not contained in these Presentation Materials . Once filed, the information in the Registration Statement will update and supersede the information presented in these Presentation Materials . INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE POTENTIAL BUSINESS COMBINATION OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN . ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE . Interests of XPDB’s Directors and Officers in the Merger In addition to the interests of XPDB’s directors and officers described in XPDB’s Annual Reports on Form 10 - K, Quarterly Reports on Form 10 - Q and Current Reports on Form 8 - K, certain members of the board of directors and executive officers of XPDB, the Sponsor, including its directors and executive officers, and their affiliates have interests in the Potential Business Combination that are different from, or in addition to, those of XPDB stockholders generally . In particular : 1. Patrick Eilers, the Chief Executive Officer of XPDB and a member of its board of directors, serves as an advisor to Montana Technologies 2. XPDB will have the right to appoint two members of the initial board of directors following the Business Combination, one of whom will be Patrick Eilers 3. TEP Montana, LLC, an affiliate of Mr. Eilers, is a minority investor in Montana Technologies with board observation rights DISCLAIMERS

Slide 6 Montana Technologies | October 2023 TRANSACTION SUMMARY SUMMARY OF PROPOSED TRANSACTION • Montana Technologies has created a transformational technology that provides significant energy efficiency gains in heating, ventilation, and air conditioning (“HVAC”) and air to potable water applications, all through its proprietary AirJoule tm units – Addresses two of the world’s most problematic issues: demand for energy - efficiency and reduction of refrigerants for HVAC and water stress • Power & Digital Infrastructure Acquisition II Corp. (Nasdaq: "XPDB") is a blank - check company focused on clean tech solutions, supported by long - time energy investor, Pat Eilers (Transition Equity Partners, LLC), and professionals from global advisory firm XMS Capital Partners, LLC, led by Ted Brombach • Montana Technologies and XPDB are combining to raise capital and continue executing on a commercialization strategy with key commercial partners – namely BASF and CATL today and other potential partners in the future – to manufacture AirJoule tm units – Montana Technologies shareholders are rolling 100% of their equity into the combined company – Transaction proceeds are being retained in the business • $500 million Pro Forma Enterprise Value at $10.00 per share (1) – Represents a highly attractive entry valuation relative to market opportunity and peer group metrics • Montana Technologies expects to raise $100 million of gross proceeds, which is expected to be sufficient to fund operations through commercialization, production and deployment XPDB has identified Montana Technologies as a highly differentiated and scalable technology provider that is developing solutions to provide a cleaner energy future across two enormous addressable markets – HVAC and water 1. Excludes earnout provision of up to $200 million at $10.00 per share that may be earned by Montana Technologies’ existing shareholders within 5 years after closing based on annualized EBITDA milestones expected from completion of new production capacity.

Slide 7 Montana Technologies | October 2023 INVESTMENT HIGHLIGHTS • Transformational Technology: 5 – 10x energy reduction, air - to - water and HVAC solutions – Applications across dehumidification, atmospheric water generation and evaporative cooling help solve two of the world’s most problematic issues: demand for energy - efficient HVAC and water stress • Leading Partnerships: – Partnerships help accelerate manufacturing of materials and components as well as provide product validation and commercialization • Capital Efficient and Highly Scalable Business Model: <$50 million capex investment expected to generate ~$100 million EBITDA per line – Montana Technologies expects to self - fund future production lines through capital - efficient production • Large Addressable Market: >$100 billion air - to - water and $355 billion HVAC markets – Scaling to base case production lines would represent a de minimis proportion of the ~$455 billion market • Key Components Plan: Deliver proprietary technology for OEM assembly – MOF - coated contactors to be sold in combination with air pumps, vacuum compressors and water vapor condensers • Strong Management: Team supported by some of the nation’s leading scientists in this area – Combined 140+ years of experience across commercialization, finance, operations and research

Slide 8 Montana Technologies | October 2023 • Over 30 years of experience successfully founding and leading innovative product - based companies • Founded Core Innovation, predecessor to Montana Technologies • Previously founded Jore Corporation, a power tool and accessories manufacturer that exceeded ~$50 million annual revenue • Led Jore Corporation through a successful IPO MONTANA TECHNOLOGIES EXPERIENCED TEAM WITH STRONG TRACK RECORD Matt Jore Founder, CEO Jeff Gutke CFO • Over 25 years of financial, operational and technical experience • Founder of Doxey Capital, a private investment and advisory services firm • Former Managing Director for Talara Capital and a member of the firm’s investment committee • Previously worked at Denham Capital, J.M. Huber Corporation, and Aquila Energy Capital Corporation Dan Gabig VP Business Development • Over 30 years in financial management and strategic corporate development • Financial management at Alumax Inc., a multinational aluminum manufacturer; Scios Inc./Cal Bio, a biotechnology & biopharmaceutical company; Jore Corporation, a power tool accessories manufacturer; and Core Innovation JJ Jenks VP Operations • Over 20 years of research experience • Co - inventor of AirJoule tm and the Harmonic Adsorption Recuperative Power System • Team member in the developed applications for Metal - organic framework nanomaterials • Expertise in thermal fluid sciences MANAGEMENT Pete McGrail CTO • Former staff member at Pacific Northern National Lab (“PNNL”) 39 years, attaining the position of Laboratory Fellow • Managed Applied Functional Materials group at PNNL • Has received five research grant awards from the U.S. Department of Energy’s (“DOE”) Advanced Research Projects Agency - Energy, more than any other researcher in the U.S.

Slide 9 Montana Technologies | October 2023 Badische Anilin und Sodafabrik ("BASF") is the world’s largest chemical producer with facilities around the world • Montana Technologies and BASF have implemented a development agreement for the production of engineered super - porous materials that are applied as a coating to AirJoule tm contactors to perform the energy and water - harvesting function • BASF has successfully produced coatings for AirJoule tm prototypes and is now scaling the processes for mass - production • Montana Technologies is executing its ongoing development agreement for global manufacturing and supply PNNL scientists conceived Self - Regenerating Dehumidifier • Montana Technologies holds worldwide exclusive rights to Self - Regenerating Dehumidifier patents • Montana Technologies has added its own significant advancements and holds independent intellectual property that allows for heating, cooling, and ultra low cost harvesting of fresh water from air • PNNL has validated performance of AirJoule tm prototypes in the lab’s environmental test facilities MONTANA TECHNOLOGIES’ STRATEGIC GLOBAL PARTNERSHIPS CATL is one of the world’s largest Lithium - ion electric vehicle battery manufacturers • CATL and Montana Technologies have executed a joint venture, CAMT Climate Solutions (“CAMT”), to manufacture and commercialize AirJoule tm to reduce CO 2 emissions, especially in Asia (1) • Montana Technologies completed its Series A investment led by CATL and its Series B investment led by an affiliate of Transition Equity Partners in cooperation with CATL Transition Equity Partners provides holistic support for the energy transition 1. Montana Technologies’ joint venture with CATL provides for a 50/50 ownership split and 50/50 sharing of profits in various countries, but provides a 60/40 split of profits in favor of CATL with respect to sales in China. That 50/50 split can be adjusted over time based on the respective capital contributions to the joint venture entity from the parties.

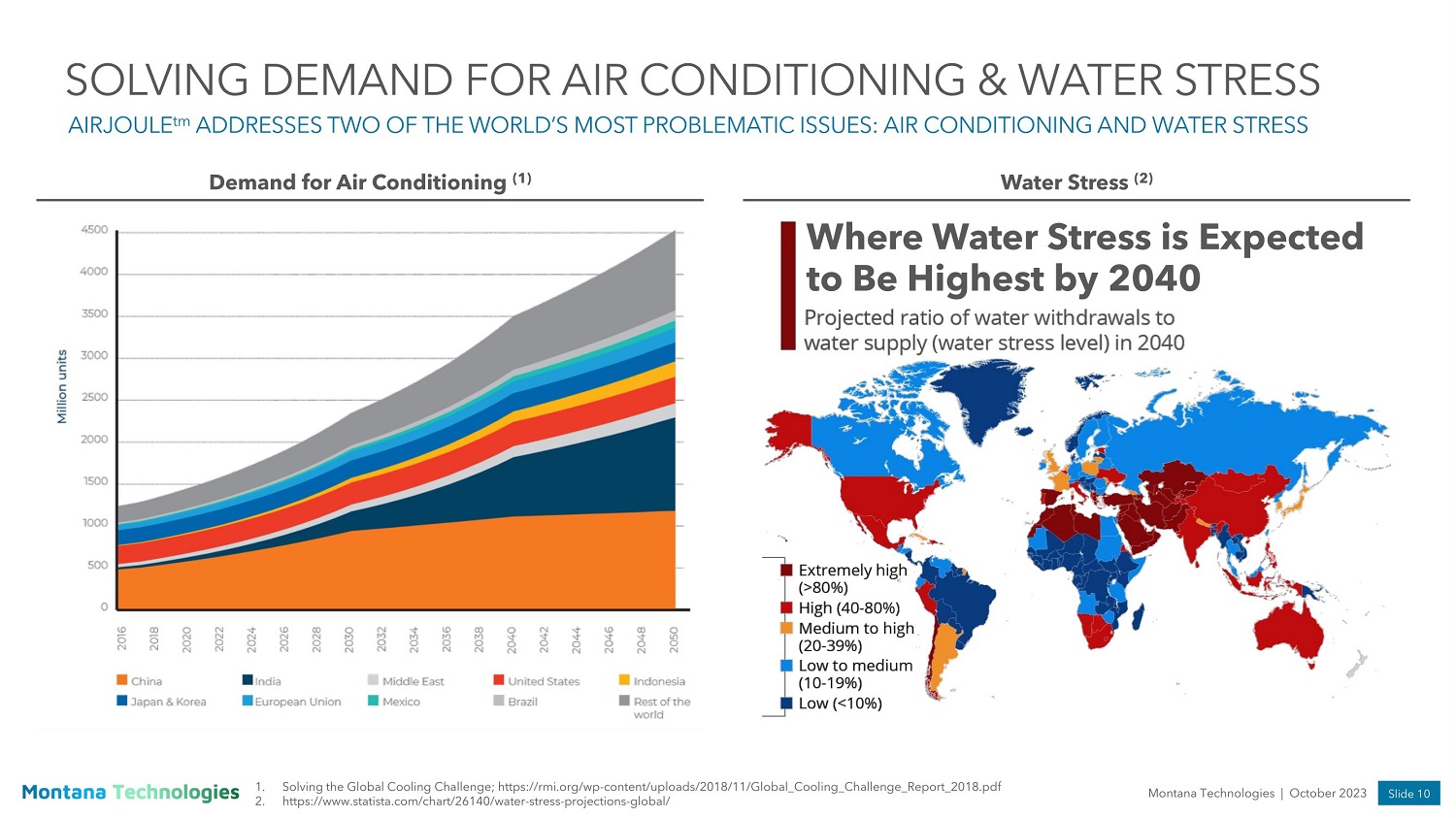

Slide 10 Montana Technologies | October 2023 Demand for Air Conditioning (1) Water Stress (2) SOLVING DEMAND FOR AIR CONDITIONING & WATER STRESS AIRJOULE tm ADDRESSES TWO OF THE WORLD’S MOST PROBLEMATIC ISSUES: AIR CONDITIONING AND WATER STRESS 1. Solving the Global Cooling Challenge; https://rmi.org/wp - content/uploads/2018/11/Global_Cooling_Challenge_Report_2018.pdf 2. http s://w ww. statista.com/chart/2614 0 /water - stress - projections - global/ Where Water Stress is Expected to Be Highest by 2040

Slide 11 Montana Technologies | October 2023 July 11, 2023 The Associated Press (2) EPA Enforcing Stricter Limits on Hydrofluorocarbons (“HFCs”) NEW GOVERNMENT LEGISLATION IS FURTHERING THE NEED FOR AN AIRJOULE tm SYSTEM June 24, 2023 GlobeNewswire (1) ASHRAE Approves Airborne Infection Risk Mitigation Standard for Buildings July 21, 2023 The Washington Post (3) U.S. Government Proposes Rule to Make Water Heaters More Efficient What are HFCs? • Highly potent greenhouse gases commonly used in refrigerators and air conditioners What is being done to limit HFCs? • More than 130 countries have signed a global agreement to phase down production and use of HFCs by 85% over the next 13 years What does the latest rule do? • This rule builds on a 10% reduction required by the end of this year and requires a 40% overall reduction through 2028 • Officials said refrigeration and air conditioning systems sold in the U.S. will emit far fewer HFCs as a result of the rule, the second step in a 15 - year phasedown of chemicals that once dominated refrigeration and cooling What is ASHRAE Standard 241? • Establishes minimum requirements to reduce the risk of disease transmission by exposure to infectious aerosols in buildings Why is the new standard important? • Standard 241 breaks new ground by setting requirements for equivalent clean airflow rate, the flow rate of pathogen free air flow into occupied areas of a building that would have the same effect as the total of outdoor air, filtration of indoor air, and air disinfection by technologies such as germicidal ultraviolet light ─ This approach allows the user of the standard flexibility to select combinations of technologies to comply with the standard that best satisfy their economic constraints and energy use goals Explanation of the new proposal: • Under the terms of the proposal, new electric storage water heaters in the most common size would have to use heat pumps and some gas - fired instantaneous heaters would have to use condensing technology Implications of the new proposal: • Water heating accounts for about 13% of U.S. consumers’ annual residential energy use and utility costs • The change would reduce harmful carbon dioxide emissions by 501 million metric tons over a 30 - year period, while saving Americans $198 billion over the same timespan, equivalent to $11.4 billion on their energy and water bills each year, or an average $1,868 over the life of their electric heater Note: AirJoule tm is a dehumidifier that provides for high moisture - removal efficiency while using less electrical energy compared to conventional dehumidifiers. 1. “ASHRAE Approves Groundbreaking Standard to Reduce the Risk of Disease Transmission in Indoor Spaces,” GlobeNewswire. "ASHRAE" refers to the American Society of Heating, Refrigerating and Air - Conditioning Engineers. 2. “EPA sets stricter limits on hydrofluorocarbons used in refrigerators, air conditioners,” The Associated Press. 3. “New rule aims to make outdated home water heaters cheaper and greener,” The Washington Post.

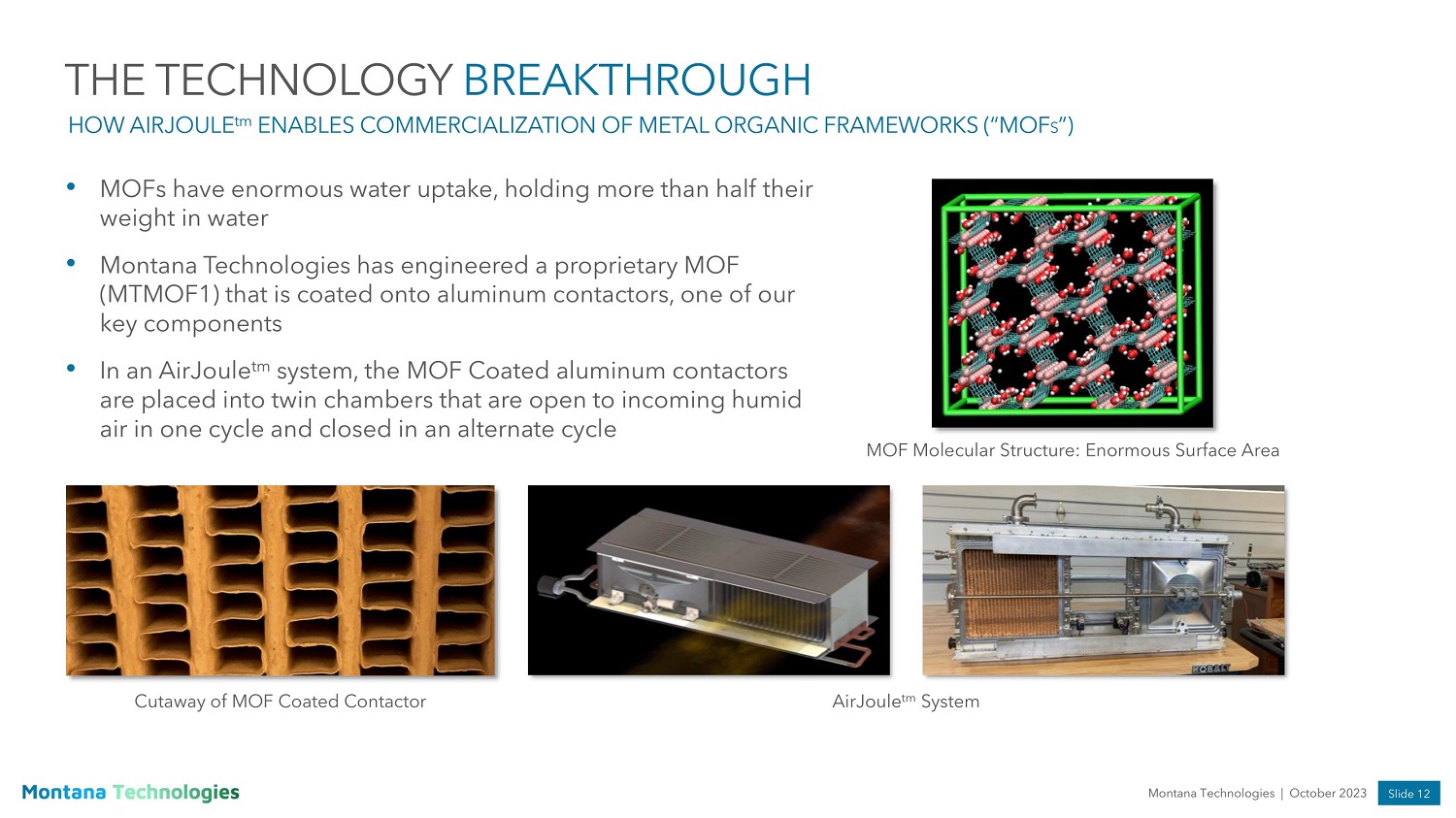

Slide 12 Montana Technologies | October 2023 THE TECHNOLOGY BREAKTHROUGH HOW AIRJOULE tm ENABLES COMMERCIALIZATION OF METAL ORGANIC FRAMEWORKS (“MOF S ”) AirJoule tm System • MOFs have enormous water uptake, holding more than half their weight in water • Montana Technologies has engineered a proprietary MOF (MTMOF1) that is coated onto aluminum contactors, one of our key components • In an AirJoule tm system, the MOF Coated aluminum contactors are placed into twin chambers that are open to incoming humid air in one cycle and closed in an alternate cycle MOF Molecular Structure: Enormous Surface Area Cutaway of MOF Coated Contactor

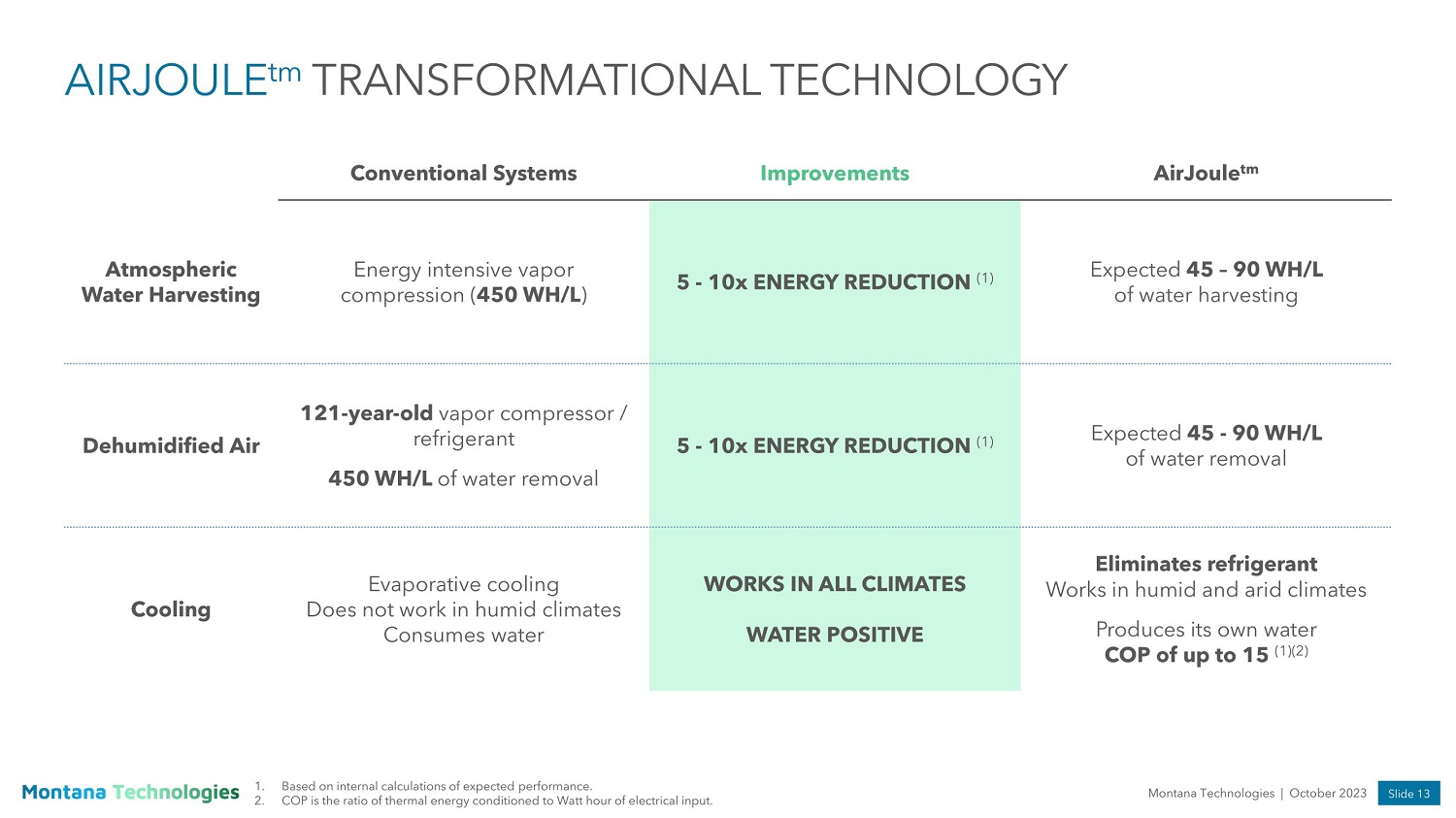

Slide 13 Montana Technologies | October 2023 AIRJOULE tm TRANSFORMATIONAL TECHNOLOGY AirJoule tm Improvements Conventional Systems Expected 45 – 90 WH/L of water harvesting 5 - 10x ENERGY REDUCTION (1) Energy intensive vapor compression ( 450 WH/L ) Atmospheric Water Harvesting Expected 45 - 90 WH/L of water removal 5 - 10x ENERGY REDUCTION (1) 121 - year - old vapor compressor / refrigerant 450 WH/L of water removal Dehumidified Air Eliminates refrigerant Works in humid and arid climates Produces its own water COP of up to 15 (1)(2) WORKS IN ALL CLIMATES WATER POSITIVE Evaporative cooling Does not work in humid climates Consumes water Cooling 1. Based on internal calculations of expected performance. 2. COP is the ratio of thermal energy conditioned to Watt hour of electrical input.

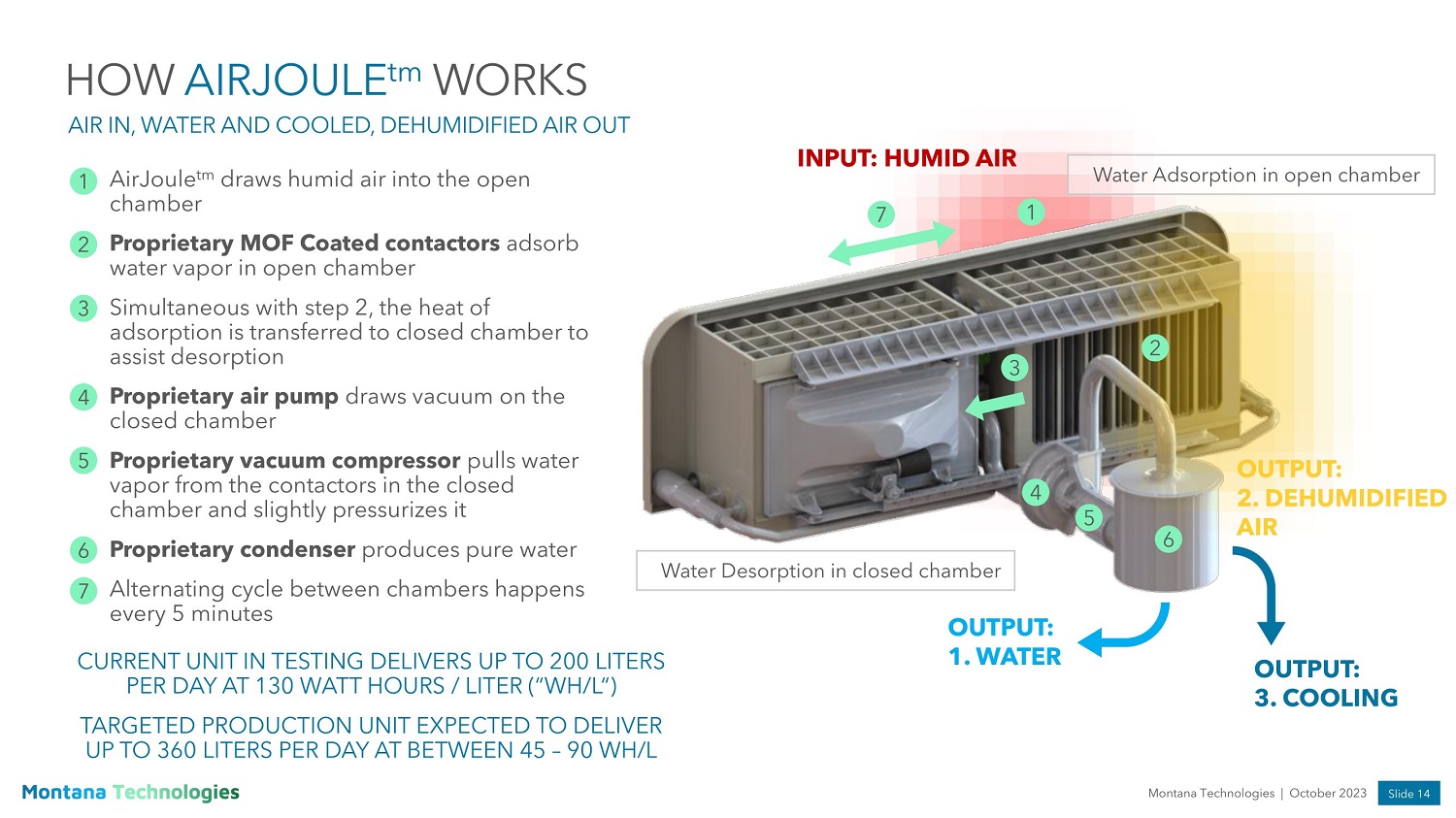

Slide 14 Montana Technologies | October 2023 HOW AIRJOULE tm WORKS AIR IN, WATER AND COOLED, DEHUMIDIFIED AIR OUT CURRENT UNIT IN TESTING DELIVERS UP TO 200 LITERS PER DAY AT 130 WATT HOURS / LITER (“WH/L“) TARGETED PRODUCTION UNIT EXPECTED TO DELIVER UP TO 360 LITERS PER DAY AT BETWEEN 45 – 90 WH/L OUTPUT: 1. WATER OUTPUT: 3. COOLING Water Desorption in closed chamber 3 4 5 6 7 1 2 3 4 AirJoule tm draws humid air into the open chamber Proprietary MOF Coated contactors adsorb water vapor in open chamber Simultaneous with step 2, the heat of adsorption is transferred to closed chamber to assist desorption Proprietary air pump draws vacuum on the closed chamber 5 Proprietary vacuum compressor pulls water vapor from the contactors in the closed chamber and slightly pressurizes it Proprietary condenser produces pure water Alternating cycle between chambers happens every 5 minutes 6 7 1 2 INPUT: HUMID AIR Water Adsorption in open chamber OUTPUT: 2. DEHUMIDIFIED AIR

Slide 15 Montana Technologies | October 2023 THE TECHNOLOGY BREAKTHROUGH AIRJOULE tm ENABLES THE AMAZING CHARACTERISTICS OF ENGINEERED SUPER - POROUS MATERIALS TO BE REALIZED MOFs are super adsorbent materials Thermal constraints have limited the potential of MOFs in historical dehumidification efforts First, when MOFs take up (adsorb) water vapor, they generate heat (heat of adsorption). This heat goes into the airstream…not good for cooling Next, the MOF must release (desorb) the water vapor to continue the cycle and historical efforts have required substantial energy to provide heat to do this…not good for economics AirJoule tm solves the issues of energetics AirJoule tm ’s proprietary pressure swing system integrates adsorption and desorption functions, so the heat of adsorption can be used to assist desorption under vacuum, eliminating the need for additional energy The result is a dramatic reduction in energy and cost, production of water, and reduction of CO 2 emissions

Slide 16 Montana Technologies | October 2023 Cost of Water per Liter $0.3700 - $1.3200 (6) $0.0160 - $0.0630 (5) $0.005 - $0.0200 Water Delivered in 3 to 5 Gallon Jugs Tanker Truck Delivery of Bulk Water Base Cost of AirJoule tm Produced Water AIRJOULE tm COMPARATIVE ANALYSIS (1)(2) AIRJOULE tm IS A TRANSFORMATIONAL TECHNOLOGY WITH APPLICATIONS ACROSS COMMERCIAL DEHUMIDIFICATION, ATMOSPHERIC WATER GENERATION AND COOLING Commercial Dehumidification Atmospheric Water Harvesting Cooling Purchase Cost of Dehumidification System ~$25,400 (4) ~$13,395 (3) < 50% of Competing Systems Silica Gel Desiccant System Dewpoint Control System AirJoule tm Unit AirJoule tm Annual Energy Cost Savings $10,273 - $19,039 (4) $5,898 - $6,911 (3) Compared to Silica Gel Desiccant System Compared to Dewpoint Control System AirJoule tm is expected to cost less than 50% of the upfront cost and use dramatically lower electricity than conventional dehumidification systems. AirJoule tm also generates water and its additionality should generate material carbon credits AirJoule tm is designed to enable evaporative cooling in regions where it is typically ineffective. The energy cost savings derived by using an AirJoule tm dehumidifier are expected to have a payback period of 1.5 years AirJoule tm Annual Energy Cost Savings per Ton 66% Savings $1,475 Compared to Air - Cooled Chiller Plant AirJoule tm Enabled Evaporative Cooling Efficiency 1.5 kWh/ton (7) 0.5 kWh/ton Air - Cooled Chiller Plant AirJoule tm Enabled Evaporative Cooling Amortizing an AirJoule tm atmospheric water generation system, with a projected purchase price of less than 50% of comparable systems over a ten - year life span, produces more than 1,300,000 liters and is cheaper than delivered water 1. Based on internal calculations of expected performance. 2. Assumes price of $0.17 kWh and operating 24 hours per day: (http s://w ww. bls.gov/c h arts/consumer - price - index/consumer - price - index - average - price - data.htm) 3. Quest Model 876 High Efficiency Dehumidifier. 4. Bry - Air Model MP - 900 Silica Gel Dehumidifier. 5. http s://w ww.m rwaterdelivery.co.za/pricing/ 6. http s://w ww. fixr.c o m/costs/bottled - water - delivery 7. http s://w ww.c semag.com/articles/air - versus - water - cooled - chilled - water - plants/

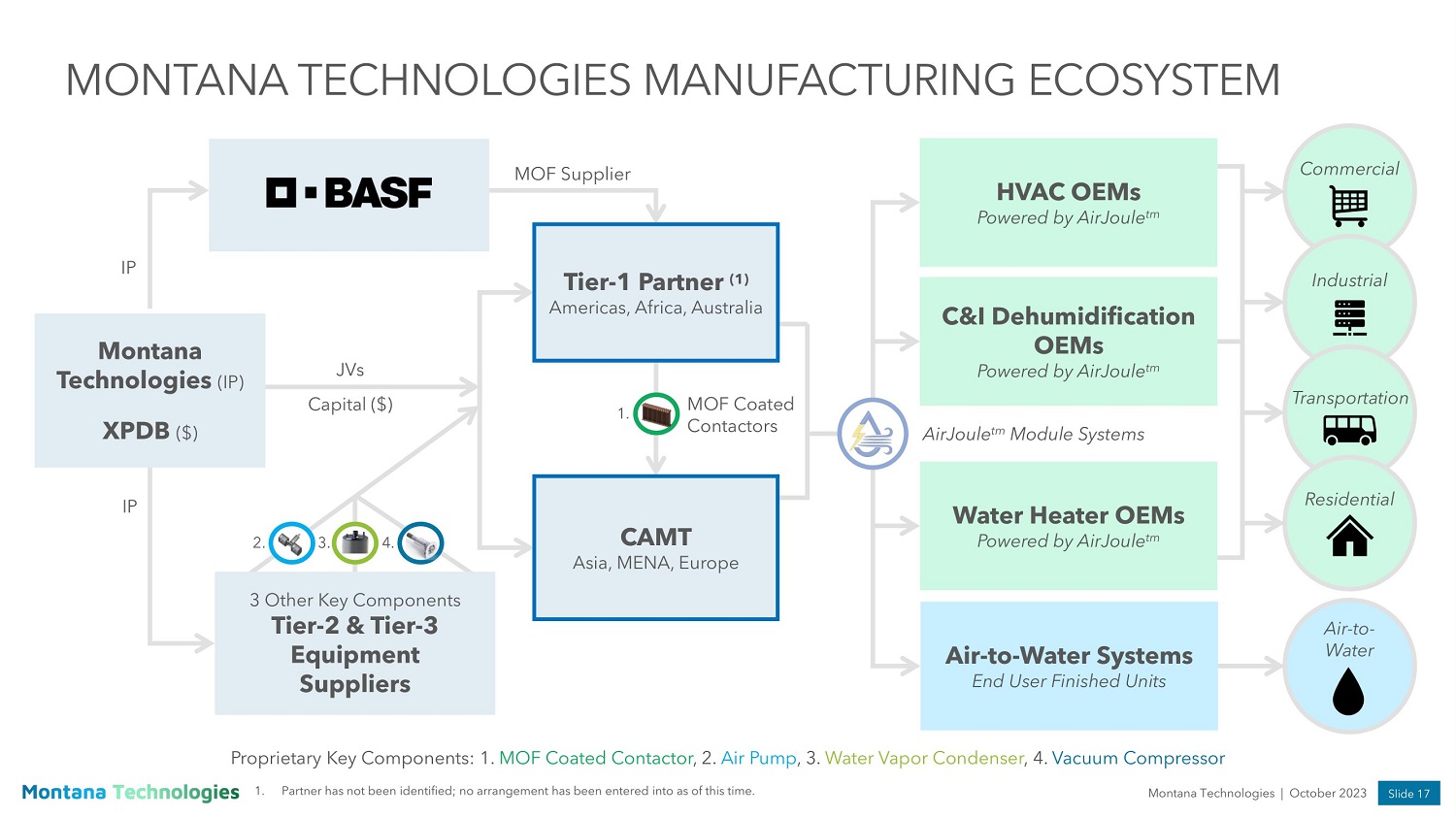

Slide 17 Montana Technologies | October 2023 MONTANA TECHNOLOGIES MANUFACTURING ECOSYSTEM Proprietary Key Components: 1. MOF Coated Contactor , 2. Air Pump , 3. Water Vapor Condenser , 4. Vacuum Compressor HVAC OEMs Powered by AirJoule tm Air - to - Water Systems End User Finished Units AirJoule tm Commercial Industrial Transportation Residential Air - to - Water MOF Supplier AirJoule tm Module Systems IP IP 3 Other Key Components Tier - 2 & Tier - 3 Equipment Suppliers Montana Technologies (IP) XPDB ($) 2. 3. 4. JVs Capital ($) 1. Partner has not been identified; no arrangement has been entered into as of this time. C&I Dehumidification OEMs Powered by AirJoule tm Water Heater OEMs Powered by AirJoule tm Tier - 1 Partner (1) Americas, Africa, Australia 1. MOF Coated Contactors CAMT Asia, MENA, Europe

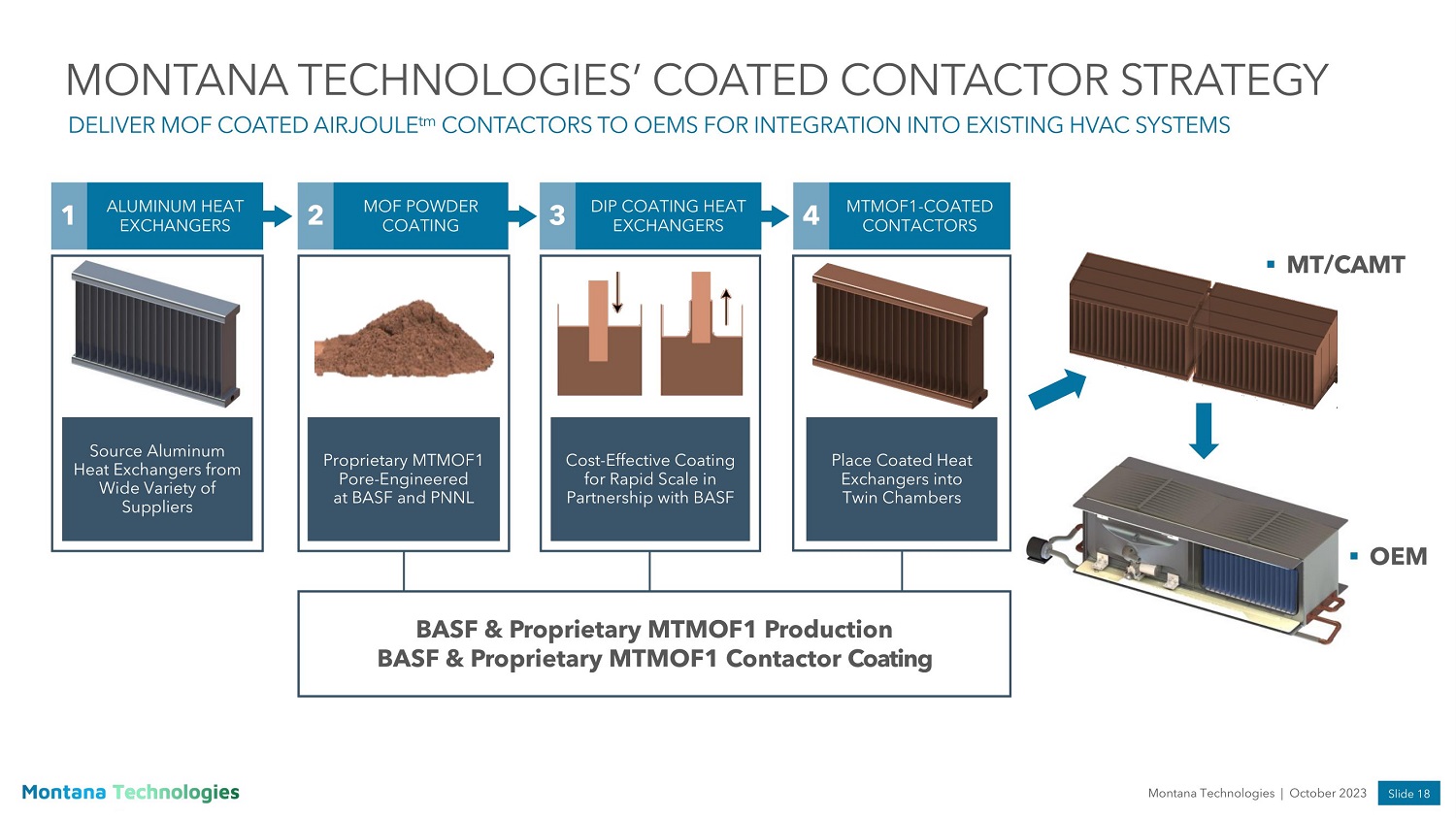

Slide 18 Montana Technologies | October 2023 MONTANA TECHNOLOGIES’ COATED CONTACTOR STRATEGY DELIVER MOF COATED AIRJOULE tm CONTACTORS TO OEMS FOR INTEGRATION INTO EXISTING HVAC SYSTEMS Source Aluminum Heat Exchangers from Wide Variety of Suppliers 1 ALUMINUM HEAT EXCHANGERS 2 MOF POWDER COATING Proprietary MTMOF1 Pore - Engineered at BASF and PNNL 3 DIP COATING HEAT EXCHANGERS Cost - Effective Coating for Rapid Scale in Partnership with BASF 4 MTMOF1 - COATED CONTACTORS Place Coated Heat Exchangers into Twin Chambers BASF & Proprietary MTMOF1 Production BASF & Proprietary MTMOF1 Contactor Coating ▪ MT/CAMT ▪ OEM

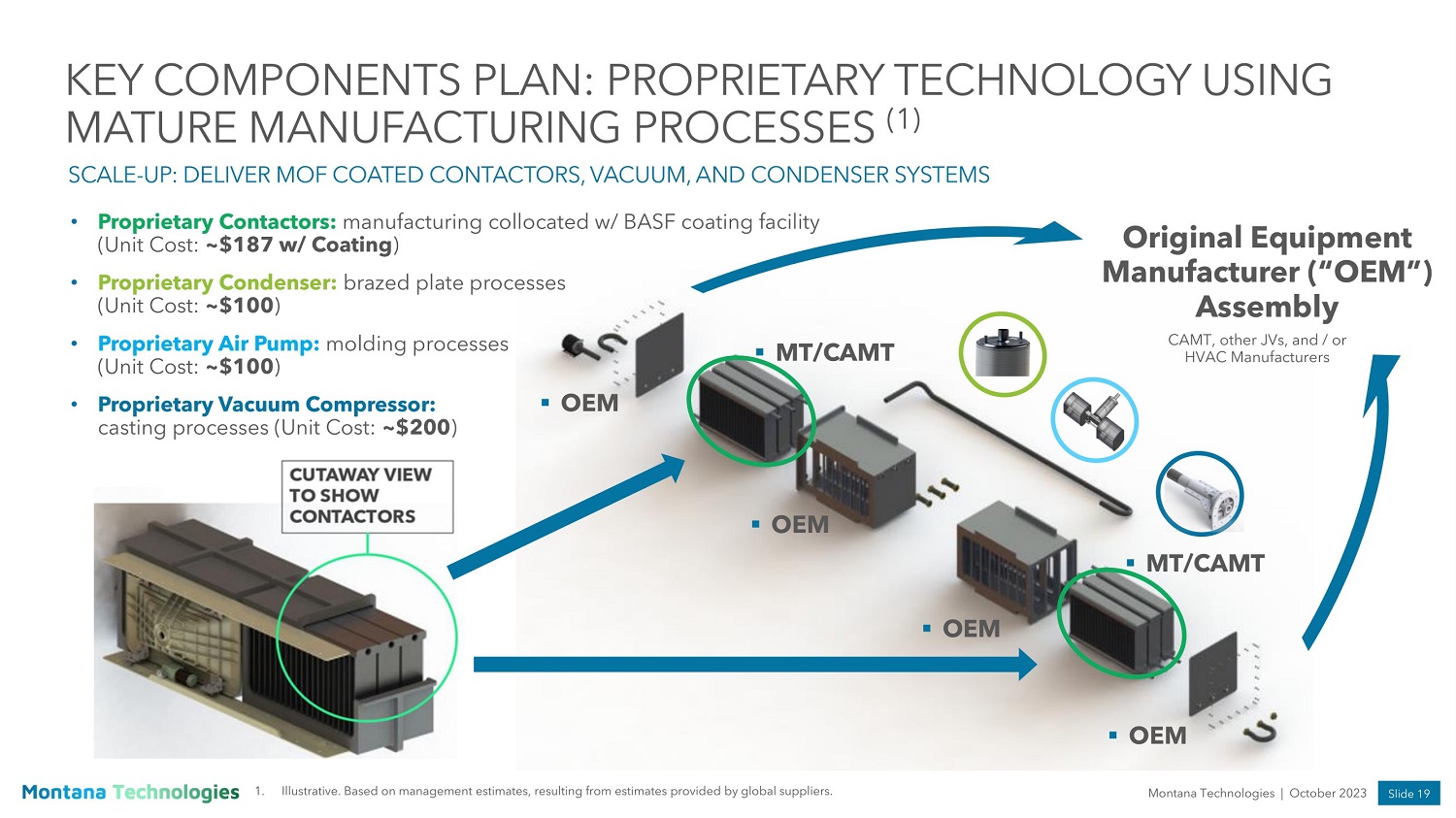

Slide 19 Montana Technologies | October 2023 KEY COMPONENTS PLAN: PROPRIETARY TECHNOLOGY USING MATURE MANUFACTURING PROCESSES (1) SCALE - UP: DELIVER MOF COATED CONTACTORS, VACUUM, AND CONDENSER SYSTEMS ▪ MT/CAMT ▪ OEM ▪ OEM ▪ OEM ▪ OEM ▪ MT/CAMT • Proprietary Contactors: manufacturing collocated w/ BASF coating facility (Unit Cost: ~$187 w/ Coating ) • Proprietary Condenser: brazed plate processes (Unit Cost: ~$100 ) • Proprietary Air Pump: molding processes (Unit Cost: ~$100 ) • Proprietary Vacuum Compressor: casting processes (Unit Cost: ~$200 ) Original Equipment Manufacturer (“OEM”) Assembly CAMT, other JVs, and / or HVAC Manufacturers 1. Illustrative. Based on management estimates, resulting from estimates provided by global suppliers.

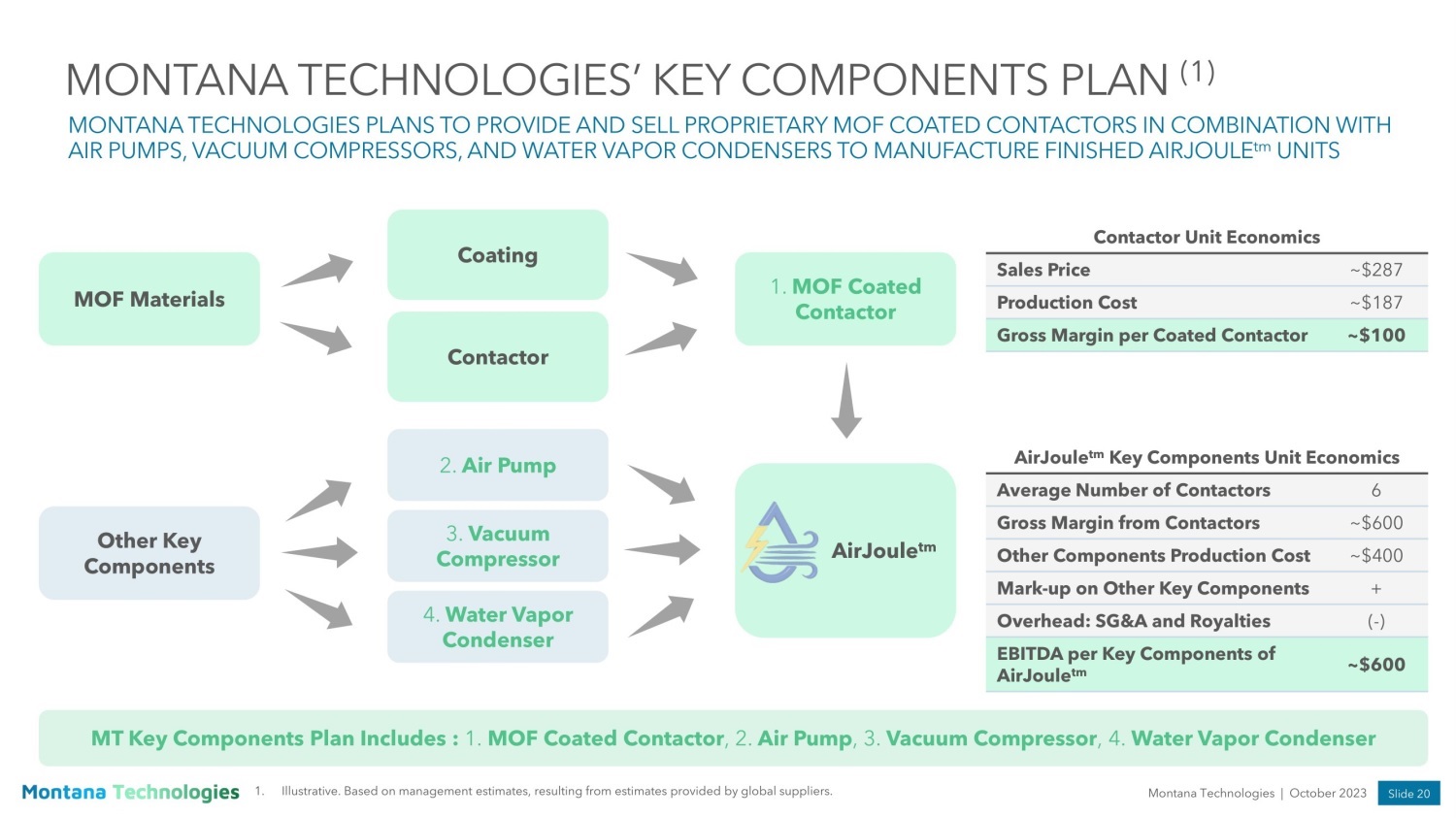

Slide 20 Montana Technologies | October 2023 MONTANA TECHNOLOGIES’ KEY COMPONENTS PLAN (1) MONTANA TECHNOLOGIES PLANS TO PROVIDE AND SELL PROPRIETARY MOF COATED CONTACTORS IN COMBINATION WITH AIR PUMPS, VACUUM COMPRESSORS, AND WATER VAPOR CONDENSERS TO MANUFACTURE FINISHED AIRJOULE tm UNITS MOF Materials Contactor Coating 1. MOF Coated Contactor Other Key Components 2. Air Pump 4. Water Vapor Condenser 3. Vacuum Compressor Contactor Unit Economics ~$287 Sales Price ~$187 Production Cost ~$100 Gross Margin per Coated Contactor AirJoule tm Key Components Unit Economics 6 Average Number of Contactors ~$600 Gross Margin from Contactors ~$400 Other Components Production Cost + Mark - up on Other Key Components ( - ) Overhead: SG&A and Royalties ~$600 EBITDA per Key Components of AirJoule tm AirJoule tm 1. Illustrative. Based on management estimates, resulting from estimates provided by global suppliers. MT Key Components Plan Includes : 1. MOF Coated Contactor , 2. Air Pump , 3. Vacuum Compressor , 4. Water Vapor Condenser

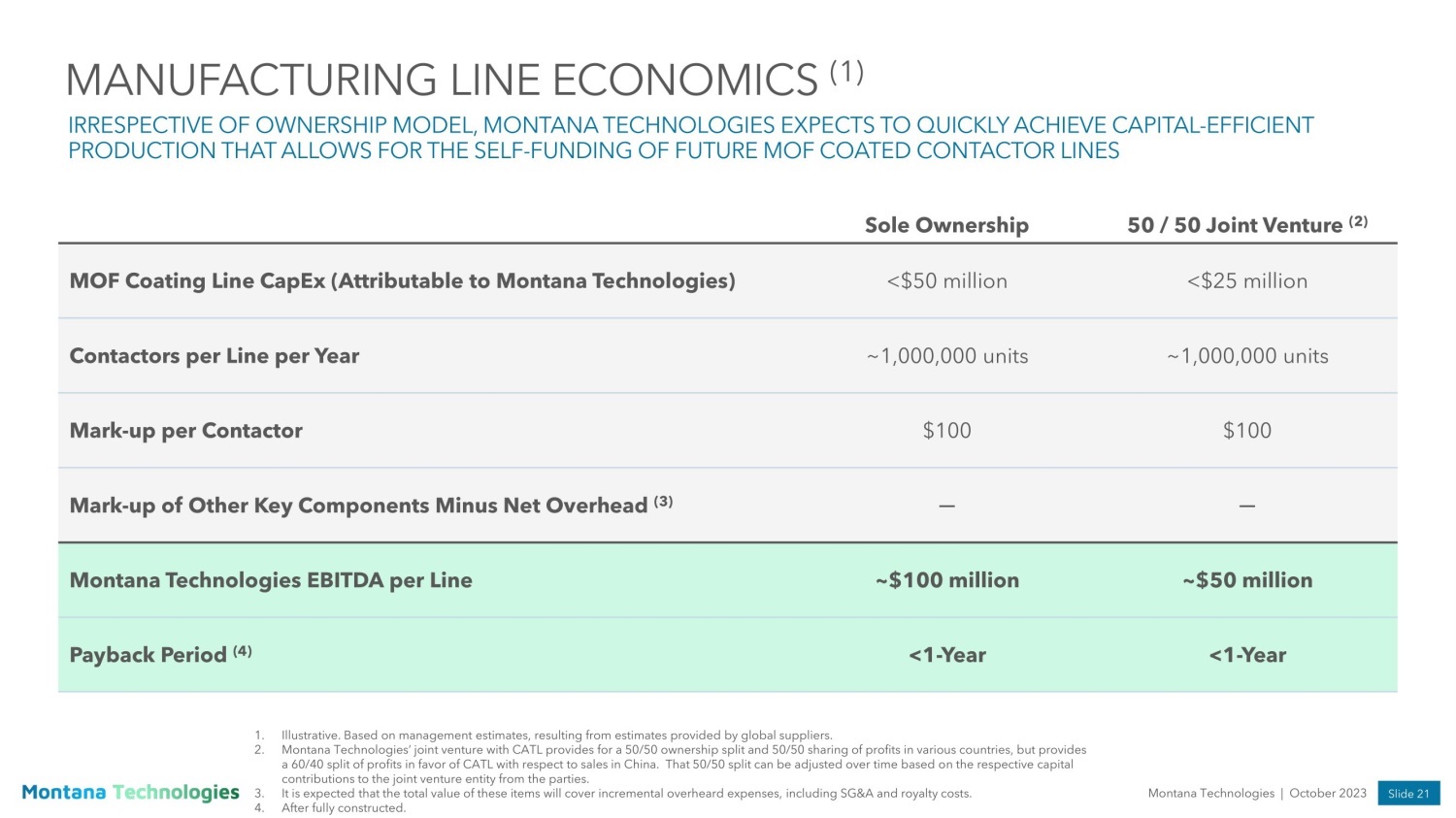

Slide 21 Montana Technologies | October 2023 MANUFACTURING LINE ECONOMICS (1) IRRESPECTIVE OF OWNERSHIP MODEL, MONTANA TECHNOLOGIES EXPECTS TO QUICKLY ACHIEVE CAPITAL - EFFICIENT PRODUCTION THAT ALLOWS FOR THE SELF - FUNDING OF FUTURE MOF COATED CONTACTOR LINES 50 / 50 Joint Venture (2) Sole Ownership <$25 million <$50 million MOF Coating Line CapEx (Attributable to Montana Technologies) ~1,000,000 units ~1,000,000 units Contactors per Line per Year $100 $100 Mark - up per Contactor ─ ─ Mark - up of Other Key Components Minus Net Overhead (3) ~$50 million ~$100 million Montana Technologies EBITDA per Line <1 - Year <1 - Year Payback Period (4) 1. Illustrative. Based on management estimates, resulting from estimates provided by global suppliers. 2. Montana Technologies’ joint venture with CATL provides for a 50/50 ownership split and 50/50 sharing of profits in various countries, but provides a 60/40 split of profits in favor of CATL with respect to sales in China. That 50/50 split can be adjusted over time based on the respective capital contributions to the joint venture entity from the parties. 3. It is expected that the total value of these items will cover incremental overheard expenses, including SG&A and royalty costs. 4. After fully constructed.

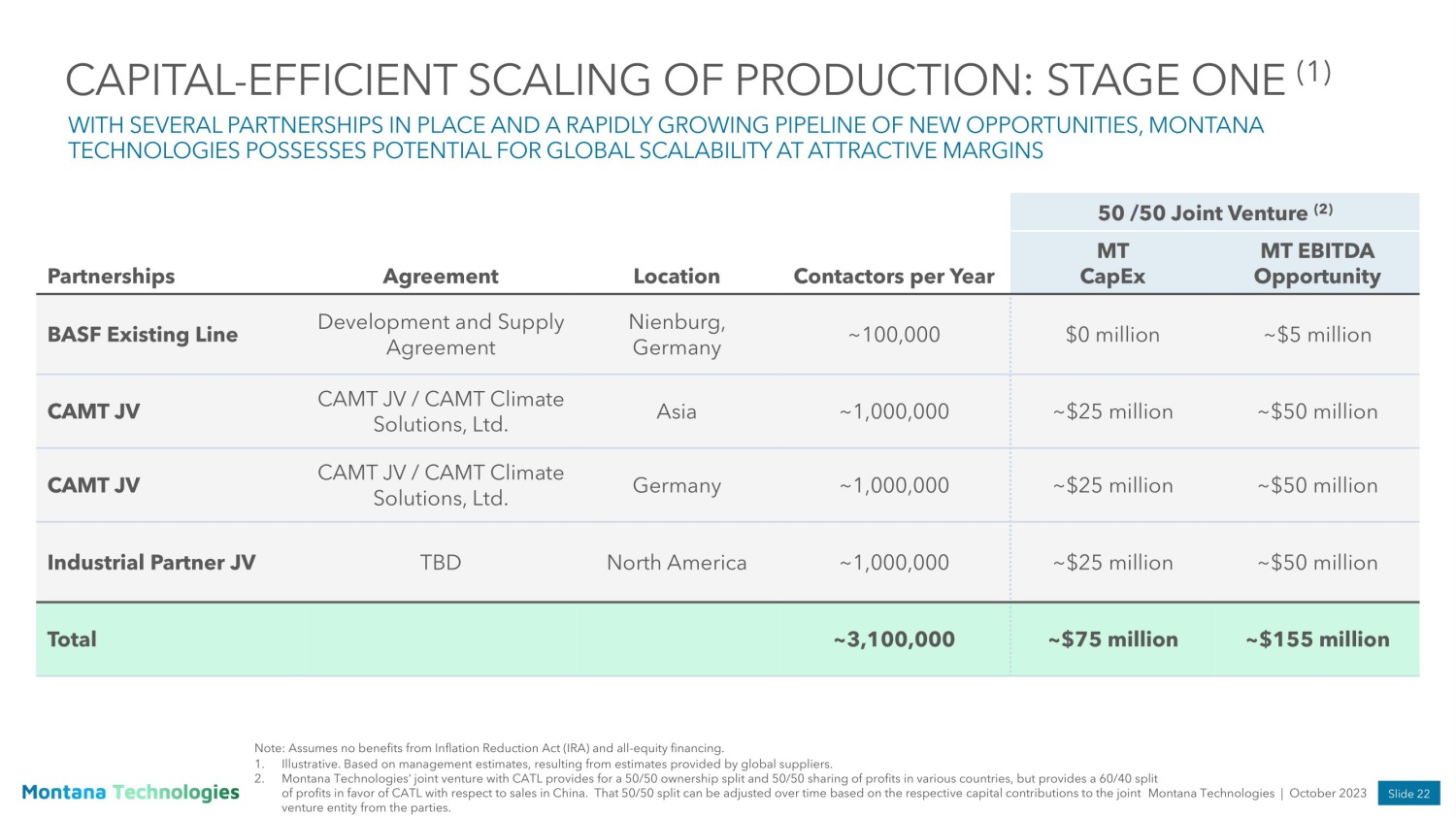

Slide 22 Note: Assumes no benefits from Inflation Reduction Act (IRA) and all - equity financing. 1. Illustrative. Based on management estimates, resulting from estimates provided by global suppliers. 2. Montana Technologies’ joint venture with CATL provides for a 50/50 ownership split and 50/50 sharing of profits in various countries, but provides a 60/40 split of profits in favor of CATL with respect to sales in China. That 50/50 split can be adjusted over time based on the respective capital contributions to the joint Montana Technologies | October 2023 venture entity from the parties. CAPITAL - EFFICIENT SCALING OF PRODUCTION: STAGE ONE (1) WITH SEVERAL PARTNERSHIPS IN PLACE AND A RAPIDLY GROWING PIPELINE OF NEW OPPORTUNITIES, MONTANA TECHNOLOGIES POSSESSES POTENTIAL FOR GLOBAL SCALABILITY AT ATTRACTIVE MARGINS 50 /50 Joint Venture (2) MT EBITDA Opportunity MT CapEx Contactors per Year Location Agreement Partnerships ~$5 million $0 million ~100,000 Nienburg, Germany Development and Supply Agreement BASF Existing Line ~$50 million ~$25 million ~1,000,000 Asia CAMT JV / CAMT Climate Solutions, Ltd. CAMT JV ~$50 million ~$25 million ~1,000,000 Germany CAMT JV / CAMT Climate Solutions, Ltd. CAMT JV ~$50 million ~$25 million ~1,000,000 North America TBD Industrial Partner JV ~$155 million ~$75 million ~3,100,000 Total

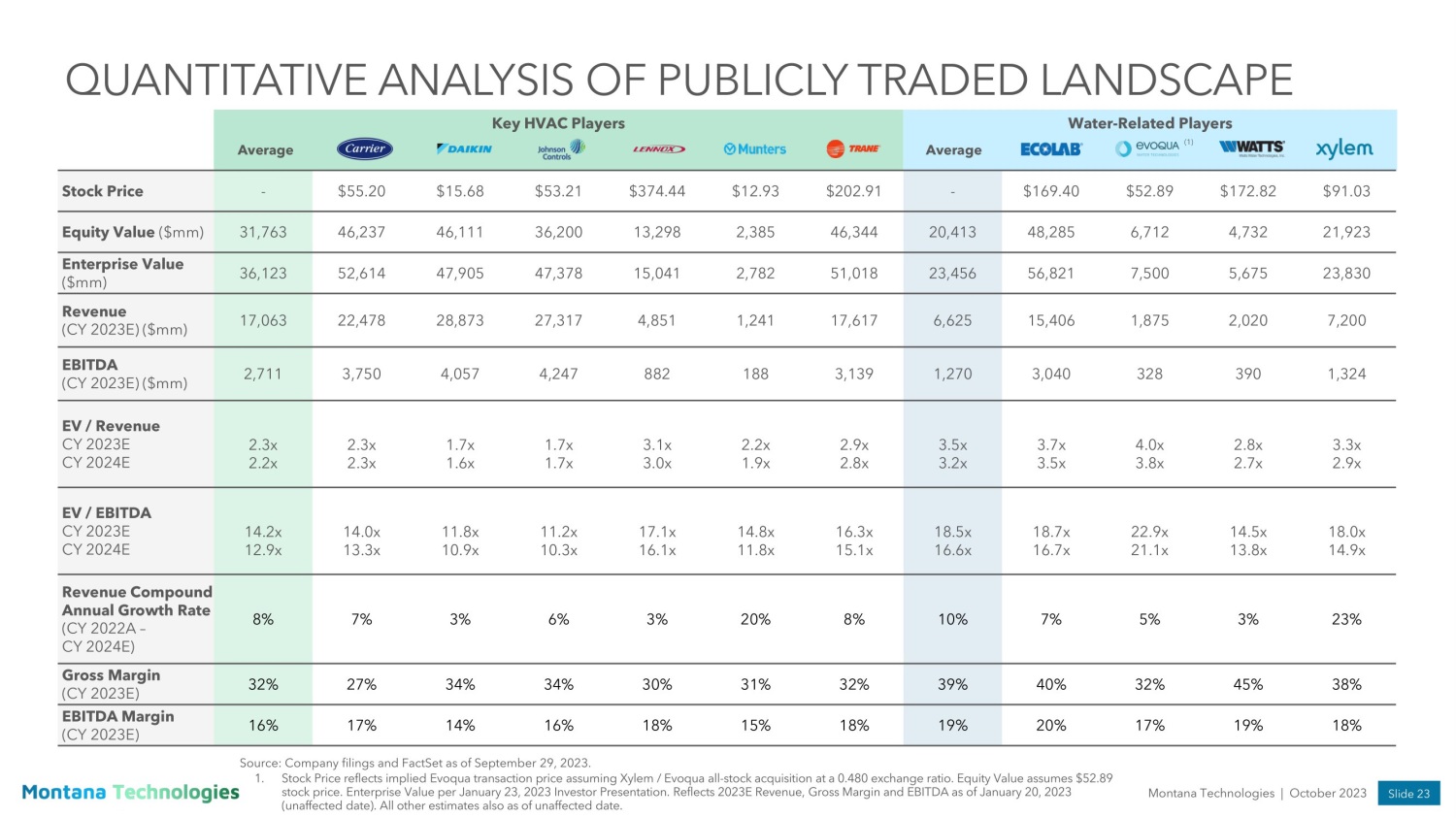

Slide 23 Montana Technologies | October 2023 Water - Related Players (1) Average Key HVAC Players Average $91.03 $172.82 $52.89 $169.40 - $202.91 $12.93 $374.44 $53.21 $15.68 $55.20 - Stock Price 21,923 4,732 6,712 48,285 20,413 46,344 2,385 13,298 36,200 46,111 46,237 31,763 Equity Value ($mm) 23,830 5,675 7,500 56,821 23,456 51,018 2,782 15,041 47,378 47,905 52,614 36,123 Enterprise Value ($mm) 7,200 2,020 1,875 15,406 6,625 17,617 1,241 4,851 27,317 28,873 22,478 17,063 Revenue (CY 2023E) ($mm) 1,324 390 328 3,040 1,270 3,139 188 882 4,247 4,057 3,750 2,711 EBITDA (CY 2023E) ($mm) 3.3x 2.9x 2.8x 2.7x 4.0x 3.8x 3.7x 3.5x 3.5x 3.2x 2.9x 2.8x 2.2x 1.9x 3.1x 3.0x 1.7x 1.7x 1.7x 1.6x 2.3x 2.3x 2.3x 2.2x EV / Revenue CY 2023E CY 2024E 18.0x 14.9x 14.5x 13.8x 22.9x 21.1x 18.7x 16.7x 18.5x 16.6x 16.3x 15.1x 14.8x 11.8x 17.1x 16.1x 11.2x 10.3x 11.8x 10.9x 14.0x 13.3x 14.2x 12.9x EV / EBITDA CY 2023E CY 2024E 23% 3% 5% 7% 10% 8% 20% 3% 6% 3% 7% 8% Revenue Compound Annual Growth Rate (CY 2022 A – CY 2024 E) 38% 45% 32% 40% 39% 32% 31% 30% 34% 34% 27% 32% Gross Margin (CY 2023E) 18% 19% 17% 20% 19% 18% 15% 18% 16% 14% 17% 16% EBITDA Margin (CY 2023E) QUANTITATIVE ANALYSIS OF PUBLICLY TRADED LANDSCAPE Source: Company filings and FactSet as of September 29, 2023. 1. Stock Price reflects implied Evoqua transaction price assuming Xylem / Evoqua all - stock acquisition at a 0.480 exchange ratio. Equity Value assumes $52.89 stock price. Enterprise Value per January 23, 2023 Investor Presentation. Reflects 2023E Revenue, Gross Margin and EBITDA as of January 20, 2023 (unaffected date). All other estimates also as of unaffected date.

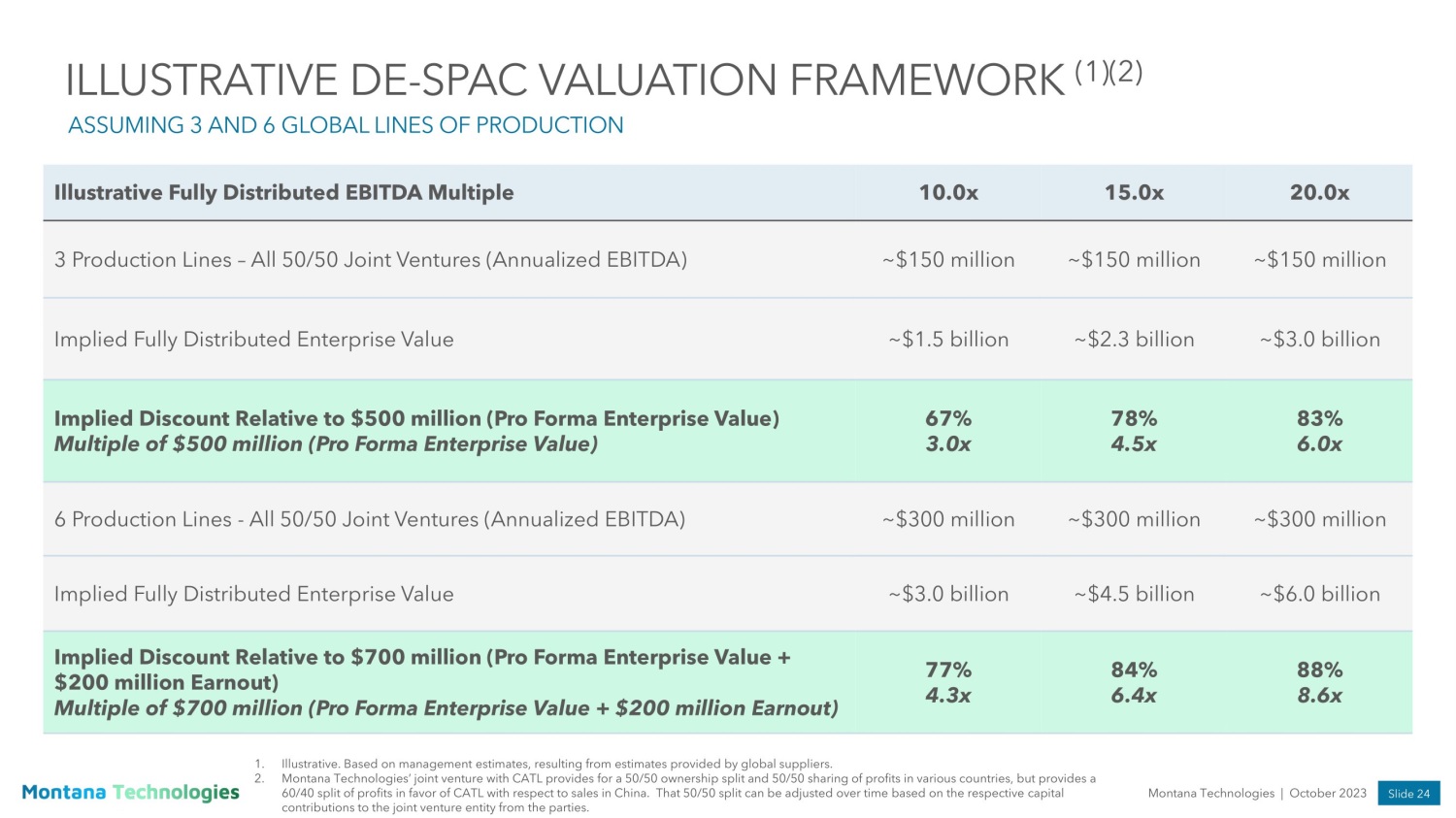

Slide 24 Montana Technologies | October 2023 ILLUSTRATIVE DE - SPAC VALUATION FRAMEWORK (1)(2) ASSUMING 3 AND 6 GLOBAL LINES OF PRODUCTION 20.0x 15.0x 10.0x Illustrative Fully Distributed EBITDA Multiple ~$150 million ~$150 million ~$150 million 3 Production Lines – All 50/50 Joint Ventures (Annualized EBITDA) ~$3.0 billion ~$2.3 billion ~$1.5 billion Implied Fully Distributed Enterprise Value 83% 6.0x 78% 4.5x 67% 3.0x Implied Discount Relative to $500 million (Pro Forma Enterprise Value) Multiple of $500 million (Pro Forma Enterprise Value) ~$300 million ~$300 million ~$300 million 6 Production Lines - All 50/50 Joint Ventures (Annualized EBITDA) ~$6.0 billion ~$4.5 billion ~$3.0 billion Implied Fully Distributed Enterprise Value 88% 8.6x 84% 6.4x 77% 4.3x Implied Discount Relative to $700 million (Pro Forma Enterprise Value + $200 million Earnout) Multiple of $700 million (Pro Forma Enterprise Value + $200 million Earnout) 1. Illustrative. Based on management estimates, resulting from estimates provided by global suppliers. 2. Montana Technologies’ joint venture with CATL provides for a 50/50 ownership split and 50/50 sharing of profits in various countries, but provides a 60/40 split of profits in favor of CATL with respect to sales in China. That 50/50 split can be adjusted over time based on the respective capital contributions to the joint venture entity from the parties.

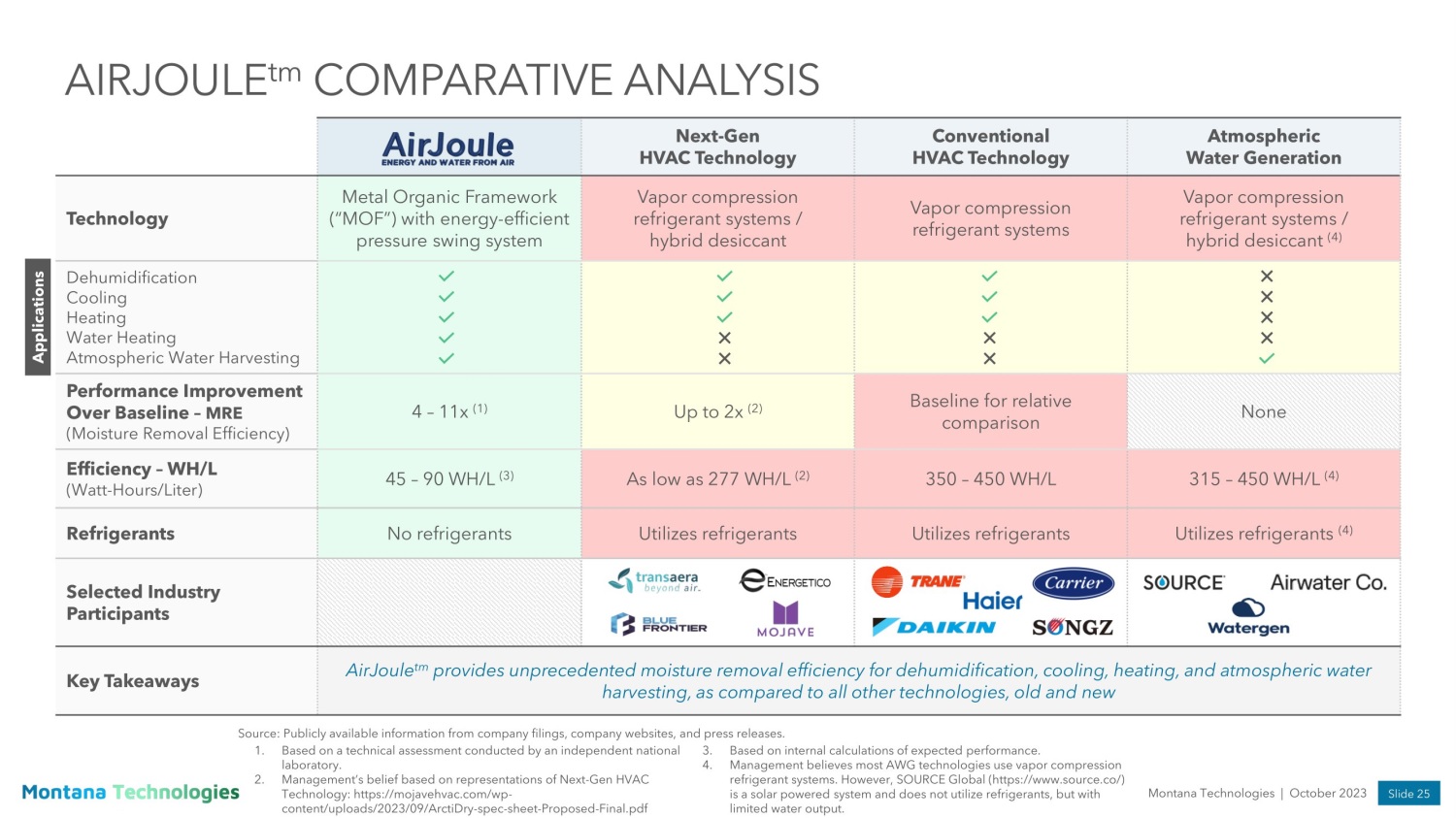

Slide 25 Montana Technologies | October 2023 AIRJOULE tm COMPARATIVE ANALYSIS Atmospheric Water Generation Conventional HVAC Technology Next - Gen HVAC Technology Vapor compression refrigerant systems / hybrid desiccant ( 4 ) Vapor compression refrigerant systems Vapor compression refrigerant systems / hybrid desiccant Metal Organic Framework (“MOF”) with energy - efficient pressure swing system Technology Dehumidification Cooling Heating Water Heating Atmospheric Water Harvesting Applications None Baseline for relative comparison Up to 2x (2) 4 – 11x (1) Performance Improvement Over Baseline – MRE (Moisture Removal Efficiency) 315 – 450 WH/L (4) 350 – 450 WH/L As low as 277 WH/L (2) 45 – 90 WH/L (3) Efficiency – WH/L (Watt - Hours/Liter) Utilizes refrigerants (4) Utilizes refrigerants Utilizes refrigerants No refrigerants Refrigerants Selected Industry Participants AirJoule tm provides unprecedented moisture removal efficiency for dehumidification, cooling, heating, and atmospheric water harvesting, as compared to all other technologies, old and new Key Takeaways 1. Based on a technical assessment conducted by an independent national laboratory. 2. Management’s belief based on representations of Next - Gen HVAC Technology: https://mojavehvac.com/wp - content/uploads/2023/09/ArctiDry - spec - sheet - Proposed - Final.pdf 3. Based on internal calculations of expected performance. 4. Management believes most AWG technologies use vapor compression refrigerant systems. However, SOURCE Global (http s://w ww. source.co/ ) is a solar powered system and does not utilize refrigerants, but with limited water output. Source: Publicly available information from company filings, company websites, and press releases.

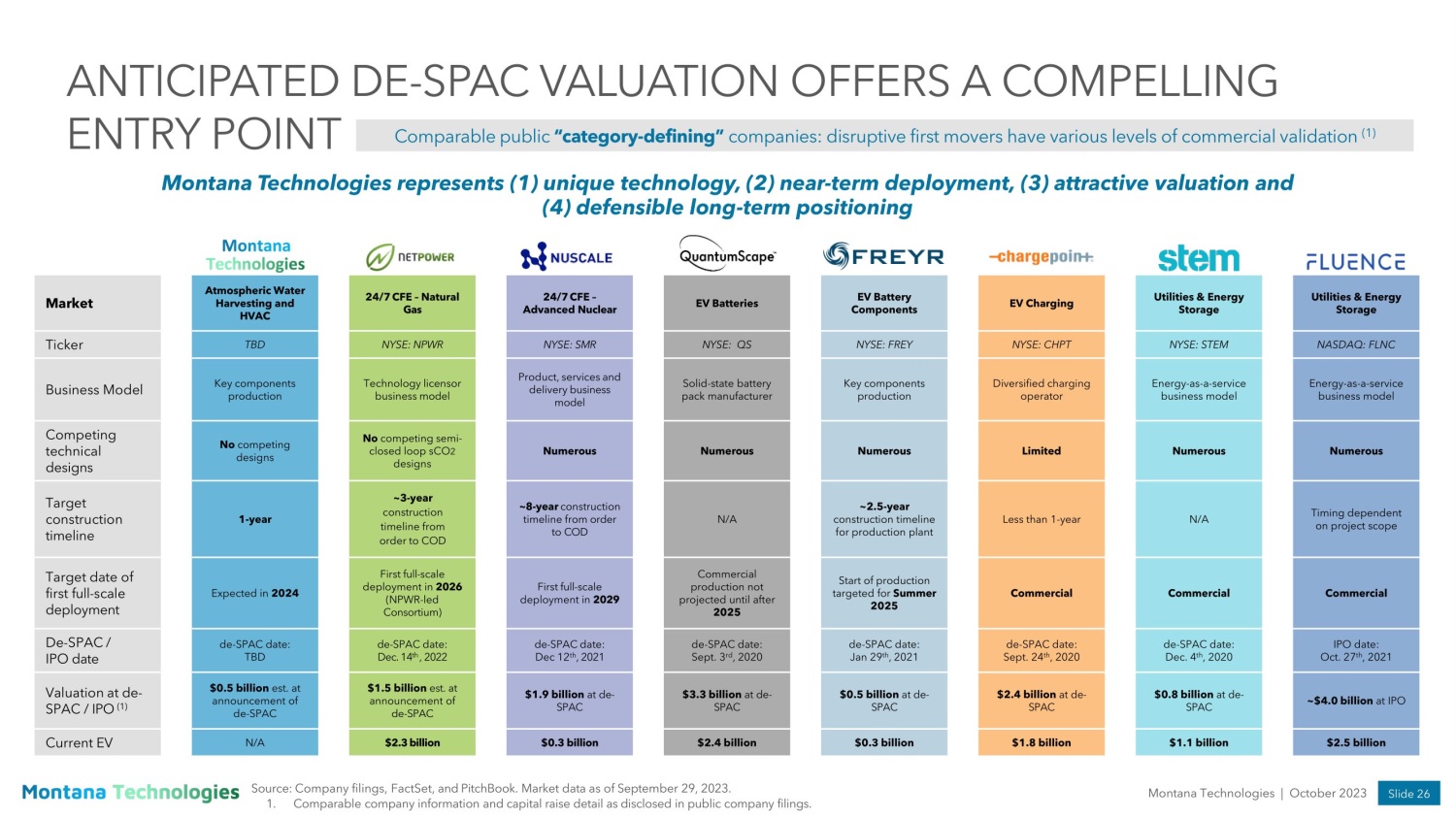

Slide 26 Montana Technologies | October 2023 Utilities & Energy Storage Utilities & Energy Storage EV Charging EV Battery Components EV Batteries 24/7 CFE – Advanced Nuclear 24/7 CFE – Natural Gas Atmospheric Water Harvesting and HVAC Market NASDAQ: FLNC NYSE: STEM NYSE: CHPT NYSE: FREY NYSE: QS NYSE: SMR NYSE: NPWR TBD Ticker Energy - as - a - service business model Energy - as - a - service business model Diversified charging operator Key components production Solid - state battery pack manufacturer Product, services and delivery business model Technology licensor business model Key components production Business Model Numerous Numerous Limited Numerous Numerous Numerous No competing semi - closed loop sCO 2 designs No competing designs Competing technical designs Timing dependent on project scope N/A Less than 1 - year ~2.5 - year construction timeline for production plant N/A ~8 - year construction timeline from order to COD ~3 - year construction timeline from order to COD 1 - year Target construction timeline Commercial Commercial Commercial Start of production targeted for Summer 2025 Commercial production not projected until after 2025 First full - scale deployment in 2029 First full - scale deployment in 2026 (NPWR - led Consortium) Expected in 2024 Target date of first full - scale deployment IPO date: Oct. 27 th , 2021 de - SPAC date: Dec. 4 th , 2020 de - SPAC date: Sept. 24 th , 2020 de - SPAC date: Jan 29 th , 2021 de - SPAC date: Sept. 3 rd , 2020 de - SPAC date: Dec 12 th , 2021 de - SPAC date: Dec. 14 th , 2022 de - SPAC date: TBD De - SPAC / IPO date ~$4.0 billion at IPO $0.8 billion at de - SPAC $2.4 billion at de - SPAC $0.5 billion at de - SPAC $3.3 billion at de - SPAC $1.9 billion at de - SPAC $1.5 billion est. at announcement of de - SPAC $0.5 billion est. at announcement of de - SPAC Valuation at de - SPAC / IPO (1) $2.5 billion $1.1 billion $1.8 billion $0.3 billion $2.4 billion $0.3 billion $2.3 billion N/A Current EV ANTICIPATED DE - SPAC VALUATION OFFERS A COMPELLING ENTRY POINT Source: Company filings, FactSet, and PitchBook. Market data as of September 29, 2023. 1. Comparable company information and capital raise detail as disclosed in public company filings. Montana Technologies represents (1) unique technology, (2) near - term deployment, (3) attractive valuation and (4) defensible long - term positioning Comparable public “category - defining” companies: disruptive first movers have various levels of commercial validation (1)

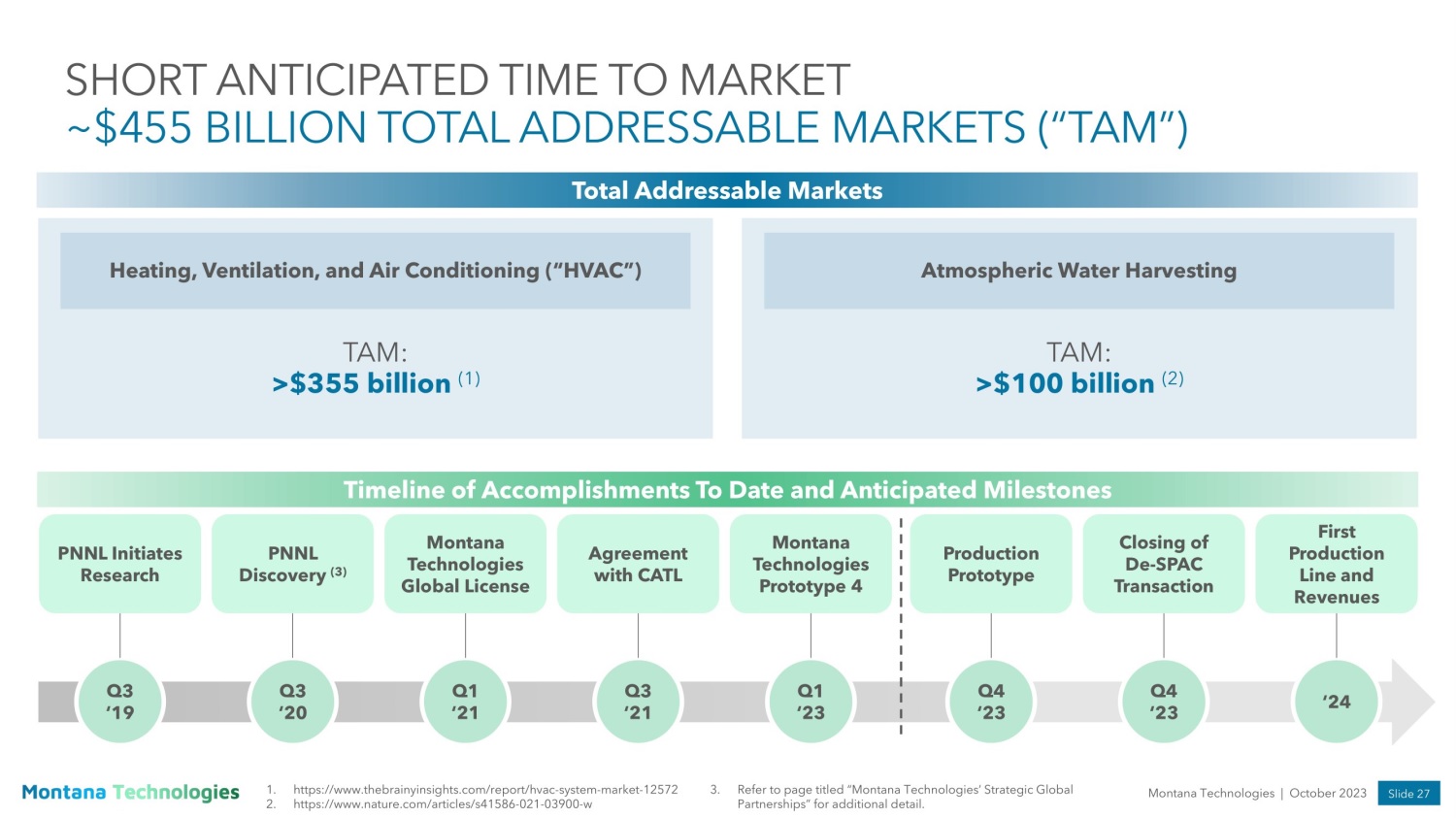

Slide 27 Montana Technologies | October 2023 TAM: >$355 billion (1) TAM: >$100 billion (2) Heating, Ventilation, and Air Conditioning (“HVAC”) Atmospheric Water Harvesting SHORT ANTICIPATED TIME TO MARKET ~$455 BILLION TOTAL ADDRESSABLE MARKETS (“TAM”) Q3 ‘19 ‘24 Q4 ‘23 Q1 ‘21 Total Addressable Markets PNNL Initiates Research PNNL Discovery (3) Montana Technologies Global License Agreement with CATL Montana Technologies Prototype 4 Production Prototype Closing of De - SPAC Transaction First Production Line and Revenues Timeline of Accomplishments To Date and Anticipated Milestones Q3 ‘20 Q1 ‘23 Q4 ‘23 Q3 ‘21 1. https:/ /w w w.thebrainyinsights.com/report/hvac - system - market - 12572 2. https:/ /w w w.nature.com/articles/s41586 - 021 - 03900 - w 3. Refer to page titled “Montana Technologies’ Strategic Global Partnerships” for additional detail.

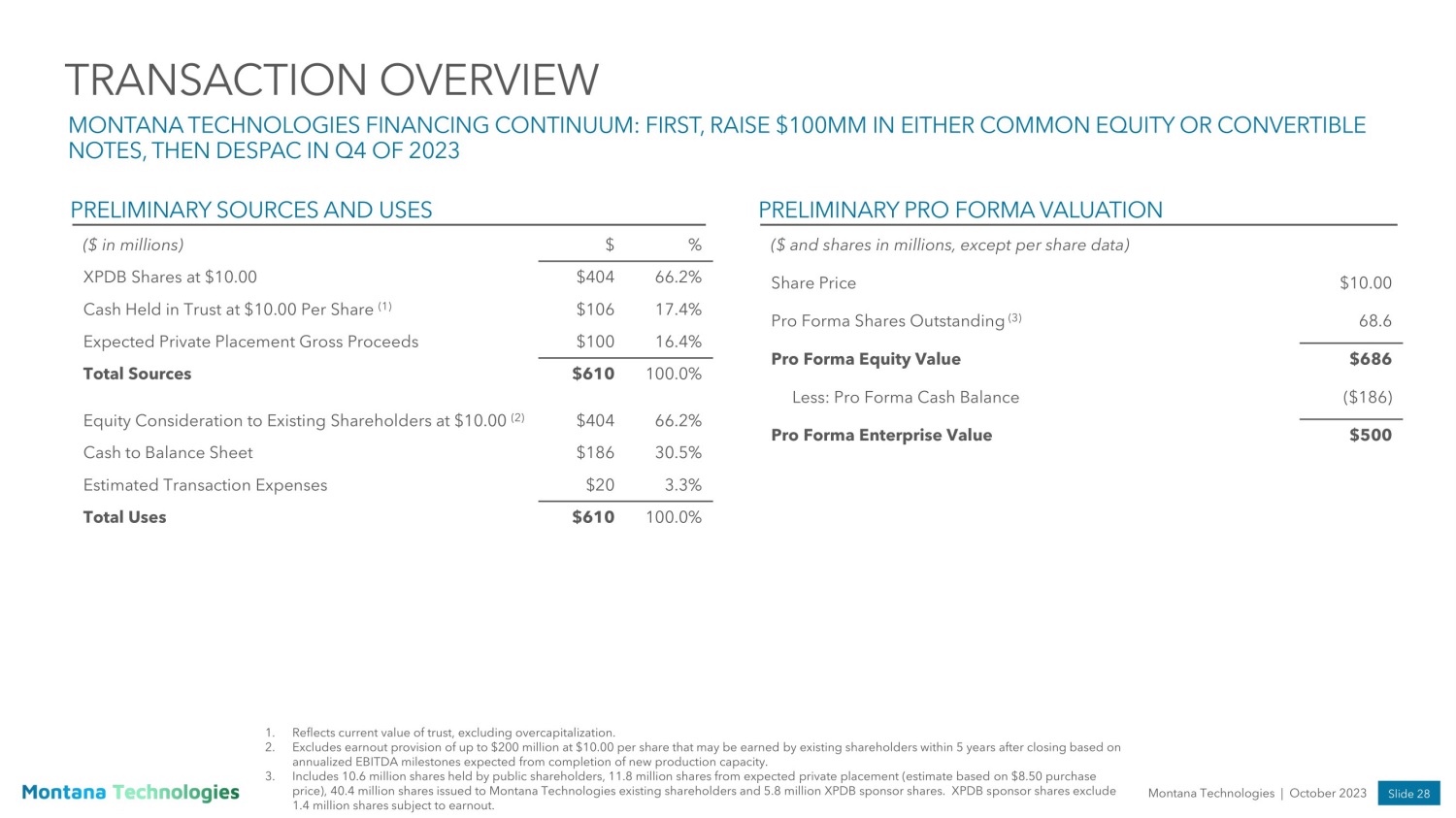

Slide 28 Montana Technologies | October 2023 TRANSACTION OVERVIEW MONTANA TECHNOLOGIES FINANCING CONTINUUM: FIRST, RAISE $100MM IN EITHER COMMON EQUITY OR CONVERTIBLE NOTES, THEN DESPAC IN Q4 OF 2023 PRELIMINARY SOURCES AND USES PRELIMINARY PRO FORMA VALUATION % $ ($ in millions) 66.2% $404 XPDB Shares at $10.00 17.4% $106 Cash Held in Trust at $10.00 Per Share (1) 16.4% $100 Expected Private Placement Gross Proceeds 100.0% $610 Total Sources 66.2% $404 Equity Consideration to Existing Shareholders at $10.00 (2) 30.5% $186 Cash to Balance Sheet 3.3% $20 Estimated Transaction Expenses 100.0% $610 Total Uses ($ and shares in millions, except per share data) $10.00 Share Price 68.6 Pro Forma Shares Outstanding (3) $686 Pro Forma Equity Value ($186) Less: Pro Forma Cash Balance $500 Pro Forma Enterprise Value 1. Reflects current value of trust, excluding overcapitalization. 2. Excludes earnout provision of up to $200 million at $10.00 per share that may be earned by existing shareholders within 5 years after closing based on annualized EBITDA milestones expected from completion of new production capacity. 3. Includes 10.6 million shares held by public shareholders, 11.8 million shares from expected private placement (estimate based on $8.50 purchase price), 40.4 million shares issued to Montana Technologies existing shareholders and 5.8 million XPDB sponsor shares. XPDB sponsor shares exclude 1.4 million shares subject to earnout.

Slide 29 Montana Technologies | October 2023 INVESTMENT HIGHLIGHTS • Transformational Technology: 5 – 10x energy reduction, air - to - water and HVAC solutions – Applications across dehumidification, atmospheric water generation and evaporative cooling help solve two of the world’s most problematic issues: demand for energy - efficient HVAC and water stress • Leading Partnerships: – Partnerships help accelerate manufacturing of materials and components as well as provide product validation and commercialization • Capital Efficient and Highly Scalable Business Model: <$50 million capex investment expected to generate ~$100 million EBITDA per line – Montana Technologies expects to self - fund future production lines through capital - efficient production • Large Addressable Market: >$100 billion air - to - water and $355 billion HVAC markets – Scaling to base case production lines would represent a de minimis proportion of the ~$455 billion market • Key Components Plan: Deliver proprietary technology for OEM assembly – MOF - coated contactors to be sold in combination with air pumps, vacuum compressors and water vapor condensers • Strong Management: Team supported by some of the nation’s leading scientists in this area – Combined 140+ years of experience across commercialization, finance, operations and research

APPENDIX Appendix

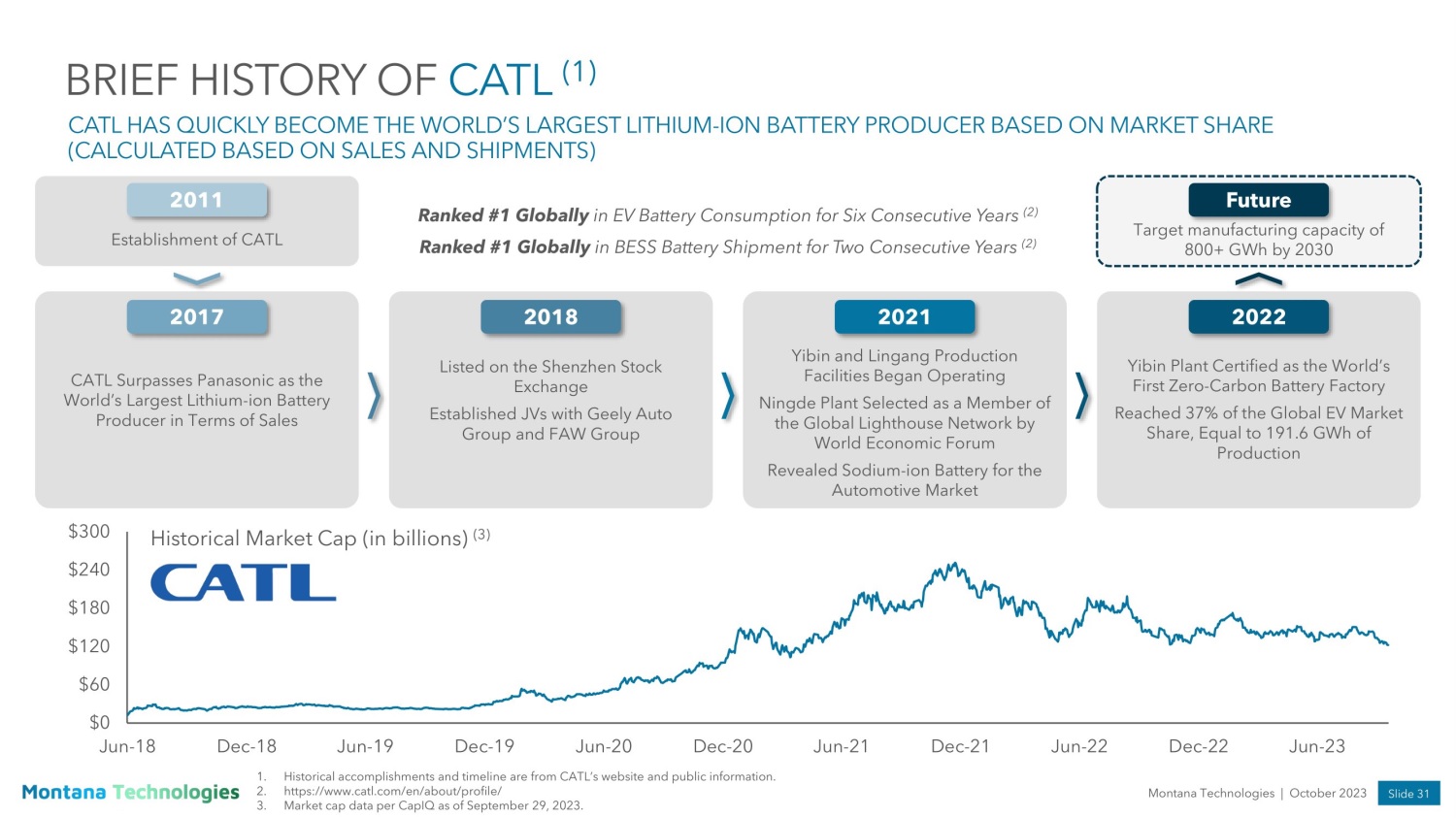

Slide 31 Dec - 22 Jun - 23 Montana Technologies | October 2023 BRIEF HISTORY OF CATL (1) CATL HAS QUICKLY BECOME THE WORLD’S LARGEST LITHIUM - ION BATTERY PRODUCER BASED ON MARKET SHARE (CALCULATED BASED ON SALES AND SHIPMENTS) $300 $240 $180 $120 $60 $0 Jun - 18 Dec - 18 Jun - 19 Dec - 19 Jun - 20 Dec - 20 1. Historical accomplishments and timeline are from CATL’s website and public information. 2. http s://w ww.c atl.com/en/about/profile/ 3. Market cap data per CapIQ as of September 29, 2023. Jun - 21 Dec - 21 Jun - 22 Historical Market Cap (in billions) (3) CATL Surpasses Panasonic as the World’s Largest Lithium - ion Battery Producer in Terms of Sales 2021 Yibin and Lingang Production Facilities Began Operating Ningde Plant Selected as a Member of the Global Lighthouse Network by World Economic Forum Revealed Sodium - ion Battery for the Automotive Market 2011 Establishment of CATL Listed on the Shenzhen Stock Exchange Established JVs with Geely Auto Group and FAW Group Yibin Plant Certified as the World’s First Zero - Carbon Battery Factory Reached 37% of the Global EV Market Share, Equal to 191.6 GWh of Production 2017 2018 2022 Future Target manufacturing capacity of 800+ GWh by 2030 Ranked #1 Globally in EV Battery Consumption for Six Consecutive Years (2) Ranked #1 Globally in BESS Battery Shipment for Two Consecutive Years (2)

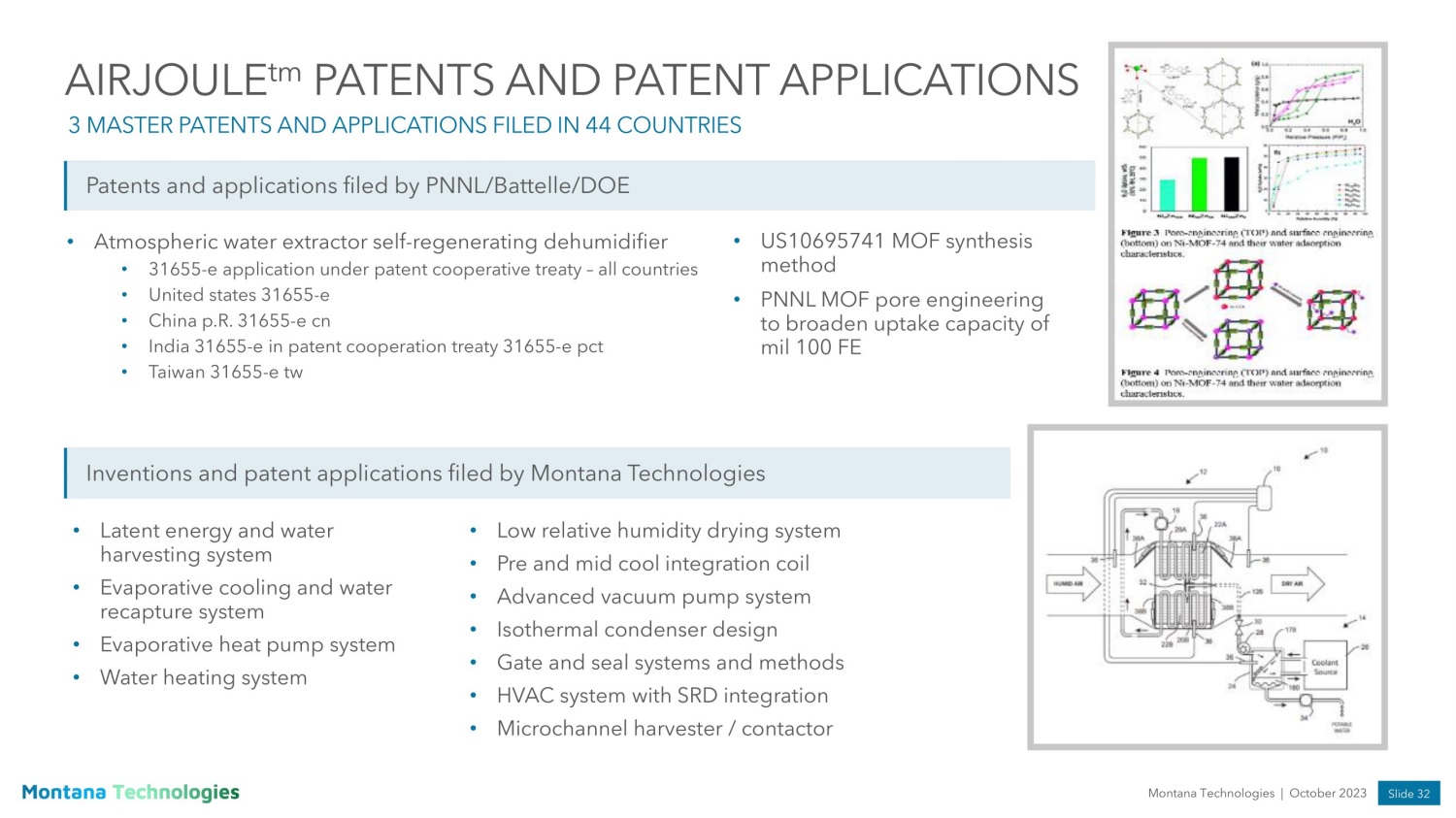

Slide 32 Montana Technologies | October 2023 • Atmospheric water extractor self - regenerating dehumidifier • 31655 - e application under patent cooperative treaty – all countries • United states 31655 - e • China p.R. 31655 - e cn • India 31655 - e in patent cooperation treaty 31655 - e pct • Taiwan 31655 - e tw AIRJOULE tm PATENTS AND PATENT APPLICATIONS 3 MASTER PATENTS AND APPLICATIONS FILED IN 44 COUNTRIES Patents and applications filed by PNNL/Battelle/DOE Inventions and patent applications filed by Montana Technologies • Latent energy and water harvesting system • Evaporative cooling and water recapture system • Evaporative heat pump system • Water heating system • Low relative humidity drying system • Pre and mid cool integration coil • Advanced vacuum pump system • Isothermal condenser design • Gate and seal systems and methods • HVAC system with SRD integration • Microchannel harvester / contactor • US10695741 MOF synthesis method • PNNL MOF pore engineering to broaden uptake capacity of mil 100 FE

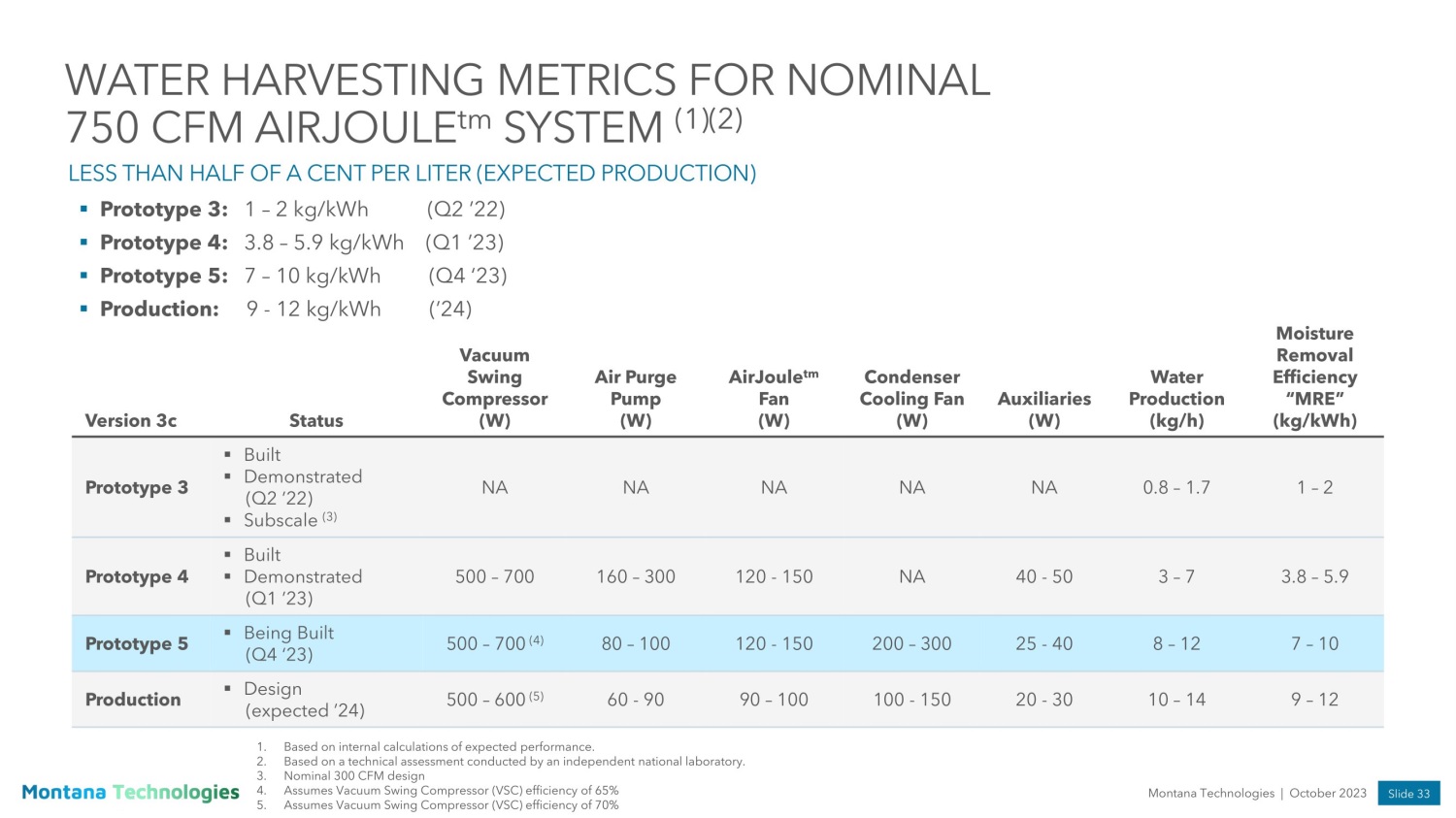

Slide 33 Montana Technologies | October 2023 WATER HARVESTING METRICS FOR NOMINAL 750 CFM AIRJOULE tm SYSTEM (1)(2) LESS THAN HALF OF A CENT PER LITER (EXPECTED PRODUCTION) Moisture Removal Efficiency “MRE” (kg/kWh) Water Production (kg/h) Auxiliaries (W) Condenser Cooling Fan (W) AirJoule tm Fan (W) Air Purge Pump (W) Vacuum Swing Compressor (W) Status Version 3c 1 – 2 0.8 – 1.7 NA NA NA NA NA ▪ Built ▪ Demonstrated (Q2 ’22) ▪ Subscale (3) Prototype 3 3.8 – 5.9 3 – 7 40 - 50 NA 120 - 150 160 – 300 500 – 700 ▪ Built ▪ Demonstrated (Q1 ’23) Prototype 4 7 – 10 8 – 12 25 - 40 200 – 300 120 - 150 80 – 100 500 – 700 (4) ▪ Being Built (Q4 ‘23) Prototype 5 9 – 12 10 – 14 20 - 30 100 - 150 90 – 100 60 - 90 500 – 600 (5) ▪ Design (expected ’24) Production (Q2 ’22) 1 – 2 kg/kWh ▪ Prototype 3: (Q1 ’23) 3.8 – 5.9 kg/kWh ▪ Prototype 4: (Q4 ‘23) 7 – 10 kg/kWh ▪ Prototype 5: (’24) 9 - 12 kg/kWh ▪ Production: 1. Based on internal calculations of expected performance. 2. Based on a technical assessment conducted by an independent national laboratory. 3. Nominal 300 CFM design 4. Assumes Vacuum Swing Compressor (VSC) efficiency of 65% 5. Assumes Vacuum Swing Compressor (VSC) efficiency of 70%

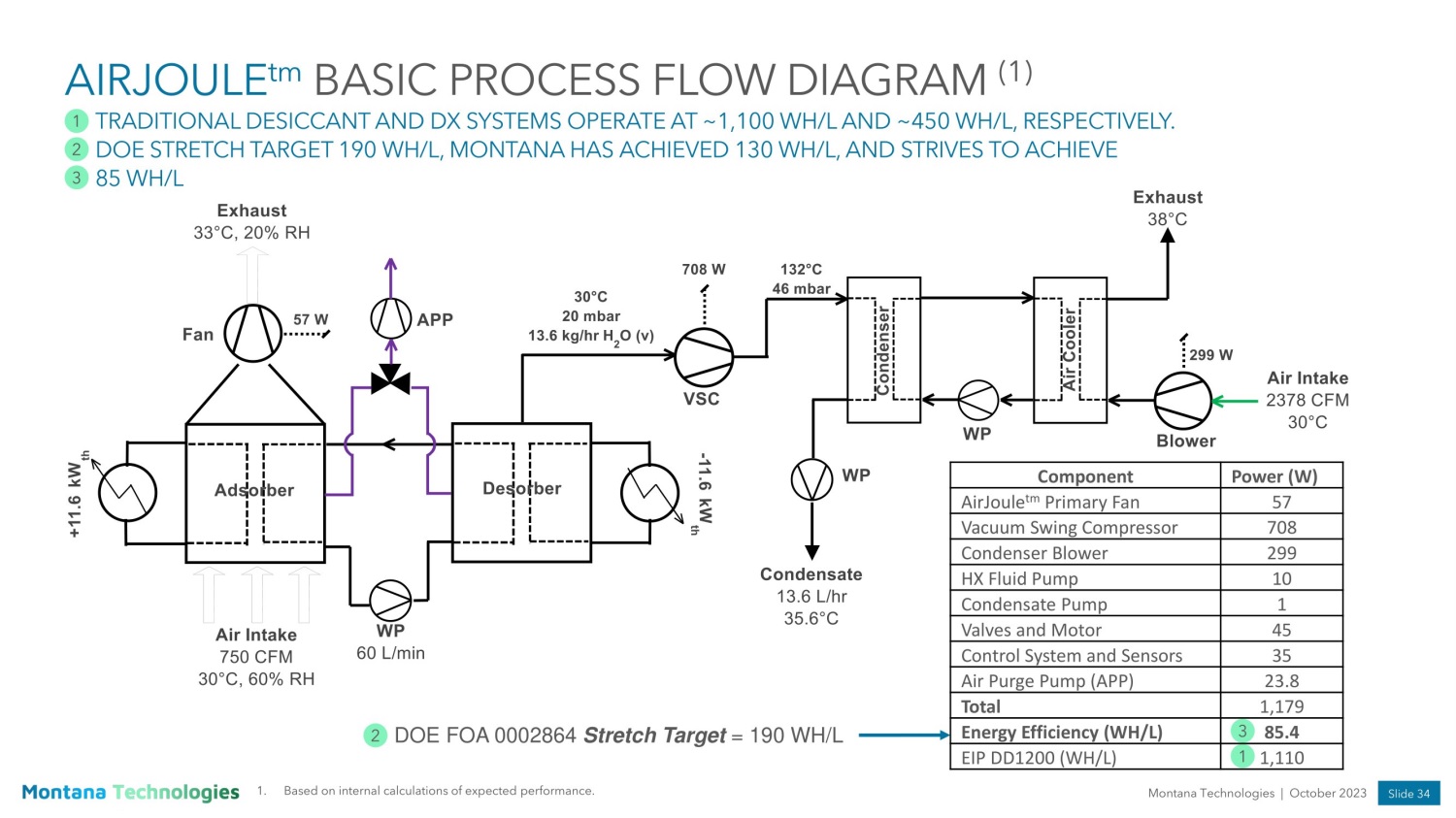

Slide 34 Montana Technologies | October 2023 1. Based on internal calculations of expected performance. AIRJOULE tm BASIC PROCESS FLOW DIAGRAM (1) TRADITIONAL DESICCANT AND DX SYSTEMS OPERATE AT ~1,100 WH/L AND ~450 WH/L, RESPECTIVELY. DOE STRETCH TARGET 190 WH/L, MONTANA HAS ACHIEVED 130 WH/L, AND STRIVES TO ACHIEVE 85 WH/L DOE FOA 0002864 Stretch Target = 190 WH/L 1 2 3 Power (W) Component 57 AirJoule tm Primary Fan 708 Vacuum Swing Compressor 299 Condenser Blower 10 HX Fluid Pump 1 Condensate Pump 45 Valves and Motor 35 Control System and Sensors 23.8 Air Purge Pump (APP) 1,179 Total 3 85.4 Energy Efficiency (WH/L) 1 1,110 EIP DD1200 (WH/L) 2

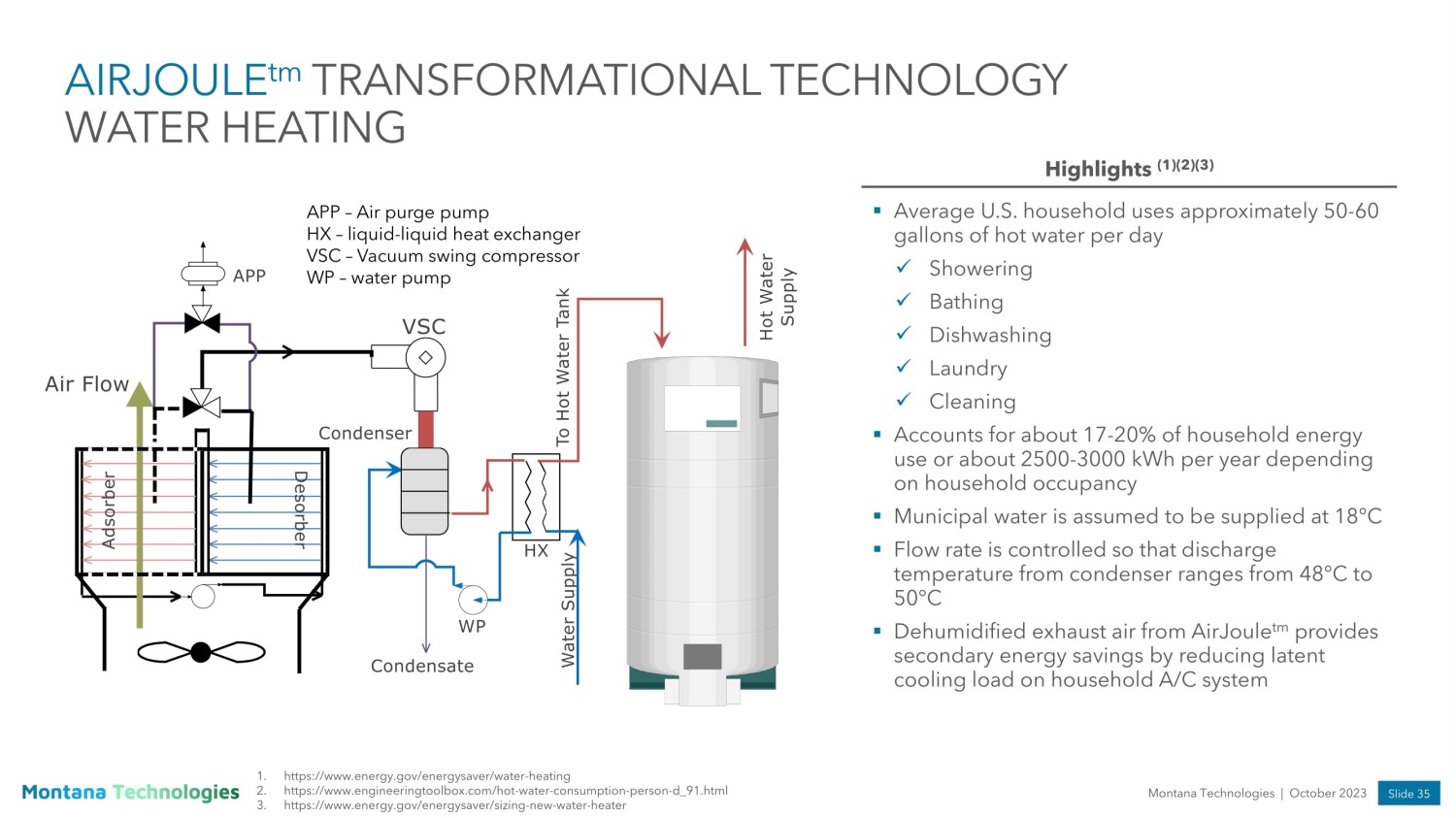

Slide 35 Montana Technologies | October 2023 1. http s://w ww. energy.gov/energysaver/water - heating 2. http s://w ww. engin e eringtoolbox.com/hot - water - consumption - person - d_91.html 3. https:/ /w w w.energy.gov/energysaver/sizing - new - water - heater AIRJOULE tm TRANSFORMATIONAL TECHNOLOGY WATER HEATING APP – Air purge pump HX – liquid - liquid heat exchanger VSC – Vacuum swing compressor WP – water pump Highlights (1)(2)(3) ▪ Average U.S. household uses approximately 50 - 60 gallons of hot water per day x Showering x Bathing x Dishwashing x Laundry x Cleaning ▪ Accounts for about 17 - 20% of household energy use or about 2500 - 3000 kWh per year depending on household occupancy ▪ Municipal water is assumed to be supplied at 18 Σ C ▪ Flow rate is controlled so that discharge temperature from condenser ranges from 48 Σ C to 50 Σ C ▪ Dehumidified exhaust air from AirJoule tm provides secondary energy savings by reducing latent cooling load on household A/C system

Slide 36 Montana Technologies | October 2023 3 1 2 AIRJOULE tm TRANSFORMATIONAL TECHNOLOGY WATER HEATING ENERGY CONSUMPTION (COP) (1)(2) AirJoule tm Water Heater Value Component Vacuum Pump 15 Intake Pressure (mbar) 2.1 Compression Ratio 31.5 Discharge Pressure (mbar) 146 Discharge Temperature ( Σ C) 150 Power Consumption (W) Condenser 50 Vapor Side Pressure Drop (Pa) - 118 Vapor Side T ( Σ C) 1.9 Cooling Duty (kW th ) 5 Condenser WP1 Power (W) AirJoule tm Fan 8.2 Efficiency (CFM/W) 24 Power Consumption (W) Coolant Exchange Pump 6 Flow Rate (L/min) 6 Power Consumption (W) Condensate Pump 2.4 Flow Rate (L/hr) 2 Power Consumption (W) Water Supply Pump 5 Power Consumption (W) Valves, Door Motor, Control System Electronics 65 Power Consumption (W) 9 Air Purge Pump 0.27 Total Power Consumption (kW e ) 1.90 Heating Power Delivered (kW th ) 7.1 AirJoule tm Water Heater COP WATER HEATERS WITH: ELECTRIC RESISTIVE ELEMENTS AND HEAT PUMPS, HAVE A COP OF 1.0 AND 3.2, RESPECTIVELY. AIRJOULE tm WATER HEATERS ARE EXPECTED TO HAVE AN AVERAGE COP OF 7.1 Electric Element COP =1.0 DX Heat Pump COP = 3.2 AirJoule tm Water Heater Diagram AirJoule tm COP = 7.1 1 2 3 1. Based on internal calculations of expected performance. 2. http s://w ww.d eppmann.com/blog/monday - morning - minutes/heat - pump - water - heaters - capacity - cop - weather - part - 8/